I write a lot about investing and always try my best to use plain language and real life examples to explain investment strategies, describe different products, and identify best practices. But I fully recognize that investing is a foreign concept to many people, especially if you're new to investing or have always handed over your savings to a mutual fund sales person at the bank.

I answer reader questions about investing every day and have heard variations of the same basic questions over and over again. That's totally fine, it's better to ask a ‘stupid' question than pretend you already know the answer (or worse, make a mistake with that lack of knowledge).

This article aims to answer many of these investing questions in hopes we can use it as an FAQ of sorts for new investors.

Q. What's the difference between management fee and MER?

Mutual fund and ETF investors will notice two different costs listed on their fund fact sheet. One is the management fee, which is the amount paid to the fund manager. The second is the management expense ratio or MER. This includes the management fee, plus operating expenses for marketing, legal, auditing, and other administrative costs.

When a new ETF is introduced, the management fee will be published but the total MER will not be known for 12 months.

What's not included in the MER is the fund's trading costs, which are identified separately as the trading expense ratio or TER. The TER may be very small, even zero in the case of some ETFs, but it could also be quite large.

VEQT charges a management fee of 0.22%. Its MER is 0.25%, and its TER is 0%. Total fee = 0.25%

Compare that to Horizons' HGRO, which has a management fee of 0%, an MER of 0.16%, and a TER of 0.18%. Total fee = 0.34%.

Q. Asset allocation ETFs like Vanguard's VEQT are “funds of funds”. Will I pay two levels of MER: One for VEQT and one for the underlying ETFs?

No. Vanguard's All Equity ETF (VEQT) charges a management fee of 0.22% and has a MER (total fee) of 0.25%. From the VEQT ETF fact sheet:

“This Vanguard fund invests in underlying Vanguard funds and there shall be no duplication of management fees chargeable in connection with the Vanguard fund and its investment in the Vanguard fund.”

VEQT's management expense ratio of 0.25% is higher than if you were to hold the four underlying ETFs on their own. But the advantage of holding an asset allocation ETF like VEQT is that it automatically rebalances its holdings so that you don't have to.

The confusion about double-dipping fees likely comes from the robo-advisor model, where the robo-advisor charges a management fee of, say, 0.50% plus the MER of the ETFs used to build your portfolio.

That's why a DIY investor who is comfortable opening a discount brokerage account and executing a trade can reduce their investment fees by holding an asset allocation ETF instead of using a robo advisor.

Q. Should I diversify outside of an asset allocation ETF?

An asset allocation ETF is designed to be a one-ticket solution. Indeed, it may be the only investment product you need in both your accumulation and decumulation phase.

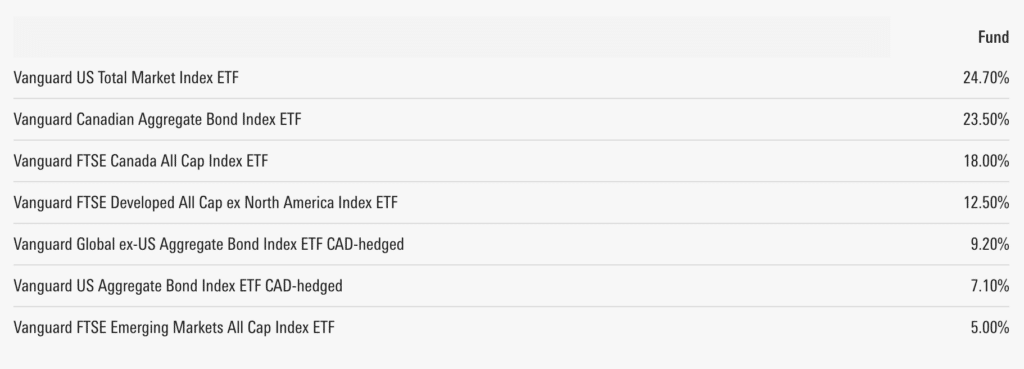

We're taught not to put all of our eggs in one basket. But consider Vanguard's Balanced ETF (VBAL). It holds 12,642 stocks, plus another 16,553 bonds from all over the world. That's a pretty big basket!

Let's look at the underlying Vanguard funds and their allocations:

This is an extremely well diversified portfolio all wrapped up into one easy-to-use product. So, the question is more about which asset allocation ETF is most appropriate for your risk tolerance and time horizon – not whether you should add even more diversification to this investment.

When does it make sense to hold more than one asset allocation ETF? When you're trying to reach an asset mix that isn't available in a single balanced ETF. For example, if your risk profile suggests a 50/50 balanced portfolio you could hold equal amounts of VBAL and VCNS (Vanguard's Conservative ETF). Similarly, to reach a 70/30 asset mix you could hold equal amounts of VGRO (Vanguard's Growth ETF) and VBAL.

Q. These asset allocation ETFs don't have a lengthy track record or performance history. Should I invest in a relatively new product?

Asset allocation ETFs were first introduced by Vanguard in 2018. But the concept isn't new.

