How To Crush Your RRSP Contributions Next Year

*Updated for October 2025*

If you’re a high-income earner staring at a mountain of unused RRSP room, you’re not alone. Many Canadians with strong salaries struggle to come up with enough cash flow to max out their RRSP deduction limit each year. And while we can debate whether middle- and low-income earners are better off contributing to a TFSA or an RRSP, the reality for high-earning T4 employees is clear: RRSP contributions are the most effective way to reduce your tax burden each year.

The RRSP deduction limit is 18% of your earned income from the prior year, up to a maximum of $33,810 for the 2026 tax year, plus any unused RRSP room from previous years.

An employee who earns $133,333 per year can contribute $24,000 annually to their RRSP. While that's straightforward enough, coming up with $2,000 per month to max out your RRSP can be a challenge. An even greater challenge is catching up on unused RRSP room from prior years.

Related: So you've made your RRSP contribution. Now what?

Let's say you live in Ontario, earn a salary of $133,333 per year, and you want to start catching up on your unused RRSP contribution room. Your gross salary is $11,111 per month and you have $2,859 deducted from your paycheque each month for taxes, leaving you with $8,252 in net after-tax monthly income.

Your goal is to contribute $2,500 per month to your RRSP, or $30,000 for the year. This maxes out your annual RRSP deduction limit ($24,000), plus catches up on $5,000 of your unused RRSP contribution room from prior years. Stick to that schedule and you'll slowly whittle away at that unused contribution room until you've fully maxed out your RRSP. Easy, right?

Unfortunately, you don't have $2,500 per month in extra cash flow to contribute to your RRSP. After housing, transportation, and daily living expenses you only have about $1,500 per month available to save for retirement.

No problem.

That's right, no problem. Here's how to fix that:

T1213 – Request To Reduce Tax Deductions at Source

This CRA form allows you to reduce the amount of income tax withheld from your paycheque if you expect to make deductible RRSP contributions (or certain other deductions) in the upcoming year.

Here’s how it works:

- Complete the T1213 Request to Reduce Tax Deductions at Source form.

- Attach proof – such as a printout showing confirmation of your automatic monthly RRSP deposits.

- Submit everything online through your CRA My Account using the Submit Documents Online service.

- Wait for the CRA to assess your request and send you an approval letter.

- Provide that letter to your HR or payroll department.

Once approved, your employer will withhold less tax from each paycheque – giving you more take-home pay to fund your RRSP contributions.

Timing tip: Processing can take several weeks, so submit your form in mid-October or early November to have everything in place for January. You’ll need to re-submit each year so you can begin the new year with the correct (and reduced) taxes withheld.

That said, the CRA will approve letters sent throughout the year – it just makes more sense to line this up with the start of the next calendar year.

Reducing taxes withheld from your paycheque frees up more cash flow to make your RRSP contributions. It’s like getting your tax refund ahead of time instead of waiting until after you file. Let's see how that would work using our example from Ontario.

You've signalled to CRA that you plan to contribute $30,000 to your RRSP next year. In CRA's eyes, that brings your taxable income down from $133,333 to $103,333. This will make a significant difference to your monthly cash flow.

Recall that you previously had $2,859 in taxes deducted from your monthly paycheque. After your T1213 form was assessed and approved, the taxes withheld from your paycheque each month goes down to $1,853 – freeing up an extra $1,006 in monthly cash flow that was previously being withheld for taxes.

That's an extra ~$12,000 that you can use to crush your RRSP contributions next year.

Now, to be clear, you need to follow through and make the $30,000 RRSP contributions that you promised to CRA. Otherwise you'll face a bigger tax bill for the next tax year, and risk not getting the T1213 form approved again.

Once your T1213 form has been assessed and approved you'll receive a letter that looks something like this to give to your employer:

The biggest advantage to reducing your taxes withheld at the source is to increase your cash flow so you can make those big RRSP contributions. Otherwise, your options are to take out an RRSP loan to help reach or exceed your deduction limit, or wait for your tax refund and then contribute that lump sum along with your smaller monthly contributions.

**Optimize Your RRSP**

I have a general savings philosophy that goes something like this:

- Utilize employer matching savings plan – basically take advantage of your employer match, it's free money!

- Optimize your RRSP contributions – contribute enough to bring your taxable income down to the bottom of your highest marginal tax rate

- Maximize TFSA – max out your TFSA, eventually.

- Prioritize short-term goals – once the first three goals have been funded, extra cash flow should be allocated to short-term goals such as buying a new vehicle, taking a dream vacation, renovating your home, funding a parental leave or early retirement, etc.

