I learned how to budget and got my finances under control back in 2009. Up until then I was like most working Canadians; my paycheque would come in, I’d pay some bills, go grocery shopping, maybe transfer some money into savings, and then (over)spend the rest on whatever.

A budget not only helped track my spending to see where exactly my money was going, but it also allowed me to look ahead and plan for future expenses. Let me tell you, having a budget is a lifesaver when you’re going through major events such as a career change, starting a family, or moving to a new house. My budget has been there for me through all of these milestones, and more.

Of course, my financial literacy and money skills have evolved over the years. You might think, why do you still bother with a budget? The truth is I love the feeling of empowerment that comes from budgeting. I can track where my money goes, plan what I’m going to spend in the future, and set-up savings targets to hit throughout the year.

Related: The 50-20-30 Approach To Budgeting

And even though there exists apps like Mint, and tools like YNAB, that claim to make budgeting easier, I still love a good budgeting spreadsheet and continue to use one to this day.

I get a lot of requests to see my Excel budgeting spreadsheet. That’s why I’m making a blank budget template available here for free.

Learn How To Budget – With Excel

What I love about this budgeting spreadsheet is that it uses a zero-based budgeting approach, meaning you assign a job for every dollar that comes in.

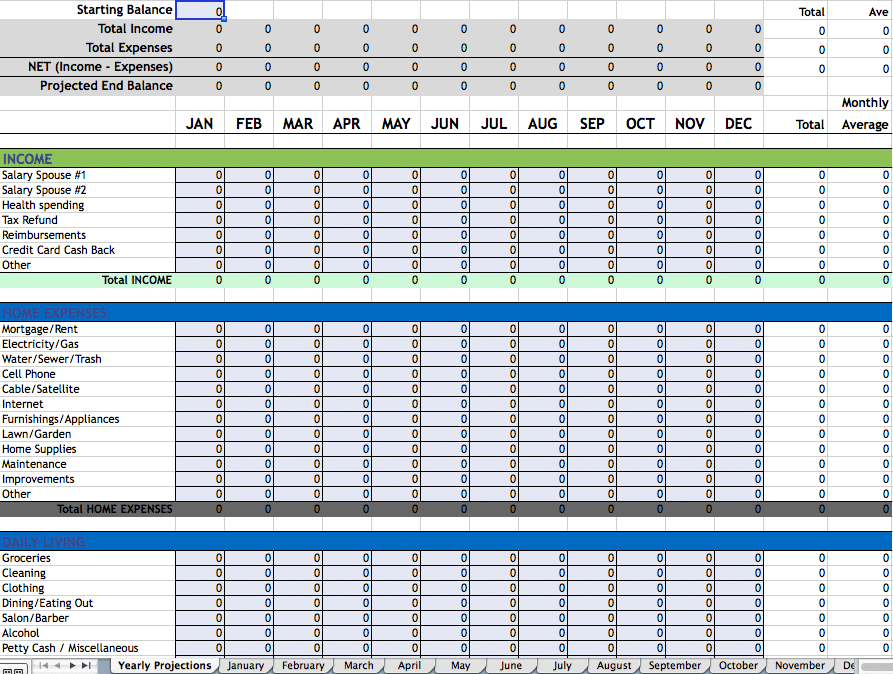

Yearly Projection / Forecast

The first tab is your year-at-a-glance. This is where you enter in your expected monthly salary for the year, plus forecast your monthly expenses. When it comes to salary, I enter the gross amount under income, and then list ALL my deductions (federal and provincial tax, CPP, EI, health & dental, life insurance, plus any pension contributions) under expenses. Remember, we’re accounting for every dollar.

Now, I’ve been at this for nearly 10 years and I like to input my savings goals first (pay yourself first, right?). For example, I might have the following monthly savings goals for this year:

- RRSP – $500.00

- TFSA – $1,000.00

- RESP – $416.66

Then list your known fixed expenses, such as your mortgage payment, property taxes, insurance, cable/internet bill, car payment, that sort of thing.

From there you’ll try to estimate or forecast what you’ll spend on variable expenses such as groceries, dining out, gas, heating & electricity, home repair, and entertainment, to name a few.

Related: Budgeting For Irregular Expenses

With nearly a decade of data I’ve got this down to a science, but if you’re just starting out you’ll have to guess on these for a few months until you begin to see the patterns in your spending.

