On January 7th, 2015 I sold 24 Canadian dividend stocks worth about $100,000 and bought two low-cost index ETFs (Vanguard's VCN and VXC). It was a bold move to switch to indexing after years of dividend growth investing. Lots of people questioned my decision. I even lost blog readers because of it (seriously). But it was the right thing for me to do for several reasons:

- I no longer had the patience and discipline to stick with a dividend growth strategy (buying blue-chip dividend growth stocks when they are value-priced and holding them for the rising dividends)

- I no longer had the time to keep tabs on 24 individual companies, plus research new potential stocks in which to invest

- Some of my stock picks were flat-out terrible

- I didn't have the stomach to watch my oil & gas stocks plummet 30-50 percent

- I recognized that my home country bias (all-Canadian portfolio) was extremely under-diversified, which increased the risk and reduced the potential for higher returns

- All the evidence I read didn't just suggest, it screamed, that low-cost passive indexing would outperform active management (stock picking) over the long term

Switching to Indexing

Selling those stocks was hard to do, but if you read this blog back in 2014 you'd know that I'd been preparing myself for this shift for several months.

Related: How behavioural biases kept me from becoming an indexer

So what happened since then? Talk about liberating! I used to check my portfolio on the daily and fuss over every individual stock (why is it down, why is it up, what do the analysts say?). I used stock screeners to hunt for new investments. I subscribed to email alerts for each of the companies that I owned.

Now I only log into my online brokerage when I've added new money and need to make a trade. Indeed, my four-minute portfolio is a breeze to manage. I own more than 10,000 stocks from around the globe so if one stock, one industry, or even one country is having a bad month I'd barely notice.

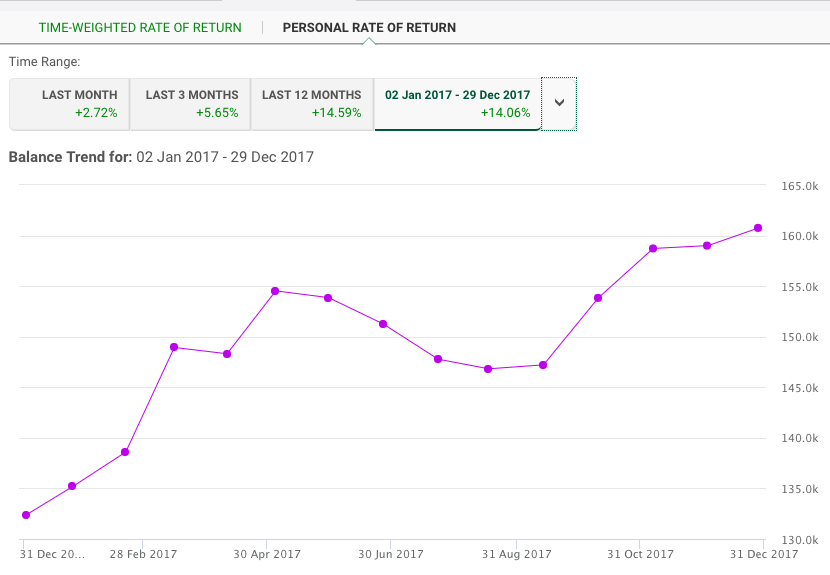

On to the big question. How has this portfolio performed? And, perhaps more importantly, how did it do compared to my old portfolio of Canadian dividend stocks? Let's take a look:

2017 Portfolio Rate of Return

2017 was a good year for Canadian and U.S. markets. The S&P/TSX Composite Total Return Index delivered 9.10 percent returns while the S&P 500 Total Return Index was up 13.76 percent for the year. Pretty good, right?

It was a good year for me, too. My personal rate of return for 2017 was 14.06 percent.

Remember, your personal rate of return, or ‘money-weighted' return, reflects the timing and amount of your contributions (and/or withdrawals), as well as the investment performance of the funds. It's different than a time-weighted return, which measures the performance of a fund or index without the effect of individual contributions or withdrawals.

All investors should now be receiving statements with their annual money-weighted investment returns.

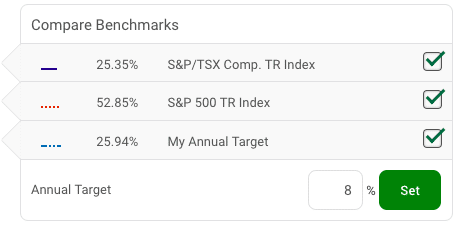

My Three-Year Returns Compared to Benchmarks

Besides freeing up incredible amounts of time, the switch to indexing has also been extremely profitable. I looked up my rate of return for the three-year period between January 7th, 2015 and January 5th, 2018.

It has been a good three-years. My personal rate of return over that time has been 41.43 percent. The annualized returns during that period were 12.26 percent. See below:

If you follow along my net worth and financial freedom updates you'll know I use a target rate of return of 8 percent for my investments. That's what I expect my portfolio to deliver over the very long term, knowing full well there will be plenty of ups and downs along the way.

I know we're in the midst of a spectacular bull market run and so I'm not patting myself on the back for outperforming my target rate of return. For instance, if the S&P 500 was down 20 percent, I'd be thrilled if my portfolio “only” lost 15 percent.

That's why I like to compare my returns against other benchmarks to see how my portfolio performed versus other strategies over the same time period. Here's a look at the three-year returns of the S&P/TSX Composite Total Return Index and the S&P 500 Total Return Index:

It's clear from these benchmarks that the Canadian market has been a bit of a laggard, dragging down my overall returns compared to the S&P 500, which has been on fire. Still, overall I'm quite happy with portfolio returns of 41.43 percent over three years…especially when you compare those results with my old portfolio.

My Index Portfolio vs. Canadian Dividend Stocks

When you look at my old portfolio of Canadian dividend stocks the best benchmark to use to replicate the strategy is iShares CDZ – the Canadian dividend aristocrats index.

This ETF holds 86 Canadian dividend stocks – established companies that have increased dividends every year for at least five years.

How has CDZ performed since January 7th, 2015? Let's take a look:

Not very good. CDZ returned just 15.01 percent for the three-year period compared to the overall Canadian market at 25.35 percent and my portfolio return of 41.43 percent.

I know every investing strategy has its moment, but as you can see I clearly picked the right time to move away from holding strictly Canadian dividend stocks by switching to a diversified global approach. I would be a lot poorer had I stayed the course.

Final Thoughts

I'm not saying indexing is the panacea for all investors. Many aren't comfortable with DIY online investing to begin with and would be better off with a robo-advisor.

Some dividend investors have the time, discipline, and temperament to stick with their strategy for the long term and their investments may perform just as well as a dedicated indexer's.

But for me, indexing has been a game-changer. I've taken back hours and hours of time. I no longer stress over one stock, one industry, or one country's performance. And, my investment returns haven't suffered – they've flourished.

If you're thinking of making a similar switch to indexing, leave a comment below or send me an email and I'd be happy to share more details.