The Costco Effect On Earning Credit Card Rewards

My wife and I do a lot of our grocery shopping at Costco and a few years ago signed up to become Executive Members, which means we get 2% cash back on nearly every purchase made at Costco. Last year the warehouse giant sent us a reward coupon in the mail for $176.61 and if you do the math that means we spent $8,825.50 – or $735 per month – at Costco in 2015.

I included the rebate in my budget under “rewards earned” even though it has no cash value and can only be redeemed at Costco locations. It also got me thinking about how shopping at Costco can throw a wrench into your calculations when determining which rewards credit card is best.

Related: Is the Costco Executive Membership worth the fee?

You see, most online calculators use general categories such as groceries, gas, and dining to help identify the credit card that gives you the best bang for your buck based on your personal spending habits.

Rewards cards that pay higher earning rates on grocery purchases, like the Scotia Momentum Visa Infinite or Scotiabank Gold American Express Card, come out ahead for individuals and families who spend a lot of their household budget on food.

The Costco effect on rewards calculations

But if your household is anything like mine and you do the majority of your grocery shopping at Costco, you can throw that calculation out the window because:

- Costco does not accept Visa or American Express cards, and;

- Costco is not categorized as a “grocery” merchant – it falls under “department store” or “other”

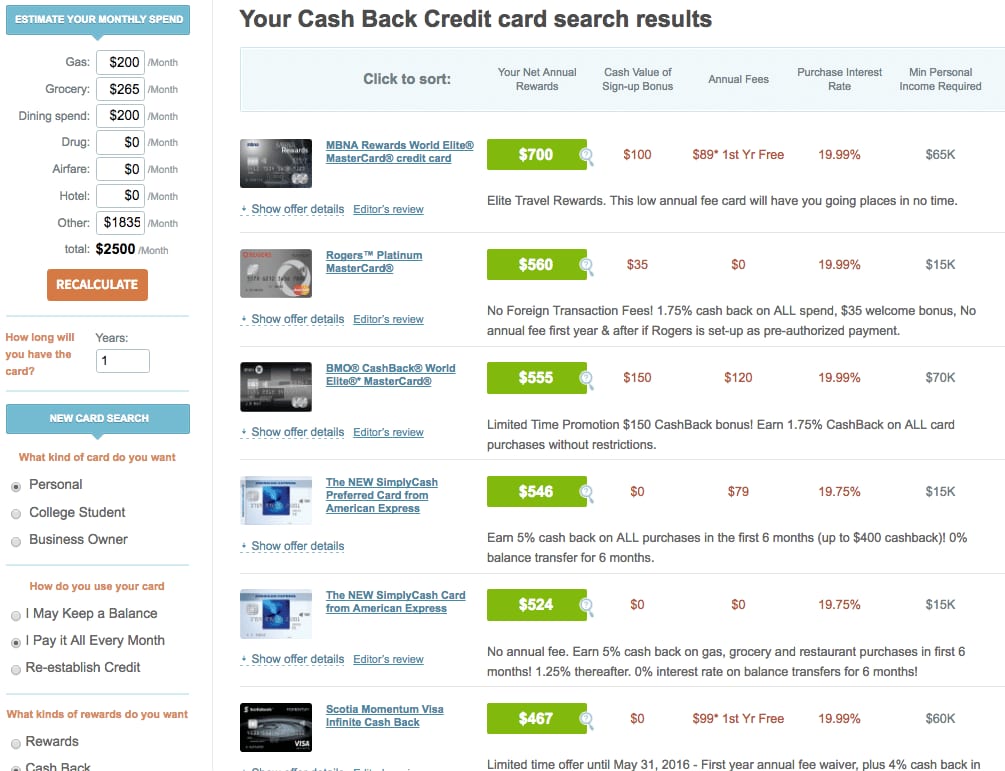

When I post our typical grocery-heavy monthly spend in the GreedyRates calculator it recommends the Scotia Momentum Visa Infinite card as the best option for earning credit card rewards:

Note the monthly spending breakdown on the left. I entered $1,000 under ‘groceries’ to reflect our overall household spend in that category. But remember that Costco purchases aren’t eligible for the 4% category bonus that the Scotia Momentum Visa Infinite offers on grocery purchases because a) Costco doesn't take Visa, and b) Costco stores have a different merchant code than other grocery stores.

Now watch what happens when I move our $735 monthly Costco spend from the grocery category to ‘other’:

The Scotia Momentum Visa Infinite card tumbles all the way down to sixth place – losing $265 cash back per year in the process. But the actual cash back number is even worse for the Momentum Visa Infinite because – again – Costco doesn’t accept Visa cards! We have to take out our $735 per month spend completely, which drops the Scotia card to just $380 cash back per year.

The cash back rewards king for a Costco shopping household like mine is the mbna rewards World Elite MasterCard. That’s because it pays 2% back on every purchase, regardless of the category, and including Costco purchases.

Also in the conversation is Capital One’s Aspire Travel World Elite MasterCard; the rewards credit card that we use for our everyday spending, including Costco. This card also pays 2% back on every purchase and its new redemption system lets you use rewards points to erase whole or partial travel purchases off your credit card statement

Final thoughts

While the Scotia Momentum Visa Infinite card reigns supreme for cash back rewards fans due to its 4% / 2% / 1% category bonus rewards structure, a good argument can be made for Costco shoppers to ditch the Visa altogether in favour of a MasterCard that pays 2% on every purchase.

In fact, I cancelled our Momentum Visa Infinite card earlier this year before the annual fee came due. As our family shifts more-and-more of our grocery spending to Costco, it made little sense to carry two everyday annual fee cards.

Readers: Does the Costco effect influence your choice of rewards credit cards?

