Weekend Reading: Your Numbers Tell A Story Edition

When I first create a financial plan for a client I tell them that this is my initial interpretation of their current situation and future goals mapped out over time. It's a projection or road map based on their current trajectory.

I'm looking for clues, patterns, red flags, and opportunities. The numbers are telling a story about what's possible.

Here's what I mean.

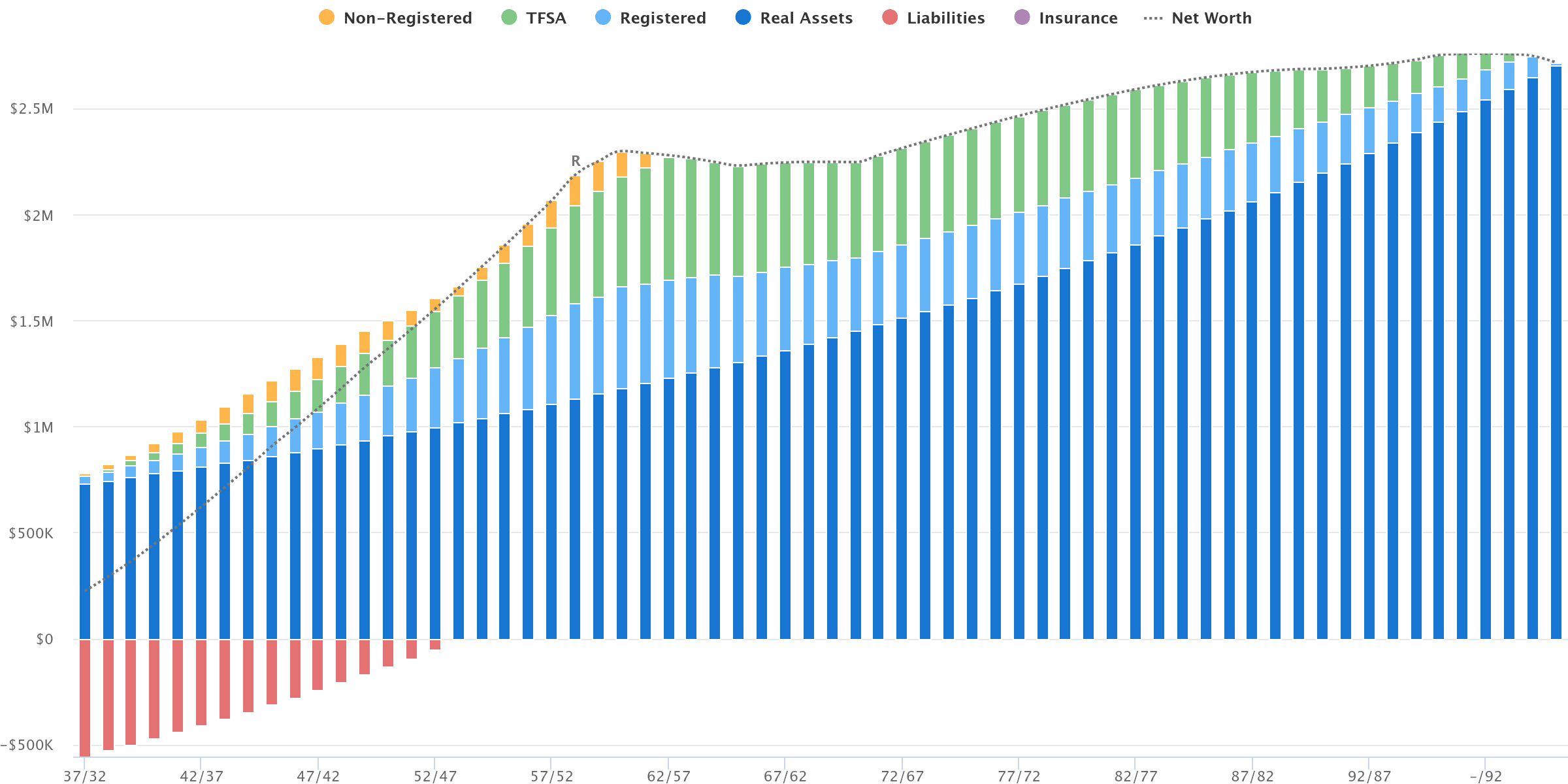

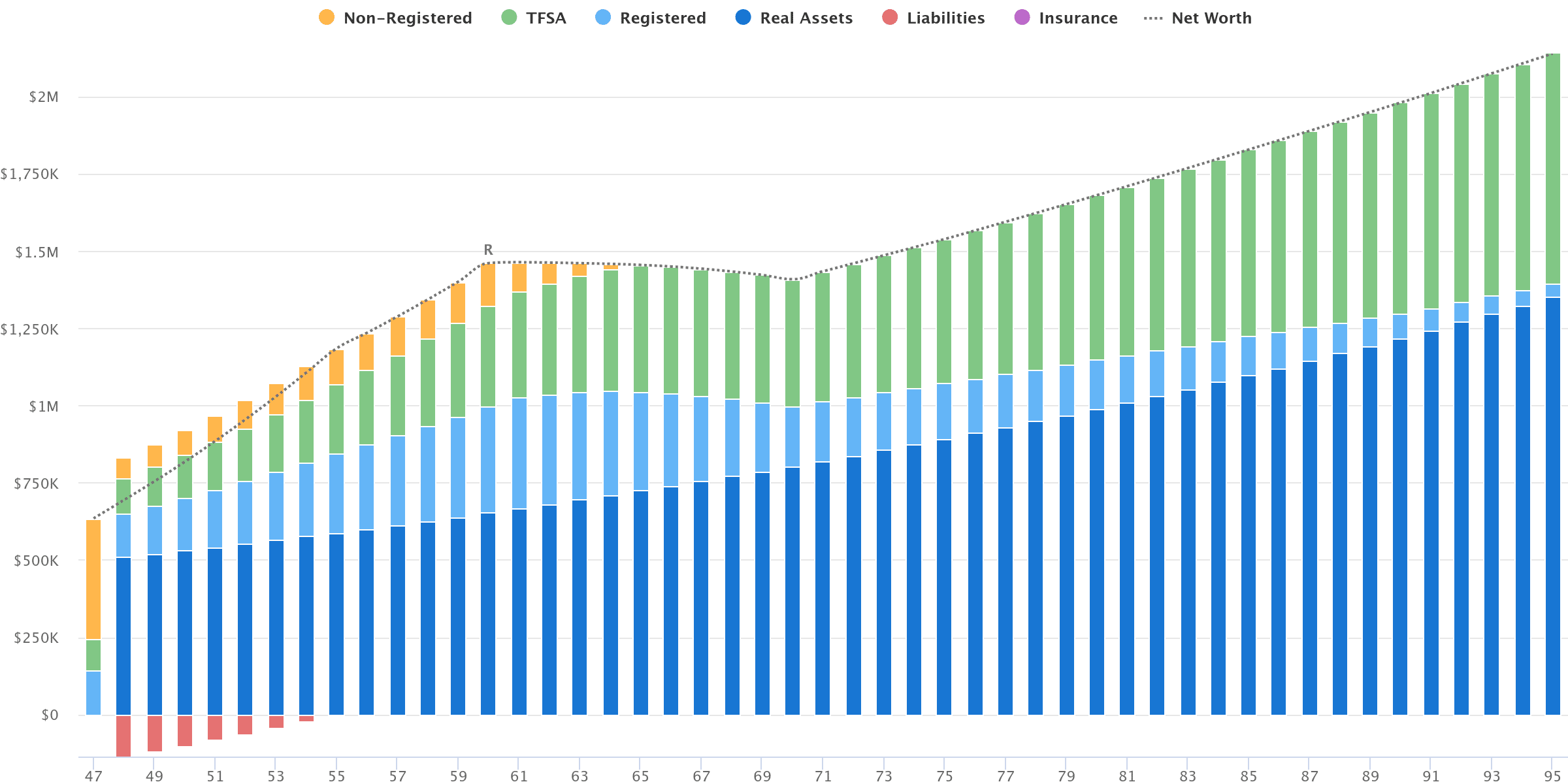

A typical net worth projection during your working years goes up and to the right. That makes sense, as you earn income, contribute to your savings, get a rate of return on your investments, and pay down debt.

But working families also have competing financial priorities. Income interruption from parental leave, child care, vehicle payments, home renovations, even upsizing a home are all real possibilities that young families are dealing with.

Your house is your largest asset and you're deep in mortgage debt. You have little in the way of savings and feel like you're not making any progress while you're dealing with one-time, temporary costs. But zooming out you can see a light at the end of the tunnel.

Child care costs subside, income increases, and mortgage payments no longer feel like they're taking up all of your disposable income. You start making some meaningful progress on your retirement savings goals and your net worth heads up and to the right.

Once the mortgage is paid off, you have options to ramp up savings and even ponder early retirement.

At this point I'm looking for clues as to whether you're on the right track to retire early, or if you'd need to downsize your home to ensure you can maintain your lifestyle throughout retirement, or if you can afford to delay taking CPP and OAS to secure more lifetime income.