On the RRSP front, I use EY's excellent tax calculators & rates page (updated annually) and the Canadian personal tax rates by province sections to determine what those marginal tax brackets are for my clients.

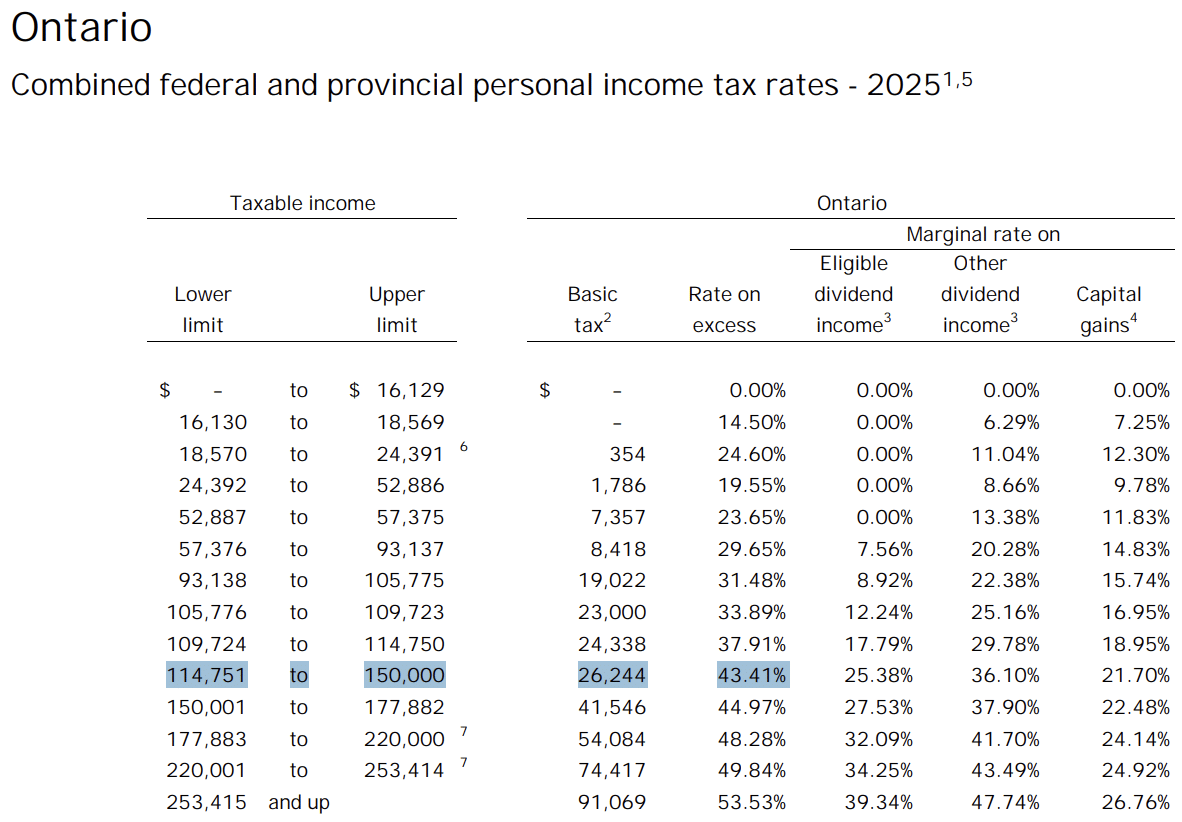

What does optimizing mean? For instance, in the example we've been using above (Ontario worker with $133,333 gross income) it might make sense to only contribute $18,582 to their RRSP to bring their taxable income down to $114,751 – the bottom of the 43.41% marginal tax bracket).

That way, every single dollar contributed to the RRSP is going to save 43.41 cents in taxes.

Contribute one more dollar, and that dollar will only receive 37.91 cents in tax relief.

Of course, it might be perfectly sensible to contribute more and get a blended tax deduction (some at 43.41% and some at 37.91%). Maybe you'd want to bring down your income to the bottom of the 37.91% marginal tax bracket, but no further.

Final Thoughts

Back to our Ontario example, let's say you did not fill out the T1213 form and instead just contributed your available cash flow of $1,500 per month or $18,000 per year. That would reduce your taxable income to $115,333 and give you a tax refund of $7,814.

You could do anything with that tax refund, and a lot of surveys suggest Canadians are more inclined to spend their refunds because they're seen as windfalls.

