Welcome to the Money Bag, where I answer questions and address comments from readers on a wide range of money topics, myths, and perceptions about money. No question is off limits, so hit me up in the comments section or send me an email about any money topic that’s on your mind.

This edition of the Money Bag answers your questions about moving investments to Questrade, investing in energy stocks, government bailouts, and managing investments during uncertain times.

First up is Lisa, who would like to move her investments to Questrade to lower her investment costs and take control of her portfolio. Take it away, Lisa:

Moving to Questrade

“Hi Robb, my investments are currently held in mutual funds at one of the big banks. I’m tired of paying fees, and want to take control of my own portfolio by opening a self-directed account at Questrade.

Can you tell me how to move my RRSP and TFSA investment accounts over to Questrade? Do I need to speak with my current advisor?”

Hi Lisa, first of all, know that you don’t need to break up with your current financial advisor or even speak to him or her at all. Simply open an RRSP and TFSA account at Questrade, request the transfer, and they’ll initiate the transfer for you.

Here’s what I mean:

- Go to Questrade

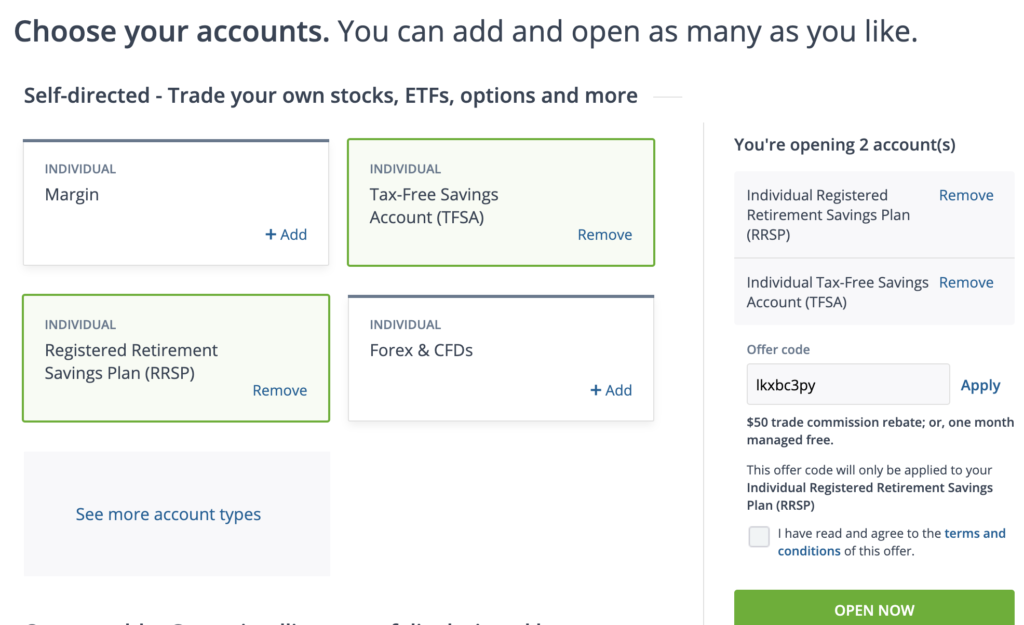

- Click “Open an Account”

- Select ‘TFSA’ and ‘RRSP’

Click ‘Open Now’

