My investing philosophy is pretty straightforward. Invest in a low cost, globally diversified portfolio of index funds or ETFs. Add bonds to help smooth out the volatility in your portfolio. Contribute regularly to meet your savings targets. Ignore everything else.

This approach comes from the belief that investing has become largely commoditized. Index tracking ETFs can be purchased and held for close to zero dollars. Furthermore, the academic research and empirical evidence clearly suggests that active management (stock selection and market timing) does not add value after fees.

I’m crystal clear about my philosophy to readers of this blog and to the clients in my fee-only financial planning service. Still, there’s more than one way to build a diversified portfolio of low cost index funds or ETFs.

I need to understand my clients before I can make an appropriate recommendation. I want to determine the client’s current needs and future goals, the rate of return required to achieve those goals, their ability and appetite to invest on their own, and their desire for simplicity versus cost savings.

I’ll use that assessment to recommend one of three investment strategies and model investment portfolios that align with my indexing philosophy and meet clients where they’re at based on those factors.

1.) The Low Cost DIY Approach

Some investors feel confident investing on their own and want to cut fees to the bone. In this case, a simple solution is to open a discount brokerage account at Questrade, which offers free ETF purchases, and then set-up a model portfolio of ETFs. That might look like this:

- BMO Aggregate Bond Index ETF (ZAG) – 40%

- Vanguard FTSE Canada All Cap Index ETF (VCN) – 20%

- iShares Core MSCI All Country World ex Canada Index ETF (XAW) – 40%

*Source: Canadian Portfolio Manager model portfolios

One alternative low cost DIY approach is to simplify your portfolio and purchase one of the asset allocation ETFs offered by Vanguard (VBAL, VGRO), iShares (XBAL, XGRO), or BMO (ZBAL, ZGRO).

Clients using this approach can expect to pay around 0.25% in annual management fees.

2.) The Robo-Advisor Approach

Some investors understand they’re paying too much in fees for their current managed portfolio of mutual funds. They still want a managed solution, but they want to save as much as they can on fees. It makes sense to match these investors up with a robo-advisor.

These online portfolio managers take the guesswork out of investing, putting clients into a portfolio of index funds and ETFs and automatically rebalancing whenever markets move too far or when client’s add new contributions.

But which one to pick? They all have their own strengths and weaknesses, but here’s a quick summary based on fees:

- Wealthsimple is best for portfolios under $250,000

- Nest Wealth is best for portfolios greater than $250,000

- Justwealth is best for RESPs

Clients using this approach can expect to pay between 0.50 and 0.70% in management fees.

Worth noting is RBC InvestEase, which is best for RBC clients who want to switch out of more expensive RBC mutual funds. That’s a good segue into the next approach.

3.) The Stay-At-Your-Bank Indexing Approach

I want clients to save as much as possible, but some investors don’t have the time or skill to become a DIY investor, and some aren’t comfortable with a robo-advisor. That’s okay – there’s still a low cost solution that allows you to stay at your existing bank.

All of Canada’s big banks offer index mutual funds. TD has the most popular and cheapest set of index funds, called TD e-Series funds. Investors who switch to e-Series funds can expect to pay roughly 0.45% for a portfolio containing Canadian, U.S., and International equities, plus Canadian bonds.

RBC clients have the InvestEase option I mentioned earlier, or they can invest in RBC’s suite of index funds for a cost of less than 1% a year.

Scotia, BMO, and CIBC also carry index mutual funds that cost 1% or slightly higher. Still better than their actively managed (or closet index) funds that come with MERs of 2% or higher.

Clients who opt for this approach may need to meet with a bank advisor and demand to switch their mutual funds to these index funds. Expect all the typical rebuttals from your advisor, but stand your ground and insist on the index portfolio.

This Week’s Recap:

On Wednesday, I wrote about my life insurance mistake – not taking out a private policy before leaving my employer group plan.

I published two posts over at Young & Thrifty:

From the archives: Coping with stock market losses.

Finally, on Rewards Cards Canada, what happened to my credit score when I applied for 13 credit cards last year?