Meanwhile, had you simply filled out the T1213 form and then contributed $2,500 per month to your RRSP, you'd have reduced your tax bill by $12,079 and have saved an extra $12,000 inside your RRSP. A tax deduction now, and additional savings for retirement in the future. Win, win.

Who's crushing it, now?

I always wondered about doing this. Putting the money to work right away, instead of having it tied up in government hands for a year or more. Now I know how! Thanks Robb!

Hey Brian, exactly – this is your money. You might as well put it to work sooner, rather than wait for a tax refund. Plus, as the example in the article showed, you get more money back and put more of it to work this way.

Thanks Robb. This looks interesting and pertinent; I will read it.

Hi Robb, in this scenario do you end up paying less tax overall or do you just get the cash sooner than waiting for a refund but the total tax paid is the same?

Hi Amrita, if your total RRSP contribution is the same then you’ll pay the exact same total taxes – but with the T1213 form you’ll get the tax relief upfront instead of scrambling to make the contribution and then getting the refund after you file your taxes.

Really great advice, Rob. Easy to do and helpful to those trying to hit their retirement goals sooner, putting their money to work for them right away.

My accountant told me it is more advantageous to leave as much money in my professional corporation as possible rather than maximizing RRSP contributions. My professional income is much lower than the $500,000 cutoff for small businesses. Maybe this could be a topic for one of your future blogs?

Unfortunately, your accountant is not correct on this. Your registered accounts are better tax deferral accounts than your Corp, so should be maxed out and the remainder of your income invested in your Corp. Give him this paper to review

https://www.pwlcapital.com/wp-content/uploads/2017/07/2017-07-20_Felix_A-Taxing-Decision-Update_Final.pdf

Thanks Grant!

Thanks Grant, this looks like a very informative article and I will read it.

Ron

Hi Ron, this particular article was aimed at the T4 employee but I understand where you’re coming from as a business owner.

Jamie Golombek has a pretty widely read paper on this topic which suggests that RRSPs may be a better choice for business owners: https://www.jamiegolombek.com/media/RRSPs-for-business-owners.pdf

This is a bit tongue in cheek but accountants love to tell their clients to leave all of their business income inside the corp, without considering important items like RRSPs, CPP, and even paying yourself a small amount so you can eat.

It could be a good strategy to pay yourself a salary up to the CPP YMPE, or enough salary to get the RRSP maximum deduction limit. Lots of factors to consider.

My wife and I own our business and pay ourselves dividends right now to meet our personal living expenses. But we also have about $300k invested in our RRSPs from prior years.

We may consider paying ourselves a salary up to the CPP YMPE and then topping up our income with dividends in the future. A blog for another time, for sure.

This is something that our family has been doing for years. It’s a great tax planning and investing/savings strategy but be prepared to educate your employer’s payroll department. The T1213 and the CRA letter is not something that many payroll people know about. The most common response we’ve personally encountered is “What’s this?” 😀

Hi Brenda, good point. I bet smaller organizations rarely, if ever, see these forms.

Thank you for the reminder! I just filled mine out and plan on submitting it this week. So helpful with tackling that remaining RRSP room. Look forward to chatting with you again soon.

Nice, Tim! Glad you found the article helpful. Looking forward to catching up soon.

My workplace does this automatically. Besides low cost index fees, this is a big reason why I save through my employer as I can maximize those contributions while minimizing the cash flow hit. On a net/net basis I think you’re further ahead and the only way to keep it consistent with after tax dollars would be to take out a loan to top up the contributions (otherwise the math dictates a lower % contribution all things being equal).

This strategy has allowed me to supercharge my savings and I still get a small tax refund at the end of the year as the math is never quite exact given other deductions, donations, etc

Thanks, Robb. I actually sent mine in early October and have yet to receive mine. Get’em in quick!

I see the annual RRSP max amount on CRA website, how do we find out what the total available contribution room from previous years is?

Thanks

Hi Martin, you can see your total available RRSP room on your Notice of Assessment or you can go to your My CRA Account online and click on the RRSP details.

I work for a company with a few hundred employees in Canada and evidently only 2 of us use these according to HR. Worth a mention is that if you end up with other unexpected income from investments, consulting, etc the CRA will get a bit grumpy if you end up owing more then 3k. You can make them happy by them paying in installments but that starts to feel like it’s defeating the purpose. I’ve stopped using the form because side income keeps pushing me over. For anyone with just T4 income though it’s a genius move!

