Five Year GIC Ladder vs. One-Year Rolling Term: Smackdown

If you have long-term money in GICs, this post is for you. I know, rates are abysmal, and I'm not here to talk you into investing in mutual funds, or ETFs, or to buy bonds directly. If you’re comfortable with GICs, and you can meet your income or capital-preservation goals with them, then keep on keeping on.

Related: Can you succeed with an all-GIC portfolio?

With that little slice of affirmation out of the way, I want you to something for me: think back to the last time that one of your GICs matured. Did you have a conversation – either with your bank representative or with yourself – that went something like this?

The difference between the one or two year rate and the five year rate isn’t that great. Interest rates are going to go up soon. (They certainly can’t get any lower.) I’ll just pick a shorter-term GIC and by the time it matures rates will be higher.

Maybe you've even had that conversation more than once. I’m here to ask you not to have it again. Please, for the love of all that’s holy, keep your GICs in a five-year ladder, renew into another five-year at each maturity, and stop trying to outguess interest rates.

You aren’t doing yourself any favours. Let me demonstrate.

Related: How to create a bond or GIC ladder

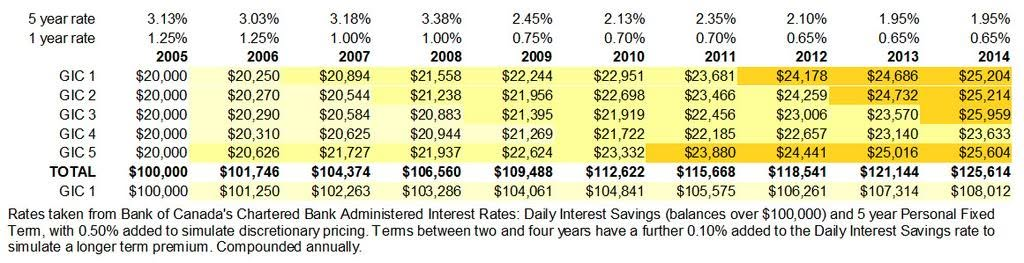

Let’s assume that you had $100,000 to invest in GICs ten year ago. You could either set up a five-year ladder (by breaking it up into $20,000 sections and investing them across one, two, three, four, and five-year term, rolling each into a new five-year term at each maturity), or keep it in successive one-year terms until rates go up enough to make you happy.

The following chart shows the downward progression of rates every year across the top cells and the compounding balance of the two strategies across the bottom, and you can see that the GIC ladder wins handily.

You’d have been ahead by over $17,000 by the end of the decade, just by ignoring what you thought rates were going to do and keeping to a time-worn, boring old strategy like GIC laddering.

GIC rates from 2005-2014

Click to see full chart

But that’s all well and good as rates were going down. Investing in a five-year GIC in 2005 was worth 3.13%. These days we’re staring down the barrel of 1.95%, and you want me to lock that rate in for five years? Interest rates have nowhere to go but up!

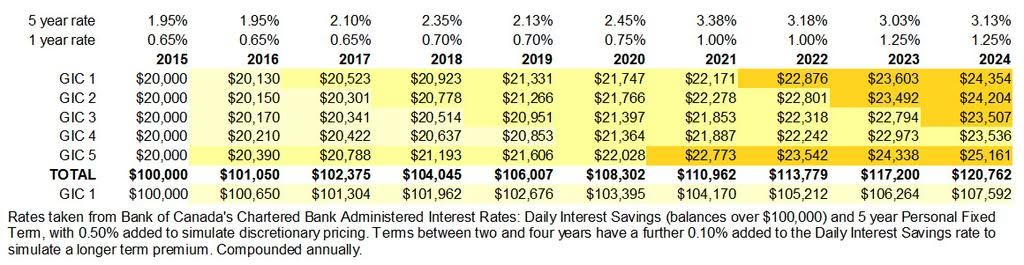

Because I like you, I turned the chart around. Now we’re imagining that rates are going to follow the same slow progression on the way back up over the next ten years, but the choice between ladder or rolling one-year terms is the same.

Hypothetical GIC rates from 2015-2024

Click to see full chart

This time, the GIC ladder wins by $13,000.

I see two emotional biases at work when faced with choices like this: we like the idea of putting off a hard decision until next year when the choices available have to be better than they are this year, and we like to think that interest rates, markets, and economic cycles follow patterns that we can recognize, identify, and use to our advantage because we’re smarter than your average bear.

Related: Should you get a fixed or variable rate mortgage?

But – as in every investing decision – emotions shouldn't enter into the equation. The math holds. So long as a rate premium, however small, is offered for longer terms, the five-year GIC ladder will always win, and so long as longer terms (and GICs) fit your investing purpose, you should always be using a five-year GIC ladder.

Sandi Martin is an ex-banker who left the dark side to start Spring Personal Finance, a one woman fee only financial planning practice based in Gravenhurst, Ontario. She and her husband have three kids under six, none of whom are learning the words to “Fidelity Fiduciary Bank” quickly enough. She takes her clients seriously, but not much else.

Follow-up question: how steep does the rise in rates have to be before playing this game does pay off? To put an order of magnitude on it without making a spreadsheet (why wouldn’t I make a spreadsheet?), you’d have to have rates rise by more than double the current spread by the halfway point, i.e. a ~2.5% increase in rates within ~2.5 years.

Yeah. Why *wouldn’t* you make a spreadsheet?!

You have demonstrated the superiority of a bond ladder over a series of one year GICs, which of course was your goal. But just to play devils advocate for a moment, in both of your examples for this 9 year period a 5 year GIC followed by 4 years of a further 5 year GIC outperforms the ladder. Now of course since people in your example expect rates to rise (which of course is reasonable today)they are unlikely to go long, but I thought the result was interesting and I must say unexpected in the rising rate scenario. Of course if rates rose quickly enough the slight advantage of the long term strategy might disappear.

