Wealthsimple Trade Review – Canada’s Only Zero-Commission Trading Platform

Wealthsimple Trade is Canada’s first and only zero-commission trading platform. In this Wealthsimple Trade review I’ll explain how you can buy AND sell from among the thousands of stocks and ETFs listed on North American exchanges without paying any fees.

I first heard about Wealthsimple Trade in 2018 when it was announced as a new self-directed investing platform that lets investors buy and sell stocks and ETFs with no trading commissions. They invited users to join a wait list and, once they attained a critical mass (130,000 participants), rolled out a beta version for users to test the platform and offer feedback.

Wealthsimple Trade officially launched in March 2019 and at that time only supported non-registered trading accounts. Later that year, the platform added RRSP and TFSA account types to its lineup. That’s when I became interested in the platform for my own self-directed investing needs.

Get a $10 cash bonus and commission-free trades when you open a Wealthsimple Trade account and deposit and trade at least $100 worth of stock.

Why I Switched to Wealthsimple Trade

I’ve held my investments at TD Direct Investing since 2009. It was out of convenience, more than anything, since I had banked with TD since I was a teenager. Back then trades disgustingly cost $29 per transaction. Today, they’re still a painful $9.99 per trade. I had enough when I noticed I paid a total of $190 in trading commissions with TD last year. No more.

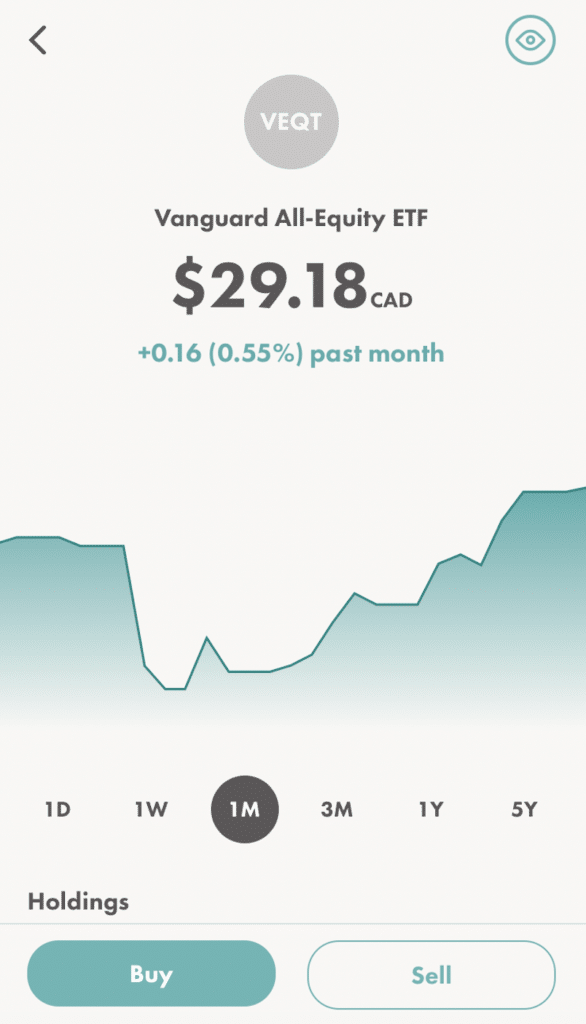

I opened a Wealthsimple Trade account on January 13 2020, with the goal to bring my trading commissions down to zero. That same day, I initiated the transfer of my entire RRSP and TFSA account balances. Both of these accounts were invested in Vanguard’s all-equity balanced portfolio – VEQT – and so I requested an in-kind transfer which simply transferred the shares from TD to Wealthsimple Trade without first having to sell them.

An email from Wealthsimple suggested an expected wait time of up to five weeks to complete a transfer request with TD. But to my surprise I noticed the funds in my Wealthsimple Trade account on January 21 2020 – just seven business days later.

Now that you have the backstory, let’s take a look at the platform.

