How To Supercharge Your RRSP

The idea that an RRSP loan can boost your savings and generate a higher tax refund does not sit well with most people. If you can afford the loan payment then why not just budget and save that amount in the first place instead of borrowing?

In The Wealthy Barber Returns, author David Chilton describes a strategy that can increase your RRSP contributions without putting you out of pocket any more than what you’d already planned to save. He explains how most of us save from our after-tax income, but when we contribute only those after-tax dollars instead of their pre-tax equivalent, we shortchange our RRSPs.

So how do you get the full, pre-tax amount into your RRSP? The answer is to use something called an RRSP gross-up strategy where you borrow a small amount equal to the tax refund that will be produced by your RRSP contribution. Here’s how it works:

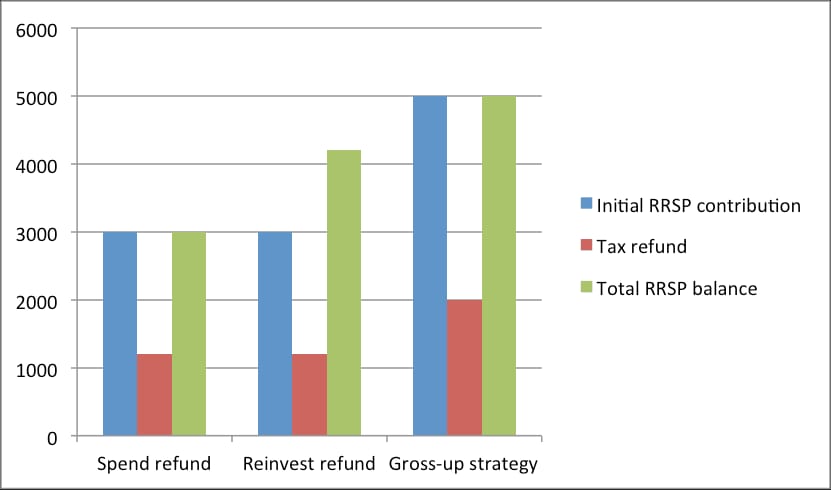

Let’s say you are in a 40 percent tax bracket and had $3,000 after taxes to invest. How much should you contribute to your RRSP?

If you're not sure of the answer, you're probably like the majority of Canadians who unknowingly invest less than they could into their RRSP, according to Talbot Stevens, author of a book called The Smart Debt Coach.

In this case, Mr. Stevens says you should put $5,000 into your RRSP. To do this you’d have to borrow $2,000 to “gross-up” your $3,000 after-tax dollars to get the pre-tax equivalent of $5,000 in your RRSP.

Your $5,000 RRSP contribution will generate a $2,000 tax refund, which is enough to completely pay off your loan. The RRSP gross-up loan allows you to turn $3,000 into a $5,000 RRSP contribution, which means you end up with 67 percent more saved in your RRSP.

Mr. Stevens takes credit for pushing Chilton to include this powerful, yet poorly understood concept in his book. He has a free calculator on his website to help you determine how much you could increase your RRSP contribution, for your tax bracket. Simply enter the after-tax amount you have available to invest, and then enter your marginal tax rate to calculate the “gross-up” amount.

Reading The Smart Debt Coach changed my opinion on using RRSP loans and I've actually used a form of the gross-up strategy in each of the last two years. I borrowed $20,000 to top-up my RRSP in 2014 and then earlier this year I took advantage of a 1.5% RRSP loan offer from Tangerine and borrowed $8,000 to contribute to my RRSP. It turns out that I like the forced-savings aspect paying back the loan over a 9-to-12 month period.

Using an RRSP loan can be a powerful strategy to boost your RRSP contributions and build your retirement portfolio. However, use caution whenever you borrow to invest and remember that this solution only works when you have the discipline to save your tax refund or use it to help pay off the loan.

Great post. People often forget about this. It works even better when you’ve been contributing to your rrsp all year and then do an additional top up.

This strategy essentially makes the RRSP equal the TFSA in terms of effectiveness when you look at pre-tax contributions and income taxes (if retiring in the same tax bracket as your contribution marginal rate)

Hey great post Robb. Question for you or Jamie. My wife and I were currently discussing this the other day. I’ve read Talbot’s book. We’ve contributed all year and now we’d like to gross up. Does it make the most sense to take out the top up loan right before the deadline? That way we’d only be paying for the loan for maybe a month before the tax refund arrives? Or is it better to have the money working sooner by taking out the loan at the end of December, and not paying it off until March-ish, when our refund arrives?

Best regards,

Joe

Hi Joe, yes it does make the most sense to wait until closer to the deadline to take out the loan. Although you could argue the opportunity cost of not being invested for a couple of months might outweigh the extra few bucks that you’d pay in interest. Of course, the market could take a dive in those two months, rendering that advantage useless…

I think as long as you know you’ll be able to pay off the loan right away then just pull the trigger when you feel you’re ready.

