Why You Shouldn’t Take CPP At Age 65

In previous articles I've looked at reasons to delay taking CPP until age 70, along with explanations why you might want to take CPP earlier at age 60. But in this article I'm going to explain why you shouldn't take CPP at age 65.

The most compelling reason to defer CPP is the increase or enhancement of your benefit – 0.7% for every month you delay past 65. Wait until age 70 and you'll receive 42% more CPP than if you took it at age 65. Taking CPP early can also be an attractive option for those with a reduced life expectancy or for those who simply need the money right away.

Once you're close to age 60, Service Canada will mail you an application form, along with an estimate of your CPP benefits. Curious, since this behavioural “nudge” may influence you to take CPP early at a reduced rate, rather than waiting until the standard retirement age of 65.

Finding out the optimal age to take CPP requires a break-even analysis and depends on a number of factors, including how much you've contributed and for how many years, plus a guess on how long you'll live. Also playing a role is your current and future tax bracket, your income needs now versus in the future, plus the impact that taking CPP early has on means-tested benefits such as GIS and OAS.

What's interesting about the break-even analysis for CPP is that the standard retirement age of 65 is never the optimal age. Let me explain:

Why Not Take CPP At Age 65?

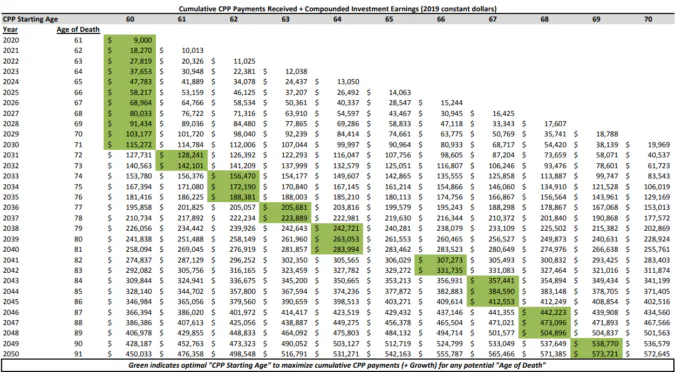

In I post I wrote years ago about taking CPP early or late, Canada Pension Plan expert Doug Runchey shared with me the interesting fact that taking CPP at 65 is never the optimal choice from a payout perspective.

Indeed, Aaron Hector, a financial planner at Doherty & Bryant Financial Strategists, expanded on that fact with an interesting analysis on optimal CPP starting ages.

Hector looked at two scenarios; one in which the retiree spends all of his or her CPP benefits, and one in which the retiree invests their CPP and earns a 3% real return after taxes.

What he found was that taking CPP at age 60 was best for those who live only until age 69 (when CPP was spent), or until age 71 (when CPP was invested). Taking CPP at age 70 was optimal for those who live until age 86 and beyond.

As you can see, age 65 is never the optimal starting age to take CPP. That said, you could argue that 65 is the sweet spot between the two extremes of taking CPP early or late.

It's helpful to know that the normal life expectancy at 60 for a Canadian is 25 years. So, if you don't have any reason to believe you'll have a shorter or longer life expectancy then 85 is a good age to use as a benchmark for your own break-even analysis. In this case, the optimal age to take your CPP payments and receive the most money is age 69.

Taking CPP early and investing

There's a mindset among some retirees that they should take CPP as soon as possible and invest. The idea being that the longer their investments can compound, the better off they'd be versus delaying CPP beyond age 65.

But Hector's analysis should put a damper on any expectation that taking CPP early and investing will lead to a better outcome. This could be due to overconfidence in one's investing ability, over over-optimism about the expected rate of return. In any case, as you'll see below, taking CPP at 60 and investing the entire amount only improves the optimal outcome by two years.

It's hard to beat a guaranteed 7.2% a year increase in CPP benefits just by delaying your application. There's also a practical argument against this approach. Is the object of the game to amass the largest bank account before you die? Or is it to spend and enjoy what you worked so hard to earn in retirement?