About Wealthsimple Trade

As mentioned, Wealthsimple Trade launched in March 2019 as Canada’s first and only zero-commission trading platform. It’s a separate, yet complementary service to Wealthsimple’s main business as Canada’s top robo advisor. With offices in Canada, the U.S., and the U.K., Wealthsimple manages more than $5 billion in assets worldwide.

Related: How to transfer your RRSP to Wealthsimple

Automated investing through a robo-advisor isn’t for everyone. Some investors want to take the reins themselves, build their own custom portfolio, and make trades in their own self-directed account. Enter Wealthsimple Trade.

While most online brokerages charge $9.99 per trade, Wealthsimple Trade doesn’t charge anything to buy and sell stocks or ETFs. It doesn’t charge account fees or have any account minimums to get started.

To get the costs down to the bare minimum (zero) the platform strips out all of the expensive bells and whistles. You won’t find cutting edge research or real-time quotes (there’s a 15-minute lag). Wealthsimple Trade also started out as a mobile app – on your smart-phone or tablet – with no desktop platform access. That, thankfully, has changed and Wealthsimple Trade now offers desktop access (January 2021):

But for self-directed investors who want to build a simple low-cost portfolio of index ETFs, and who want to contribute frequently without getting dinged each time they buy or sell, Wealthsimple Trade is the perfect platform.

Signing Up and Opening an Account

How do you open an account? Easy. Download the Wealthsimple Trade app on your Apple or Android device and select ‘Get Started’. From there, follow the prompts to enter your information and agree to your account documents.

Note that even though the Wealthsimple Trade app is NOT connected at all to the Wealthsimple robo advisor platform – existing Wealthsimple clients can skip some of the preliminary questions.

Here’s what you’ll need to get started:

- Full Name, Email, Mailing Address, Phone number, Date of Birth

- Social Insurance Number

- Employment information

There are no account minimums or fees associated with opening the account. To fund it, though, you’ll need to link a chequing or savings account.

Transferring Investments to Wealthsimple Trade

Transferring my existing investments to Wealthsimple Trade couldn’t have been easier. As mentioned, I initiated the transfer on January 13, 2020. I entered a few details about the accounts I was transferring, selected the institution (TD) from a list of choices, and snapped a picture of my account statements.

Next, I indicated how I wanted the transfer to take place. Typically, you can choose to transfer funds in cash, meaning your institution sells your current holdings and then moves the money. If you go this route, you may incur DSC or trading fees. Note that your contribution room or taxes won’t be affected when you transfer a non-taxable account like an RRSP or TFSA.

Instead, I chose to transfer my account in-kind or “as-is”. This means your institution transfers your entire account. Note that Wealthsimple Trade only accepts the transfer of stocks and ETFs. You’ll have the option to sell non-eligible assets like mutual funds, bonds, or options, or leave them with your institution.

As I said earlier, the entire transfer process took just seven business days. Your mileage may vary.

Using Wealthsimple Trade

Wealthsimple Trade works like any other online brokerage, with the exception that it’s a mobile-only platform. There’s no desktop support.

To search for a stock or ETF, tap the search icon at the top-right of your screen and enter the name or ticker symbol.

Once you have the stock or ETF profile up on your screen, simply tap the ‘Buy’ or ‘Sell’ button. Then, select the account in which you want to buy the stock or ETF (RRSP, TFSA, or non-registered).

Now, enter the number of shares you wish to purchase. You’ll see the current price of that security, the estimated cost, and how much you have available to trade. Remember that Wealthsimple Trade does not show real-time quotes – there’s a 15-minute delay in the market information.

This is a good time to remind you about bid-ask spreads and market vs. limit orders.

The bid price is the what you’re likely to get if you’re selling the stock or ETF. The ask price is the price you are likely to get if you’re buying the stock or ETF.

The default purchase setting is for a market order. This means your order will be filled at the best available price on the market.

With a limit order, you choose the highest price you are willing to pay (your limit). Your order will only complete if and when the market price is at or below your limit.