What I’m Listening To, Reading, and Watching:

In this new segment I’ll share what podcasts I’m listening to, which books I’m reading or have read, and what I’m watching on TV or YouTube.

Here’s my current weekly podcast lineup:

- Animal Spirits with Michael Batnick and Ben Carlson

- Rational Reminder with Ben Felix and Cameron Passmore

- Freakonomics Radio

- Solvable

- Throughline

Published less often, but still on my list:

- Against The Rules with Michael Lewis

- Mostly Money with Preet Banerjee

- The Knowledge Project with Shane Parrish

- Revisionist History with Malcolm Gladwell

Books I’ve read this year and recommend include Range by David Epstein, Talking to Strangers by Malcolm Gladwell, and Thinking in Bets by Annie Duke.

My favourite personal finance book of the year was Happy Go Money by Melissa Leong.

With two kids (10 and 7) it was a given we’d subscribe to Disney+ when it launched last week. My kids have surprisingly been enjoying the National Geographic content more than the Disney / Pixar content. That’s cool.

My wife and I watched the first three episodes of Star Wars: The Mandalorian – and it’s excellent. I kind of like the release of one episode a week to build the anticipation.

Weekend Reading:

What’s better than a no-fee credit card with up to 4% cash back bonus? It’s stacking a free $75 Amazon.ca e-gift card on top.

Dale Roberts at Cut the Crap Investing looks at living off the dividends and that 4% rule.

Dan Kent at Stock Trades put together a monster post on the 2019 Canadian Dividend Aristocrats List.

Why thinking you’re ‘bad with money’ can become a self-fulfilling prophecy.

Should you roll the dice with an all stock portfolio in retirement?:

“But in retirement the order of stock market and portfolio returns do matter. That’s called sequence of returns risk. A bad year or a few bad years early in retirement can permanently impair your portfolio and your retirement.”

As many as one quarter of Canadians are finding that retirement is not all it’s cracked up to be. It’s so important to ‘find your why’ in retirement.

Rob Carrick says parents are increasingly willing to help their children with the cost of post-secondary and says, don’t blame parents for the student debt problem in Canada.

Nick Maggiulli on Renaissance Technologies and the Medallion Fund: The greatest money making machine of all time.

In his latest Common Sense Investing video, Ben Felix explains why some home country bias is a good thing for Canadian investors:

My Own Advisor’s Mark Seed and PlanEasy’s Owen Winkelmolen do a retirement case study for a couple with $1.2M invested and no pensions.

Tim Cestnick offers five ideas to reduce the clawback of OAS benefits.

Canada’s rental costs are climbing due to strong demand and lack of new supply. This is leading to an increasing affordability problem in Canada’s major cities.

Finally, Scotiabank refused to honour two decades-old GICs until CBC stepped in.

Have a great weekend, everyone!

Life insurance is a must if you have a spouse or children who depend on your income to get by. But asking a life insurance agent if you need more life insurance is like asking a barber if you need a haircut. Of course the answer is going to be ‘yes’. Indeed, the life insurance business has a long history of commission-hungry agents pushing expensive policies onto consumers who would be better off with simple term coverage.

While you should view any life insurance discussion with a skeptical eye, the reality is that many people are severely under-insured. Most group insurance policies at your workplace only provide coverage for one or two times your annual salary. You might need 10 or 15 times that amount if you have a young family at home.

The other challenge with group life insurance coverage is that it’s not transferable – you can’t take it with you when you leave your employer.

Ending My Group Coverage

That’s the situation I find myself in right now. The group coverage I have with my employer is quite generous at 2.5 times salary. They also offer the voluntary option to add up to an additional $500,000 in coverage at favourable rates (each $100,000 in coverage cost just $4.50 per month). I took the maximum optional coverage and increased my overall life insurance coverage to approximately $700,000. My total premiums cost less than $35 per month.

The rational side of me knew that I’d eventually leave my job and would need to take out a private insurance policy. But I didn’t get around to it. Then I quit my job.