I like devil’s advocates, and I agree with both you and John that if rates rise rapidly enough the ladder would do worse than the one year rollover…BUT:

How do we know that rates are rising – and will continue to rise – fast enough to make that call? That’s the point that I want regular investors (as in, the ones least likely to make that call correctly, although I don’t have hopes for most of the people advising them or the people advising the advisors) to take away.

I think I’m missing something. If rates continued to fall forever, the appropriate strategy would not be a ladder but a series of 5 year GICs. The problem for this long term strategy kicks in when bond rates rise, as in your second scenario. The result that surprised me was that in the second scenario of rising rates the long term approach(series of 5 year GICs) was still superior to the ladder, which points out that the ladder is superior in a rising rate environment, but only when rates rise quickly enough. By the way, if I were to invest in GICs, I would take the ladder approach you advocate, since I have expectations of rising rates in the future (albeit I don’t know that they’ll rise quickly enough).

Now we’re both confused. What rates would you use to demonstrate that a ladder doesn’t prove out in both falling and rising rate scenarios? Excluding, of course, instances whereby sheerest luck you happen to time your entry exactly right.

To me, the only time a ladder wouldn’t work is if there was either a zero or negative rate premium on terms longer than one year.

Edited: Ah, I’ve reread your question and now I think I see where the confusion lies. In each example the first person only ever has $20K (+ gains) available to reinvest every year, and reinvests it exclusively into another five-year GIC. It’s only in the first year that anything other than a five-year is used, and only to “start the ladder off right” and create it in the first place. Does that make more sense?

Sorry to take so long to respond. I have been having problems accessing this website. At any rate the calculation I did involved simply investing the $100,000 in a 5-yr GIC in 2005 (or in scenario 2: 2015)(at the 5 year rate in the table); then in 2010 (or 2020 in scenario 2) re-investing the GIC proceeds into a further 5 year bond at the 5-yr rate stated in the table in 2010 (or 2020 in scenario 2); and then calculating the value (albeit for only 4 additional years) at 2014(or 2024 in scenario 2). In the first scenario of falling rates I initially invest the $100,000 in a 5-yr bond at 3.13%, which yields $116,600 by 2010. I then roll this into a further 5 year bond in 2010 at 2.13% and after 4 years the total value of the initial investment is $126,921, which of course exceeds the ladder value. I repeat the same exercise in the rising rate scenario and the terminal value ($121.335)also exceeds the terminal ladder value ($120,762). It seems clear why this strategy (rolling 5-year terms) is dominant in the falling rate environment, since I’m alway investing 80% of the money at a higher rate than the ladder. In the rising rate environment I’m sure the result is just an artifact of the numbers, but it was (at least to me) a bit surprising that the 5-yr rolling strategy could yield more in some circumstances even with rising rates than the 5-year ladder. That being said I would think that in the current situation expectations are of rising rates, maybe rising somewhat more quickly than in your table, which would of course favour the 5-yr ladder. I think?

Ah-hah. I see your point, now, thanks.

My recommendation remains, though. The issue isn’t with the math that shows which strategy would have reaped the most reward in the past, although I can see why an argument like mine might allow people to think so, but rather against using our expectations of rate change to determine our strategy going forward.

If we prove that in certain infrequently-occurring rising or falling rate environments that abandoning a ladder would have worked out more optimally in the past, it continues to encourage those investors (and advisors, let’s be honest) who want to believe that *this time* they’ve called it correctly.

It’s the idea of regular people (a category that includes almost all of us, in my opinion) trying to outguess what rates will do and how they’ll do it that worries me

Great post. In my situation,my wife wants to only invest in GIC’s. I have tried to explain ETF’s, stocks. No luck. Our seg funds are losers. So is my financial saleman. This past May I put 10 k in Mawer Balanced Fund. I know its still a mutual fund but I hope its a good one. I don’t want to rant and rant but keep up this great blog.

Sandi, I really like that you backed up your arguments with simple math. The 2 charts perfectly demonstrate what you say and the information was easy to follow.

I keep a significant portion of my portfolio in GIC to be safe and yes, for the last 8 years, I have been renewing 1 year at a time. Each time, I believed that the rates would rebound and rise. They still have not! I will be renewing GIC soon and your article was very timely. Thank you.

Harry, I’m delighted that it was of any use to you at all!

Couldn’t a similar argument be made for why a 1-year fixed rate mortgage beats a 5-year fixed rate mortgage? In this case you’d want to go with the lowest interest rate (1-year) rather than locking into a 5-year term at a premium.

It’s certainly the reason that a variable rate tends to be more optimal than a fixed rate over the long term. (Ha! She used the word optimal!)

I agree, especially in the current environment. I certainly wouldn’t be buying 5 year GIC’s, but some people are. Indeed I had just been talking to friends recently (who were predisposed to safety and thus GICs) and I had suggested to them that if they were going that route they should consider a ladder. I saw your article a few days after this conversation and decided to play with the numbers you presented, and got a result I didn’t expect in the rising rate case. However, if I had a strong belief that rates would be falling substantially at some point in time (as for example in the early 1980’s when interests rose above 18%), I certainly wouldn’t be in a GIC ladder. If I was going to hold a GIC in that case, and I did, it would be a 5 year term, or longer if I could get it. But in the absence of such priors (which are based on an extreme case) and given one is going to invest in GICs, I agree with your premise that the ladder is ‘optimal’ or it is at least the satisficing approach.