Wealthsimple Trade Highlights

What stands out the most for me about Wealthsimple Trade is of course the ability to buy and sell ETFs for free. I was paying $9.99 per trade for years – which is what most discount brokerages charge. Yes, a select few brokers offer free ETF purchases, but Wealthsimple Trade is the only platform that offers zero-commission trades across the board (buy or sell).

You can choose from thousands of available stocks and ETFs that traded on North American stock exchanges (NYSE, NASDAQ, TSX, TSX-V). You cannot trade mutual funds, options, preferred shares, over-the-counter securities (OTC), or stocks that trade outside of North America.

Wealthsimple Trade will reimburse any transfer fees on transfers larger than $5,000.

The mobile app is incredibly intuitive and user friendly. And, the new desktop access is an excellent addition to the Wealthsimple Trade experience.

The app is secure and fully encrypted, relying on two-factor authentication protection to keep your data safe. It requires a PIN, and you can also enable touch ID to access your account.

Your money is secure. Wealthsimple Trade is a division of Canadian ShareOwner Investments Inc. and is a member of the Canadian Investor’s Protection Fund (CIPF) which protects accounts up to $1,000,000 against insolvency.

The zero-commission trade platform is ideal for investors who have simple, low cost portfolios and who frequently add new money to their accounts.

Downside to Wealthsimple Trade

I’d be remiss not to mention any cons to the Wealthsimple Trade platform.

For one, clients are limited to three account types at this time (RRSP, TFSA, and non-registered accounts).

The platform is mobile-only, so it can only be accessed on your smart-phone or tablet. A desktop version has been rolled out as of January 2021.

There is no option (at this time) to support auto-deposits. Instead, a one-time deposit must be set up each time you’d like to fund your account.

While not necessarily a con, you should know that Wealthsimple Trade makes its money by charging a 1.5 percent currency conversion fee on CAD to US dollar conversions (and vice versa) that are required to trade US-listed stocks and ETFs.

Finally, since this is a no-frills platform, you won’t find in-depth research on stocks and ETFs. Also, stock quotes are not updated in real-time – there’s a 15-minute delay.

Wealthsimple Trade Review: Pros and Cons

| Account fees | None |

| Trading fees | None |

| Account minimum | $0 |

| Other fees | Corporate rate + 1.50% for CAD to USD foreign exchange |

| Minimum deposit | None |

| Account types | RRSP, TFSA, non-registered account |

| Access | Mobile app and desktop |

| Transfer fees | Wealthsimple Trade will reimburse transfer fees on transfers greater than $5,000. |

| Market research | Wealthsimple Trade does not have in-depth market research and does not support real-time quotes (delayed by 15 minutes) |

Wealthsimple Trade vs. Questrade

I considered moving my self-directed investing accounts from TD Direct to Questrade before ultimately switching to Wealthsimple Trade.

Questrade has long been known as the top discount brokerage in Canada due to its low fee structure, free ETF purchases, and stock trading for as low as $4.95. Questrade has also been around the block for 20+ years and built a solid reputation for its robust platform, market research, and customer service.

If you’re the type of investor who has more advanced trading needs, or someone who needs to hold more than just an RRSP, TFSA, or non-registered account (like a LIRA, RESP, Joint investing account, or Corporate account), then the Questrade platform is still an excellent choice.

I like the no-frills approach to Wealthsimple Trade, and I like that, as a company, Wealthsimple is committed to continuously improving their product lines. As an example, they just announced a new hybrid chequing and savings account product called Wealthsimple Cash that pays slightly better interest than the big banks.

I figured, since I will be trading frequently (by my standards) – at least once per month in my TFSA, plus a few times a year in my RRSP – and I don’t need access to more account types at this time – Wealthsimple Trade would suit my needs just fine.

Final Thoughts

I’m happy with my decision to move my RRSP and TFSA accounts to Wealthsimple Trade and finally avoid paying $9.99 per trade when I contribute money to my investments.

This platform is ideal for any investor who is comfortable in a mobile app or desktop environment and who wants to trade stocks and ETFs without paying any fees.

