Converting Your RRSP To A RRIF At Questrade

Many investors like to take the reins and self-manage their own investment portfolio using a discount brokerage platform. DIY investing can be relatively straightforward during your contribution years, but investing can get more complicated when it comes time to withdraw from your portfolio. This article will explain the steps involved in converting your RRSP to a RRIF using the Questrade platform (know that the process should be similar across discount brokerage platforms).

Before we get into the details, here's a quick guide to Registered Retirement Income Funds:

RRIF Basics

A Registered Retirement Income Fund (RRIF) is a way to convert your RRSP into an income stream. You can open a RRIF at any time, but you must convert your RRSP to a RRIF by the end of the year you turn 71.

Once your RRSP has been converted to a RRIF you must begin withdrawals by the next calendar year. There's a minimum mandatory withdrawal schedule that you must follow, which increases every year.

The withdrawal formula for those 70 and under is calculated as 1/(90 – age). For example, a 65-year-old must withdraw a minimum of 4% (1/90-65).

The minimum withdrawal amount is based on the value of your RRIF on December 31 of the previous year. Again, our 65-year-old investor who has a RRIF balance of $425,000 as of December 31 last year would need to withdraw a minimum of $17,000 (4% of $425,000) by the end of this year.

The minimum RRIF withdrawal at age 71 is 5.28%.

As a RRIF holder you must follow the minimum withdrawal schedule, but know that there is no maximum limit to how much you can withdraw in a given year (whether you want to withdraw more is another story).

Investors can continue to invest their funds inside a RRIF in the same way they invested inside their RRSP.

RRIF Tips To Consider

Minimum required withdrawals from a RRIF will not be subject to withholding taxes from your financial institution. Withdrawals from your RRSP are immediately subject to withholding tax of 10% to 30%, depending on the amount withdrawn. Of course, RRIF withdrawals are still considered taxable income so plan your cash flow accordingly for tax time.

RRIF withdrawals at age 65 qualify as eligible pension income. This allows the recipient to claim the Pension Income Tax Credit (a non-refundable tax credit of up to $2,000). RRIF withdrawals at 65 and older are also eligible for pension splitting with your spouse.

Lump sum withdrawals from an RRSP are not considered eligible pension income and does not qualify for the Pension Income Tax Credit. RRSP withdrawals cannot be split with a spouse.

Some financial institutions charge what's called a partial de-registration fee to withdraw funds from an RRSP (the fee can be as high as $50 per withdrawal). Withdrawals from a RRIF plan are typically done fee-free.

Many retirees convert their RRSP to a RRIF well before the mandatory age of 71 to take advantage of the above benefits. Know that you can hold more than one RRIF. You can convert a small portion of your RRSP to a RRIF to take advantage of the Pension Income Tax Credit while keeping the remainder of your RRSP intact until age 71.

One retirement income strategy that is becoming more popular is to withdraw from an RRSP or RRIF to meet your spending needs in your 60s and then defer taking CPP until age 70 to lock-in a 42% enhancement to your government benefits.

Converting Your RRSP To A RRIF At Questrade

With the RRIF basics and tips out of the way, let's look at exactly how a DIY investor can convert their RRSP to a RRIF on their own.

