RRSPs Are Not A Scam: A Guide For The Anti-RRSP Crowd

“I don’t invest in my RRSP anymore because I’ll have to pay tax on the withdrawals.” This type of thinking around RRSPs has become increasingly common since the TFSA was introduced in 2009.

The anti-RRSP crowd must come from one of two schools of thought:

- They believe their tax rate will be higher in the withdrawal phase than in the contribution phase, or;

- They forgot about the deduction they received when they made the contribution in the first place.

No other options prior to TFSA

RRSPs are misunderstood today for several reasons. For one thing, older investors had no other options prior to the TFSA, so they might have contributed to their RRSP in their lower-income earning years without realizing this wasn't the optimal approach.

Related: The beginner's guide to RRSPs

RRSPs are meant to work as a tax-deferral strategy, meaning you get a tax-deduction on your contributions today and your investments grow tax-free until it’s time to withdraw the funds in retirement, a time when you’ll hopefully be taxed at a lower rate. So contributing to your RRSP makes more sense during your high-income working years rather than when you’re just starting out in an entry-level position.

Taxing withdrawals

A second reason why RRSPs are misunderstood is because of the concept of taxing withdrawals. The TFSA is easy to understand. Contribute $6,000 today, let your investment grow tax-free, and withdraw the money tax-free whenever you so choose.

With RRSPs you have to consider what is going to benefit you most from a tax perspective. Are you in your highest income earning years today? Will you be in a lower tax bracket in retirement? The same? Higher?

The RRSP and TFSA work out to be the same if you’re in the same tax bracket when you withdraw from your RRSP as you were when you made the contributions. An important caveat is that you have to invest the tax refund for RRSPs to work out as designed.

Future federal tax rates

Another reason why investors might think RRSPs are a bum-deal? They believe federal tax rates are higher today, or will be higher in the future when it’s time to withdraw from their RRSP.

Is this true? Not so far. I checked historical federal tax rates from 1998-2000 and compared them to the tax rates for 2018 and 2019.

The charts show that tax rates have actually decreased significantly for the middle class over the last two decades.

Someone who made $40,000 in 1998 would have paid $6,639 in federal taxes, or 16.6 percent. After adjusting the income for inflation, someone who earned $59,759 in 2019 would pay $7,820 in federal taxes, or just 13.1 percent.

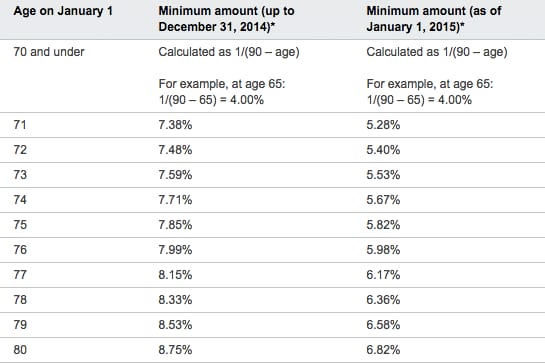

Minimum RRIF withdrawals

It became clear over the last decade that the minimum RRIF withdrawal rules needed an overhaul. No one liked being forced to withdraw a certain percentage of their nest egg every year, especially when that percentage didn’t jive with today’s lower return environment and longer lifespans.

In 2015 the federal government made changes to the minimum RRIF withdrawal table, bringing it more in-line with today’s reality:

The dreaded OAS clawback

Canadians who receive Old Age Security and have annual income between $75,910 and $123,386 will have all or part of their OAS pension reduced. This clawback is especially concerning for retirees whose minimum RRIF withdrawals push them over the income threshold.

Canada Revenue Agency uses the following example on its website:

The threshold for 2018 is $75,910.

If your income in 2018 was $86,000, then your repayment would be 15% of the difference between $86,000 and $75,910:

$86,000 – $75,910 = $10,090

$10,090 x 0.15 = $1,513.50

You would have to repay $1,513.50 for the July 2019 to June 2020 period.

This is a legitimate concern for retirees. No one wants to lose out on benefits that they’re entitled to receive. An advisor or tax accountant can help you determine a strategy that best optimizes your retirement withdrawals.