Now I’m scrambling to get an insurance policy in place before the end of the year to avoid any lapse in coverage. First, I performed a life insurance needs analysis. A lot has changed in 10 years. My kids are older (11 and 8 next year). We have a lot more money saved. We have less debt. Do we still need $700,000 in coverage? Do we need more?

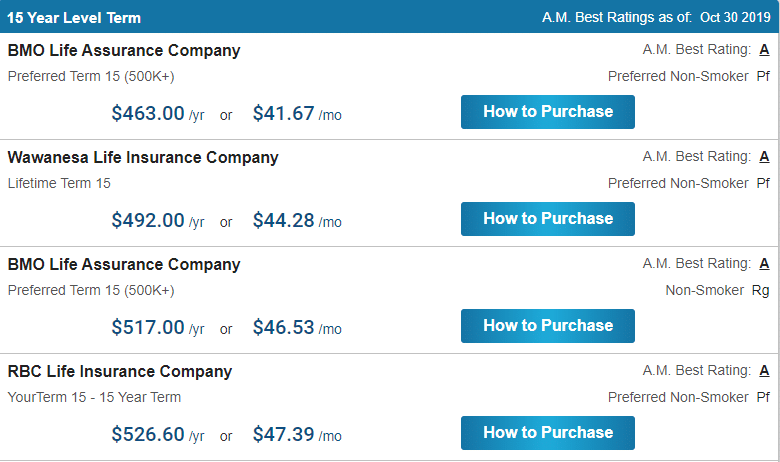

A needs analysis considers things like your survivor’s income and spending needs, years of income replacement, personal and household debt, children’s education, non-registered assets, and final expenses. My analysis found that a 15 year term with $600,000 in coverage would be sufficient.

Term Life Insurance Quotes

I shopped around for term life insurance quotes using the website term4sale.ca (no affiliation). I like the site because it offers unbiased comparisons from various life insurance providers, and I can obtain a quote within seconds (without entering an email address or phone number and risk being hunted down by commission-hungry agents).

Armed with a range of quotes from various insurers, I called my long-time auto and home insurance broker to see what he could do for me. He asked about the quotes and so I shared where I found them. He said his quotes might vary somewhat because the insurer will do a more rigorous interview and examination, which makes sense. After all, I filled out a quick five question form online to arrive at those other quotes.

We settled on one insurer who offered the 15-year, $600,000 term life policy at a price that seemed reasonable (less than $45/month). They set up a 20-minute phone interview, and then arranged to have a nurse visit my home to take blood and urine samples, and to take my blood pressure. Definitely more thorough than an online quote!

Final thoughts

As I await the results to see if 1) I qualify for coverage, and 2) I received an “excellent” health designation to qualify for the lowest premiums, I can’t help but kick myself for making such a rookie personal finance mistake.

Topping up my life insurance with my group coverage provider was the easiest and cheapest option available to me at the time. But in hindsight I should have taken out a private insurance policy much earlier and held it in tandem with my workplace coverage.

Not that I could have predicted I’d be leaving my employment after 10 years and going to work for myself. But the lesson here is that insurance is cheap and plentiful when you’re young and healthy, so you might as well buy as much as you need through a private policy – just in case. After all, isn’t that what insurance is for?

One big decision I need to make as I transition from salaried employee to entrepreneur is whether to take a salary from my business or pay myself dividends. I set up a corporation for my online business back in 2012. My wife and I are 50/50 owners of the small business, and we’ve used the corporation to stream dividends to my wife for the past seven years. I earned a salary and my wife stayed home full time, so this structure allowed us to split our income somewhat and save on taxes.

We’ll need to change things up next year and decide whether to pay ourselves a salary, continue to pay dividends, or come up with some combination of the two.

Pros and cons of a salary

The main advantage of taking a salary from the business is that it will give us a personal income. That means we’ll pay into CPP, and also earn contribution room for our RRSPs. A salary paid out will also be a tax deduction for our small business.

