This week I had the pleasure of being a guest on the Rational Reminder podcast with PWL Capital’s Ben Felix and Cameron Passmore. We discussed how I built the blog, my switch from dividend investing to indexing, my thriving fee-only financial planning business, and simplicity versus optimization in your investment portfolio.

Check out the Rational Reminder Episode 11: Simple vs. complex with Robb Engen. While you’re at it, make sure you subscribe to the podcast on iTunes, Stitcher, Spotify, or wherever you get your podcasts. Great intelligent conversations around investing and financial behaviour.

![]()

I want to expand a bit on the simplicity versus optimization discussion. I mentioned that I know I’m leaving money on the table by holding a Canadian listed ETF (VXC) in my investment portfolio instead of getting my U.S. and International stock exposure through U.S.-listed ETFs.

The tradeoff is cost versus convenience. By holding VXC, I’m giving up about 50 basis points in costs due to additional foreign withholding taxes on dividends. By using U.S.-listed ETFs instead, I could bring the total cost down to about 0.20 percent (versus 0.70 percent total cost with VXC).

That said, the U.S.-listed ETFs add a layer of complexity that may not be worthwhile for many investors. Multiple ETFs makes rebalancing more complicated, not to mention more trading costs to deal with. Then there’s the foreign currency conversion trick known as Norbert’s Gambit, which can be problematic to execute even for seasoned investors.

For those reasons I choose, for now, to keep things simple with my VCN and VXC two-ETF portfolio. That choice costs me about $750 a year in higher fees, which is certainly not trivial and will only get higher as my portfolio grows. But it’s a tradeoff I accept right now, perhaps until my portfolio reaches $250,000 or so. Who knows, by then a new product might come along that elegantly solves this problem for Canadian investors.

This Week’s Recap:

Earlier this week I compared Canadian cash back shopping sites, Ebates.ca vs. Great Canadian Rebates.

I finally was able to book our return flights home from Dublin next July. We fly on United Airlines from Dublin to Chicago to Calgary. The reason we chose United Airlines for both our flights to Edinburgh and our flights home from Dublin is because United does not levy any fuel surcharges.

We redeemed Aeroplan miles for both the departure and return flights. Altogether we spent 240,000 Aeroplan miles and just $590 total on taxes, fees, charges and carrier surcharges.

Weekend Reading:

Dale Roberts at Cut the Crap Investing shares his background a DIY investor and lists some ETF model portfolios on his site.

Dale also neatly recaps the week with a weekend reading post of his own (he’s giving me a run for my money!). He includes a great quote:

“Your portfolio is like a bar of soap; the more you touch it, the smaller it gets.”

Jason Heath explains how to reinstate your Old Age Security benefits after they’ve been clawed back.

Personal finance columnist Rob Carrick talks to author Fred Vettese about the best practices to stretch your retirement savings:

Carrick is also set to launch a retirement podcast called A Look Ahead: Rob Carrick’s Retirementality. It debuts with a three-part series starting October 1st.

Her elderly mother sold the family home for $300,000. Here’s how to help a parent invest in their 80s.

Ben Felix tells regulators, lobbyists, and investment firms to go ahead and keep charging deferred sales charges. He’s confident his firm, PWL Capital, will reap the benefits.

Mark Seed, the blogger behind My Own Advisor, says he’s feeling financial trapped as he inches closer to an early retirement goal and is realizing there is more to life.

The Million Dollar Journey blog lists the biggest weed stocks in Canada, along with an ETF to get exposure to the budding industry.

Nick Magguilli looks at abnormal markets and how to prevent forced selling with this gem: Why you don’t know the price until you sell.

Whether or not you need life insurance is a question that many people struggle to answer. In this latest Common Sense Investing video, Ben Felix looks at whether you need permanent life insurance:

Why for baby boomer couples, synchronize or stagger is the new retirement dilemma.

Thinking about retirement? Here are two key income sources to expect.

Consumer advocate Ellen Roseman looks into the Expedia experience: How the giant travel agency treats its customers.

Finally, why some of the best data on human behaviour is privately held by social media companies, and how universities can convince them to share that information.

Have a great weekend, everyone!

Whether you’re clipping coupons, shopping at thrift stores, or lining up at Costco to save on gas, the mark of a good saver is someone who is willing to go the extra mile to save a buck or two. While some frugality traits can border on the extreme, others require less effort than you might think.

Take online shopping, for instance. Websites such as Ebates.ca and Great Canadian Rebates offer consumers the chance to earn cash back from purchases made online. Simply pass through these ‘portals’ on your way to retailers like Amazon.ca or TheBay.com, or before you book a hotel room on Expedia.ca, and you’ll not only earn cash back but also often get access to special coupons and discounts.

Here’s how they work:

Ebates.ca

Ebates.ca launched in Canada in 2012. It now has 4.1 million members across Canada and offers access to over 750 retailers. In the last six years Ebates.ca has paid out over $49 million in cash back.

