Weekend Reading: What’s Going On With Bonds Edition

Bonds are meant to be the ballast that helps smooth out volatility in your portfolio. They act as a cushion – the steady yet unspectacular asset class that balances the unpredictable movement of stocks. But a sudden decrease in bond prices has investors looking for answers.

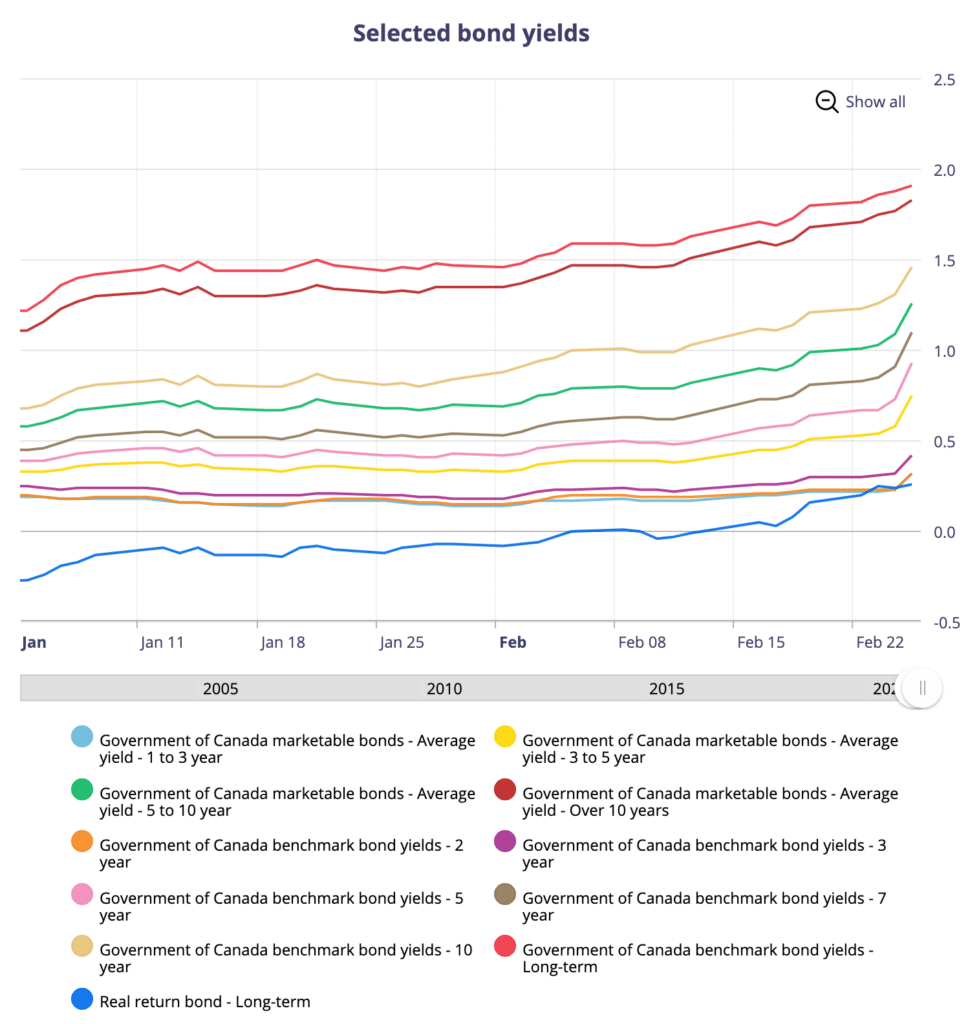

In short, bond yields are on the rise because investors are optimistic about future economic growth. The U.S. 10-year Treasury yield climbed to its highest level in more than a year. Here in Canada, 10-year government bond yields have more than doubled since the beginning of January.

Rising rates spell trouble for bond prices, though. Long-term bonds are particularly sensitive to changes in interest rates. A good way to measure that sensitivity is by looking at a bond's duration. A bond with a duration of 5 years will see its price fall by 5% if interest rates rise by 1% (and vice versa).

