Welcome to the Money Bag, where I answer questions and address comments from readers on a wide range of money topics, myths, and perceptions about money. No question is off limits, so hit me up in the comments section or send me an email about any money topic that’s on your mind.

This edition of the Money Bag answers your questions about cryptocurrency FOMO, selling stocks at a loss, selling stocks at a gain, and comparing your finances to others.

First up is Terri, who wants to know if she should invest a small amount of money in cryptocurrency, given its recent ‘hype’. Take it away, Terri:

Cryptocurrency FOMO

Hi Robb,

I wanted to get your opinion on this crazy cryptocurrency move – I’m sure you’re getting a lot of questions about it. I’m not sold on it as an alternative to fiat currencies or a way to hedge against inflation. To be honest I’m not 100% sure how it works and I don’t think anyone really understands how it derives value. However, it does seem like an opportunity to invest in an asset class in its infancy. Have you done much research into this? I will admit to having some “FOMO” with the recent move, I think I’d like to look into investing a very small portion.

Hi Terri,

I’ll be honest, I heard more about Bitcoin during its last run-up at the end of 2017. That culminated when our 19-year-old restaurant server talked about wanting to buy it with her student loan money. The price proceeded to plummet from nearly $20,000 per coin to about $8,000 in two months and continued down to as low as $3,200 per coin a year later.

So why should this time be any different?

Here’s a bit of background on Bitcoin and Ethereum (the distant number two cryptocurrency):

Bitcoin really only has two uses: a digital currency and a store of value. The primary goal is to establish itself as an alternative monetary system. Like gold, there’s no intrinsic value but its price goes up or down based on public sentiment and speculation. Investors will bid the price up if they believe the demand for Bitcoin will increase, or sell and drive the price down if they believe demand will fall.

Ethereum, on the other hand, is an entire blockchain network that can be used to run decentralized applications, create and enforce smart contracts, and even create additional cryptocurrencies. Ether – the cryptocurrency of Ethereum – can be sent, received, and stored as digital money. It’s used to pay transaction fees on the Ethereum network.

You can buy Bitcoin and/or Ethereum on Wealthsimple Trade (WS Crypto), but the platform is quite a bit different than a traditional crypto trading platform like Coinbase where you actually hold crypto coins in digital wallets. WS Crypto simply allows you to trade the two cryptocurrencies – you don’t get to take hold of any coins in your own digital wallet. These traditional exchanges are prone to major hacks and security breaches. And, if you lose your “key” your coins are lost forever. Not ideal!

All of this said, I don’t recommend speculating on cryptocurrency any more than I’d recommend speculating on gold or other precious metals. Bitcoin is highly volatile, and if you do decide to buy make sure your stake doesn’t make up any more than 2-3% of your portfolio. You can’t hold it in an RRSP or TFSA, so it must be purchased in a taxable account and you track any capital gains or losses associated with buying and selling.

I don’t believe there is an ETF that holds a bunch of different cryptocurrencies. There is The Bitcoin Fund (QBTC) from 3iQ Corp – it comes with a management fee of 1.95%

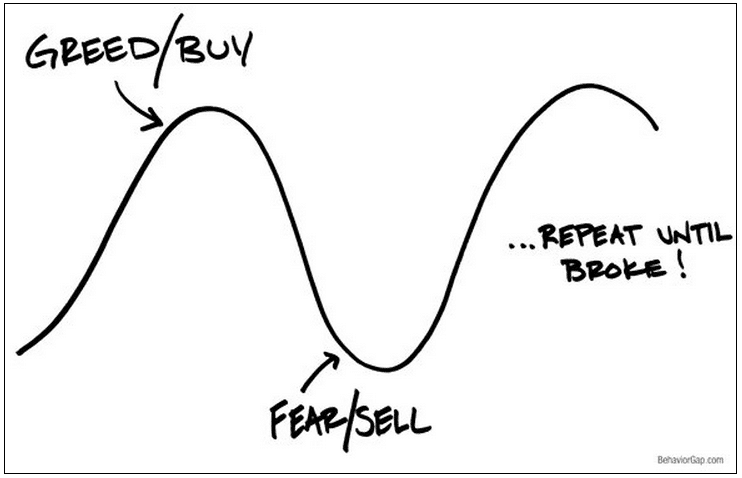

Finally, I’ll leave you with one of my favourite investing charts from Carl Richards, called the Fear and Greed cycle:

All the best!

Selling Stocks at a Loss

Here’s Norm, whose portfolio of individual stocks has taken a beating. He’s wondering when to pull the trigger on switching to a globally diversified index ETF. Sounds familiar:

Hey Robb,

I am planning to switch over my investments to a one-ticket ETF solution (VEQT) in a non-registered account, but I’m wondering about timing. Sadly, my portfolio is down significantly – the original investment of $175,000 is now down to $143,000. It’s largely made up of Canadian dividend payers that includes banks, materials, telecoms and oil stocks. It’s the oil companies that have ravaged the account – with some names down 80%.