Members earn cash back when they begin their online shopping at Ebates.ca, click through to one of the partner retail sites, like Amazon.ca, Indigo.ca, Ebay.ca or Expedia.ca, and then complete their purchase on that site.

Or you can download the Ebates Express Cash Back Button, which hangs out in your browser and provides automatic cash back notifications when you visit participating websites.

Ebates.ca tracks your purchase and you receive a percentage of everything you buy back in cash.

Every three months, Ebates.ca sends members cash back in the form of a cheque or PayPal payment.

Some unique features that help Ebates.ca standout from other cash back shopping sites:

- Gift Card Shop, where members can earn cash back on more than 75 gift cards including gas, groceries, dining, and travel.

- Ebates In-Store Cash Back, which gives members the ability to earn cash back when shopping at participating stores nationally.

- Buy online, pick up in-store.

You can join Ebates.ca by clicking here.

Great Canadian Rebates

Great Canadian Rebates was founded in 2008 and serves an estimated 120,000 customers across Canada. The site lists approximately 500 retailers and up to 700 merchants in total.

Members earn cash back when they begin their online shopping at GreatCanadianRebates.ca, click through to one of the partner merchants, like Amazon.ca, TheBay.com, Microsoft.com, or Hotels.com, and then complete their purchase on that site.

Or you can download the GCR Browser Extension, which sends automatic notifications when you visit participating merchant websites.

Once your online purchase is verified then cash back gets deposited into the member’s account and paid out monthly via PayPal or Amazon.ca gift card. Members can also request a cheque anytime their cash back balance exceeds $30.

Some unique features that help Great Canadian Rebates standout from other cash back shopping sites:

- It’s Canadian owned and operated. (Japanese firm, Rakuten owns Ebates.ca)

- It offers a large marketplace for members to sign-up for credit cards from the likes of American Express, Tangerine, MBNA, or Scotiabank and earn $30 to $75 in cash back rebates.

- A generous referral program. Sign up a friend and collect 15 percent of all Cash Back Rebates your referral collects (per transaction) for the next five years.

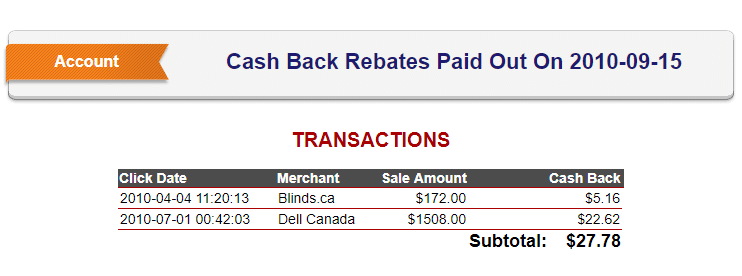

I’ve been using Great Canadian Rebates since 2010 when I first heard about the cash back shopping site. I visited the GCR portal on my way to purchase new blinds for our home, and also to purchase a laptop from Dell. I’ve been earning cash back for my online purchases ever since – sort of a habit ingrained in me now whenever I shop online.

You can join Great Canadian Rebates by clicking here.

How do cash back sites make money?

How do Ebates.ca and Great Canadian Rebates make money? Simple. They get a commission from the store whenever their customers make a purchase. These sites then pass along a portion of that commission back to their members in the form of a cash back rebate.

Think of it as a finder’s fee for sending a purchaser (you) to a vendor (the online retailer).

The Verdict

Cash back websites like Ebates.ca and Great Canadian Rebates allow you to shop at all your favourite online retailers and get money back on purchases you would have made anyway.

Ebates.ca offers a greater selection of retailers. For example, my wife quickly noticed Lululemon on Ebates.ca’s list of retailers, but they’re not listed on Great Canadian Rebates. GCR, on the other hand, has a bit of a cult-like following in the credit card churning community for offering applicants up to $75 cash back in addition to any sign-up bonuses offered by the card issuer.

Average savings could get you 1.5 percent back on electronics, 3 percent back on apparel, 5 percent back on hotels, not to mention the deals, coupons, and promo codes added to each site daily.

By making a habit of stopping by these sites first before you make an online purchase, or by using their web browser extensions, a savvy shopper can easily put money back into his or her pocket for very little effort.

No, I’m not starting my own podcast. But I have started listening to a few good investing podcasts lately and I wanted to share three of them with you. I like these podcasts because they’re smart, quick-hitting, 30-minute talks about investing, personal finance, and current market trends.

The first one, which you’ve likely heard of, is Dan Bortolotti’s Canadian Couch Potato podcast. It’s published infrequently, perhaps once a month, but each one is well worth a listen. Dan typically interviews an expert, from financial planners to financial journalists, to investing and real estate analysts. Then he gets into one of the better podcasting segments out there, Bad Investment Advice, where he’ll call out a poor or misinformed article from a major publication (usually with a scary headline like this crap, Are We Headed For A Passive Indexing Meltdown?). Finally, Dan answers a reader question on investing before wrapping up the episode.