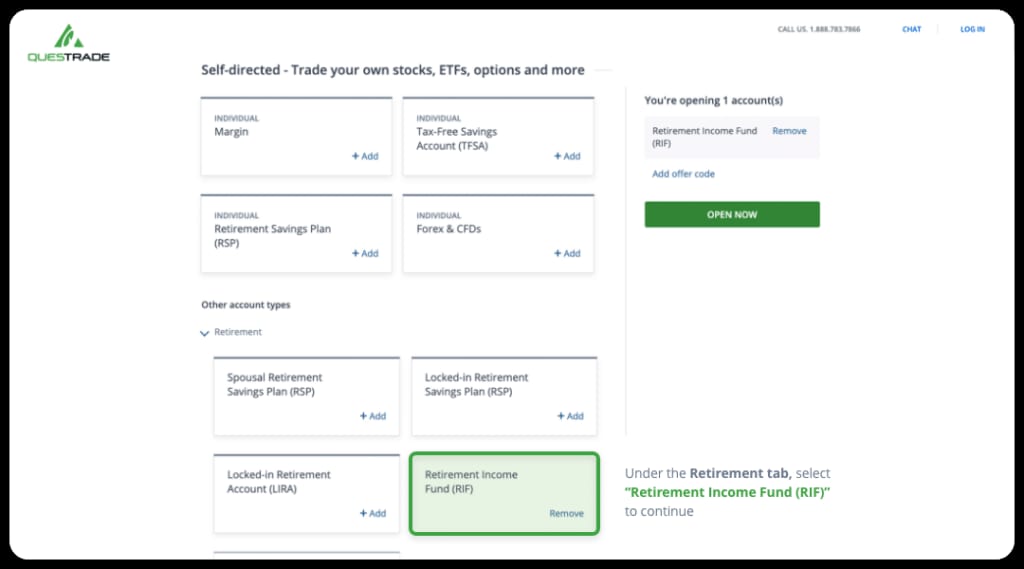

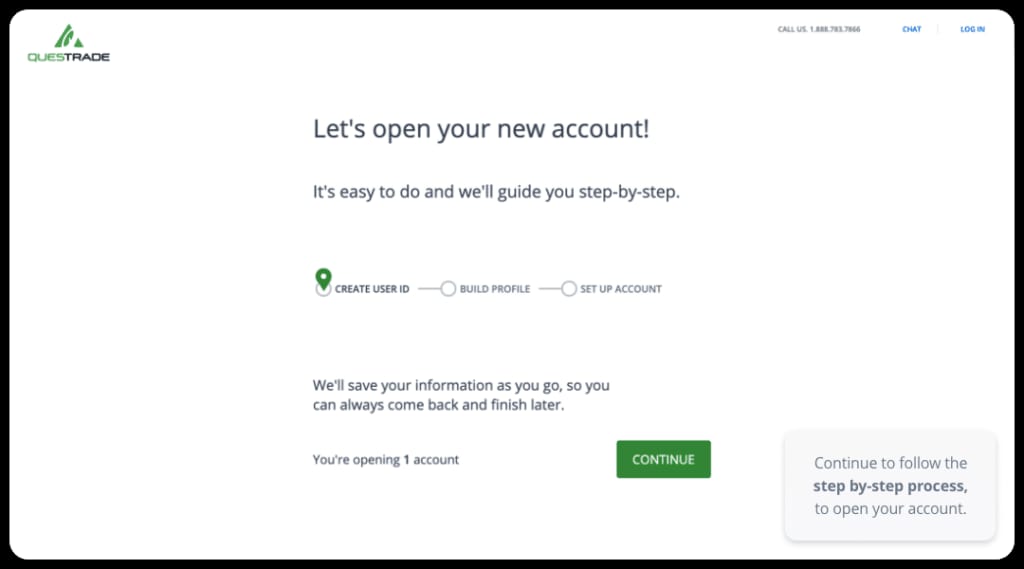

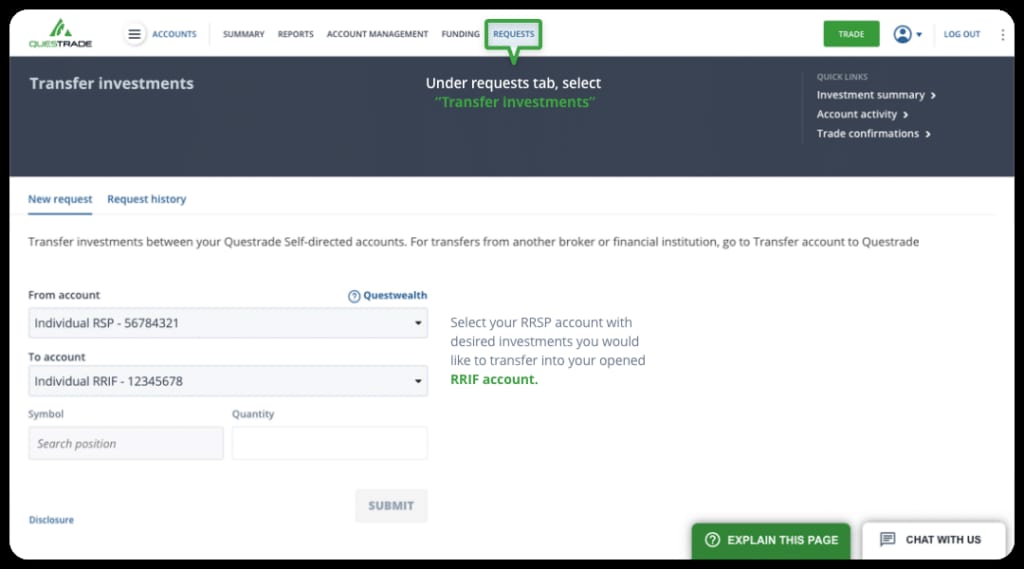

The process of converting your RRSP to an RRIF at Questrade is quite simple and only requires three steps:

