I’ve banked with TD my whole life but while I consider myself to be a fairly loyal customer that doesn’t mean I’ll blindly accept blatant fee grabs without fighting back.

That’s exactly what happened two years ago when the big green bank announced changes to its chequing account fees and minimum balances. Their basic chequing account, which I used, charged $3.95 per month but waived the fee as long as you maintained a $1,500 balance. That was about to increase to $2,000 and I had enough.

I sent an email to an advisor at my local branch and said I’d like to close my account ahead of these changes and asked him about moving some of my automatic withdrawals to another bank.

He replied back right away with an offer too good to pass up:

“Hi Robb, I can help you with this. I would need a void cheque and some signatures, so we would need to book an appointment. If you are interested, though, I will change your chequing account to a student account. It’s a free basic account, includes 25 transactions and no minimum balance, and this way you won’t have the hassle of making a bunch of changes to any direct debits you have going out.”

Well, needless to say, I jumped at the offer and today continue to bank fee-free with TD. It’s a win for me, of course, but also for the bank as they get to keep all of my business that includes banking, a mortgage, line of credit, plus RRSP, TFSA, and RESP accounts.

A chequing account might be the linchpin that holds all of your banking needs in one place. Let that go, and it becomes easier to move other aspects of your banking as well.

So, how can you comfortably bank for free? Here are some options I recommend to avoid monthly bank fees:

Unlimited chequing account, high minimum balance

If you’re the type of person that uses a debit card for the majority of your purchases, has a lot of automatic bill payments, and requires a full-service bank for in-branch transactions then you’ll have to bite the bullet and opt for a full service chequing account.

Unlimited transactions at most banks will cost about $14.95 per month and you’ll need a high minimum balance to waive the fees. You’ll have to decide if having $5,000 sitting around in a chequing account is worth it to get unlimited banking.

Basic chequing account, still a minimum balance

The big banks were volun-told by the federal government to offer low cost accounts to consumers for $4 per month. These accounts offer bare minimum services, 10-12 transactions per month, and some will waive the monthly fee provided you maintain a minimum balance.

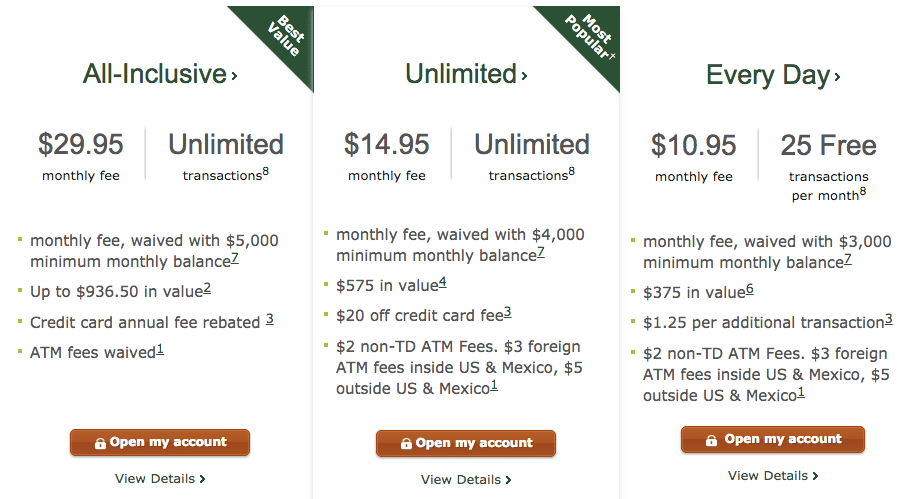

Look for terms like ‘basic’ or ‘minimum’ accounts, as they’re not well advertised by the banks and in some cases buried well below other more profitable banking options online. Here’s what’s highlighted at the top of TD’s chequing account page:

And then waaaay down at the bottom of the page you’ll find some other options:

A minimum or basic account is not a bad choice for those who use cash or a credit card for the majority of their transactions but still require the use of a full-service branch from time-to-time.

Combo: No-fee online bank + Basic chequing account at big bank

This is the sweet spot for those that have broader banking needs but don’t want to pay monthly bank fees or maintain a high(er) minimum monthly balance.

Open a no-fee chequing account at an online bank such as Tangerine or PC Financial, or at a local credit union, and pair it with a basic chequing account at a big bank, while maintaining the minimum balance to waive any monthly fees.

With the free-banking combo you can use the free account for any transactions such as bill payments, debit purchases, email money transfers (free with Tangerine) and cheque payments (free with PC Financial). Then you still have access to a full-service branch to get a bank draft, cash a cheque without a long hold, and have a wider network of ATM’s from which to choose.

I did this for several years with a Tangerine chequing account alongside my basic TD account. I got fed up when the minimum balance kept increasing (from $1,000 to $1,500 to $2,000).

No-fee online bank or credit union

Let’s face it, technology has changed the way we bank and unless you have complicated banking needs most customers can pretty much get the same level of service from an online bank or credit union as they can at a full-service bank.

The biggest difference: no fees. I’ve received countless emails from readers who have banked at PC Financial for over a decade and rarely paid a fee or ran into an issue where the no-fee bank couldn’t meet their needs. Plus, PC Points!

Credit Unions are also becoming more competitive and offering low or no-fee accounts to attract your business.

Just ask

It’s an annual ritual for some Canadians to call up their telecom provider and negotiate a better deal on their cable, internet, or phone charges. We should be doing the same for our banking. You always see awesome deals and promotions to attract new customers. What about an incentive for their existing customers? Since the bank is not going to just freely offer everyone a better deal, it’s up to you to ask (or demand!) one.

Related: Want a better deal? Just ask.

Final thoughts

Banks continue to make it difficult for customers to avoid monthly bank fees by increasing the minimum balance required or eliminating that option altogether.

You might not luck into a free full service bank account like I did but you’ll increase your odds if you have a back-up plan. There’s no harm in opening a no-fee bank account online and trying it out for a few months. Then, if you like what you see, go to your main bank with offer in-hand and threaten to close your account.

Keep in mind that the only way this negotiating tactic will work is if you’re actually willing to walk away. For some, it’s too much hassle to change their banking, but if you’re serious about saving money on bank fees you need to have an exit plan.

Readers: How do you avoid monthly bank fees?