The first one, which you’ve likely heard of, is Dan Bortolotti’s Canadian Couch Potato podcast. It’s published infrequently, perhaps once a month, but each one is well worth a listen. Dan typically interviews an expert, from financial planners to financial journalists, to investing and real estate analysts. Then he gets into one of the better podcasting segments out there, Bad Investment Advice, where he’ll call out a poor or misinformed article from a major publication (usually with a scary headline like this crap, Are We Headed For A Passive Indexing Meltdown?). Finally, Dan answers a reader question on investing before wrapping up the episode.

Second on my list is the Animal Spirits podcast with Ben Carlson and Michael Batnick, two incredibly smart financial writers who work for Ritholtz Wealth Management. Although U.S. based, Animal Spirits explores everything from financial markets to personal finance, to recent articles and books they’ve read, or movies they’ve watched. It’s fast, funny, and full of interesting tidbits from inside their world of wealth management. Animal Spirits airs weekly.

Second on my list is the Animal Spirits podcast with Ben Carlson and Michael Batnick, two incredibly smart financial writers who work for Ritholtz Wealth Management. Although U.S. based, Animal Spirits explores everything from financial markets to personal finance, to recent articles and books they’ve read, or movies they’ve watched. It’s fast, funny, and full of interesting tidbits from inside their world of wealth management. Animal Spirits airs weekly.

![]() My latest investing podcast subscription is The Rational Reminder podcast with Ben Felix and Cameron Passmore of PWL Capital. This new weekly podcast started in August and has already proven to be one of the top investing podcasts in the country. Ben and Cameron have a great rapport and they riff on current events related to personal finance, investing, and financial markets, while unafraid of tackling complex topics like factor investing, behavioural finance, and regression analysis on investment returns. Think of Rational Reminder as Animal Spirits North.

My latest investing podcast subscription is The Rational Reminder podcast with Ben Felix and Cameron Passmore of PWL Capital. This new weekly podcast started in August and has already proven to be one of the top investing podcasts in the country. Ben and Cameron have a great rapport and they riff on current events related to personal finance, investing, and financial markets, while unafraid of tackling complex topics like factor investing, behavioural finance, and regression analysis on investment returns. Think of Rational Reminder as Animal Spirits North.

Not investing related but an honourable mention goes to the Freakonomics podcast by Stephen Dubner. Like the Freakonomics’ books, the podcast explores the hidden side of everything. You’ll be smarter after every episode.

This Week’s Recap:

Earlier this week I compared one-ticket investment solutions from Vanguard and Horizons. Lots of interest in this super simple investing approach that will likely give the robo-advisors a run for their money.

Speaking of podcasts, I’m excited to be a guest on The Rational Reminder podcast with Ben and Cameron next week. Stay tuned for that and I’ll promote and share it when it gets published.

Next week I’ll also be comparing cash back websites Great Canadian Rebates vs. Ebates.ca to see which one can help put more money back into your wallet from your online shopping activities.

Weekend Reading:

Industry regulators have already proposed a ban on discount brokerages charging trailing commissions to self-directed investors. Trailing commissions are intended to pay for ongoing financial advise from a human advisor, but discount brokerages are not legally able to offer advice and so DIY investors who hold such funds are paying for a service they’re not able to obtain.

Ahead of the proposed ban are now two class action lawsuits against TD and CIBC by investors looking to recoup those fees.

That brings up a heated debate over who is at fault: the industry for knowingly charging investors for services they cannot legally provide, or do-it-yourself investors who shoulder the responsibility of looking after their own investments.

Is investing 100% in an S&P 500 index ETF a smart thing to do? While not a bad strategy, experts suggest diversifying globally.

Ben Felix shares his latest Common Sense Investing video and explains why the 4% rule is probably not the best way to plan for retirement, especially if you plan on retiring early:

Jason Heath helps a reader who is concerned about the tax withholding on his RRIF withdrawals. He’s not sure he’s drawing down his investments properly.

Michael James weighs in on the Financial Independence, Retire Early movement: What does FIRE mean?

He also looks at the interest tax deduction when borrowing to invest, a follow up to a previous post about the Smith Manoeuvre.

Kerry Taylor writes the best way to repay credit card debt is by siding with math over behaviour and tackling your highest interest rate debt first.

Nick Maggiulli offers a different perspective on the global financial crisis. He was just starting his first semester at Stanford:

“Coming back to have my first meal at Stanford in January 2009 was when I realized that the university was taking the crisis seriously. At my first meal back my dining hall ran out of croissants and I couldn’t believe it. While houses were being foreclosed and jobs were being lost by millions of Americans, my version of the recession was my parents losing their home and my university running out of pastries.”

Morgan Housel writes about the lessons of predicting financial markets: Fool me three times and I give up.

Finally, a shocking (but not surprising) undercover investigation by CBC to expose Ticketmaster’s secret scalper program.

Have a great weekend, everyone!