How does the calculation change if you have an employer matched RRSP?

Hi Anu, you’ll want to find out if your employer is already reducing your taxes at the source based on those RRSP contributions. The clue is if you typically get a big tax refund or not.

If it doesn’t match up, like if your employer reduces your taxes based on their contribution but not yours, then you’d fill out the T1213 form with your contributions to get the full upfront tax savings on each paycheque.

Some good discussion here. Pardon if it’s already been mentioned (didn’t see it while skimming): I file a T1213 every year (yes, you gotta do it every year) and with around a 2 month turnaround time with CRA, right now is when you want to be filing it for 2023. You get the form back, that Robb mentioned, sometime in December and can pass it along to your company HR to reduce your withholding.

Thanks Robb for reminding me to file my T1213. Gonna do that right now, hah!

Awesome, good timing!

Comment removed. Covered in post. Thanks!

I’m a bit confused about the ON example showing the CRA proof they contributed $2k/month before they had $2k/month to contribute. Does a printout with upcoming scheduled deposits into your rrsp qualify as proof? I’ve been interested in this idea and think this might be the year it happens. Thanks!

Hi Shanna, yes – a print out showing your automatically scheduled recurring deposits would suffice.

I’m not 100% sure that’s even necessary but it probably helps. I had one client just include a handwritten note about his intention to contribute $xx amount a month to his Wealthsimple RRSP and that was accepted just fine.

Wow I’ve never heard of a handwritten note being accepted. I’ve only ever filed after the contributions were made but based on this article and the reader comments, I’ll try filing the T1213 differently this time.

An update: This is my second year filing the T1213. The CRA accepted my hand written note of my intentions of $xx monthly payments last year. Let’s hope they accept it again this year!

Do you have a recommendation for people who max out their registered accounts partway through the year and are trying to decide between investing in a taxable account for the remainder of the year versus setting the money aside for next year’s registered account contributions? That is, do the tax advantages of maxing out next year’s contribution room in January outweigh the opportunity costs of investing in the market now? I’d be filing a T1213 early next year and using the reduced withholding tax to invest the difference. (I understand that the investing best practice and mathematically optimal answer is to invest money in the market as soon as it’s available. I’m with a brokerage that doesn’t support the transfer of securities in-kind from a taxable account to a registered account though so I’d have to sell to cash, withdraw from taxable, deposit to registered, and buy again. Hoping to avoid this long round trip.) Thanks in advance!

Hi Brenda, if you’re able to max out your registered accounts early with regular 2022 cash flow, then I would assume you could do the same in 2023.

That tells me you have extra cash flow that you can direct to another goal (like investing in a non-registered account, or paying down your mortgage faster if you have a mortgage, or saving towards some upcoming one-time expense).

So rather than pre-saving for your 2023 RRSP and TFSA contributions, start contributing to a new goal for the remainder of the year.

That said, if you just love the idea of having $6,000 already saved up so you can max out your annual TFSA limit on January 2nd then go ahead and do that.

Hi Robb, thanks for the input. I’m self employed so my cashflow is irregular but yes you’re right, I have historically been able to max out contributions. I’m on a SlowFI/CoastFI path so my primary goal is FI. I’ve been able to start re-prioritizing travel this year as things have opened up and have taken multiple smaller trips already. Perhaps it’s time to start planning trips for next year. Your revenge travel and credit card rewards posts have gotten me thinking too.

Robb, another great article!!! – He my scenario and wondering if you could advise.

I have a child with a TFSA value of $50,000.00. Who presently earns 75K/yr.

They also have 25k of unused RRSP contribution room.

I am thinking of suggesting to my child to withdraw 25k from TFSA and putting that into their RRSP. Claim the tax refund

Put the tax refund (which is a must to be reinvested ) back into their RRSP as well as their TFSA (max 6k/yr). When they go to withdraw RRSP at retirement, I am sure they will be in a far lower tax bracket or should they do nothing and just leave money in TFSA

Thank you for taking the time to read. I just hope I was able to explain my thoughts onto paper

Regards

jim

Hi Jim, thanks for the kind words. Really tough to say if this is a good idea without knowing more details. What province does your child live in? Do they expect to be in a higher tax bracket later in their career, which may be a better time to take advantage of unused room? Did they have other plans for the TFSA money, or is it retirement savings?

Remember, if you have $75k in taxable income, and then make a $25k RRSP contribution, your taxable income is reduced to $50k. It’s certainly not a given that they would be in a lower tax bracket than $50k in retirement.