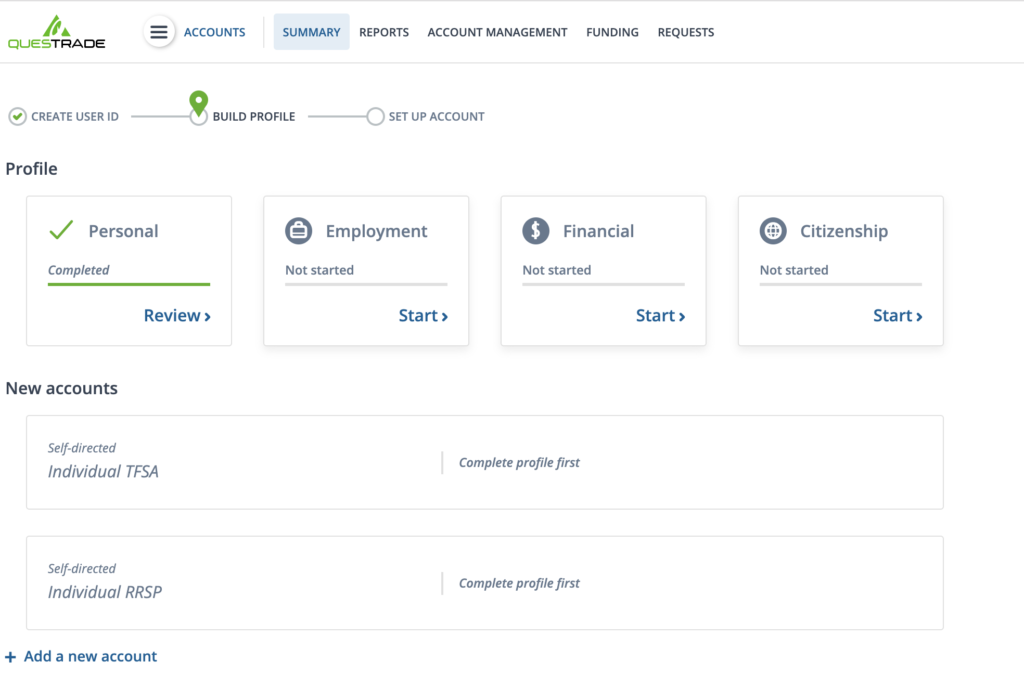

It’ll ask you to create a user ID and profile. Fill out your name, email, and phone number, and click ‘Continue’.

Create a user ID and password.

Once you’ve set up your individual profile and get to the main dashboard, you’ll want to click on ‘Account Management’ at the top of the screen:

- Then click ‘Upload Documents’

- Complete all fields. For Document type, select ‘Rebate’

- Click ‘Upload’

Questrade will even rebate any transfer fees charged from your current financial institution up to $150. To get your fee rebate, send a copy of the statement from your financial institution showing the transfer fee you were charged within 60 days of submitting your transfer request to Questrade.

One important note: As we covered in the last edition of the Money Bag, there are two types of account transfers.

- An in-kind transfer means your investments move over from your current institution to Questrade exactly as is.

- An in-cash transfer has your financial institution liquidate your investments and send Questrade the cash.

Another important note: Assuming you are transferring an account such as an RRSP or TFSA, the transfer will happen within those tax-sheltered containers. Meaning, there will be no tax implications at all. You’re simply moving money to another institution – you’re NOT making an RRSP or TFSA withdrawal.

That’s it. Questrade will initiate the transfer and you’ll have the money within two weeks or so (banks are slow at transferring).

Use my referral link to open your Questrade account. I’ll get a small commission, and you’ll get $50 in free trades.

Investing in Energy Stocks

Next up is Jeremy, who wants to take a flyer on some energy stocks and wonders about the best way to make this investment:

Hi Robb, I have a question. I would like to buy some energy stocks with some money I have sitting around. What is the cheapest, best way to do this?

I am aware of how energy stocks have done and I am also not a stock picker and believe in broad based investing. This is just a small amount of money and I am going to take a flyer on just a few energy stocks.

Hi Jeremy, I don’t advocate for buying individual stocks, and even if I did I’m not sure energy stocks would be at the top of my list. The past five years have not been kind to energy stocks compared to the broad market.

Vanguard’s energy ETF (VDE) is down 61.39 percent over the last five years. Meanwhile the S&P 500, despite its recent turmoil, is up 31.74 percent in that same period.

That said, I can’t begrudge an investor who wants to bet a small portion of his portfolio on individual companies or sectors. As long as it’s money you can afford to lose.

I get the appeal. It doesn’t take a huge stretch of the imagination to see a future where oil prices return to their previous highs.

Individual energy stocks:

Let’s say you want to take 5 percent of your portfolio and invest in energy stocks. A number of dividend paying energy stocks look attractive with yields above 8 percent (i.e. Canadian Natural Resources, Enbridge, Suncor).

Be careful about chasing high dividend yielding stocks. The company may choose to reduce, suspend, or eliminate its dividend, a move which often sends share prices down.

A safer bet might be to look at energy stocks whose price-to-earnings ratio has fallen. These stocks may or may not pay a dividend, so investors would be betting on share prices returning to their former oil-boom glory. Cenovus and Imperial Oil would fit the bill.

Energy ETFs:

How should you invest in energy with little money? Instead of picking one or two individual stocks, the smart play might be to invest in an ETF that tracks the energy sector.

There’s the iShares ETF called XEG. This ETF aims to track the performance of the S&P/TSX Capped Energy Index. If you want to invest in Canadian energy, this isn’t a bad way to do it.

This ETF, like the entire energy sector, has gotten killed over the past five years, but still has net assets of more than $426M. XEG also pays an attractive distribution of 5.6 percent. It comes with a MER of 0.61 percent, which is expensive compared to broad market ETFs but is a reasonably cheap way to invest in 22 Canadian oil and gas companies with just one fund.