I know it’s never a good thing to try to time the market, but I do feel like the banks, materials, and especially the energy sector finally have some tailwinds as the economy starts to reopen and could potentially recoup some of their losses. I wondered about waiting until this time next year, seeing how the portfolio does, and then making the official switch.

Hi Norm, thanks for your email. My advice would be to cut your losses and make the switch as soon as possible. You’ll benefit from the capital loss, which can be carried forward indefinitely to use against a capital gain in future years.

Related: Tax Loss Harvesting Explained

It’s a classic psychological mistake to wait for your losing stocks to come back to even. The stocks don’t care what price you paid for them. Their future prospects may continue to be bleak. Meanwhile, VEQT represents a significantly more diversified and therefore more reliable outcome over the long term.

You’ll still have exposure to all of those sectors, especially given VEQT’s 29% weighting to Canadian stocks.

It hurts to sell something at a big loss. I know, I’ve been there when I used to be a stock picker. It might be helpful to think of your non-registered portfolio as one large lump sum of cash right now. If it were in cash, would you re-purchase the exact same positions that you have now – or would you just buy VEQT? There’s your answer.

Selling Stocks at a Gain (to Rebalance)

Next up is Tracy, who took a chance on some growth stocks last year and now wonders if it’s time to take some profits and rebalance:

Hi Robb,

Last March I took advantage of the COVID dip by purchasing VEQT and some “play” stocks in electric vehicle companies. As a result of the growth in recent months, those “play” stocks now represent a double-digit percentage of my portfolio.

How does one go about rebalancing their portfolio in this scenario? Take out the original amount invested in the stocks (to buy VEQT) and leave the rest in? Leave it all in? Get out of the stocks altogether?

I don’t have much experience with stock investing, and I know you started in stocks, so thought I’d ask.

Hi Tracy, this would first depend on which account type you’re talking about. If in an RRSP or TFSA, I’d say trim your stock holdings by selling off shares to get you back to a comfortable level of “explore” compared to your core.

Yes, the idea would be to rebalance by using those proceeds to buy more VEQT. Set some rules around your stock picking, like no more than 5-10% of your total portfolio value, and then you’ll always have some guidance when to take some profits off the table.

Things are more complicated in a taxable (non-registered) account, as selling any holdings will trigger capital gains for this tax year (2021). You could get closer to your target asset mix by contributing any new money to VEQT only.

Letting your winning stocks ride can be risky as the range of outcomes is much more volatile with one single stock than it is with a globally diversified basket containing thousands of stocks.

Comparing Your Finances to Others

Finally, here’s a question from Peter who seems worried about how his finances are doing compared to his peers:

Hi Robb, I’m a relatively new passive investor, starting Jan 2019, but have been inspired by your timeline and I’m aiming for a goal you had early on: $100k by age 35.

I’m almost 34. My net worth is currently small at $76k. Therefore, my “plan”: save, save, save and at $100k seek out some fee-only advice (most likely yours) to hopefully find what I’m missing and if there are any inefficiencies in my portfolio.

What I didn’t realize until today though, upon reading your “2020 Year-End Review” post, was that at 35 you hit $100k in investments, PLUS you already had a home (purchased three years earlier). As a result, your net worth was MUCH higher than $100k at 35. Suddenly your timeline seems far less achievable…

My questions (finally):

-

- Should this dissuade me / am I on the right track?

- Does a home-purchase “before it’s too late” and then restarting my investment growth after that make any sense, especially considering I don’t really want or need a house currently?

- Does my “plan” make sense considering my late start to saving/investing?

Hi Peter, thanks for your email. I don’t think it’s useful to compare your situation to others. Everyone gets out of the starting gate at different times and with different circumstances that are largely out of their control.

Focus on your short- and long-term goals and strive to keep the needle moving forward each year. You can’t do everything all at once, so prioritize what’s important to you and make adjustments to those priorities as you move forward.

There’s nothing wrong with renting while you grow your investments. Renting offers flexibility and affordability, which can’t be understated.

If your employer offers a matching program, be sure to take full advantage of it. Make sure you’re investing the money in your TFSA rather than just keeping it in cash (if it is intended for long-term growth). Focus on increasing your savings rate each year. The milestones will come.

My finances were a mess in my 20s. I used my late 20s / early 30s to get them cleaned up and start saving. But I largely benefited from a sudden surge in real estate prices on my first home (from $129k to $239k in just a few years), which gave us some breathing room.

I changed careers to a slightly higher paying job that required less travel and was more of a 9-5. That freedom allowed me to start blogging, freelance writing, and eventually doing financial plans. The income earned from these side hustles significantly accelerated our savings goals.

My point is, don’t get bogged down looking at age-based savings goals. Focus on what you can control and keep improving each year. You’ll get there.

Best of luck!

Do you have a money-related question for me? Hit me up in the comments below or send me an email.