One such strategy is to make small withdrawals from your RRSP between the ages of 60-70 and delay taking CPP and OAS until age 70. This reduces the size of your RRSP for when you are forced to convert it into an RRIF and make mandatory withdrawals. It also increases your CPP and OAS benefits by 42 percent and 36 percent, respectively.

Related: CPP Payments – How Much Will You Receive From Canada Pension Plan

Canada Child Benefit

Parents with children aged 17 and under can be eligible to receive a tax-free monthly payment from the Canada Child Benefit. The CCB is a means-tested program, so the more income your household earns the less money you receive from this government program.

The Canada Child Benefit is completely phased out when your income is between ~$157,000 and ~$206,000, depending on the number of eligible children in your family.

The government uses adjusted net family income to determine how much you'll receive from the program. Since RRSP contributions reduce your net income, it could be wise for young families to prioritize RRSP contributions ahead of TFSA contributions to reduce their net family income and help them receive more from the Canada Child Benefit the following year.

RRSP Matching

Some lucky employees work for companies that offer a matching program for your RRSP contributions. This is the best deal out there for savers. A guaranteed 100% return on your contributions. In fact, one could argue that contributing up to the maximum of your company's RRSP matching program could be prioritized over paying off a credit card balance at 19% interest. It's that valuable.

A company match will typically have some limits or restrictions. For example, your employer could match contributions up to 5% of your salary with the caveat that you must contribute to a group RRSP plan at a particular bank or investment firm.

It's important to note that, even if the investment options are terrible high fee mutual funds, you should still contribute the maximum and take advantage of these generous matching dollars. You can always transfer the money over to a low fee indexing portfolio at some point in the future.

Final thoughts on RRSPs

RRSPs aren’t a scam; they’re a still a critical tool for Canadians to save for retirement. They’ve just got a bad rap over the years because of some misguided thinking around withdrawals, taxes, plus the introduction of a new and seemingly better (re: tax-free) savings vehicle.

RRSP contributions are still a key component of my financial plan. I’ve caught up on all of my unused contribution room and so now my goal each year is to max out my contribution limit (which is reduced by my pension contributions).

Related: TFSA Contribution Limit and Overview

TFSAs are great, and they get filled up next. In fact, when we paid off our car loan a few years ago we started catching up on our unused room and maxing out our TFSAs.

Both accounts are valuable parts of our financial plan and, along with my pension, will make up the bulk of our income in retirement.

There’s a lot of us who’d like to have that $75,000/year problem!

The reality is for us low income earners who do not have the benefit of a company matched RRSP is that once our taxed money is deposited into our bank accounts then we have to decide where our after-tax dollars go. Into an RRSP or a TFSA. I have around $12,000 in my RRSP and with the help of an expert, I know I need to withdraw it by age 63. That’s so the income won’t affect the possibility of getting GIS after I turn 65.

Although RRSPs aren’t a scam, unless there’s an employer matching plan, or you’re a high income earner, they don’t make a lot of sense to own.

Money going into an RRSP is NOT after tax dollars, as contributions are deducted from your income and so are untaxed dollars .

Only if you request it to be pre tax $.

The amount you contribute is deducted from your income, reducing your income, effectively making them pre tax dollars!

I get that, however, thru our plan at work you need to specify before or after tax and some choose after, not sure why they would though

I built a free RRSP GIS Calculator for exactly this purpose – for low income Canadians approaching or thinking about retirement, having an RRSP can reduce the amount of GIS they’re eligible for. Use this tool to find out if that’s the case and feel free to leave feedback https://rrspgiscalculator.site/

Count me in the anti RRSP crowd from this one aspect. My parents saved within RRSP’s while earning in the lowest tax bracket. They both died within weeks of each other. When their cashed in RRSP’s were added to their pension income in the year of death, they had to pay income tax in the next higher bracket.

So, saving in a lower tax bracket but having to cash out in the next higher tax bracket is a huge negative.

The lesson is to be very aware of your health status and, if questionable, cash out annually to keep your taxable income in the same tax bracket in which the tax was saved. With TFSA’s, this is not a consideration.

I absolutely agree that RRSPs do not make sense for low income earners, and that the introduction of the TFSA has been a blessing for low earners – giving them a choice to shelter savings and withdraw them tax-free without impacting GIS.