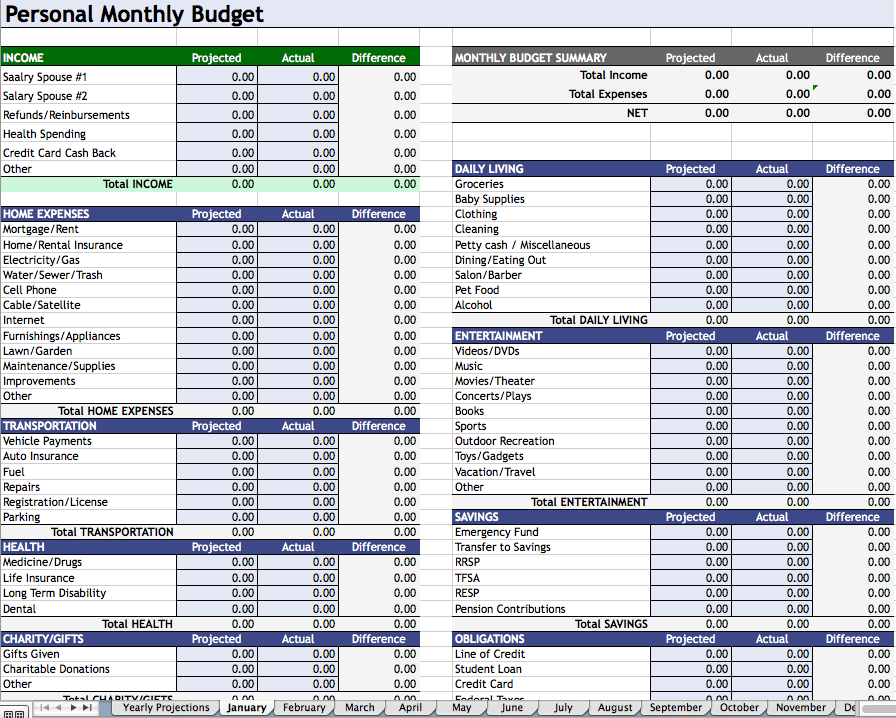

Monthly Budget

The next tab is your monthly budget. This is where you take the numbers from your yearly forecast and plug them into the current month under the “projected” column. This is what you expect to happen with your money this month. Reality is usually quite different. That’s why there’s an “actual” column so you can include the ‘actual’ expenses as they come in.

I’m pretty anal about keeping receipts and so I just enter them into the spreadsheet (under the appropriate category) daily or every other day to stay on top of things.

I tend to have a lot of categories in my budget – we’re a family of four and have a wide variety of expenses. If you find the number of categories overwhelming feel free to pare them down (or combine two or three into a more general category) to suit your budgeting needs.

A Word About Zero-Based Budgeting

The reason I’m a fan of using a zero-based budget is that it allows you to be both flexible and strategic with your dollars. For example, in the year-at-glance tab you will quickly notice that not every month is going to have the same expenses. No, you’ll likely have some vacation expenses in the summer time, and kids’ activities in the fall, and don’t forget to set a budget for Christmas gifts in December.

Related: Why Budgeting Is Not A Waste Of Time

Also, once you’ve paid the maximum into CPP and EI for the year those contributions will stop coming off your paycheque, meaning your net take-home pay will increase. Since we’re assigning a job for every dollar, you can now take those freed-up dollars and assign them elsewhere, perhaps to help meet your savings goals or pay down debt.

Speaking of savings goals, you might not be able to save a specific amount every single month. For instance, even though my goal is to contribute $1,000 per month into my TFSA, it doesn’t always work that way. I put more into my RRSP in January and February, so I actually hold off on my TFSA contributions until March. I’ll still hit $12,000 in contributions for the year, but it won’t be evenly distributed from month-to-month.

That’s the beauty of the zero-based budgeting approach. Using the year-at-a-glance tab I can spot the problem months where my expenses surpass my income and make appropriate adjustments in other months so that everything works out by the end of the year. Right down to the penny.

Final Thoughts

I know it can be hard to stick to a budget. But maybe that’s because we’re doing it wrong. It’s not enough to simply track your expenses. That’s a backward looking solution.

Your budget needs to provide you with actionable intelligence that helps you make better decisions about your future spending.

This budgeting spreadsheet gives you the best of both worlds; a yearly forecast to plan your spending and saving, plus individual monthly tabs to help you keep track of your expenses in the moment.

Now that’s how you budget.