Wealthsimple Trade is especially suited for investors who make frequent contributions to their investment accounts, since they can buy small amounts without worrying about getting charged a commission every time. This puts more of your money to work right away, rather than saving up an appropriate amount of cash before buying (which is what I would do at TD Direct).

Open a Wealthsimple Trade account and enjoy commission-free trading.

Watch for more improvements to roll out over time, as Wealthsimple Trade hopefully adds more account types and the ability to auto-deposit from your bank account (perhaps a direct link with its new Wealthsimple Cash account?).

Too bad, with all the retirees who follow you, that Wealthsimple does not allow RRIF or RLIF accounts. I would be very interested in transferring all my accounts if this were the case

Hi Angelo, I completely agree and hope to see more account types on the product roadmap in the future.

For DIY retirees, Questrade is still a great option as it’s a more robust trading platform that allows for more account types and investment products.

And, for those looking for a bit of help with their retirement withdrawals, the Wealthsimple robo advisor option is also worth a look: https://boomerandecho.com/wealthsimple-case-study-robo-advisor-retirement/

Rob, great article on zero commission Wealthsimple trading platform. Do you know if they will accommodate set up of DRIPs for those stocks that offer them (usually additional stock of a company can be acquired at a discount) for any of the accounts they currently offer? Also, for non-registered accounts do you know if they will accommodate transfer of margin accounts?

Hi J-Bay, I assumed the answer was ‘no’ to each of your questions, but I reached out to Wealthsimple for clarification anyway. Here’s what they had to say:

“There’s no concrete timeline for DRIPs (but it’s on the roadmap). Margin accounts are not on the roadmap so I wouldn’t expect it in the near future for right now.”

Thanks for the article Robb. I wasn’t even aware Wealthsimple offered this.

Are LIRA accounts transferable? Any plans for RESP accounts?

Hi Brian, thanks for your comment – I’m glad you found the article useful. I know that more account offerings are on the product roadmap, along with features like pre-authorized contributions. Unfortunately, LIRA accounts aren’t transferrable until that account type comes available. Likewise, RESPs are not available at the moment. I’ve kept our kids’ RESP account at TD (e-Series funds) for now.

Does Wealthsimple have the ECN fees that Questrade has? Those can add up when you have a large amount of shares.

Hi Emily, you’re right – ECN fees at Questrade often go unnoticed (or unmentioned) but can really add up.

No, Wealthsimple Trade does not charge ECN fees. The only trading fee they charge is a currency exchange fee for USD trades at the daily corporate rate + 1.5% — most brokerages charge around 2% on top of this rate for currency conversion.

It truly is a commission-free trading platform!

Interesting article.

Good to loose ECN Fees.

To avoid 1.5% currency exchange fee is Norbert’s Gambit possible?

Questrade offers more than market and limit orders. Does Wealthsimple offer more? For example “Trailing Stop-limit Order”.

Do you or anyone have a link to a full list of order types available? I’m curious if more is available on a more expensive platform than discount brokerages like Questrade?

Thanks

Hi Jeremy, best to think of WS Trade as a no-frills platform. It’s not trying to compete with the other brokerages on all the bells and whistles – it’s offering basic trading functionality. If your needs are any more sophisticated than ‘basic’ then you’re better off with a platform like Questrade, or one of the big bank brokerages. It looks like just market orders and limit orders are available.

You can read a list of FAQs here – https://tradehelp.wealthsimple.com/hc/en-ca/sections/360002249634-Trading-Account-Activities

One other downside you don’t mention is that a number of stocks and ETFs aren’t available on the platform. There are a number of limits, and I quote:

“in order to purchase an asset on Trade, it must:

be a common stock or ETF,

be actively listed on a supported exchange (NYSE, NASDAQ, TSX, TSX-V),

be CDS eligible,

have a 52-week high price that exceeds $0.50 (stocks only, excl. new issues like IPOs),

have an average daily volume that exceeds 50,000 shares (stocks only, excl. new issues like IPOs),

and be the Canadian-listed security if dual-listed”

See https://tradehelp.wealthsimple.com/hc/en-ca/articles/360012164133-Why-can-t-I-find-the-particular-stock-or-ETF-I-m-looking-for-

That being said, I opened a TFSA on Wealthsimple Trade and it’s been a great, easy, and cheap way to dabble in DIY investing.