Hey Joe, It does make a difference for sure. Carrying the loan for an extra 2 months has costs. A $10,000 loan at 4.5% the interest for the extra 2 months is ~75$. Not huge but still a non-deductible interest cost.

However if a favourable market event happens and your investments you were going to buy go on sale by 30% a few months early it’d be worth it to buy them for cheaper.

Another thing to consider is that some mutual funds do their yearly distributions in December (TD e-series included). So buying the funds before this date would mean you’ll be paying tax on a years worth of distributions. Buying after or in the new year avoids this tax bill. However, if buying dividend paying investments, you may be looking to collect the extra divided payment anyways.

Jamie

The distributions mean ZERO – we’re talking about investing inside of an RRSP, so it simply doesn’t matter

Outside of an RRSP it would essentially mean “pre-paying” some taxes that you’ve not seen the gains on. It increases your ACB, so it all washes in the end.

Thanks Rob. Good call, I got ahead of myself with the distributions. In an RRSP that will make no difference and wouldn’t influence your timing on an RRSP loan.

@Rob @Joe Distributions come from the funds assets so the price of the fund will drop accordingly – so it can make a difference when you make a purchase.

Hi Jamie, right on! The RRSP and TFSA are mirror-images of each other as long as you re-invest the refund.

Yup! A lot of people don’t realize that as there has been a lot of RRSP bashing recently, especially with the increased TFSA limit (for now!).

One way to ensure RRSP is superior to TFSA is to contribute to a spousal income in a lower bracket. The difference in tax rates guarantees RRSP wins over TFSA. Just need to make sure the refunds are used appropriately (i.e. reinvest/gross up).

People often say its good to defer tax as long as possible., It’s also good to save tax NOW!

One area where the TFSA would still win is on mandatory the minimum withdrawal front. Save too much in an RRSP and the minimums could force you to take more income into your hands than you want to. Of course, this would only apply to those who are maxing out RRSPs….. a pretty small group.

Thanks so much for all the insights. One of the reasons I read this blog is because there’s lots of people who hang out here who are WAY smarter then me! Have a good one guys. Joe

Another thing people may want to consider is marginal tax rates. If one spouse is in a higher tax bracket it would make sense to bring the taxable income of that spouse down one bracket (if possible) and then contribute to the other account. This is assuming of course the cont room is available.

Hi Dan, thanks! Definitely consider your MTR and your total available contribution room.

Another way to achieve this is to request your employer takes less tax off your paycheques by changing your TD1 (in this case, $2,000) and contribute the $5,000 either evenly over the year to achieve dollar cost averaging or, preferably at the beginning of the year to get the most of the time-value of money. In essence, borrow off the government interest-free instead of yourself.

Hi Don, great advice – thanks for sharing!

I’d be careful about promoting this – just my take. You are borrowing money, for investment purposes, for money you don’t have to invest in the first place due to a variety of factors.

I’m not saying the “gross-up” contribution isn’t a good idea for some people. It can make good sense but if you don’t use the full RRSP-generated refund to pay off the loan – which is really the government’s money not yours – then you’re fooling yourself I think.

Thoughts Robb?

Mark

Hi Mark, I think the essence of the strategy is to take a small top-up loan before the RRSP deadline and then use the refund to pay off the loan shortly thereafter. It’s not really using money you don’t have, but more like taking full advantage of a great program like RRSPs.

There’s definitely an element of risk when you get into the top-up loans with longer pay-back periods. But as long as you have a reasonable time frame to pay back the loan and the payments don’t hamper your ability to live and save in other areas then I think it’s fine. Invest in something long-term and reasonable, too, but that should go without saying 😉

Interesting concept the grossing up.

I dont believe an RRSP and TFSA are equal. Everyone seems to be missing a very important point which no Advisor or Financial experts ever discuss.

When you contribute to a TFSA you pay tax before you contribute. So no further taxation ever.

An RRSP is an unfunded tax burden of which you have no idea how much you will be taxed until you get there in 10 or 20 years. The Government could be in rough shape and tax you excessively.

Thats why I prefer to top a TFSA first.

Hi Andrew, thanks for your comment. RRSPs and TFSAs are equal, given the right variables. The flaw in your argument, other than making a gross assumption that a future government will tax you at a higher rate in withdrawal, is that you can control the amount you withdraw from your RRSP (to a point) in order to minimize taxes paid.

If you were making $50,000/yr when you contributed to your RRSP, and you want to withdraw $100,000 a year from it in retirement, of course you’re going to pay more in taxes and a TFSA would have been the better choice. But if you flip that scenario and contribute to your RRSP while you’re making $100,000/yr, and then withdraw $50,000/yr in retirement, then the RRSP comes out ahead.

Andrew – you may find that a gov’t who is willing to tax that RRSP to get revenues they otherwise wouldn’t is also a gov’t that will find ways of taxing the TFSA – I fully expect to see things like TFSA withdrawals added to calculate OAS Clawback, etc.

Stupid question, but can you take money out of your TFSA to do this? (And then put the refund back into the TFSA to “pay it back”, making sure you don’t go over contribution limits…)