I had the same realization when I switched to Tangerine Master card. I think it is still a better value because it has no fees, 2% categories, no limits, and the essential insurance programs. But I hoped to double-dip by using it at Costco for groceries. Unfortunately like you said they aren’t a grocery store so I’m only getting 1% back (which is still better than the 0.5% from Capital One’s Costco card).

Hi Schultzter, I agree that the Tangerine MasterCard offers better value than Costco’s Cap1 Platinum MasterCard, especially for Tangerine clients who get the extra bonus category. But yeah, too bad you can’t include Costco purchases in the category bonus for grocery spending.

FYI: the Capital One Costco Card offers 1% back on other purchases (3% on restaurants; 2% gas).

Well, you analysis points to what I’ve been saying all along. The MBNA Reward World Elite MasterCard is the best cash back credit card in Canada. For rewards reasons and overall value reasons:

http://www.howtosavemoney.ca/best-cash-back-credit-cards

You have to be a really heavy gas and grocery spender for the Scotia Momentum Visa Infinite to beat it and then it has a higher annual fee, no sign up bonus, you can only redeem once a year instead of however and whenever you want, and has worse insurance coverage. It’s really no contest at all.

Hi Stephen, it really depends on where you like to shop. The Scotia Momentum Visa Infinite card came out ahead for us when we did all of our grocery shopping at Safeway, but now that we’ve switched to 85-90% Costco the Cap1 Aspire Travel comes out ahead for us.

The one-time rebate is annoying – I’ll give you that.

You can get it to edge out slightly higher rewards under certain circumstances, I’ll give you that 🙂

I also have the Momentum Visa Infinite card and it appears that the rewards are paid once per year. Did you get your rewards when you cancelled before the year was up?

I got my card in October, received my rewards for one month in November and I`m hoping that I can collect my rewards if I decide not to keep the card after the free year.

Hi Stan, your timing might be a bit tricky (see my reply below to Mel). I’d try to call closer to the when the fee comes due and try to get it waived again. Use some of the techniques discussed here – https://boomerandecho.com/want-better-deal-just-ask/

Good luck!

Thanks, I will try to get the fee waived.

Thanks Echo, I’ll try to get them to waive it

No Stan, they will NOT give your cash if you cancel early, which is frankly appalling. However, you can keep your card until you can cash out your rewards and then call to cancel and ask for a pro-rated fee refund. They should accommodate this request. Or do what Robb is suggesting and get them to try and waive or reduce the fee to keep you on.

Thanks Stephen. If I can’t get them to waive it, I’ll try for the refund.

If Costco gift cards ever become available at grocery or gas stations, that would skew the choice back to the Scotia Visa.

Hi Garth, good point but I wouldn’t hold your breath!

I also have the Scotia Momentum Visa Infinite however I will not renew it after the 1 year is up. Would like to know if I will be able to receive my rewards before I notify that i will not renew the card.

I was not able to do this, even when I offered to keep the “no fee” version of the same card, they took away all my rewards. 🙁

Hi Mel, it turns out that you forfeit any rewards if you cancel before you get your annual cash back rebate. Fortunately for me the date of my cash back rebate was early November and the annual fee was not due until February. So once I got my cash back rebate I just stopped using the card and then cancelled it a couple of months later. I ended up forfeiting about $4.

I think the Costco Capital one card gives 1% on outside Costco purchases and 2% on gas

Hi Pellrider, the Capital One Platinum MasterCard for Costco members is likely not the best card to use to earn rewards, especially when there are other MasterCards that pay 2% back on every purchase.

Here’s what the Costco MasterCard pays:

3% on restaurant purchases

2% on gas purchases

0.5% on the first $3,000 you spend annually on all other purchases, and 1% after that

Wondering if the World Elite Mastercard, whether offered by Bank of Montreal or President’s Financial or MBNA, offers the same benefits? If so, doesn’t it make sense to choose the provider that has the lowest annual fee?

Hi Sandy, yes – any of those premium MasterCards that pay 2% back on every purchase – not just specifically for groceries because that won’t work at Costco.

The PC Financial World Elite MasterCard, while it comes with no annual fee, only pays 1% back on purchases outside of Loblaws, Shoppers Drug Mart, and Esso, so that likely wouldn’t earn you the most rewards if you shop a lot at Costco.

BMO World Elite MasterCard would fit the bill, although you earn travel points that must be redeemed through the BMO Rewards travel centre, so not quite as flexible as the Capital One Aspire Travel World Elite MasterCard or the mbna Rewards World Elite MasterCard.

I don’t buy at Costco at all (I don’t have a car and I don’t have space at home to stock on groceries), and I use a mix of the Scotia Infinite and Tangerine credit cards. So far the results have been good. When I get to the one-year mark I’ll analyse other options.

Thanks for the trigger to think about it, Robb!

With the Tangerine M/C you get 2% on gasoline at Costco if you have selected fuel as one of your three bonus categories. I am getting 4% until mid-July. I agree for store purchases/groceries etc you only get 1%.

That’s what we do Robb. We use a MC for all our Costco shopping, a grandfathered CapOne card with 1.5% cash back and tons of great travel benefits. No annual fee.

We usually spend about $250 per month at Costco.

Cheers,

Mark

I use the BMO World Elite MasterCard card for all the same reasons. Our family spends even more at Costco than your’s Robb! I get 2% towards travel (no restrictions), plus all the usual “premium card” benefits. The four priority pass visits make it easier to accept the annual fee!

MBNA World Elite is what I use as well – not just Costco but for all my day-to-day. Obviously each person’s needs/circumstances are different, but in my opinion the only comparable cashback card in Canada is the C1 Aspire Travel. Those two cards are easily the best cashback cards (for the first year at least).