We all have quirky behaviours when it comes to managing our money. One trick we fall victim to is called mental accounting. We separate our money into different types of mental accounts, with different rules, depending upon how we get it, how we spend it, and how it makes us feel.

An easy example is when you have funds set aside for something like a vacation or house down payment while at the same time carrying high-interest credit card debt. Or how you decide to spend a $1,200 tax refund versus what you’d do with $100 per month if you had the correct amount of tax coming off your paycheque in the first place.

I’m guilty of mental accounting every month when I budget $1,000 for groceries, $200 for dining out, $125 for clothing, and $75 for alcohol. I manipulate those mental accounts all the time, like when I overspend in one category and just take it out of another (shifting a meal from ‘dining’ to ‘entertainment’ for example).

The Mental Accounting Challenge

Why do we assign money to these mental categories? One answer is to control how we think about it. If we were perfectly rational and could figure out the opportunity costs and complex trade-offs of every single financial transaction then it wouldn’t matter how we label our money – it would just come from a big pool called ‘our money.’ It’s just money, after all; totally fungible and interchangeable.

But because we’re human with cognitive limitations and emotions we need help with our money decisions. That’s where mental accounting comes in and acts as a useful shortcut for what decisions to make.

Another interesting way we classify our financial decisions has to do with the length of time between when we bought an item and when we consumed it.

Nobel Prize winner Richard Thaler studied wine purchases and consumption and found that advance purchases of wine are often thought of as investments. Months or years later, when the bottle is opened and consumed, the consumption feels free, as if no money was spent on wine that evening.

Think of a couple that prepays an all-inclusive holiday to the Dominican versus a couple who books their flight and hotel, but opts for a-la-carte dining and entertainment options. The all-inclusive couple probably paid more for their trip, but since it was prepaid and all of their drinks, food, snorkelling and surfing is included, they likely had a more enjoyable experience than the couple who saved money on flight and hotel, but then had to pay as they go for everything else – feeling the pain of every purchase in the moment.

In the personal finance world, one common way to try and save money is with a ‘no-spend’ challenge for a day, week, or month. The idea is pretty straightforward – try not to spend any money. What we’re really doing is playing a mental trick on ourselves.

It’s damn near impossible to go a day without spending if you think about your money as one big pool of interchangeable dollars. Let’s say your rent is $1,200 and it comes out on the 1st of the month. Does that mean you don’t spend any money on rent from the 2nd to the 30th? Or is it that rent actually costs $40 per day and you simply prepay it at the beginning of every month?

The same can be said for insurance, groceries, gas, electricity, the list goes on. It’s easy to game a no-spend challenge the day after your fridge was filled and your bills were paid.

Indeed, when we talk about a no-spend day what we really mean is we’re not going to violate or manipulate our spending rules today.

Final thoughts

Behavioural economist Dan Ariely says mental accounting is perfectly normal. We’re real people after all, with emotions and stress and annoyance and deadlines and a lot of other things to do.

If we have to think about the pros and cons of our decisions every time we want to buy a specific item such as coffee, gas, an app, or a sandwich, it’s going to be a huge pain in the butt. The creation of complex budget categories often gets people to stop budgeting altogether.

Instead, if you have a hard time controlling your spending, Ariely suggests you decide how much you want to spend on a broad category of ‘discretionary items’ – things you can live without, like special brew coffee, fancy shoes, or a night of drinking.

Take that amount, on a weekly basis, and put it on a prepaid debit card. The opportunity cost of your decisions in this general category will be more apparent and more immediate. It still requires effort, but it’s not as annoying as separate accounts for coffee, beer, and Uber.

According to Ariely, this is one way we can use mental accounting in our favour while recognizing the complexity and pressures of our real lives.

Do you use mental accounting to help manage your money?

Welcome to my latest edition of Weekend Reading. I’m writing from our flat in London, whilst enjoying a coffee on this beautiful Saturday morning. We’re on day four of our 24 day trip to the U.K. that will soon take us up to the Lake District and then into and around Scotland.

London is an expensive city, especially when you consider the foreign exchange into British Pounds. Thankfully, the Canadian dollar has strengthened versus the British Pound over the last year. As of today, 1 CAD will get you 0.64 Pound Sterling. That’s up from 0.58 Pound Sterling last summer.

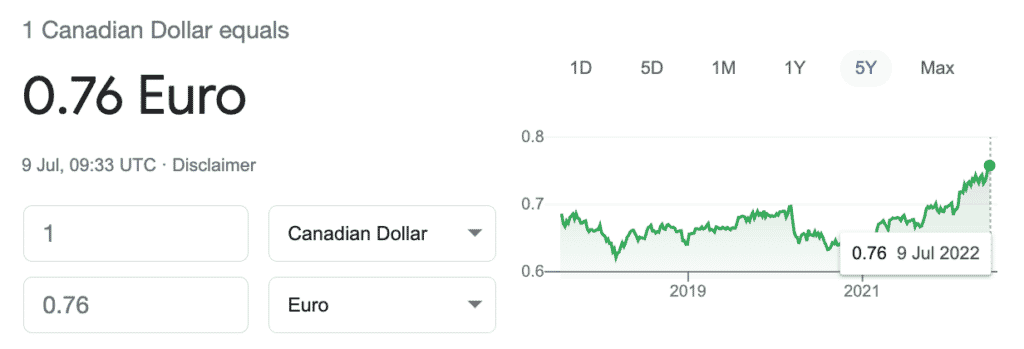

The Loonie is doing even better versus the Euro. Last summer 1 CAD would get you 0.63 Euro, but as of today 1 CAD will get you 0.76 Euro.