Hi Mark, thanks for this. As I said to Jeremy, the platform is built for basic trading needs. You’re not going to find penny stocks or stocks traded over-the-counter (OTC). All of these constraints apply to stocks and not ETFs.

That’s another downside I failed to mention: the notion that zero-commission trading might turn investors into day traders. As an ETF investor, my interest in this platform is strictly about the ease of use and saving fees.

that’s a serious limitation. many canadian etfs, units warrants and even some equities on tsx trade less than 50K shares average. And what about drips? do they support drips on stocks and etfs? simple wealth building requires drips for dividend investors, the cornerstone of simple low fee compounding.

Also no mutual funds, and preferred shares, both basics, means many would need several accounts at different institutions (not to mention options). I once had a interactive brokers account because option contracts were so much cheaper, but it was the opposite of simple. I hope some broker in canada can crack that one of these days,

Do they offer account performance tracking?

Hi Azul, yes you can track your account’s performance over 1 day, 1 week, 1 month, 3 months, 1 year, and all-time. It’s not as robust as what I was used to with TD, but it does the trick.

Robb, how do you transfer money (monthly ‘dividends’) from Wealthsimple or Questrade to my bank account?

Hi Brien, in Wealthsimple Trade you can withdraw available funds to your linked bank account.

Hey Robb, great article (as usual). I get the no fee for purchases in the applicable accounts. Are they any fees associated with selling shares/units?

Thanks

Hi Rod, thanks! There are no fees to buy or sell stocks and ETFs. Zero. None. $0.

Can you transfer funds out of an RRSP to the linked bank account without any fees? My bank (TD) will charge $25.00 per transfer out -i.e. funds withdrawn before having to convert to a RRIF . And it cannot be done electronically – you always need to visit a branch or call it in to the WebBroker desk.

Hi Gerald, yes you can. Here’s the super-easy process:

Tap the Home Screen, then select ‘transfers’, then ‘withdraw funds’.

It will ask you to select the account from which you want to withdraw, and how much is available to withdraw (cash available).

Select ‘RRSP’ and then ‘continue’. You’ll see this note:

“What’s the reason for this withdrawal?”

– Home Buyers’ Plan

– Lifelong Learning Plan

– Neither of the above (I’m withdrawing from my RRSP for another reason and understand there may be tax implications)

Select the third option and tap ‘continue’. You’ll see this note:

“Are you sure? RRSP withdrawals often have tax implications, with a few exceptions. If you’re not withdrawing for an exempt reason, we recommend withdrawing from another account.”

Select ‘I’m sure’. You’ll see this note:

“You have $xx.xx available to withdraw from your RRSP account.”

Select your desired amount and tap ‘continue’.

That’s as far as I was willing to go in my own account – but you get the idea 😉

Nice review Robb. I just opened an account myself so I can buy small amount of shares of an ETF. If I stayed with RBC it would have cost me $9.99 per trade.

If WS Trade does not offer RRIF accounts, does that mean that when your RRSP has to be converted at age 71 you would have to move it to another institution?

I’m also interested in Gerald’s question about whether or not there is a charge, like the $25 TD charge, for withdrawing RRSP funds?

Is it accurate that WS Trade will not allow joint taxable accounts?

Are Mutual Funds on the horizon? Now that TD allows the purchase of the e-series funds at other institutions it would be nice to have that option?

How does WS Trade make their money? Surely just charging 1.5% on currency conversion isn’t their only source of profit.