First of all, balanced mutual funds have been around for decades. Second, the underlying ETFs used to build an asset allocation ETF likely have a much longer track record. Finally, the stock and bond indexes tracked by these ETFs have been around for a long time and so the fund can be back-tested to determine how well it would have performed had it existed for the last 25 years.

In fact, PWL Capital's Justin Bender has done exactly that on his Canadian Portfolio Manager blog. There, you'll find the theoretical annualized returns of each of the Vanguard and iShares asset allocation ETFs dating back 25 years.

One reason this question comes up so often is because the mutual fund industry has taught us to look up a fund's long-term performance to determine its quality. But this was done (ineffectively) to help investors identify top fund managers. We compared the performance to that of other mutual funds – not to its benchmark index.

With an ETF that's passively tracking an index there's no need to see a lengthy track record of performance. It's designed to mirror the performance of a specific market index, which should have a long history of its own.

Instead, what investors should be looking at in an ETF is its tracking error, or the difference between the ETF returns and the benchmark index returns.

For example, Vanguard's Total Market Index ETF (VUN) has annualized returns of 16.12% since inception. Its benchmark is the CRSP US Total Market Index, which returned 16.53% annually during the same period. VUN has a cost (MER) of 0.16%, which leaves a tracking error of 0.25%.

A high tracking error (after fees) means the ETF may not be reflecting the returns of its underlying index very well. If an investor was trying to decide between two ETFs tracking the same index, the one with the lower tracking error could be the better choice.

Q. Are robo advisors safe?

Canadians know and trust that our big banks are financially stable. But what about upstart robo advisors? Will your money be safe if you move to a digital investing platform?

The short answer is, yes. Robo advisors use what's called a custodian broker to hold onto your money. For example, the robo advisor Nest Wealth uses National Bank Independent Network (NBIN) to hold your assets in your name. Nest Wealth only has the right to issue trading instructions and cannot access your money other than to receive its monthly advisory fee.

Your account is also protected by the Canadian Investor Protection Fund (CIPF) for up to $1 million per eligible account in case of member insolvency.

Finally, robo advisors use bank-level security measures and encryption to ensure your data is collected and stored safely.

Q. Can I pick my own investments at Wealthsimple?

It depends on which Wealthsimple platform you're referring to.

Wealthsimple Invest is the robo advisor platform that offers its clients a pre-packaged (and risk appropriate) portfolio of ETFs that are automatically monitored and rebalanced. Clients cannot choose their own investments within this platform. All you can control is the risk level or asset mix used to build your portfolio.

Wealthsimple Trade is the commission-free self-directed trading platform where clients can buy and sell stocks and ETFs without paying fees.

One is a digitally managed portfolio that you can't change (outside of your risk level), the other you're on your own to trade and build your own portfolio. The other key difference is that Wealthsimple Trade does not have as wide a variety of account types, with only RRSPs, TFSAs, and taxable accounts available at this time.

Q. I have a large lump sum to invest. Should I invest it all at once or spread it out over a period of time?

The mathematical answer says that it's best to invest the lump sum immediately and all at once. Vanguard studied this in a 2012 paper and found that immediate lump sum investing beat dollar cost averaging about 66% of the time. That’s because markets historically increase about two out of every three days. Having the money invested for a longer period of time improves the odds of capturing positive returns.

However, we're not all emotionless robots and, behaviourally, it’s much more difficult to invest a large sum of money all at once. Loss aversion tells us we’d prefer to avoid losses rather than acquire an equivalent gain. The pain of losing is about twice as strong as the pleasure of winning. There’s also the fear that our decision may turn out to be wrong in hindsight, making us more averse to taking on risk.

Even though investing smaller amounts gradually over time is a less optimal way to invest a lump sum, it might feel better from a behavioural perspective.

If you decide to take this approach it's best to design some rules around your gradual entry into the market. Set a pre-determined investing schedule so that you avoid relying on your intuition around when markets ‘feel’ safe.

What that looks like in practice could be taking a $100,000 lump sum and investing $20,000 per month for five months until you're fully invested. Take that one step further by selecting the specific day of the month when you'll deploy each tranche (e.g. the 15th of every month).

Finally, if you're nervous about investing a lump sum perhaps your risk tolerance isn't as high as you think. Instead of waiting, or dollar cost averaging, go ahead and invest the lump sum all at once but reduce your allocation to stocks (say, a 40/60 asset mix instead of a 60/40 mix) to make investing the lump sum feel less risky.

Final Thoughts

There are no stupid questions when it comes to investing. We're all learning and trying to navigate our way through an often confusing and noisy environment.

That's one reason why I prefer a simple investing approach using the following principles:

- Low cost

- Broadly diversified

- Risk appropriate

- Automated where possible (deposits, withdrawals, rebalancing)

- Holding the same asset mix across all of my accounts

You can do this on your own with a single asset allocation ETF, with help from a robo-advised portfolio of ETFs, or with your bank's own index mutual funds.

That said, we all have our own unique circumstances or legacy portfolios that aren't exactly easy to untangle. If you have an investing question, leave it in the comments below so we can all learn together or send me an email and I'll respond to you directly.