One potential disadvantage is the pain-in-the-ass factor of setting up a payroll account with the CRA and filing all of the related paperwork. We’ll also have to pay into CPP twice as both the employer and the employee. Finally, personal income is taxed at a higher rate than dividend income, potentially increasing our tax burden.

Pros and cons of dividends

We’ll definitely pay less personal tax since dividends are taxed at a lower rate. My quick estimate is an average tax rate of 13 percent with dividends, versus 27 percent with a salary. We’ll also save money (today) by not paying into CPP.

Dividends can be declared at any time, helping smooth out our cash flows throughout the year, and optimize our tax situation come tax time.

Paying dividends is fairly straightforward. We simply write a cheque to ourselves and then update our corporate minute book.

The disadvantages of receiving dividends is that we won’t pay into CPP, which will lessen our entitlements in retirement. We also won’t have eligible income to create RRSP contribution room.

Salary vs. Dividends: Why not do both?

An accountant once told me to pay ourselves a salary up to the RRSP contribution maximum and then top-up with dividends as needed. He also suggested to leave as much money in the corporation as possible to keep taxes low.

Reality check. The RRSP contribution limit is 18 percent of income, up to a maximum of $26,500 (2019). To earn the maximum deduction limit you’d need income of $147,222. Each. That’s not going to happen.

A more realistic approach for us would be to pay ourselves enough salary to max out the Year’s Maximum Pensionable Earnings (YMPE) for CPP. The CPP maximum for 2019 is $57,400.

We plan to pay ourselves between $66,000 and $70,000 each to meet our spending and saving goals. So we could pay ourselves a salary of $57,400 and then top-up with dividends for the remainder of our needs.

This hybrid approach would allow us to max-out our CPP benefits, while also creating ~$10,000 each in RRSP contribution room per year.

This Week’s Recap:

November is Financial Literacy Month and this week I asked whether banks should have a hand in promoting financial literacy.

Over on the Young & Thrifty blog I took a long look at passive investing and why it’s about to finally take off in Canada.

I went on a bit of a shopping spree at Amazon recently, in anticipation of some extra free time on the horizon. I’d like to read more in 2020, and I’m getting a head start now.

I just finished Malcolm Gladwell’s latest – Talking to Strangers: What We Should Know about the People We Don’t Know. In the typical Gladwell fashion, he shares several interesting stories that are all connected around a central theme. It’ll have you questioning your own assumptions around complex topics like police shootings, terrorism, espionage, sexual assault, and deception.

Next on my list is Profit First: Transform Your Business from a Cash-Eating Monster to a Money-Making Machine.

Weekend Reading:

What’s the best Aeroplan credit card? The Credit Card Genius team compares the TD Aeroplan Infinite Visa vs. the American Express Gold Rewards Card.

Not sure how to get the most out of Aeroplan? Read how I maximized Aeroplan flight rewards for our epic trip to Scotland and Ireland.

Millennials are facing all the risk and none of the reward in today’s financial realities.

Millionaire Teacher Andrew Hallam explains how retirees can withdraw more than 4 percent per year from their investments.

Shane Parrish says better “mental models” are vital to improve society. How what’s in our heads changes what’s in the world:

“When we understand how someone sees the world, a lot of their actions and beliefs start to make sense. The medical profession offers a helpful model. Would you think highly of a doctor that offered a diagnosis without first understanding your symptoms?”

Collaborative Fund’s Morgan Housel explains what a spectrum of wealth would look like if you described it with words, not numbers.

Here’s a hodgepodge of smart investing commentary from Downtown Josh Brown and the Irrelevant Investor Michael Batnick:

Dale Roberts looks for an explanation as to why Canadians have given robo-advisors the cold shoulder? I’ve also wondered this.

Another reason to avoid time-shares. A Thornhill woman said she can’t get out of her timeshare agreement more than three years after she paid a company over $4,000 to break the contract.

My Own Advisor’s Mark Seed gives an update as he zeroes in on his financial independence goals.

Finally, this man tested Canada’s tax laws by moving in a canoe – and he won.

Have a great weekend, everyone!