It’s common for investors to be concerned about inflation because it brings to mind the high inflationary period of the 1970s that completely wrecked stock and bond returns. It’s also easy for investors to draw spurious conclusions about government debt and linking that to the hyperinflation that occurred in Zimbabwe or Venezuela. This article aims to set the record straight about inflation and let investors know how to invest during periods of high inflation.

Are We Experiencing High Inflation?

Inflation is one of the biggest concerns as we near the end of the global pandemic and economies begin to re-open. Governments around the world spent record amounts to keep their citizens, small businesses, and corporations afloat over the past two years, while a majority of those still employed were able to save money thanks to an economy devoid of travel and entertainment.

The result was a significant uptick in savings rates, with Canada’s household savings rate reaching a high of 28.2% in July 2020.

All this money sloshing around on the sidelines has been and will continue to be deployed into goods and services, creating additional demand for a still strained global supply chain. Consumers are ready to dine out in restaurants, attend concerts, and engage in “revenge travel” to make up for lost time.

When that happens, prices tend to rise. Canada’s consumer price index (CPI) has been rising steadily since March 2021. The 12-month change in the CPI for February 2022 was 5.7% (Stats Can). That’s well above the Bank of Canada’s 2% inflation target, and even above their acceptable range of 1-3%.

Meanwhile, the U.S. inflation rate soared to 7.9% in February 2022. (Trading Economics).

Both the Federal Reserve and the Bank of Canada previously signalled they were willing to let the economy run a little hotter than usual to make sure we achieve so-called full employment. But both central banks are now in tightening mode, raising interest rates by 0.25% in March 2022 to kick-off a series of expected rate hikes for the rest of 2022.

It’s clear that high inflation has arrived and persisted for longer than expected. The question is what should investors do about it (if anything)?

How Investors Should Position Their Portfolio to Deal with High Inflation

What exactly is an inflation hedge? In an episode of the Rational Reminder podcast, Benjamin Felix said an inflation hedge needs the following three characteristics:

- It will correlate positively with inflation, including responding to unexpected inflation.

- It won’t be too volatile

- It will have a positive real expected return

The problem, Felix said, is that asset doesn’t exist.

Indeed, most investors should just stick to their original (sensible) investment strategy and not try to change it up based on market conditions. But there may be good reasons to re-position your portfolio to try to combat high inflation. Here are some ideas to consider:

Stay Invested in Global Stocks

We don’t know for sure which sectors and individual stocks will outperform in the future, especially over the long term. That’s why it’s always wise to invest in all of them through a low-cost and globally diversified ETF portfolio.

Even if Canada or the US experiences inflation, that doesn’t necessarily mean that Europe or Asia will also be hit with higher inflation, or that global markets will react in the same way. So, we diversify that risk away by owning a global portfolio of stocks.

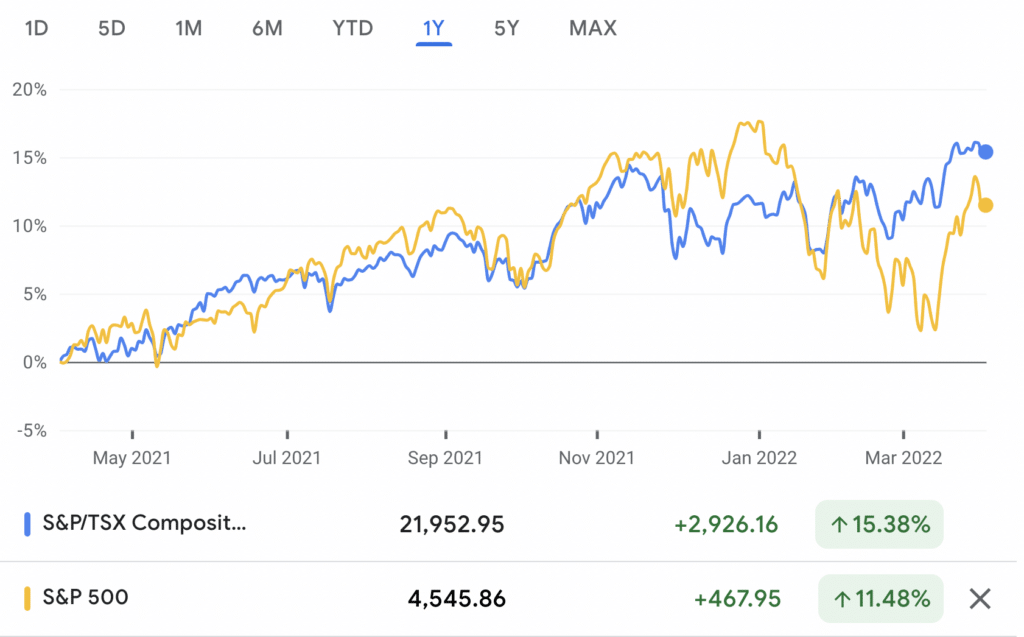

For example, Canada’s resource-driven stock market seems to have held up better than the US stock market over the past year, and in particular since the beginning of 2022. That’s not to say investors should pile into Canadian stocks – it just illustrates why diversification is so important.

Investors may look for profitable businesses that generate positive cash flow and that can raise prices. Since inflation increases the input costs for businesses (think lumber and gasoline), the ones that can respond quickly and increase their prices can keep their profit margins intact. Energy and industrial sectors have performed well during periods of high inflation. As demand for commodities rise, so do their prices and in turn their profits. Oil and gas stocks were particularly hit hard during the pandemic and are now surging higher as the global economy recovers.

It’s important to note, however, that individual stocks or sectors are too volatile to be considered an inflation hedge. The same is true for commodities.

