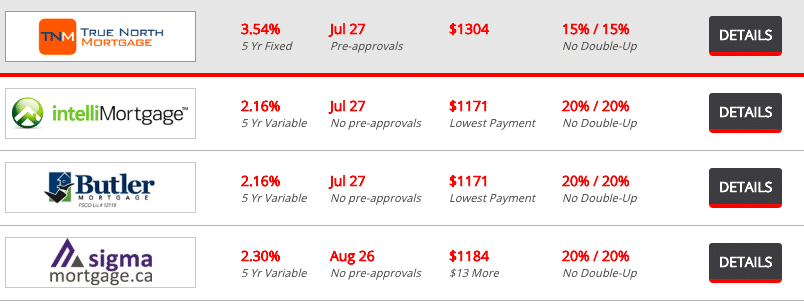

When I wrote about my mortgage renewal strategy last week a reader asked if it was a good idea to visit a rate comparison website and simply select the lender with the lowest rate. No doubt if you frequent these sites you'll have noticed the lowest mortgage rates tend to come from online mortgage brokers such as Butler Mortgage, True North Mortgage, intelliMortgage, and Sigma Mortgage.

Online Mortgage Broker Rate Comparison

An online mortgage broker offers two main benefits for its clients:

- Interest savings – Online brokers may use up to half of their commission from lenders to “buy down” the customer's rate and/or provide cash rebates. The savings is typically 10 to 20 basis points versus a big bank, which is roughly $1,800 savings on a typical $200,000 mortgage.

- Convenience – Speed and ease are the other big draws. There’s no need to drive to a branch or haggle with a salesperson who's trying to quote you advertised rates (which are rarely the bank's best rates).

The downside? There are several. For one, you may get less personalized service with an online broker. That's because their margins are much less than a traditional bank or broker, so they don't have the time or resources to spend hours counselling clients or explaining the minutia of mortgage contracts.

That lack of personalized service shows up in consumer reviews online, which can be unflattering to say the least. For example, this one from Yelp:

“Please read their BBB review before contacting this company. [Butler Mortgage] is literally fighting with one of their customers instead of trying to make peace. If you try to deal with this company you will receive nothing but horrible customer service and lies. My credit rating was affected and this company has yet to communicate with me on the status of my application after 4 months.” – Samantha S., Toronto

You might also hesitate to deal with an online mortgage broker if you're worried about not getting a name brand lender (i.e. one of the big 5 banks). Online brokers do deal with the big banks, but their best rates often come from non-bank lenders.

In this way dealing with an online broker is much like booking a hotel room on Priceline. You can get a four-star hotel downtown on the cheap, but you're blind to the exact property until you confirm the reservation. This works for a certain type of consumer who values price above all else.

With an online mortgage broker, you might get a market-leading mortgage rate but from a non-traditional lender such as MCAP, Street Capital, First National, or Bridgewater Bank.

This is less of a downside than it is a misconception from consumers, says intelliMortgage founder and CEO Rob McLister.

“That big bank mortgages are somehow better is one of the biggest fallacies in the industry. Not only are non-bank lenders typically funded by the big banks, but their mortgage terms (e.g., their prepayment penalties) are often much more favourable.”

Moreover, Mr. McLister says, there is virtually zero risk of a regulated non-bank lender going out of business and causing your mortgage to be cancelled or called-in.

Even if Home Trust would have gone out of business, for example, the trustee holding their mortgage portfolio would have sold it and mortgagors would have simply kept making their payments to someone else.

How online mortgage brokers operate

My first impression of online brokers is that they must be small shops who happen to be very good at online marketing. They buy ads on rate comparison sites to get ‘preferred' placements, and give up as much of their commission as they can afford to “buy-down” customer rates and get listed as the best deal.

With such low margins they'd have to scale their operations and gather as many mortgage applications as they can manage. Hence the lack of time and resources to answer questions or deal with complicated mortgage needs.

Most operate the same way, says Mr. McLister. You call or message them for a rate quote, apply online, speak to an underwriter to validate your application information, email or fax your documents (including the lender's approval) and close (sign the registration documents) with a lawyer or title company.

It's a bit different at intelliMortgage, as the e-broker streamlines much of the process with things like digital e-signing, online document uploads and automated status notifications. Mr. McLister says it’s the only broker in Canada that lets borrowers compare all mainstream lenders online (including those who don’t pay brokers) and customize their own rate and terms without salesperson bias.

“This last point is key because some of the very best deals in Canada are from lenders who don't deal through brokers, like HSBC.”

Final thoughts

Mr. McLister likens the online mortgage broker revolution to how E*Trade changed the investing landscape back in 1983. It puts mortgage agents and traditional brokers on notice to provide advice and expertise that justifies any cost premiums.

As consumers become more rate sensitive, and get more comfortable sharing personal data online, deep discount online brokers will continue to eat up their share of the mortgage business.

I'm one of those rate-sensitive shoppers with pretty basic mortgage needs. We don't plan on moving anytime soon, so I'm not overly concerned with mortgage penalties or portability. I do want the ability to increase my regular payments up to a point, but have no desire to put outrageous lump sums onto the mortgage each year.

Perhaps I would be a good candidate for an online mortgage broker to find me the best deal for my mortgage renewal in the fall. I'd hate to leave money on the table, especially when we could be talking potentially thousands of dollars over the life of our mortgage.