John Stapleton has done some really important work on low income retirement planning, including these excellent resources at Open Policy Ontario: https://openpolicyontario.com/retiring-on-a-low-income-3/

It’s important to identify what constitutes ‘low income’. For instance, the GIS threshold for a single retiree is $18,240. If you feel like you’ll be eligible for GIS in retirement then you absolutely need different advice when it comes to saving for retirement.

Also, look at how wide those federal tax brackets are. If your income falls between $47,630 – $95,259 then an RRSP contribution certainly makes sense. There’s also a good chance that your income in retirement will be in that tax bracket (or lower).

For low income Canadians approaching retirement, this calculator will help determine if cashing out an RRSP early could result in receiving greater GIS benefits (built in collaboration with John Stapleton), try it out and feel free to leave feedback https://rrspgiscalculator.site/

There are always different scenarios for each individual as is often pointed out on Robb’s commentary.

As an example;

Background: I am currently 64 years old. I coach personal finance to young people (18-30) as a “hobby” because I like to see them make good choices early and think their decisions through in order to succeed.

Plan: I plan to take OAS from age 65-71 and limit other income to below the clawback amount. At age 72 when I have to convert to a RRIF I will be getting about $50k from my RRSP as it has done very well to date. With other income income I will be closer to $100k or more and the clawback kicks in. So the plan is to maximize OAS until age 72. If my wife happened to pass away before me, my RRIF would withdrawal be over $100k alone and i know there would be full clawback.

I am fortunate to be able to have several buckets to draw income from which is why each person’s scenario needs to be thought through and a full plan developed.

(As a side note I have not contributed to my own RRSP in over 25 years and it is still larger than my wife’s spousal RRSP to which I have been contributing the maximum to over all those years. The point being we are all walking different financial journeys and one of the keys is to save early!). Having a financial plan early and then revisiting is critical.

Of course they are after tax dollars. You contribute money that has already been affected by deductions.

After-tax versus pre-tax RRSP contributions is a concept I struggled with myself. To maximize your desirable contribution the goal is to get as much pre-tax income into your RRSP as possible. If your company does RRSP payroll deductions they most likely will contribute your pre-tax income and your job is done…no tax removed and a full contribution is made.

The question becomes how to maximize your after-tax RRSP contributions? Fortunately Rob has written a great article with an example on the “gross up” strategy that shows how to make your after-tax contribution equivalent to a pre-tax contribution.

https://boomerandecho.com/how-to-supercharge-your-rrsp/

On a side note, really enjoy your blog Rob. Been following since middle of last year and enjoy your weekly posts.

I’m doing fine without your ‘advice’. Lol

Thanks for covering a list of increasingly common misunderstandings Robb.

I’ve had people argue that because growth is taxed at withdrawal, the RRSP is worse than the TFSA.

The best way I’ve been able to explain the benefits of an RRSP is by taking a deposit through the life of the account to withdrawal. This can then be compared to the same situation with a TFSA. This of course isn’t always an option, and articles like this one help in place.

Hi everyone, I’m in the lowest tax bracket at the moment and am interested in buying some US stocks and/or ETFs. I was wondering, would it make sense to hold US equities in my RRSP to avoid the withholding taxes, even though I’m in the lowest tax bracket? Thanks for your help!

Not sure I agree that the TFSA and RRSP are equal assuming you are in the same Marginal Tax Rate

if you have little other NR savings the RRSP withdrawal is really at you ‘average Tax Rate’ since you get some CPP maybe, maybe some NR dividend and div tax credits

so assuming you drawn out 80k a year + 10k cpp (and assume nothing else) only a small portion of the withdrawal is actually at your MTR, some will be 0%, some 20%, etc

which specially when you put in 100% at a reasonable MTR > 30% up to 50+% MTR now is a big win when you draw it out on average @ 20% (even though your MTR @ withdrawal might be the same 30%)

and of course as you mention, if low/middle income taxes are declining which the government seems to want to do, then the average rate on your withdrawal will be even less which is another win

ignore OAS clawback etc for the time being

and of course the issue of early death

I suppose if you’re saying the MTR of the 1st dollar of the RRSP withdrawal as opposed to the last dollar of the RRSP withdrawal

really need to average the tax over the whole withdrawal, and compare that vs the MTR of the contribution (which since usually smaller than the withdrawal and take off the top is more likely at the MTR)