Setting up the initial asset allocation for your investment portfolio is fairly straightforward. The challenge is knowing how and when to rebalance your portfolio. Stock and bond prices move up and down, and you periodically add new money – all of which can throw off your initial targets.

Let’s say you’re an index investor like me and use one of the Canadian Couch Potato’s model portfolios – TD’s e-Series funds. An initial investment of $50,000 might have a target asset allocation that looks something like this:

| Fund | Value | Allocation | Change |

| Canadian Index | $12,500 | 25% | — |

| U.S. Index | $12,500 | 25% | — |

| International Index | $12,500 | 25% | — |

| Canadian Bond Index | $12,500 | 25% | — |

The key to maintaining this target asset mix is to periodically rebalance your portfolio. Why? Because your well-constructed portfolio will quickly get out of alignment as you add new money to your investments and as individual funds start to fluctuate with the movements of the market.

Indeed, different asset classes produce different returns over time, so naturally your portfolio’s asset allocation changes. At the end of one year, it wouldn’t be surprising to see your nice, clean four-fund portfolio look more like this:

| Fund | Value | Allocation | Change |

| Canadian Index | $11,680 | 21.5% | (6.6%) |

| U.S. Index | $15,625 | 28.9% | +25% |

| International Index | $14,187 | 26.2% | +13.5% |

| Canadian Bond Index | $12,725 | 23.4% | +1.8% |

Do you see how each of the funds has drifted away from its initial asset allocation? Now you need a rebalancing strategy to get your portfolio back into alignment.

Rebalance your portfolio by date or by threshold?

Some investors prefer to rebalance according to a calendar: making monthly, quarterly, or annual adjustments. Other investors prefer to rebalance whenever an investment exceeds (or drops below) a specific threshold.

In our example, that could mean when one of the funds dips below 20 percent, or rises above 30 percent of the portfolio’s overall asset allocation.

Don’t overdo it. There is no optimal frequency or threshold when selecting a rebalancing strategy. However, you can’t reasonably expect to keep your portfolio in exact alignment with your target asset allocation at all times. Rebalance your portfolio too often and your costs increase (commissions, taxes, time) without any of the corresponding benefits.

According to research by Vanguard, annual or semi-annual monitoring with rebalancing at 5 percent thresholds is likely to produce a reasonable balance between controlling risk and minimizing costs for most investors.

Rebalance by adding new money

One other consideration is when you’re adding new money to your portfolio on a regular basis. For me, since I’m in the accumulation phase and investing regularly, I simply add new money to the fund that’s lagging behind its target asset allocation.

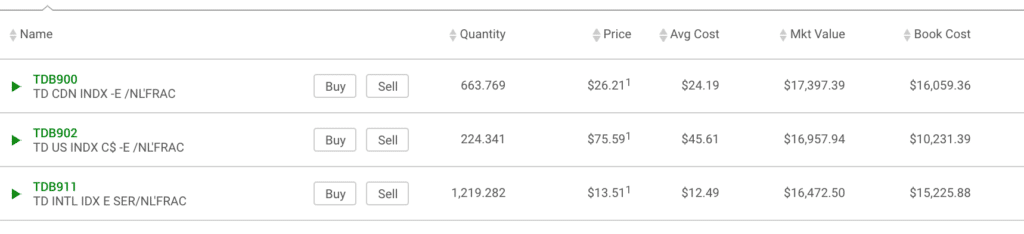

For instance, our kids’ RESP money is invested in three TD e-Series funds. Each month I contribute $416.66 into the RESP portfolio and then I need to decide how to allocate it – which fund gets the money?

My target asset mix is to have one-third in each of the Canadian, U.S., and International index funds. As you can see, I’ve done a really good job keeping this portfolio’s asset allocation in-line.

How? I always add new money to the fund that’s lagging behind in market value. So my next $416.66 contribution will likely go into the International index fund.

It’s interesting to note that the U.S. index fund has the lowest book value and least number of units held. I haven’t had to add much new money to this fund because the U.S. market has been on fire; increasing 65 percent since I’ve held it, versus just 8 percent each for the International and Canadian index funds.

One big household investment portfolio

Wouldn’t all this asset allocation business be easier if we only had one investment portfolio to manage? Unfortunately, many of us are dealing with multiple accounts, from RRSPs, to TFSAs, and even non-registered accounts. Some also have locked-in retirement accounts from previous jobs with investments that need to be managed.

The best advice with respect to asset allocation across multiple investment accounts is to treat your accounts as one big household portfolio.

That’s easier said than done if you’ve got multiple accounts held at various banks and investment firms. The goal in this case should be to simplify your portfolio and, if possible, hold the same portfolio across all accounts to avoid complexity and confusion.

This goes counter to the idea of keeping fixed income in your RRSP, and Canadian equities in your TFSA, for example.

In my experience, the simpler the portfolio, the easier it is to manage and stick to for the long-term. Imagine the nightmare of trying to rebalance multiple portfolios with different asset allocation targets whenever you add new money and as stocks and bonds move up and down.

Related: Top ETFs and Model Portfolios for Canadians

My investment accounts are super easy to manage today, with my RRSP, TFSA, and LIRA all invested in Vanguard’s VEQT. The beauty of these asset allocation ETFs is that they are a wrapper containing multiple ETFs, each representing different stock and bond indexes from around the world. The funds are then automatically rebalanced for you to always maintain their initial target mix.

If you prefer to hold multiple index funds or ETFs in your accounts, aim to keep the same asset mix across all of your accounts to avoid complexity. Follow a rebalancing strategy by date or by threshold and stick to it. And, when adding new money, contribute to the fund that’s lagging behind its target weight.

Ideally, you can avoid rebalancing altogether by using an asset allocation ETF (VBAL, VGRO, etc.), or by investing with a robo advisor where they automatically rebalance your portfolio for you.

Final thoughts

Your original target asset mix is arguably the most important decision when it comes to building your investment portfolio. Over time, as your investments produce different returns, your portfolio drifts away from that initial target, exposing it to risks that might not be compatible with your goals.

Rebalancing your portfolio reduces that risk exposure and increases the likelihood of achieving your desired long-term investment returns. The other benefit of a rebalancing strategy is that it forces you to buy low (i.e. the lagging fund) and sell high (or at least avoid buying as much of the high-performing fund).

Do you have a question about rebalancing your portfolio? Ask away in the comments below: