Comparing Your Net Worth

Do you ever wonder what others are doing with their finances and where they stand? My usual, rather pessimistic, thought is that I’m not doing nearly as well as my peers.

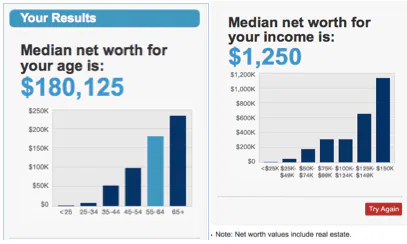

I came across this calculator on CNN Money that gave a median net worth comparison for income and age. My income is pretty low at $24,000 and I entered this amount and my age – 60 and this was the result.

My net worth is in the $700,000 range, but before I start congratulating myself I realize that this compares the net worth of US residents. Canadians must be better savers. After all, I always read about Boomers with $5-million residences and portfolios in the seven figures, so now I feel I’m falling extremely short.

Related: Fun with calculators (and other online financial resources)

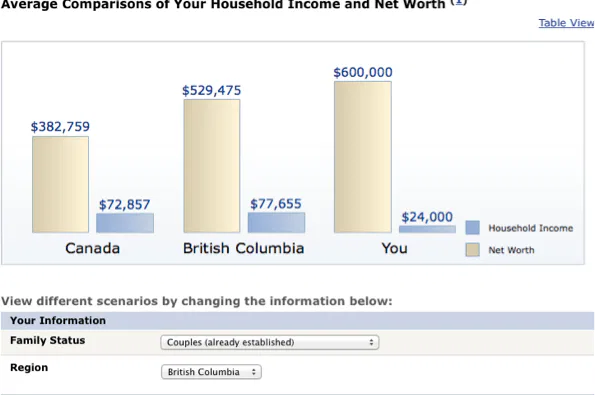

I found another net worth comparison calculator from the Royal Bank that give me this result:

So What?

We all like to compare ourselves to what others are doing, especially in financial matters, where our conversations are vague and we always want to sound smart and on top of our money.

We’re curious about what the benchmark – or median – is. But, really, these types of calculators and comparisons are useless because there is no other context. Everyone is different and has different circumstances.

Related: Why age-based savings benchmarks are dumb, but we look anyway

Assets only have the value that you give to them. Some people might be thrilled to have the above-mentioned $180,000. Then there are others that worry themselves sick because they don’t think several million dollars is enough.

Final thoughts

Having a comfortable life has less to do with how much wealth you have stored up and more to do with your state of mind. How much do you need to maintain a comfortable lifestyle? The “magic number” is going to be different for everyone depending on chosen lifestyle, spending, and priorities.

You only get meaningful data by calculating your own net worth at least annually, and comparing the results with your previous information. Your annual review can help you measure the progress of your financial plan. It helps to keep you on track and stay focused on achieving your own vision. You then have a choice of whether you’re willing to make any necessary changes.

What do you think of these net worth comparison calculators?

I’m in the camp that worries. If there’s one thing I know it’s that money always finds a way to spend itself and without a massive stockpile I don’t know if I’ll ever be comfortable enough to relax about my finances.

I enjoy using those calculators to see what the “average” person is doing. But I take them with a grain of salt because they’re not telling me how well we’re doing for where we want to be.

I use these as a general guideline. Everyone’s scenario is different so it’s rather hard to gauge what “average” means. Having said that if your net worth is lower than the average then maybe this is a warning light.

As an artist, I wish I could find a calculator or set of figures that allowed me to compare my financial situation to that of my peers. For me there’s no point in trying to keep up with what someone working on Bay Street or in civil service job is doing.

@Trevor

Might I suggest trying http://www.networthshare.com? I use it to track my own progress and compare to others in the same profession/income/age group. It’s free, easy, and doesn’t require you to provide any sensitive personal information.

I don’t worry about keeping up with my peers or use calculator’s. I know I’m a late starter to saving. I tell you who ruin it for me for using calculator’s, it was my bank. They drilled it into me that I was way below the national chart. Well guess what I will be pulling out of that bank in July 2019. I don’t think they had a right to tell me I’m not keeping up with my peers. Thanks for the posting

Calculators like this are interesting but this is where it ends for me. I prefer to focus on what I can do/what we can do with our goals vs. comparison studies.

My generation is going to need at least $1 M in invested assets to retire on comfortably so I have to keep my head down and focus on that 🙂

I don’t mind comparing to my peers. Since I am a proud type it sometimes gives me motivation to go forward. I do take all this with a grain of salt though as my circumstances might be a lot different than others (owning a house, having three kids, etc.)

As others have already said, I don’t see much value in these comparisons either. Whether you feel great by comparing yourself to the “average poor person” or get depressed that you can’t keep up to the “average rich person”, the whole metric seems to boil you down to a net-worth number that is 100% arbitrary to your real worth as a person or family.

Two parents who spend a lot on private education for their children, or work less and volunteer more in the community, may have a lower net worth than a single person who is a heavy saver. Neither lifestyle is wrong, but their priorities are totally different and the net-worth “number” will reflect those priorities.

I agree with the benefits Marie wrote about keeping track of your own net-worth year-over-year. I’m all for growing wealth, but not just so I can say I have a bigger number than someone else.

We have retired and put our RRIF’s, TFSA and other savings into high interest saving accounts. We are not making much interest, but we are frugal. High MER’s were draining our mutual funds and our understanding of the stock market was vague. The financial planner at our bank suggested that we put it into long term GIC’s that were attached to the market and equity mutual funds. He said we would never lose our principal with the GIC, so we decided a savings account would work the same way.

Everytime I see one of these “comparison tools” I have to laugh at my situation. I, like a lot of other newcomers to Canada, just have no way to compare with the average Canadian or American, so I just giggle and keep living my life. And I am fine, thanks 🙂

I think one has to define what “comfortable lifestyle” means.

Thank you for the post! A lot of things to think about here!

I love checking out these calculators for fun, but that’s it. It is just for fun. Like others mentioned, there are a lot of things the calculators don’t take into consideration. My wife and I had to pay for our own school, which is not cheap by the way. We both graduated with some debt and starting jobs are not always well paid. Because of co-op, I didn’t graduate 2-3 years after my peers, but it did help pay for a good chunk of my tuition and school expenses. It took us another year just to get to a positive net worth.

But I assume there are a lot of other people our age who had their school paid for and their parents helped them get on their feet after graduation, and boost the average net worth for our age bracket.

I must agree with you ‘Young Millennial’. I know of a few families that not only paid for their children’s education, but let them stay at home rent free while they worked and got a down payment for their first homes which was matched by their parents. They are debt and mortgage free. Not sure what they have learned about life though. It sounds like you have it all together. You appreciate what you earn more than what is handed out to you on a sliver platter.

I’ve got one in the works which will use the age range of the household and the net worth, and give a percentage quantile. Most of the places I’ve seen net worth broken down in greater detail seem to be more academic papers, but most of the consumer sites seem to concentrate on the median.

Unfortunately, it will also suffer from the United States bias…