In my mind, it's not a rational argument that a retiree will invest every single dollar of CPP benefits. At some point we're going to spend our money.

Final thoughts on taking CPP at 65

The standard retirement age of 65 is embedded in our society and triggers most Canadians to take their CPP benefits at that age – like a rite of passage for retirement. But what I've explained here clearly shows that it's never optimal to take CPP at age 65, from a purely financial perspective.

If anything, this analysis and research should at least give us pause before automatically applying for CPP at age 65. Look at your family history – are they leading long and healthy lives, or is there a trend of illness or disease? Beyond that, what kind of shape are your finances in today? Where will your retirement income streams come from? Do you fear you'll outlive your money?

All of these questions should play a role in your decision as to whether to take CPP early, late, or somewhere in-between.

You will get more than 0.7% increase in payment/month since CPP is indexed to inflation. Need to add the indexing to the payment.

For those who are not yet collecting CPP it is indexed to wage growth in Canada, not CPI. Wage growth is usually higher than CPI. This year CPP increased over 5% for those waiting. CPI was lower.

My accountant advised me to take my CPP at age 60. I guess I did invest it and have done reasonably well but here I am at 90 with a very minimal CPP because I didn’t start paying until I was 4o years old. Just FYI.

The deferral benefit of 0.7% / month only started in 2012, prior to that it was only 0.5%.Congratulations on making it to 90.

If a couple both delay until 70, the maximum survivor benefit also increases by 42%. In our case, my wife will have a small CPP payment and will be able to use the entire 60% survivor benefit should I die first.

The survivor benefit is not enhanced by the 42% as it is based on the age 65 amount. The maximum survivor benefit is 60% of the maximum age 65 amount, not any enhanced amount, or $692.75 monthly. A survivor receives a combination their own CPP + the survivor benefit to a maximum of a single age 65 amount.

Taken from a post by Doug Runchey who Robb quoted in his article:

https://retirehappy.ca/cpp-survivor-benefits/

“Someone who started their CPP retirement pension at age 70 (with a 42% increase) would effectively have a maximum combined benefit as high as $1,639.50 for 2019 (142% of $1,154.58).”

Interesting, thanks for the link. When calling Service Canada they indicate the maximum does not include the bonus, guess it depends on who one connects with. Appreciate the data, even more reason to delay…

You’re welcome. I asked this question of Doug on another forum as it is relevant for me. My wife will have a small CPP benefit, so she can make use of all of the survivor benefit she can get.

Service Canada is hit or miss on getting correct info.

I have been doing some further reflecting on this subject and I think we have all missed an important variable if you are married. While I may die at less than the “breakeven” point, my spouse will end up getting some of my CPP during her lifetime.

So it would suggest in some cases that the assumed age of death for your spouse is quite relevant. I have not yet seen a spreadsheet that takes this into account in some way. In my case my spouse is 6 years younger than me so if I died at say age 75 she would only be 69 and would continue to get a large portion of my CPP. In her case she will only be getting perhaps $400 per month from CPP while i will receive the maximum. I have assumed our marginal tax rate will be 30%. If we assumed she lives to be 85 she would still get 16 years of benefit from my CPP.

If I wait until 70 take CPP I will only get 5 years worth but she continues with the reduced payments.

Would it be better to wait until 65 or later in this case?

Would like to hear thoughts/comments on anyone who has factored this in.

Not to mention the risk of one of the individuals in a couple passing away and no real survivor benefit being paid out (if the survivor has own CPP). The longer you delay, the higher the liklihood of this happening.

I built my own detailed spreadsheet, complete with federal/provincial income tax calculations, inflation assumptions, modelling of investment returns, future living expenses, CPP entitlements and various strategies for drawing down my RRIF/LIRA accounts early versus living off the distributions in my unregistered account. The optimum age for starting my CPP (which was based on maximum net worth at death) varied between age 61 and 63, depending on whether my life expectancy was 75, 80 or 85 years. I retired early and worked outside Canada for 4 years so delaying CPP didn’t automatically mean higher payments due to the dropout rules. Bottom line: do your own analysis for your own unique situation because taking or not taking CPP at a certain age has push/pull affects on your other income streams and the amount of income tax you’ll pay throughout your life.