1.) Open an RRIF at Questrade (you’ll be asked to confirm payment details as part of the account application process to ensure your RRIF payments will be processed correctly).

2.) Transfer the holdings of your RRSP to the new RRIF account (the rollover process takes 3-4 business days, and you won’t be able to trade during that time).

3.) Start receiving your RRIF payments

Questrade has a team of customer service agents to help if you need assistance. I've personally found the online chat feature to be helpful if you don't want to wait on hold.

If a customer hasn’t opened their RRIF and rolled over their assets by December of the calendar year they turn 71, then Questrade will automatically open the RRIF and complete this process for them – all at no additional cost. To re-iterate, there is no mandatory minimum withdrawal in the year the RRSP is converted to a RRIF, but there are mandatory minimum withdrawals beginning the next calendar year.

When it comes to converting a Locked-In Retirement Account (LIRA) to a Life Income Fund (LIF), the process is almost identical, except that you open a LIF from the account opening screen instead of a RRIF.

Final Thoughts

Many self-directed investors are confused about converting their RRSP to a RRIF. They want to know if they can do it themselves, or if the process is automatic. They want to know if it's possible to convert an RRSP to a RRIF prior to age 71, and why it would make sense to do so.

Hopefully this article has shed some light on how easy it is for DIY investors to convert their RRSP to a RRIF using the Questrade platform, or any other discount brokerage platform.

Good explanation Robb. Can I assume if the RRSP was held at another bank, I could transfer to a Questrade RRIF?

Thanks

Greg

Hi Greg, indeed just like any other account type you could open a RRIF at Questrade and then transfer a RRIF or RRSP from another financial institution to your new Questrade RRIF.

What you really need to talk about is a practical strategy for converting the right amounts to cash when withdrawals are made from the RRIF. Perhaps a follow-up article?

Hi Karen, that would be interesting. I can definitely look into some different approaches for how to structure your investments inside a RRIF so you can easily make your minimum withdrawals.

A few months ago, when I tried to convert my RRSP to a RRIF at Questrade, I found that it was anything but easy. I had to deal with several different people and it was a hassle.

Hi Jerry, sorry to hear that. Was there a specific issue that made things difficult for you?

There were multiple issues. My memory is getting a bit fuzzy about the whole process but the difficulties I experienced setting up my RRIF shook my confidence in Questrade to the core. Here’s one of the emails I sent to Questrade: “I want to convert my RRSP held at Questrade into an RRIF held at Questrade. When I log in, none of the 4 funding options suggested to me seem to apply to this situation. What exactly should I do?” There were a total of 14 emails exchanged between me and several different Questrade employees, and I believe there may have been phone calls and chat sessions too, but as I mentioned already, my memory is getting a bit fuzzy at this point. All of this happened four and a half months ago.

If it gives you any comfort, this process is not much easier with iTrade. Transferring in from another account is absolutely painful and involved many contacts with multiple people. We manage most of our RRIFs and LIFs but you have to be savvy to do so.

My wife converted her LIRA to a LIF, immediately transferring 50% of the LIF to a Manitoba Prescribed RRIF (PRIF). At the same time, she had to advise them of her desired withdrawal amount. The process was not what I would call straight forward or easy, but we got there in the end. The process and rules pertaining to the LIRA and PRIF were too much for dealing with via the chat, so we put everything she wanted to do in a letter and sent it to Questrade- that helped move things along.

Can you do an article on the strategy of using RRSP/RRIF to fund retirement to deferring CPP to 65 or 70. I have seen this strategy alot and understand it however by the calcuation for CPP end up with 42% for waiting to 65, it isn’t addressed the CPP rule avg and their backing out worst 7 years in the calculaton. My fear is by waiting to 65 and retiring at age 60 that 5 years with no YMPE pd would negate the .6% per month increase for every month deferred collecting. I have seen no one address this.