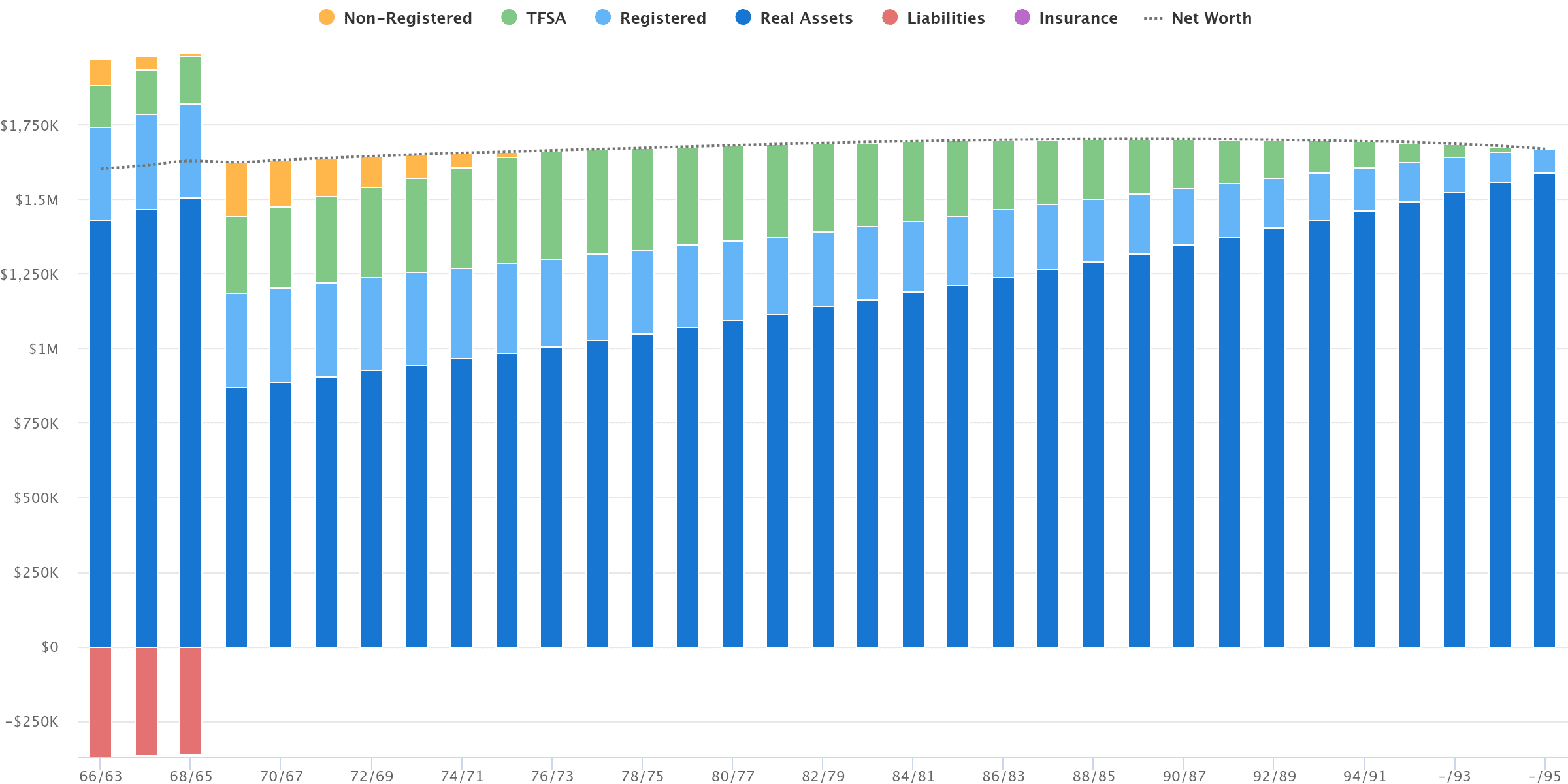

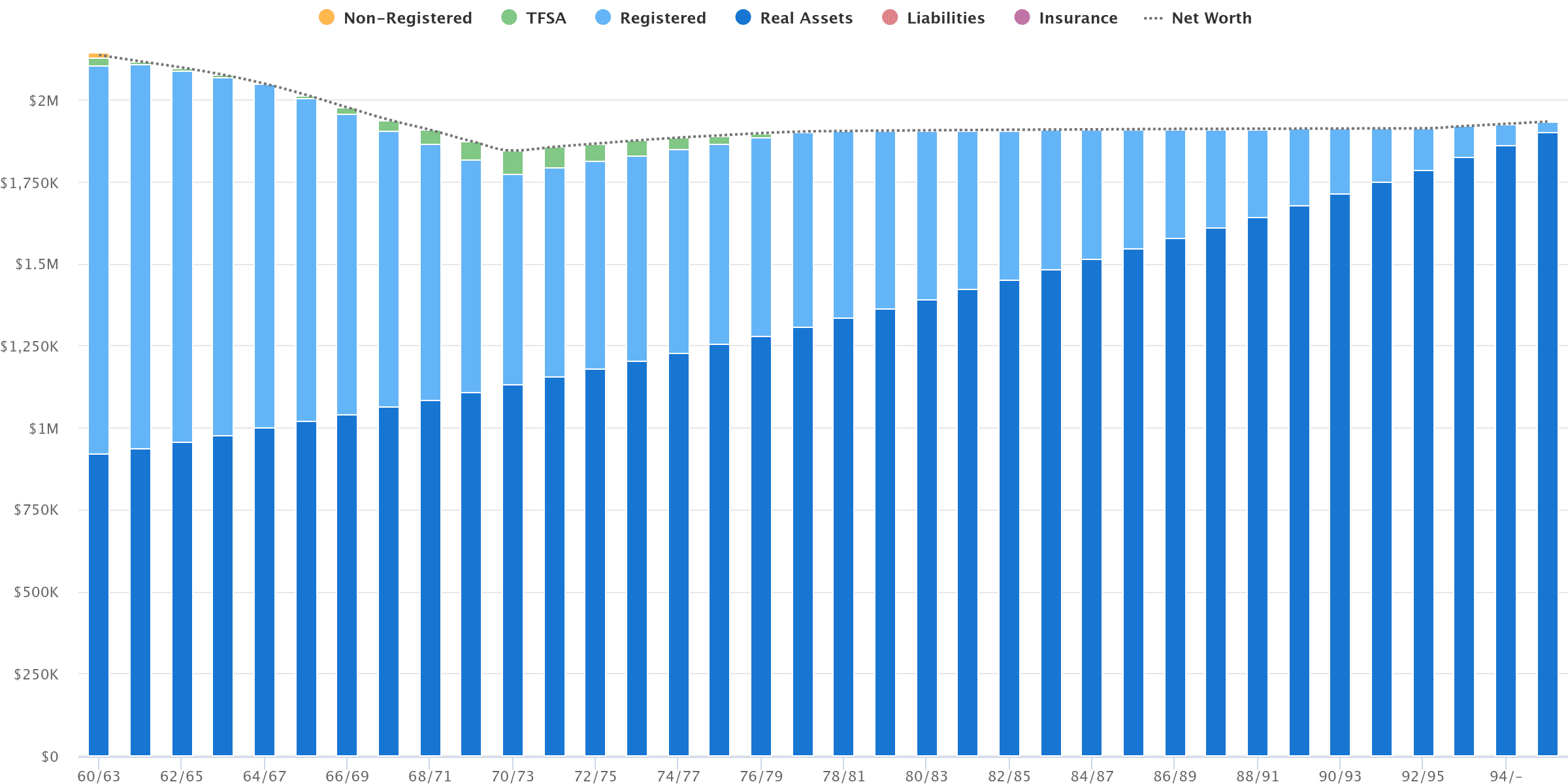

I recently wrote about a concept called your home equity release strategy and it's becoming more and more important to think about, especially in high cost of living areas where retirees may be sitting on untapped home equity of $1M to $2M (or more).

In the above example, the retired couple downsize their home at or shortly after retirement to eliminate their mortgage, add precious home equity back into their savings, and ensure they can maintain their lifestyle throughout retirement.

There is still a slight danger of running out of money in their old age, but they do have the paid off home equity in their downsized home to fall back on, just in case.

Another option is to sell the family home and rent throughout retirement. This has the added benefit of being able to maximize retirement spending, but with the trade-off of not having a fall back option to sell the home in case of unplanned spending shocks or poor market returns. A prudent spending plan is paramount in this case.