What about if someone retires at, say, 62 and receives a fixed benefit pension that is ‘topped up’ until age 65 when CPP is supposed to make up the difference? Would it then make sense to take CPP at 62 and have three years of receiving both the topped up pension and (admittedly lower) CPP?

Wow,

Forgot about the spouse completely!

These financial calculations make s lot of sense when you’re doing the work on paper but it’s not easy factoring in the major uncertainty of one’s death. What do you say about the idea of accessing your CPP at age 65 and investing them if you have the budgeting leeway to do so?

I did not take my C.P.P. early because my LIRA was all converted to a 30 year guaranteed term certain annuity. This started just last month and I get $4,237.18 a month until I am age 92.

I don’t have any debts and my house is modest and so I really need only $1,500 a month to live decent. After all my taxes, cost of living I still have $2,000 a month left over. I will increase my emergency fund from currently $20,000 to $40,000 and top up my TFSA’s to the max every year.

My goal as a single women is to have $200,000 in other savings, investments by my 70th birthday.

The auther says age you have to live past 86 (I say 82) to make delaying to age 70 to pay off, sounds risky

If one turns 70 in June: Is it possible to wait until the next January to apply retroactive for both OAS/CPP and have 6 month paid the following year? Self employed income pushes income over OAS clawback and high(er) tax rate in 70th year. Looking to do some ‘tax Manning’s.

If I quit work at 48 years am I better to take the pension at 60 or 65? I don’t need the money tho.

I am thinking if I take it sooner it will be a smaller cheque which will reduce taxation later when my other pensions kick in? Feedback?

From all the above it is clear perspective is everything. Money is also not everything. This last year and a half has made us wake up to that.

Do any of these analysis take into account the erosion of capital. If you delay CPP you will need the income from somewhere.

Hi Dave, the point of delaying CPP is to increase your guaranteed lifetime income. It implies that you replace the income by drawing from your personal savings (assuming you have enough to tide you over while you defer CPP). It does not mean spending less.

So, yes, you will be drawing down your personal savings more quickly while you defer. A recent study suggested this approach will lead to $100,000 more lifetime income: https://boomerandecho.com/weekend-reading-100000-lifetime-loss-of-cpp-edition/

It sounds counter-intuitive, but it works.

Great discussion especially from the standpoint that it gets people to look at the numbers. Like all of you I have crunched numbers in my retirement spreadsheets and after all the number crunching was done I ended up deciding to take my CPP at age 60 for one simple reason: net of the 25% income tax deduction the government withholds at my request I net a whopping $498/month. This number is not material to my overall financial planning – it doesn’t cover gas for our cars each month. If this number is material to someone then they likely will be able to gain access to other government support programs. The incremental amount “earned” by waiting longer for this money seems nominal when facing the larger question regarding how do we support ourselves in retirement? The debate of when to take CPP is dwarfed by this larger question. Time is better spent on financial planning and recognizing that there are broadly two stages of retirement: the let’s enjoy life stage when we are active and the later stage (post 75-80 barring illness) when our ability to venture too far from home dwindles. Accessing time and the use of our time is far more important than when we should start taking CPP in my opinion.

Alan, of course we need perspective here and how CPP fits into your personal retirement situation. Life should be lived outside the spreadsheet.

But I want to push back on the notion that delaying CPP means spending less in your early retirement years. It’s simply not the case, at least it’s not what I and other financial planners advocate for when discussing when to take CPP.

Spend what you want to spend to enjoy a nice retirement. Just get those funds from your personal savings until age 70. This transfers risk from your riskiest assets (investments) to a guaranteed, paid for life, indexed to inflation income stream.

The only caveats are that you need to have sufficient savings to make this work, you need to be comfortable spending down your capital (knowing that extra CPP will help backstop you later in retirement), and we need to come to grips with our own behavioural biases and fears of dying early without getting “our share”.

As Fred Vettese says, if you die early you have bigger problems than leaving CPP money on the table – like not breathing!

