“I don’t invest in my RRSP anymore because I’ll have to pay tax on the withdrawals.” This type of thinking around RRSPs has become increasingly common since the TFSA was introduced in 2009.

The anti-RRSP crowd must come from one of two schools of thought:

- They believe their tax rate will be higher in the withdrawal phase than in the contribution phase, or;

- They forgot about the deduction they received when they made the contribution in the first place.

No other options prior to TFSA

RRSPs are misunderstood today for several reasons. For one thing, older investors had no other options prior to the TFSA, so they might have contributed to their RRSP in their lower-income earning years without realizing this wasn’t the optimal approach.

Related: The beginner’s guide to RRSPs

RRSPs are meant to work as a tax-deferral strategy, meaning you get a tax-deduction on your contributions today and your investments grow tax-free until it’s time to withdraw the funds in retirement, a time when you’ll hopefully be taxed at a lower rate. So contributing to your RRSP makes more sense during your high-income working years rather than when you’re just starting out in an entry-level position.

Taxing withdrawals

A second reason why RRSPs are misunderstood is because of the concept of taxing withdrawals. The TFSA is easy to understand. Contribute $6,000 today, let your investment grow tax-free, and withdraw the money tax-free whenever you so choose.

With RRSPs you have to consider what is going to benefit you most from a tax perspective. Are you in your highest income earning years today? Will you be in a lower tax bracket in retirement? The same? Higher?

The RRSP and TFSA work out to be the same if you’re in the same tax bracket when you withdraw from your RRSP as you were when you made the contributions. An important caveat is that you have to invest the tax refund for RRSPs to work out as designed.

Future federal tax rates

Another reason why investors might think RRSPs are a bum-deal? They believe federal tax rates are higher today, or will be higher in the future when it’s time to withdraw from their RRSP.

Is this true? Not so far. I checked historical federal tax rates from 1998-2000 and compared them to the tax rates for 2018 and 2019.

The charts show that tax rates have actually decreased significantly for the middle class over the last two decades.

Someone who made $40,000 in 1998 would have paid $6,639 in federal taxes, or 16.6 percent. After adjusting the income for inflation, someone who earned $59,759 in 2019 would pay $7,820 in federal taxes, or just 13.1 percent.

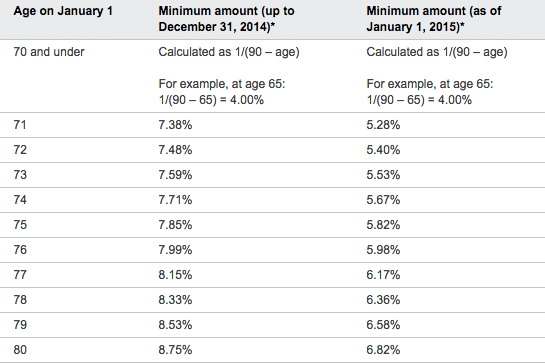

Minimum RRIF withdrawals

It became clear over the last decade that the minimum RRIF withdrawal rules needed an overhaul. No one liked being forced to withdraw a certain percentage of their nest egg every year, especially when that percentage didn’t jive with today’s lower return environment and longer lifespans.

In 2015 the federal government made changes to the minimum RRIF withdrawal table, bringing it more in-line with today’s reality:

The dreaded OAS clawback

Canadians who receive Old Age Security and have annual income between $75,910 and $123,386 will have all or part of their OAS pension reduced. This clawback is especially concerning for retirees whose minimum RRIF withdrawals push them over the income threshold.

Canada Revenue Agency uses the following example on its website:

The threshold for 2018 is $75,910.

If your income in 2018 was $86,000, then your repayment would be 15% of the difference between $86,000 and $75,910:

$86,000 – $75,910 = $10,090

$10,090 x 0.15 = $1,513.50

You would have to repay $1,513.50 for the July 2019 to June 2020 period.

This is a legitimate concern for retirees. No one wants to lose out on benefits that they’re entitled to receive. An advisor or tax accountant can help you determine a strategy that best optimizes your retirement withdrawals.

One such strategy is to make small withdrawals from your RRSP between the ages of 60-70 and delay taking CPP and OAS until age 70. This reduces the size of your RRSP for when you are forced to convert it into an RRIF and make mandatory withdrawals. It also increases your CPP and OAS benefits by 42 percent and 36 percent, respectively.

Related: CPP Payments – How Much Will You Receive From Canada Pension Plan

Canada Child Benefit

Parents with children aged 17 and under can be eligible to receive a tax-free monthly payment from the Canada Child Benefit. The CCB is a means-tested program, so the more income your household earns the less money you receive from this government program.

The Canada Child Benefit is completely phased out when your income is between ~$157,000 and ~$206,000, depending on the number of eligible children in your family.

The government uses adjusted net family income to determine how much you’ll receive from the program. Since RRSP contributions reduce your net income, it could be wise for young families to prioritize RRSP contributions ahead of TFSA contributions to reduce their net family income and help them receive more from the Canada Child Benefit the following year.

RRSP Matching

Some lucky employees work for companies that offer a matching program for your RRSP contributions. This is the best deal out there for savers. A guaranteed 100% return on your contributions. In fact, one could argue that contributing up to the maximum of your company’s RRSP matching program could be prioritized over paying off a credit card balance at 19% interest. It’s that valuable.

A company match will typically have some limits or restrictions. For example, your employer could match contributions up to 5% of your salary with the caveat that you must contribute to a group RRSP plan at a particular bank or investment firm.

It’s important to note that, even if the investment options are terrible high fee mutual funds, you should still contribute the maximum and take advantage of these generous matching dollars. You can always transfer the money over to a low fee indexing portfolio at some point in the future.

Final thoughts on RRSPs

RRSPs aren’t a scam; they’re a still a critical tool for Canadians to save for retirement. They’ve just got a bad rap over the years because of some misguided thinking around withdrawals, taxes, plus the introduction of a new and seemingly better (re: tax-free) savings vehicle.

RRSP contributions are still a key component of my financial plan. I’ve caught up on all of my unused contribution room and so now my goal each year is to max out my contribution limit (which is reduced by my pension contributions).

Related: TFSA Contribution Limit and Overview

TFSAs are great, and they get filled up next. In fact, when we paid off our car loan a few years ago we started catching up on our unused room and maxing out our TFSAs.

Both accounts are valuable parts of our financial plan and, along with my pension, will make up the bulk of our income in retirement.