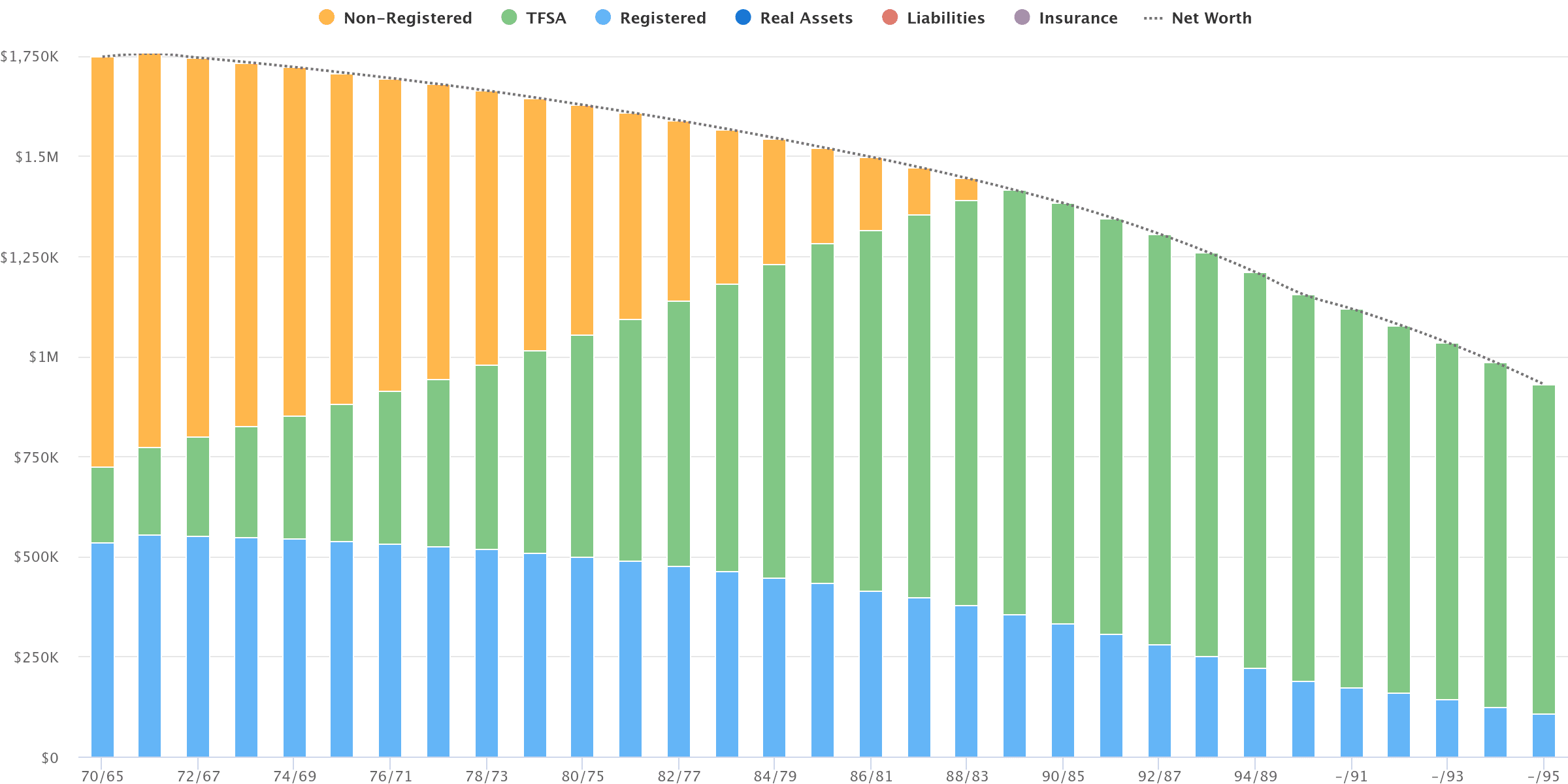

What about singles? In my experience, singles can have a difficult time in two phases of life.

One, buying a house as a single in a high cost of living area may be incredibly challenging.

Two, without the benefit of a partner with whom to split income in retirement, singles face higher tax rates and are more likely to incur Old Age Security clawbacks.

In the above scenario, this single individual was fortunate to receive a small inheritance in her late-40s to finally be able to afford a condo in her desired location and price range.

If she keeps her spending consistent with the lifestyle she enjoyed in her final working years then it's possible that she won't have to sell that condo to fund her long-term retirement spending. But, in many cases, singles who buy a home are more likely to have to downsize or sell their home to maintain their lifestyle.

Finally, several of my clients are interested in the “die with zero” approach to retirement planning. I don't love it, because spending every dollar and having your last cheque bounce leaves no margin of safety for unplanned spending shocks.

So, for homeowners looking to maximize spending, I prefer to show them a “die with zero, but stay in your house” scenario. This way, you have a fall back option to sell your home and move into a retirement facility if necessary as you run out of money.

Your numbers tell a story about what's possible. Projected over time, we can start to see patterns, red flags, and opportunities in your financial plan. We're looking for clues to see if you're on the right track or need to change course.

I'll be honest, more often than not these net worth projections show that my clients can spend more than what their current budget suggests.

But, often we do see red flags that suggest clients will need to make difficult choices about working longer, downsizing or selling the home, or reducing spending to ensure they won't run out of money.