Hi Scott, there’s good research on deferring CPP until 70 to secure more lifetime retirement income. See this article and the research paper linked inside: https://boomerandecho.com/weekend-reading-100000-lifetime-loss-of-cpp-edition/

To your specific question about retiring early and having more “zero” contribution years, know that the age credit for deferring CPP is great than the penalty of having another zero contribution year.

As pension expert Doug Runchey says, “you’ll get a bigger slice of a smaller pie by waiting, but you’ll always get more pie.”

You can run your own estimates (including manually entering future zero years if retiring early) at http://www.cppcalculator.com.

The calculator didn’t fully cover our situation, so we engaged Doug Runchey to run our CPP numbers. I was pleased with the results, including getting a better understanding of how those zero years did indeed have an impact. Between the ages of 60 and 65, the annual gain was less each year we delayed, to the point where, without adjusting for inflation, at age 83 the better option was to start CPP at 64 instead of 65. With a little bit of inflation thrown into the mix, this switches around, but then when you throw in conservative gains on investments not used in the earlier start at age 64, it’s almost a wash for us.

One caveat with Doug’s calculations is that he only guarantees them to be 99.9% accurate 🙂

My plan is to cash out my RRSP before it needs to be turned into a RIF. There’s enough in my RSP to buy a nice used car. Interesting Jerry says this was a hassle at Questrade. The transfer process might be one of these things that looks simple on paper, but the reality of executing it – not so much.

Hi Robb. Some of our funds were “locked in”, as they dated back to DC pensions in past careers. It would be helpful (in a future article) to explain a) that locked in funds must be directed to a LIF b) that LIF’s have minimums and maximums c) there are different maximums depending on the province of origin. For example, I have a LIF (from a position in a federally regulated business) that resides in Ontario. The maximums are lower than that in my own province. Thanks.

Thanks for that tip !! I am jumping on this right away as I am using RSP funds currently. I can’t split that income and I am missing out on the 2K credit !! Excellent financial assistance from you Robb. I will open RIF and move some of my money asap.

“Many retirees convert their RRSP to a RRIF well before the mandatory age of 71 to take advantage of the above benefits”…. If converted before the mandatory age of 71, do you have to take out any minimum amount every year between the age of 65 to 71 ? Or it could be any amount you want to withdraw depending on your circumstances.

Another (silly) question but good to know the answer. When converted to RRIF or LIF,….

(A) In case of over 71 years, do you have to withdraw a certain amount every month ? Or you can withdraw once a year whatever you need to withdraw for that year.

(B) same question if you are between 65 to 71 years

If the withdrawal formula for those 70 and under is calculated as 1/(90 – age), what is the formula over 70 because when you are 89 the entire amount is paid out (1/1). Can not find the information on the CRA site.

Thanks

Hi Bill, that’s the formula for calculating minimum mandatory withdrawals prior to age 71. The percentages slow down from 71-95 and cap out at 20% of the balance at 95.

Thanks Robb, found the table on the CRA site. Looking at the impacts of time and income to reduce taxes.

Can you set up a RRIF before 65

Yes you can Jim. I converted my RSP to RIF when I retired at 63 100 % as the funds in it provide my

retirement income to supplement CPP and OAS. You can do partial conversion to RIF and keep the rest of the RSP until you turn 71 by which time you have to convert all your RSP to RIF or Annuity.

I too held my RRSP at Questrade and transferred it to a Questrade RRIF, and the process was not quite as simple as they made it sound – although still not particularly onerous. I had excellent help from the Chat Desk once we figured out what the problem was (it took several tries for that!) As I recall, the issue was around the actual transfer of RRSP funds to RRIF, it wasn’t a straight transfer but (I think) a withdrawal and funding. This is one area where Questrade can put some additional details into their instructions. PS, the withdrawal process is simple, I have the minimum transferred monthly into my Questrade Margin Account and just have to keep an eye on the cash balance held in the RRIF.