Hi Robb, I have been reading on your site for awhile now and have now moved my RRSPs to TD and purchased VBAL last year. Unfortunately to fill the order it took 3 trades therefore $30. Therefore for my TFSA, I am considering trying WS Trade after reading this. Please bear with me as I am new to this, so my questions are: 1) I plan on putting $5k CAD into either VBAL or VEQT, therefore there is no 1.5% charge if these are bought? 2) CIPF is as secure as CDIC? Please advise and thanks for all the information. This is a great site!

Hi Surya, thanks for your comment. You won’t be charged anything when you purchase those ETFs with Canadian dollars. The 1.5% currency conversion spread only comes into play if you were to buy a U.S. listed ETF (like Vanguard’s VT) with Canadian dollars.

CIPF is not the same as CDIC. It does not protect the value of your account (since markets move up and down). Instead, CIPF’s role is to ensure that clients of an insolvent member firm receive their property held by the member firm at the date of its insolvency.

Say you buy 100 shares for $5000, and the shares are held in an account with a CIPF member firm. If your CIPF member firm becomes insolvent, CIPF’s objective is to ensure the 100 shares are returned to you. CIPF does not protect or guarantee your initial investment of $5000.

However, if the 100 shares are missing from your account, CIPF would provide compensation based on the value of the missing shares on the date of the member firm’s insolvency.

Hi !

Thanks for tipping us all !

I am just wondering if it’s really worth the shot.

We’re all investing for our retirement and for that matter, all of us will be often be buying instead of selling. In that context, Questrade or WS are the same.

Also, selling ETFs is max 10$ each time. Unless you’re planning to retire soon, this fee does not matter right ?

Also, even if you retire next month, you can still move all your assets from Questrade to WS and sell there your ETFs : is it sane to think like that ?

Plus : Questrade is better for those who are planning to start a business because they can get familiar with their tool before opening a corporate investing account.

============

I am planning to buy some VEQT and VGRO : is there any advantage of putting one of them in a TFSA instead of a RRSP ?

Hi Robb,

Great review and thanks for offering your experience with this new online broker. Wondering since you’ve written the article how you are finding WealthSimple Trade thus far (i.e. with the market volatility)? Are you still able to successfully buy/sell?

I tried to sign up, but was put on a “waiting list”!? Never thought this would happen in Canada in 2020. First no toilet paper in stores and then waiting lists to sign up with an online brokerage? I know with the virus things have changed somewhat, but this is silly.

Hi Sam, thanks for your comment. Interesting to hear about the wait list – that’s the first I’ve heard of it.

I can confirm that WS Trade had some intermittent outages at the beginning of the market crash but I haven’t noticed any issues since then. I’ve had no problem at all adding funds and executing trades.

Hopefully they’re able to get through these delays in opening accounts. I do like the platform, so I hope WS invests appropriate resources to ensure its success.

Will I be able to connect my CIBC account to WealthSimple? When I tried, Wealth

Simple told me to contact my bank. Do you know if that will work? I imagine you have quite a few customers that use CIBC.

Log out. Try again (a few times if needed). I had a similar problem for some reason.

If not you can manually enter the details (transit, acct. #) and show a copy (picture) of your bank statement.

How do the reports prepared for tax time (for non-registered accounts) compare to your experience with TDDI? Do they help to simplify the tax preparation process (calculating adjusted cost base, summary of dividends, T3 and T5 statments, the usual)?

Hi there, how will my american currencies be transfered into my WS trade account? will they just be converted based on the current corporate conversion rate?

Is there any admin fees other than currency exchange fee? I’m most interested in two fees – 1. RRSP withdrawal or closing. 2. Account transfer out.

Hi,

I understand that WealthSimple charges USD conversion fee of 1.5% , so if i buy VEQT funds, would they be charging me conversion fee since part of the VEQT ETF is in USD? And, also if i sell these funds, the conversion will take place again? Thanks

Hi Robb

Do you know if Wealthsimple reimburses transfer fees for non registered accounts? I called them today and they said they only cover TFSA and RRSP accounts. There is no mention on their site regarding not reimbursing non registered (personal) accounts.

Hey.

Do you know if wealth simple takes canada learning bond amount ($600 per child) when you transfer from TD ? I heard during transfer this money go back to government.

Unfortunately you can’t open a joint investment account. This is a real downside, if one is married and wants to leave a tidy estate.

You should mention that currently you can only hold Canadian dollars. EVERY time you do a foreign trade it will convert it, so you will pay 1.5% when you BUY the foreign stock. And then you will pay 1.5% when you SELL the stock because it has to convert back in to Canadian dollars in to your account.

WealthSimple says they plan to add USD Accounts so that you don’t have to keep converting it, but there is no timeframe for that.

Thanks for this excellent article, Robb, and for updating it to include the fact that Wealth Simple Trade now offers a desktop trading platform as of January 2021.

So if I want to transfer a TD Direct Investing RRSP or TFSA to Wealth Simple Trade and the TD account currently holds only mutual funds (TD D series funds and e-funds), what steps would I need to take given that you can only hold stocks and ETFs in Wealth Simple Trade accounts?

If I sold all the mutual fund holdings in the TD account into cash, could that account then be transferred to Wealth Simple Trade?

Also, can a Spousal RRSP or a Locked-In RRSP be transferred to Wealth Simple Trade?

Thanks,

Robb

Hi Brendan, no need for you to sell the mutual fund holdings yourself (although you could). What I’d do is open the WS Trade account, open an RRSP and a TFSA, then select ‘transfer from another institution’, and select ‘transfer in cash’.

Wealthsimple’s back office will send the request to TD Direct’s back office, sell the mutual funds, and send a cheque to Wealthsimple to fund your accounts.

No, WS Trade does not have spousal RRSPs or LIRAs at this time.

Thanks very much, Robb, for your very clear, concise, and helpful response to my questions.

Hi Robb

Great to see a good review. I’ve tried getting ahold of anyone from Wealthsimple on the phone to answer my questions but no luck..just put on hold until the call drops.

I’m a beginner investor that has a trade account with Wealthsimple. Since opening I have made some trades. Invested a fair amount. $10+. I just recently realized that you can trade from a TFSA account (avoid capitol gains) so i opened one within Wealthsimple since never contributing into one. I should have $75,000 to transfer over. What I would like to know is should I sell my stocks one at a time and move them over to the TFSA account? (3 day delay to and from of course) Does this make logical and financial sense? They state that they cant transfer stocks over to one another.

Hi Robb, are you referring to your TD E-series investment being transferred to Wealthsimple? Thanks.

Hi Joanne, my RRSP and TFSA were invested in VEQT at TD Direct, so I moved this over “in kind” (or “as-is”) instead of in cash since I wanted the same investments at WS Trade.

I still have TD e-Series funds in my kids’ RESP at TD Direct.

Hi Robb,

Do you advice me to only invest in Canadian shares to avoid the +1.5% exchange rate fee.

Thanks a lot

Thanks for the informative article. I would like to transfer to Wealthsimple, but I find their communication to be frustrating. It takes 5 business days for them to reply via email and its impossible to get someone on the phone. If something happened to Wealthsimple as it did to Robinhood with the game stock, there would be no way to even reach them. When it comes to money/finances I think they should have a support line with available reps.

You get what you pay for. WS charges no trade fees and thus they have to save money somewhere. Support staff and representatives is almost certainly one of those areas. If your trading needs are such that you need a faster response or the ability to speak with your broker on the phone, well then go with a one of the major banks, TD/RBC. But, you’ll pay more fees to receive the support it seems you want. It is unrealistic to expect WS to offer TD/RBC levels of customer support at a considerably lower price point. If they did that they wouldn’t be in business for long.

Thanks for the great review, Robb.

Hoping you could answer a question on fees. I’m looking to open an account with them but want to be aware of all their fees. I sent an email close to 2 weeks ago and no answer. Could you explain when the “Special Requests & Investigations for $75/hr” would apply? Same with “Voluntary Corporate Action/Election for $50? I’m not sure I’ll ever need them but I want to avoid finding out the hard way. Thank you in advance.