Live in Ontario

I believe is in a DC pension plan and has about 28yrs to retirement. Retirement funds not as good as a DB plan. So in 28yrs I cant see being in to high a tax bracket

Salary is steady with usual annual increase of 2%

Also plans to start a family soon, so by dropping their salary by cashing in TFSA and buying RRSP before birth of child, would this increase amount of CCB received

Sorry Robb my mistake all information above is correct except it is a DB plan and not a DC plan

I used to do this when I had a T4.

Now I just have diversified income.

Does the T1213 only work with automatic monthly deposits or can you just make a lump sum contribution to your RRSP for the current calendar year (assuming you have the cash on hand)?

Hi Peter, you can do a lump sum! All that matters is that you make the contributions you told CRA you’d make.

Super Appreciate the reminder! It’s a life saver being able to do this!

I am on a DB pension plan which I was told reduces the RRSP contribution room.

I was also told NOT to contribute to an RRSP as you’ll pay double in taxes when withdrawing etc.

Is this true? If I have leftover RRSP after my DB pension contributions, should I put that in RRSP or not?

Thanks

Hi RP, it’s impossible to advise you on whether or not to contribute to your RRSP without knowing a lot more information about you, your income, and your financial goals.

That said, you won’t pay double taxes when withdrawing from an RRSP.

Withdrawals from an RRSP count as income, just like the pension you’ll receive in retirement counts as income. And, just like with your employment income, you’ll pay taxes according to our progressive tax system (using marginal tax brackets).

Your RRSP contribution room is calculated as 18% of the previous year’s income (plus any unused contributions carried-forward from previous years). But that amount is reduced by a pension adjustment due to your defined pension plan.

For example, when I worked in the public sector and earned, say, $90k in salary I should have been able to contribute $16,200 to an RRSP (18% of $90k). But the pension adjustment reduced my annual RRSP deduction limit to about $3,600 per year.

For what it’s worth, I maxed that out every year. But every situation is unique.

That was a quick reply; thank you!

Current salary is about 90k, 20 years to retirement. Been in a DB job for the past 4 years.

TFSA’s are maxed out annually.

I guess I was primarily asking about your last sentence. Is it a good idea to contribute whatever remaining amount is left of RRSP room after pension contributions?

Awesome article! Just reading it now, hopefully if I get my form in this week it won’t be too late for the new year 🙂

Hi Robb,

I’m used to file the T1213 every year. The CRA delay used to be 8 weeks but last year, it took a lot more time to be processed. When I called at CRA, they told us that it could take up to 23 weeks to process. So this year, I filed it earlier to be on time.

Hi Robb… Solve a argument for me… lol

A tax payer has completely funded his RSSP to the maximum, including all past unused amounts to the end of 2023. The same tax person is itching to make his 2024 contribution in the first week of January to get his money working immediately…..

So question is… Can he do this or will that contribution be ruled as an over contribution to his 2023 tax return because he never waited past March 1st.

Even my accountant is confused on this. But I believe I am right and can make my 2024 contribution and anytime of 2024 calander year. I just need to indicate that on my return.

So help me put this to rest asap. 2024 is almost here.

Thanks kingly… Keith

Hi Keith, I wouldn’t recommend doing this.

Here’s one interpretation from CFP Jason Heath:

Interestingly, if you make your 2024 RRSP contribution in early 2024 based on your estimated new RRSP room, even though you cannot deduct it until next year, you may have to claim it on your 2023 tax return. This is because you claim RRSP contributions when made, even if they are not deducted until a future year.

Contributions made in the first 60 days of the year get reported on your previous year’s tax return. So, contributions made up to and including Feb 29th, 2024, get reported on a 2023 tax return. You do not have to deduct a RRSP contribution either, even if you have sufficient room.

Claiming the contribution was made and choosing to deduct that contribution are two different things.

Bottom line: I would avoid new contributions until the 61st day of the year, just to not muddy these waters.

Thanks Robb… That was a very quick response. . Thank you.

I have actually done a RRSP contribution in the first 60 days in the past and have never had a problem. That may be because I have maxed out my contributions ever since I was 20 (now 69), so CRA has good history on me. I have never overcontrubuted neither. Because my income was high, since I’vd done that, I could always calculate 18% of my income without worrying about contributing to much.

So is this something new, or just a grey area. I’m not sure why the CRA would want this to be a grey area. It seems common sense to me to make this very clear… but interesting… But I know I have done it.