A couple of years back I converted my RRSP to RRIF in my QTrade account, and it was quite easy, even though I was quite concerned that it would be done correctly. And QTrade will do it automatically (just like Questtrade) if I didn”t do the conversion by the required time. On the Canada Revenue site as well as in my QTrade account is listed the amount I have to withdraw each year.

And by the way, I took my Canada Pension as soon as I turned 65 for the very good reason that I might not be around in later years. I have enjoyed the money coming in every month since!

I’d love to see more information about how you manage a self-directed RRIF. Can you transfer only a portion of an RRSP into an RRIF? The screenshots look like it has to be the whole account. And then what happens? How do you control which investments are liquidated for the payments…or can you control that? I don’t want to see x% taken from each of my investments periodically, regardless of whether they are up or down at the time.

It’s really hard to find this information anywhere!

Prior to your mandatory RRSP to RRIF conversion date you can do a partial conversion. If you later find that you don’t need the income, say, because you go back to work, you can convert the RRIF back into an RRSP. Having not done a partial conversion or conversion back to an RRSP myself, I can’t say how you do this in Questrade. Knowing what you can or can’t do is half the battle.

Prior to the scheduled withdrawal date, annually in our case, we sell equity and bond ETFs so as to maintain our desired target asset allocation for the account. You can also allow the dividend payouts to accumulate and top up the cash at the appropriate time with the sale of the equity and bond ETFs. Questrade told me that if they have to sell the assets to cover the scheduled payout, there is a charge of $45.

For our entire portfolio (ie all accounts combined) we have five years worth of fixed income, the rest being in equities, and as there is a cap on how much can be withdrawn annually from a LIF, we only hold five years of maximum withdrawals in bonds in the LIF. If we went to 100% bonds in the LIF we would be short on accessible fixed income in our other accounts if indeed we needed to use the full five-year fixed income buffer. That was my thought process anyway.

Commentating on my own comment here! Thinking about this a little more, if I did go 100% bonds in the LIF and running short on fixed income, say by year three after the mother of all stock crashes, I could in effect swap out the stock in the RRSP for the bonds (or cash) locked in the LIF ie sell as needed the stock in the RRSP, sell the corresponding value of bonds in the LIF, and buy the stock back in the LIF. I think that would do it.

Just when you think you’ve got it, another twist or idea comes along.

Hi Bob, it’s good to get these thoughts out on paper (computer?) and wrestle with them.

This is why I shy away from asset location and prefer to hold the same mix across all accounts. It gets complicated enough when trying to rebalance or add new contributions across various accounts and keep things in line. I can’t imagine the frustration when you’re making withdrawals from different accounts while trying to maintain your asset location mix.

That said, I get that if you’ve already designed your portfolio this way it can be difficult to change approaches.

I hear what you say Robb. On one hand, I would like things to be simpler, while on the other, I enjoy optimizing and keeping costs to a minimum (individual EFTs vs an all-in-one). I doubt that my strategy brings significant gains over the alternative, but with travel still being limited for now, I have the time.

As per your suggestion, I recommend the simpler approach to family members, along with providing links to the best blogs, yours obviously included.

Not clear on how the amount coming out of a riff account is atually taken out or receiveed from the new riff account. Does one have to make the withdrawal or is it transfered to a cash account?

I think Questrade has ?recently? updated several RRIF-related processes.

You can use “Transfer funds” to transfer any amount from RRSP to RRIF.

You can make withdrawals similar to a RRSP withdrawal – using “Withdraw funds”, to your linked chequing account, or with fees by wire transfer.

Here’s an interesting opportunity – there’s a $50 + tax fee to withdraw (partial deregistration) from a RRSP. But no fee from a RRIF. So if you have a RRIF, you can by-pass the fee with a internal transfer RRSP > RRIF, followed by a withdrawal from the RRIF. If you have zero RRIF balance at the beginning of the year, there won’t be any mandatory withdrawal. But you will get the $2k additional “Pension income amount” on line 31400 of your tax return :-).

Can you transfer ‘in kind’ from a RRIF to an unregistered account? That would eliminate the need to sell investments when you might not want to.

That’s what I was planning to do. Instead of (potentially) multiple withdrawals from my RRSP at $50 a pop, I’ll just transfer to a RRIF and withdraw from there for free 😉

However, I don’t think you can claim the $2k pension amount if nothing is withdrawn. The pension amount is “up to” $2k.