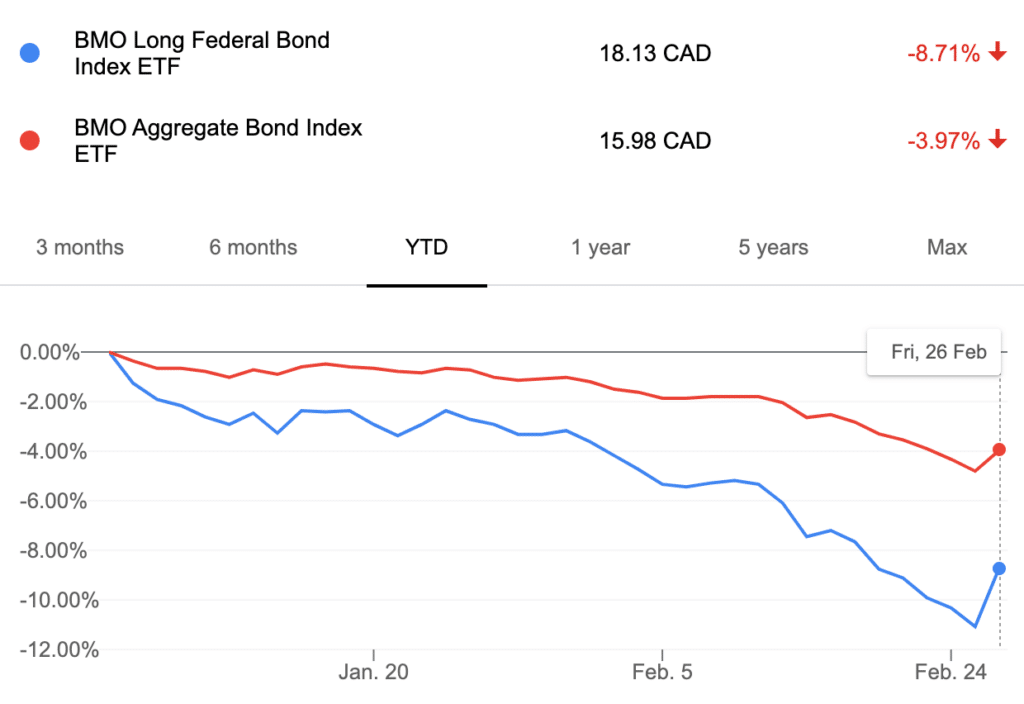

BMO's ZFL, which tracks Canada's long-term federal bond index, has an average duration of 17.94. The price of ZFL fell by 11.08% as of Thursday before a slight uptick in prices on Friday. BMO's popular ZAG ETF, which tracks the Canadian aggregate bond index, has an average duration of 8.1 years and its price was down 4.81% as of Thursday.

Short-term bond ETFs have a lower yield but they are less sensitive to interest rate movements and more preferable to hold in a rising rate environment.

The iShares Core Canadian Short Term Bond Index ETF (XSB) has an average duration of 2.71 years. Its price is down just 1.10% on the year, compared to the iShares Core Canadian Universe Bond Index ETF (XBB), which has an average duration of 7.91 years and is down 3.87% year-to-date.

The silver lining for bond holders is that you're still getting interest payments from your bonds, and those payments should eventually rise as new bonds are purchased at higher interest rates. That's why investors with a long time horizon should stick to their plan and rebalance – buying bonds at low prices and higher yields.

Retirees, on the other hand, should consider the average duration of their bonds and determine if it's appropriate for their age and stage of life. Clearly, holding long-term bonds when you have short-term spending needs is not a wise strategy.

Fears over rising interest rates have plagued investors for the past decade. As this 2011 article from Canadian Couch Potato Dan Bortolotti explains:

“The key message for investors: as long as your time horizon is at least as long as the duration of your bond fund, you won’t lose any capital. Any price decline from rising interest rates will be offset by higher coupons within that time frame. In fact, history suggests the recovery is likely to be more swift than that: even a three-year period of negative bond returns is extremely rare.”

This Week's Recap:

Earlier this week I wrote my annual letter to Engen Householders.

Read the Oracle of Omaha Warren Buffett's annual letter to Berkshire shareholders here.

From the archives: Why I Don't Hold Bonds in My Portfolio.

Promo of the Week:

The American Express Cobalt Card is arguably the best ‘hybrid' card in Canada. Cardholders earn 5x points on groceries, dining, and food delivery, plus 2x points on transit and gas purchases.

New Cobalt cardholders can earn 30,000 points in their first year (2,500 points for each month in which you spend $500) plus, you can earn a welcome bonus of 15,000 points when you spend a total of $3,000 in your first 3 months.

Sign up for the Cobalt card here.

Weekend Reading:

Our friends at Credit Card Genius share how you can take advantage of record low interest rates in Canada.

Jim Wang at Wallet Hacks brilliantly explains what you should do with all the financial advice on the internet.

A fantastic piece by Morgan Housel on investing and speculation – when everyone's a genius.

For Globe and Mail subscribers, Rob Carrick explains that what's happening with housing and stocks is not normal:

“Gen Xers, boomers and older generations have one benefit young adults lack in making sense of what’s happening now – perspective. If you opened your eyes to personal finance and investing in the pandemic, you’re seeing things that may never happen again. Take advantage, and take care.”

What would Warren Buffett make of this stock market silly season? He's already told us.

A perfectly timed new video by PWL Capital's Ben Felix on the pitfalls of chasing star fund managers:

With the 2020 RRSP deadline fast approaching, My Own Advisor Mark Seed shares RRSP facts you must remember this year and beyond.

Michael James on Money explains that the great thing about managing other people's money (from a fund manager's perspective) is you can dip into it to pay yourself.

On the Evidence Based Investor, Larry Swedroe looks at the odds of outperformance through active management.

A Wealth of Common Sense blogger Ben Carlson debunks everyone's favourite hyperinflation scenario.

Of Dollars and Data blogger Nick Maggiulli sold his Bitcoin. Have fun staying poor.

Global's Erica Alini reports that fixed mortgage rates are on the rise.

Finally, this New York Times article takes an interesting look at how boredom is impacting the economy today.

Have a great weekend, everyone!

good for seniors. New Annuity will be better with higher rates.

Thank you for sharing my post on what to do with advice! 🙂

Hi Jim, my pleasure – it’s a great post!

Thanks for article and explanation. Great insight.

Thanks Robb for this great article about bonds and here i have a question for you ,do you recommend holding your age in bonds or each case is different ? I’m 50yo and I do hold 18% only in bonds and lately i was debating if i should go to holding none , I have a rental income that in a way i consider a sort of safe fixed income .

Thanks

Hi Gus, holding your age in bonds is a decent rule of thumb but as in most personal finance situations the answer depends on your unique circumstances.

I will say in my case, holding 100% equities, I had regrets during the March 2020 crash when I could not rebalance. I had no unused contribution room in my RRSP or TFSA so I just had to sit and watch my portfolio fall 34% in short order. So, bonds do certainly play a role and will in the next equity sell-off.

Thanks Robb, I think that’s the only reason why I’m keeping those bonds for the next downturn so I can buy some equity on sale.

I don’t understand why someone would buy a bond for the speculation in market price. I’ve held bonds several times in my portfolio. I purchased them because of the attractive income and for diversification. If you are trading bonds like some people trade equities, then the whole point of a bond is defeated.