As a side note, when contributing to my RRSP on a monthly or bi-weekly bases in the past, any contributions in the first 60 days each triggered a separate RRSP receipt. I was told it was because the institution did not know which year the client wanted to report the receipt. .. This definitely happened with Sun Life. The choice was mine.

So is this something new now? Because I have done it in the past, I am not sold on this…. But regardless, it just doesn’t make sense for the CRA not to be completely clear on this.

Any further thoughts, I’m interested…

I finally overcame some paranoia about promising to make the contributions and not doing so (ie. Because of losing my job for example) and sent in the form. I did it online. No idea what the expected response time is. There’s no record of the submission online and it’s not currently something the cra tracks for status. So I’m hoping to see something soon. I think it’s been a couple of months at least

Hi Robb

‘Utilize employer matching savings plan’ is great but what do you recommend doing with those funds which are usually managed by an insurance company with limited investment options. I hate the high fees those Seg funds charge so I’ve just left it as GIAs with the thought that at least every pay cycle my investment is matched by the employer so my overall return=100% plus whatever interest peanuts the GIA pays. Or should I be investing into Seg funds? Quite sure time horizon would be relatively short (compared to TFSA/RRSP) as I dont plan working for ever with the same company! And if I quit/get fired, I certainly dont intend keeping on paying the high fees for shitty investment products.

The match far outweighs the fees, so I wouldn’t avoid contributing just because your menu of investment options is poor.

Check for any transfer out policies, and for sure move the funds if/when you leave that employer.

Hi, Robb!

For someone with $125,000 or more gross income, would you still recommend focusing on RRSP first if TFSA is not maxed out yet?

Thanks!

Hi Alex, it really depends on your goals, the province in which you reside, your age, your expected marginal tax rate in retirement, etc.

That’s why I say “optimize” your RRSP contributions. For some, that might be a modest contribution to bring their income down to the bottom of their highest marginal tax bracket. For others, that might mean no contributions at all.

At $125k I’d say there’s a good chance you would benefit from *some* RRSP contributions but it would be impossible for me to say more without knowing more about your situation.

Thanks Robb. Just a note re your comment that “the CRA will approve letters sent throughout the year”. This seems to have recently changed. I submitted my letter in July and got a reply back from CRA that it was rejected as it was too early in the year, and instructing me to resubmit it in October.

Hi Tracey, that comment was meant to say that you can submit the form during the year “for the current year” and get some relief on your taxes.

Submitting for the next year should be done in October to ensure it gets applied in-time for your first pay cycle in January.

Last year I submitted the T1213 form through the CRA My Account document upload in late September and received the CRA’s response by mail in early January (about 3 months later) This year I submitted a little earlier, in mid September, hoping to get the CRA response in time before the January paychecks started. Shockingly I just received the CRA response by mail this week, about six weeks after submitting the T1213. It was by far the fastest response I’ve ever had.

Hi, I’m going on early retirement ( 60years old), my income is 60000. And I’m getting 89000 lump sum which I can divide in to 3 years. I will also get around 40000 in severance pay at the time of retirement. I have 65000 room in my RRSP. I live in BC. How I should divide all those money to avoid overpaying taxes?

Hi Robb

I am in Ontario. Retiring in January

I have $25K RRSP room still. My salary is $120K

Should I contribute to my RRSP now and get the refund in March? Or forget about it to have less in my RRSP

Please advice

Hi Fausto, I can’t give specific advice to you in the comment section – so much depends on your goals and other financial resources.

That said, if you look at Ontario’s marginal tax brackets it could make sense to contribute ~$5,000 to reduce your taxable income to $115,000 (roughly the bottom of the 43.41% marginal tax bracket), ensuring every single dollar contributed gets you 43.41 cents back in tax relief.

https://www.ey.com/content/dam/ey-unified-site/ey-com/en-ca/services/tax/tax-calculators/2025/ey-tax-rates-ontario-2025-06-01-v1.pdf

If a T1213 was approved by the CRA and HR acknowledged, how would this be reflected on the pay slips? Would each pay slip have a new line to reflect the effect of T1213?

Hi Marek, there wouldn’t be a new line on your pay slip – you’d just have less tax withheld at the source.

Hi Robb, do you know if I can submit the T1213 if my priority next year will be to max out contributions to my FHSA instead of RRSP since those contributions are also tax deductible?

Hi MJ, yes you can do that – and I would just indicate that you’re contributing to your RRSP since the effect is the same (a reduction in taxable income). All CRA cares about is that your taxable income ends up reflecting what you indicated in the T1213 form.