One of the biggest decisions as you edge closer to retirement is when to take CPP. The standard age to take your Canada Pension Plan benefits is when you turn 65; but you can take a reduced CPP retirement pension as early as 60, or you can get an increased benefit by delaying CPP up to age 70.

I asked Doug Runchey, pension expert at DR Pensions Consulting, to weigh-in on the benefits of taking CPP early versus late.

Taking CPP early

The earliest you can take your CPP benefits is the month after your 60th birthday, but you’ll get 36 percent less than if you had waited until 65.

This chart shows the monthly CPP pension you’d receive if you retired in 2016 and elected to take your benefits early:

| Age | Reduction | Monthly benefit* |

| 60 | 36.0% | $681.60 |

| 61 | 28.8% | $758.28 |

| 62 | 21.6% | $834.96 |

| 63 | 14.4% | $911.64 |

| 64 | 7.2% | $988.32 |

*Assumes the maximum pension amount of $1065 per month

Things to consider before deciding to take CPP early:

When you take CPP at 60, your benefits are based on your best 35 years of earnings, rather than your best 39 years of earnings if you were to take it at 65.

If you’re confident that you will be eligible for the Guaranteed Income Supplement (GIS) once you reach 65, you should generally take your CPP at 60.

Finally, if you’re thinking about taking CPP early because of ill health, always apply for a CPP disability pension instead.

“If approved, the CPP disability amount will always be higher than a retirement pension and it will convert to a full retirement pension at 65,” says Runchey.

Taking CPP late

The advantage to taking CPP after 65 is that you’ll receive a healthy 8.4 per cent increase for each year you delay receiving benefits, up to age 70. That works out to a 42 percent incentive for taking CPP at 70 instead of 65.

This chart shows the monthly CPP pension you’d receive if you delayed taking your benefits until after age 65:

| Age | Increase | Monthly benefit* |

| 66 | 8.4% | $1,154.46 |

| 67 | 16.8% | $1,243.92 |

| 68 | 25.2% | $1,333.38 |

| 69 | 33.6% | $1,422.84 |

| 70 | 42.0% | $1,512.30 |

*assumes the maximum pension amount of $1065 per month

Things to consider before deciding to take CPP late:

You will always get more CPP by waiting, even if you’re not working.

Runchey says that your “calculated (age-65) retirement pension” may decrease if you’re not working between age 60 and 65, but the age-adjustment factor will always make up for that decrease, and then some.

“In that situation I use the expression that you will receive a larger piece of a smaller pie if you wait, but you will always get more pie,” he said.

If you’re withdrawing RRSPs from age 60-70, it makes sense to defer your CPP until age 70 when you might be in a lower tax bracket.

The Verdict: When to take CPP

The choice of when to take CPP should be based on your individual numbers and take into account your life expectancy, current and future tax bracket, your immediate versus future income needs, plus the impact that taking CPP early has on any other benefits that you’re receiving, such as GIS and OAS.

One thing that’s clear, according to Runchey, is that taking CPP at 65 is never your optimal choice from a CPP payout perspective.

The bottom line: You will always eventually be ahead if you take CPP later.

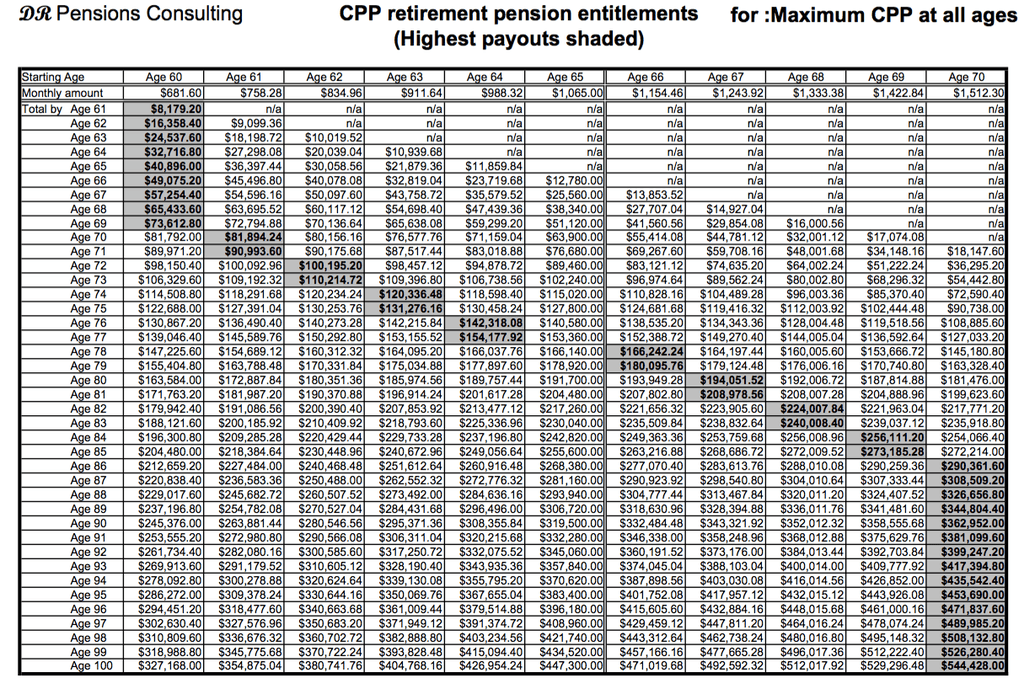

As you can see from this chart (click to open in a new window), you will be ahead financially – considering the CPP only – if you take your CPP:

- At age 60 and if you don’t live past age 69

- At age 61 and if you live past age 69 but not past age 71

- At age 62 and if you live past age 71 but not past age 73

- At age 63 and if you live past age 73 but not past age 75

- At age 64 and if you live past age 75 but not past age 77

- At age 66 and if you live past age 77 but not past age 79

- At age 67 and if you live past age 79 but not past age 81

- At age 68 and if you live past age 81 but not past age 83

- At age 69 and if you live past age 83 but not past age 85

- At age 70 and if you live until at least age 86

Final thoughts

If you’re unsure about your Canada Pension Plan benefits, have questions about the optimal time to take your CPP benefits, or simply want to go over some different scenarios, I highly recommend consulting Doug Runchey at DR Pensions. He charges a fee-for-service, and in many cases it is well worth the money.

Also read:

Understanding your retirement benefits: Part 1 – CPP

Understanding your retirement benefits: Part 2 – OAS

Understanding your retirement benefits: Part 3 – Private Pension Plans

CPP’s child-rearing dropout provision