Hi Robb, agree with your comments. I guess to me this debate happens so often in both formal and casual environments and to me there isn’t a right answer and it’s a red herring. I love your blog because it gets people talking and thinking. The CPP age debate should serve as a catalyst for discussion in the other areas. It would also be interesting to see the spreadsheets you included in this blog done in such a way as to only show the incremental dollars between the aged delay times and net of say 25% income tax. This would really highlight the limited incremental annual impact of delaying each year.

That makes the most sense to me. I turn 60 this spring and I want the money sooner than later. I get the max which means I will have collected 92400.00 by the time I am 70. I hope I can enjoy the money in early retirement vs late.

Does the same “logic” for delaying CPP hold true for OAS, when married andwhen one partner dies does the surviving partner’s would all be clawed back?

If you take CPP at 60, invest it in your TFSA, all you have to have as a return is 4.2% (hmmm that is what is recommended as a withdrawal rate in retirement) if you are in a 40% tax bracket as CPP benefits are taxable and TFSA withdrawals are not.

Has this option been explored?

Don’t forget about the CPP rules

I turned 60 in the spring and the government had already sent paperwork to encourage me to apply for my CPP. My husband and I have done numerous calculations to factor in his expected life of 85 years and mine of over 100. We have looked at how much I will receive once he passes (again with a single person maximum). This took me several hours, but for us, the sweet spot for me is age 68 and for him 66. I had good earnings at maximum for several years, but took off some years to be a stay-at-home mom. This calculation has to be done as a couple. It is extremely complicated, and if you can’t do it yourself, it would be a good investment to hire someone who can. The difference over your lifetime could be significant.

If you take CPP at 60, invest it in your TFSA, all you have to have as a return is 4.2% (hmmm that is what is recommended as a withdrawal rate in retirement) if you are in a 40% tax bracket as CPP benefits are taxable and TFSA withdrawals are not.

Has this option been explored?

Don’t forget about the CPP rules upon the death of a Spouse before and at age 65 regarding the maximum amount the surviving spouse can receive.

I’m 59 and I received the application form for next year in the mail from Service Canada. Still deciding on when to take it – I don’t need the money now but I’m concerned about clawback of my OAS later if my income is too high with my pension.

“Life should be lived outside the spreadsheet.” Excellent line.

My decision is based on the crossover points and how much money I was willing to potentially leave on the table. That means having accurate numbers so I hired DRpensions to run them. This determined that at age 90 I would potentially leave 57K on the table. (60 vs 65) – I never intended to wait pass 65 becomes longevity is not strong in my family history.

My plan is to invest a portion of CPP and spend a portion. That closes the gap on the 57K and will create a bit more inheritance for the kids. I enjoy these articles as they create discussion and help us. There is no perfect answer for everyone.

There is no rule that dictates taking CPP before OAS. depending on income streams and tax situations, it might make sense for some to take OAS at 65 and CPP at age 70.

After a few days of spreadsheeting out when my wife and I will commence our CPP, we concluded that it will be the January after we turn age 63. In order to do this analysis we had to first answer two key questions:

1. At what age can we expect to expire?

2. Do we have enough to protect against longevity and inflation risks?

Our answers were ‘age 85 (me), age 87 (wife)’, and ‘Yes’.

We have many dropout years, and our drawdown calls for us being right on the limit of us going into the next tax bracket up. The dropout years reduce the gains of delaying between age 63 and 65, and the increase in CPP between age 66 and 70 is somewhat muted because the additional CPP income will unavoidably be in a higher tax bracket.

Aaron Hector‘s chart, where CPP is invested, (we are missing many factors behind this chart), provides some indication of why we ended up at an age earlier than 65. Look at the line for age 85. The difference is relatively small between all ages from 64 to 70, with 70 being even less than 64. Now throw in the impact of inflation on that difference, and over 20 years it’s almost halved. This relatively minuscule amount has to be weighed against the odds of either of us expiring before age 85 and 87, respectively. I think the odds are high.

In addition to determining our CPP commencement date, I’ve concluded that there are many factors that should be considered and included in arriving at an optimal decision. This is where a fee-for-service financial planner could really help. I’m not a qualified financial planner, I just like analyzing stuff.

One other note: we have kids, so leaving a higher inheritance is an important factor in our financial plan.

Lot of people die before 70 years old.

What is the use of getting CPP after 70 if you do not exist on the earth?

In 2000 CPP had approx 2.4 Billion in assets (google it)…. in 2021 it had $490B. It has grown because 1. A good investment mandate leading to superior performance 2. increased funding from Canadian workers and 3. People die before taking all their contributions.

I lost both of my parents in their early 70s. They did not take out the principal they contributed since the plan’s inception in 1966

I hope I live a long life but both my wife and I began collecting at age 60 because if one of us dies the survivor amount will be negligible. We are either investing, giving it away or helping the economy and spending it.

Hello Everyone, I really like this forum and there are excellent points from everyone on when to take your Cpp. I have been struggling with this myself and have done my own analysis to try and sort out when is best for our household. I have even downloaded my statement of contribution for my wife and I from the CRA portal. Running the statement of contribution numbers through the applicable Cpp calculator you will find this a worthwhile endeavours. By the way the Calculator at CRA is rubbish because it assumes that you will be contributing to Cpp until taken which is not the case for me or my wife we retired at 55. Which means when we decide to start taking our Cpp we will have more drop out year included in our overall calculations. But with that said using the Cpp calculator I found through another site and I believe is available here as well. If there calculator is not available, here is the calculator I used which allowed me to input my non contributory years as well to give my wife and I the actual dollar amount we will be receiving when taking our Cpp. https://www.cppcalculator.com/

This allowed us to make our final decision based upon actual dollar values, this is based on our major concern of how our non-contributory year would affect our overall final Cpp payment. To our surprise even with a high non contributory years which would be 10 years at 65 and 15 years at 70, we are getting still getting over $1700 each by delaying until 69 which is the optimal year for us to start taking our Cpp. We don’t need the cash and we are using this strategy for us based upon our estate need by melting down both our RRSPs.

One subject that was not covered in this forum is the tax burden on your estate if you happen to pass away with a large amount of RRSP still in your possession. This is all part of our estate plan as well because we have worked hard to acquire enough to live well and have a defined pension through both our work. Therefore, we do not want to give 45 – 50% to the government though our estate. I know we will not be here but I have always made sure to pay our fair share of income tax but think it’s right to give up such a large percentage to the government when it could go to our children. This means we would use our RRSP to supplement our bridging benefits once it’s dropped at 65. We are fortunate enough to be able to apply this startegy in our case because we not only planned ahead but have two government defined pension on which to draw. However, even with this in mind my wife and I are on different pages when it comes to when to actually take our Cpp. But we have compromised on an age that seems good to us. We took into account the break even point for each of the years 60, 65, 70. Once again this decision is a very personal one. Despite my wife having parents that are still living into their 84 and 88 year of existence she would like to take our Cpp earlier while I wanted later. My parents have both passed away at 75 and 76 however I still to be opmistic about my longevity because I did not have to work myself to death as they had to just to make ends meet. So as you can see my wife and I are on the same page with all out finances with this one exception but I have shown her the percentages of taking it early as opposed to taking it later and she still would like to take it at 65. However, since I have always been entrusted with the overall finances she has given into my agreement of a 33.8% indexed increase life time over a loss.

However, despite that I will keep and eye on our finances and modify it accordingly. Just because you make a decision on when to take it that does not mean you have to stick with that decision what happen as one individual develops and illness that terminal not to be morbid but then you would definitely start taking that Cpp right away and adjust as you age.

Final note if I was everyone I would go online and download your statement of contrubution from Cra. Then follow the Cpp calculator instructions on downloading the calculator and run your html download through the Cpp calculator. You will find it an eye opener and well worth the effort. It will surprise you how much you will get from your Cpp despite having a a significant amount of non-contributory years by delaying your Cpp one or two years.