Want to know what kind of story your numbers tell? Reach out to me and we'll come up with a financial plan.

This Week's Recap:

Have you considered your home equity release strategy?

How much do you plan to spend in retirement?

Here's how I plan to catch-up on my TFSA room.

Promo of the Week:

We activated player two for our rewards cards strategy, meaning earlier this year I signed up for the American Express Business Gold card, hit the minimum spend target to reach the welcome bonus, and then referred my wife (player two) to get the same card in her name.

The result is 15,000 additional Membership Rewards points for me for the referral, and now my wife has a chance to earn 75,000 Membership Rewards points after spending $5,000 in the first three months.

We activated player two for our rewards cards strategy, meaning earlier this year I signed up for the American Express Business Gold card, hit the minimum spend target to reach the welcome bonus, and then referred my wife (player two) to get the same card in her name.

The result is 15,000 additional Membership Rewards points for me for the referral, and now my wife has a chance to earn 75,000 Membership Rewards points after spending $5,000 in the first three months.

Weekend Reading:

Should I pay myself dividends from my company to avoid CPP premiums?

Many Canadians own foreign property. Whether its stocks, ETFs, bonds, real estate, or even crypto, you may have some tax obligations to consider.

Private credit funds are pitched as safe and stable, but investors aren’t getting anything special for the high risk and fees.

Is $1 million in savings enough to retire on if we withdraw 4% per year?

A fantastic conversation with the Canadian Couch Potato Dan Bortolotti on the Rational Reminder podcast last week:

A Wealth of Common Sense blogger Ben Carlson asks how would you invest $14 million?

RRSP to RRIF, and LIRA to LIF: Here's how it all gets done.

How Wealthsimple is trying to beat the big banks at their own mortgage game:

“I’ve seen mortgage cashback gimmicks in the past, but this one is more interesting. Unlike other lenders’ rebate offers, Wealthsimple’s calculator makes it easy to estimate the savings — and they have compelling savings options.”

Here's why variable rate mortgages are the best bet to save you money after Bank of Canada cut.

Dr. Preet Banerjee explains why AI outperforms humans in financial analysis, but its true value lies in improving investor behaviour.

Andrew Hallam shares the surprising truth: children likely increase your wealth.

Anita Bruinsma explains why divorcing parents are facing tough choices amid sky-high real estate prices.

The one place in airports people actually want to be: Inside the competition to lure affluent travelers with luxurious lounges.

Finally, Nick Maggiulli looks at when maximizing credit card rewards is worth it and when it is not.

Have a great weekend, everyone!

Hey Robb – I have been having a lingering thought for a while. If someone had a portfolio of $1MM in January 2020, appx what is the value of their portfolio as of May 2024?

I know this depends on a variety of factors (ex stock / bonds allocation), but any educated guesses here as you work with many clients. Thanks !

Out of curiosity, I looked at ours (myself and wife). It was $1,147,000 on Jan 1 2020. It’s now at $1,934,000. No major additions other than annual TFSA contributions (both myself and my wife) and annual RRSP contributions. I’m mostly all equity though with a combination of stocks and ETF’s

Very interesting DLE. I share similar growth as the numbers you’ve shared. I thought I had done “better” than the average (that may still be the case). While I shouldn’t be comparing my growth vs anyone else or the average, it is something I am curious about to gauge. If many folks have had this growth, it would make sense that the economy would thrive as people’s spending ability would be fine (in theory).

Thanks for answering.

Hi DJP, that’s a tough question to answer but if we assume no contributions or tinkering, and *some* bond exposure, it’s reasonable to think it could be worth between $1.3M to $1.4M.

Thanks Robb for answering!

Hi Robb nice article. Is your present strategy still drawing Dividends from your inc/corp to pay for day to day? Do you see the pivot to Salary or a blended approach better at all ?

Hi Rick, thanks! No changes to report at this time. If I do, I’ll definitely write about it here!