Or, look at a similar ETF such as BMO’s Equal Weight Oil & Gas Index ETF (ZEO). It holds 11 large-cap oil companies using an equal weighted approach, rather than XEG’s market-cap weighting. It charges the same MER of 0.61 percent. ZEO’s concentrated approach has led to better returns than XEG, but it’s still down 66 percent over the past five years.

The most cost-effective way to invest in either energy stocks or ETFs is to open a self-directed investing account at either Questrade – which offers free ETF purchases – or with Wealthsimple Trade, a mobile-trading platform that offers zero-commission stock and ETF trading.

Unintended Consequences from Government Bailouts

Wilson would like to know what I think about the unintended consequences of government stimulus during this COVID-19 crisis:

Hi Robb, what are your thoughts on the massive amounts of government bailouts in both the U.S. and Canada? There are people like Ray Dalio and Charlie Munger who suggest that while it may be necessary, the end result is the rich get richer and the wealth gap widens, not to mention inflation, etc.

Ray Dalio was suggesting some kind of paradigm shift coming even before this pandemic.

Hi Wilson. That’s a tough question. In short, I’m in favour of governments doing everything possible to hand out stimulus to individuals and small businesses to help them through this crisis. It must be done, and it must be done quickly.

In fact, I’d be in favour of sending every single person a stimulus cheque, regardless of their circumstances, until the crisis subsides. We can sort out the consequences later, at tax time next year, by clawing back up to 100 percent of the stimulus for those who earn over a certain threshold.

*Note: Here’s a really good argument for why sending everyone a stimulus cheque would not be faster and would not actually reach everyone.

Central banks have proven they can keep inflation under control. Critics thought the massive amount of stimulus injected into the economy during the 2008 financial crisis would lead to hyper-inflation – but that never happened.

I do agree that the wealth-gap is only going to widen. That’s a big problem. But I think the paradigm shift is going to lead to more acceptance of a universal basic income and a larger investment in healthcare.

It’s not the time to worry about how we’re going to pay this bill. People need money now, and I’m glad a large portion of the bailout is going to regular people on Main Street rather than just to corporations on Bay Street and Wall Street.

Managing Investments in Uncertain Times

Finally, Meaghan wants to check in to make sure her personal finance and investing strategy still makes sense during the coronavirus crisis:

Hi Robb, I wanted to touch base with you about the current situation in financial markets. Our current strategy is:

- Keep our focus on our long term retirement goals and not worry (too much!) about short term losses.

- Ensure we have 6-12 month’s emergency cash savings

- Keep my regular diversified investments into RRSPs etc going (with the hope of reducing my cost average)

Is there anything obvious we are missing?

Hi Meaghan, I think you’ve hit the nail on the head. Don’t worry about short term losses. We’ve just seen the largest one-month decline in history. Markets hate uncertainty, but once we see the light at the end of the tunnel then markets should price in the eventual recovery and things could climb just as quickly (as we might be seeing already).

Cash is king, so you’re right to focus on a large emergency cash savings buffer.

One tip might be to divert anything you’re not spending on right now towards your cash savings. For example, we put our gym memberships on hold, saving $118/month. We’re likely not going to be spending as much on dining / take out and instead just preparing meals at home – which will likely save a few hundred bucks a month. We had prepaid a bunch of travel (trip to Italy in April) which has now been cancelled so that refunded money has been put into our emergency savings.

Avoid the urge to put a large amount of money to work in the market right now and instead stick to your regular contribution plan. I know it’s tempting when you see “stocks on sale” but no one has any idea how long this will last and putting a lot of money into the market right now goes against the idea of building up your cash savings.

Rebalance. I’m in the unfortunate position of being 100 percent invested in equities (VEQT) and having used up all of my RRSP contribution room. So I can’t rebalance by selling bonds and buying equities, and I can’t even add to my account because I am all out of room.

That’s okay. I’ve got a long time horizon and I know markets will recover eventually. But it’s a good reminder to be mindful of your true risk tolerance and to ensure you have an appropriate asset mix that you can live with in good times and bad.

Holding bonds, while reducing some of your upside in the long term, is certainly beneficial at times like this because you can rebalance “into the pain” and buy more stocks at lower prices without having to come up with more cash to invest. That’s a good thing.

I hope that provides some comfort. It sounds like you’re in a good position to ride out this period of uncertainty and come out in good shape on the other side. It’s just going to take some time.