Hold Some Cash in High-Interest Savings

It may sound counterintuitive to hold cash during periods of high inflation since the increased cost of goods is literally eating away at your purchasing power.

But consider that central banks will likely continue to raise rates to combat any sustained high inflation. This should drive up the interest rates earned on your savings deposits. This favours the idea of putting your cash in a high-interest savings account over a GIC, since you can’t take advantage of the upswing in rates when your money is tied up in guaranteed vehicles.

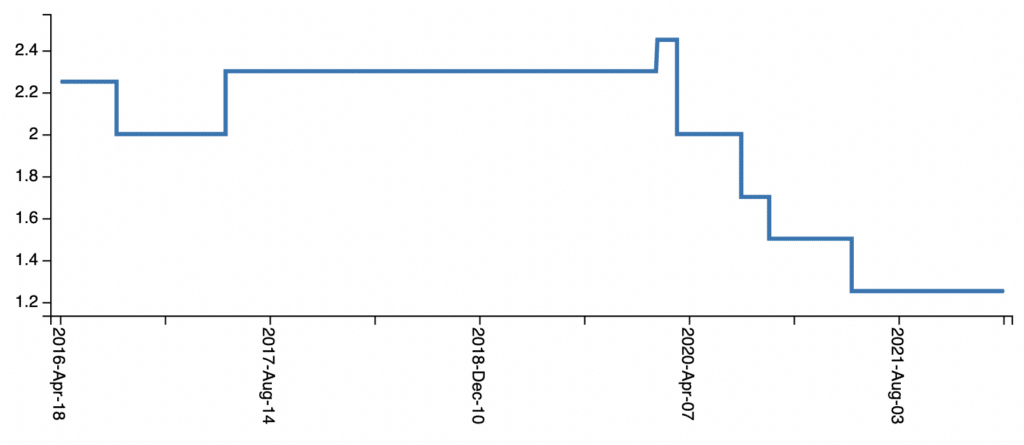

EQ Bank offers one of the leading high-interest savings account rates at 1.25%. Keep in mind, EQ Bank’s interest rate was as high as 2.45% in March 2020 before the Bank of Canada’s emergency rate cuts took hold, so there may be upside as the year goes on.

Inflation-protected Bonds

Rising interest rates and inflation are terrible for long-term bond prices. If rates increase by 1%, a bond with an average duration of 10 years would fall in price by 10%. That’s not ideal when central banks increase rates to cool things off in a high inflationary environment.

But investors who are concerned about inflation can hold US Treasury Inflation Protected Securities (TIPS), or real return bonds in Canada, for inflation-protected income. These bonds offer inflation-protected income from federal government bonds that pay semi-annual interest.

According to Benjamin Felix, inflation-protected bonds are an obvious inflation hedge if the bond duration perfectly matches your investment time horizon. However, short-term inflation-protected bonds have negative real return yields, and long-dated inflation protected bonds are too volatile to be a hedge in the short term.

Holding Fixed Interest Rate Debt

Rising inflation can actually be a good thing for fixed interest rate borrowers (such as mortgage holders) because they’re repaying their loans with money that is worth less than what it was worth when it was originally borrowed.

Think about it: Let’s say you still have a $250,000 balance outstanding on your mortgage and make payments of $1,600 per month. In a high inflation environment, your money isn’t worth as much as it used to be. So that $1,600 mortgage payment becomes less and less of a burden as wages (hopefully) rise and interest rates move up.

The bottom line – don’t be in a hurry to pay off your low-interest fixed rate mortgage during periods of higher inflation. But, don’t go actively seeking fixed rate debt as an inflation hedge. You still need to borrow sensibly, and you may be forced to renew a mortgage term at much higher rates in the future.

What About Gold?

Investing in gold has long been touted as an inflation hedge, but in reality, gold is an unreliable hedge at best over an investor’s lifetime. Researchers analyzed gold returns dating back to 1975 and found that, due to its price volatility, gold had not been a good inflation hedge over the short or the long term.

The researchers even looked at gold during Brazil’s hyper-inflationary period between 1980 and 2000 (where annual inflation averaged 250%) and found that the real price of gold in Brazilian terms fell by 70%.

One of the main findings was that the real price of gold – its purchasing power – remains the same around the world at any given time. That means if your home country happens to be experiencing periods of high inflation there is no reason to expect that gold will be a reliable inflation hedge for you.

Going back to our three characteristics of an inflation hedge, gold is not positively correlated with inflation, including with unexpected inflation, it is a volatile asset, and it does not have a positive real expected return.

Final Thoughts

Inflation has increased in Canada and the United States over the past year and that has many investors panicking to re-position their portfolios. While it’s doubtful that inflation will run out of control in our advanced and developed economies, central banks have retired the ‘transitory’ language and will be working quickly to cool inflation and return it to the target range of between 1% to 3%.

Most investors with a long time horizon should not concern themselves with temporarily high inflation numbers. With no perfect inflation hedge, investors would be smart to stick to a sensible, low cost, globally diversified investment portfolio.

Related: An evidence based guide to investing

Investors who are concerned about the impact that rising inflation may have on their investments – particularly their fixed income holdings – may consider shifting away from long-term bonds and move into short-duration bonds or treasuries as an inflation hedge.

Be mindful that the type of stocks and commodities often touted as inflation hedges are likely too volatile to offer true inflation protection.

Think of your fixed rate mortgage debt as a small hedge against inflation, since your payment stays fixed while the purchasing power of your dollars erode.

Finally, holding some cash in a high-interest savings account may offer more upside than locking it into a GIC (and certainly more upside than keeping it under your mattress or in a chequing account).