Hi Michael, my pleasure. I highly doubt you’d ever come across either of these situations. Wealthsimple Trade explains that these represent transactional fees that would only be incurred “if the specified action were requested by the client and the request is approved by a Wealthsimple Trade representative.” Go ahead and Google what a voluntary corporate action is.

Remember, this is a bare-bones platform that comes with no advice. It’s no surprise that you didn’t get an answer to your question. They might even consider that a “special request and investigation” and charge you for the time. I’m kidding, but want to reiterate that if you’re expecting big bank levels of customer service and support, WS Trade is not going to meet your needs.

There are no fees to buy and sell stocks and ETFs. The “gotcha” fee is truly the 1.5% foreign currency conversion fee charged whenever you buy/sell a US-listed stock or ETF. This is because WS Trade does not allow you to hold USD cash.

The platform works great for investors who buy CAD listed stocks and/or ETFs. If you want it to do anything beyond that you’ll likely be disappointed.

“The “gotcha” fee is truly the 1.5% foreign currency conversion fee charged whenever you buy/sell a US-listed stock or ETF. This is because WS Trade does not allow you to hold USD cash. The platform works great for investors who buy CAD listed stocks and/or ETFs. If you want it to do anything beyond that you’ll likely be disappointed.”

Thanks Robb, good review. You answered all my questions. WS seems like a decent low cost option for investors who want to keep it simple and stay in CAD. That said, re: USD fees, you should add your comment above and perhaps an example to your review as a clear con and cautionary note.

1.5% on the purchase and sale of US-listed stocks or ETFs. Purchase $50,000 in USD stock and then sell that stock for $55,000, that is $1575 in foreign exchange fees! I guess WS is hoping new clients who may be buying in smaller dollar amounts won’t notice as much. But, even if you only buy $1000 USD in stock and sell at $1100, that’s $31.50. That’s much more than Norbert’s Gambit costs with Questrade or even one of the big banks.

Great overview! I’m a big fan of Wealthsimple Trade as well. I also used to use TD but the 9.99 fees were forcing me to make bigger transactions than what was appropriate for me at the time. Now with WST often just buy one or two stocks at a time, and have a much easier time balancing my portfolio =)

Hi Robb

Great post. I do have a question regarding the transfer process, but first let me explain my situation. I have an individual margin non-registered account in my name at TD direct investing. I would like to do an in-kind transfer out of TD to either National Bank Discount Brokerage or Desjardin Disnat. My plan is to transfer my securities out of TD into another individual non-registered account (in my name) and convert that individual account to a joint account (my wife being the joint holder). I talked to a representative at Disnat to see if this was possible and they said that it is possible, but it can produce a capital gains/loss event during the transfer (their explanation wasn’t very clear). I talked to various people and got mixed messages about where the actual capital gains/loss even occurs. I then asked the CRA for their perspective and they said that the capital gains/loss event only occurs during the transfer of securities from an individual account to a joint account (not from an individual account to another individual account with the same name), they said something about this event being called a deemed disposition. That being said, can you tell me:

Did you do any in-kind transfers into Wealthsimple from a non-registered account?

If yes, did that trigger any taxable events for you?

I am not asking you for advice on which situations are deemed dispositions, but I just want to hear from your experience. Many thanks.

Cheers,

Lawrence

Hi Robb

In the section above with the header “Wealthsimple Trade vs. Questrade” you write that you trade monthly in your TFSA and a few times a year in your RRSP. Considering that you had 100% VEQT in these two accounts, I’m not clear what (or why) you would be trading that costs you a fee (considering that purchasing ETFs has no fee in Questrade). Thanks

Hey Chad, this article was originally written a little over four years ago.

I’m not positive but I may have been referring to ECN fees at Questrade, which are tiny but not nothing. The underlying point was WS Trade suited my needs for frequent free purchases in an RRSP and TFSA.