Travel is definitely back and the city is absolutely packed with tourists. We tried booking the Warner Bros. Studio Tour London – The Making of Harry Potter, and it was sold out until the third week of August.

Still, we managed to see Wicked at the Apollo Victoria Theatre on our first night here (bucket list experience for my wife and oldest daughter), and braved the heat and endless queue to ride the London Eye.

More exploring of London today before heading to the Lake District for the more relaxing part of our vacation.

This Week’s Recap:

A few weeks ago I recapped the investment performance of various asset classes and sectors so far this year.

I updated our net worth for the year. Portfolio is down, house value is up. An overall small decline from the end of 2021.

Finally, earlier this week I explained why a financial navigator might come in handy at different stages of your life.

I’m putting the final touches on a new course for DIY investors where I’ll walk you through the exact steps to leave your bank managed mutual funds behind and invest on your own using a single asset allocation ETF.

It’ll be like me sitting in your living room, patiently walking you through the process of opening a discount brokerage account, opening the appropriate account types, setting up new contributions, buying an ETF, and transferring over your existing accounts.

Stay tuned for more details soon.

Promo of the Week:

The most frequently asked question about our travels this year? How did you earn enough points to fly a family of four to Europe / U.K. three times in 2022?

My wife and I each have our own American Express Cobalt cards and make sure to charge $500 per month in groceries (not hard these days!) to the cards to earn 5x points on groceries plus a 2,500 point monthly bonus for the first 12 months.

That adds up to 30,000 points for regular spending, plus the 30,000 bonus points for hitting the monthly spending target. There’s 120,000 points combined, which we transfer to Aeroplan to use for flight rewards.

We also signed up for the American Express Aeroplan Reserve Card, where right now you can earn up to 90,000 in bonus points when you spending $1,000 per month over six months ($3,000 in the first three months, and a total of six monthly billing cycles where you spend $1,000).

I know many people will balk at paying a $599 annual fee. But you need to look objectively at your net return after fees. You can earn up to $2,800 in travel rewards with the American Express Aeroplan Reserve Card in the first year of card membership. Subtract the annual fee and you’re still netting $2,200.

For me, as long as I can meet the spending requirements without making meaningful changes to my normal expenses, these cards can make good sense.

Weekend Reading:

A good piece in MarketWatch on why index funds beat stock picking.

Does (fill in the blank) belong in my portfolio? Dimensional offers a general framework for you to assess the merits of a new investment opportunity.

Jonathan Chevreau on why rising rates are good news for near-retirees seeking longevity insurance.

I loved this post by Morgan Housel on the power of staying the course with your investment strategy:

The most important investing question is not, “What are the highest returns I can earn?”

It’s, “What are the best returns I can sustain for the longest period of time?”

PWL Capital’s Ben Felix explains why the “good company is a good investment” fallacy is something that every investor needs to understand:

Dimensional founder David Booth asks about your investing plan for the bear market.

Travel expert Barry Choi explains how to calculate the value of your reward points.

Jason Heath explains what to consider before selling your home or getting a reverse mortgage. The math reveals the real costs for retirees.

Why big banks are blocking online sale of cash ETFs that compete with bank savings products (G&M subscribers).

Finally, a fascinating case of the missing $46 million – the untold story of historic crypto heist.

Have a great weekend, everyone!

I get really nervous when driving in strange places. The anxiety comes from my poor sense of direction – I could get lost in a phone booth. My wife, on the other hand, makes a fine navigator. She could be trapped in an underground cave and still tell which way is north.

We didn’t plan on renting a car during our trip to Scotland and Ireland. We thought we’d mostly get around by walking and taking public transit. That worked out well in a big city like Edinburgh, but after a few days in the Scottish Highlands it was clear that a car would give us more freedom to explore our surroundings.

It’s fair to say I was scared out of my mind, not only to navigate through a foreign land but also to drive for the first time on the opposite side of the road. Still, the prospect of discovering new sights and experiences was too great to pass up, so I steeled my nerves and hired a car from the Inverness airport.

I gripped the wheel tightly, and with my wife deftly guiding us through roundabouts, across narrow roads, and underneath breathtaking viaducts, we discovered new castles, stone circles, and famous battlefields throughout the Scottish Highlands. It was a road trip to remember.

Brimming with confidence, and a newfound sense of freedom, we thought nothing of hiring a car again in Ireland and driving across the country for two-days of sightseeing.

If I were travelling solo, given my lack of navigational skills, I would’ve been forced to use technology to guide me through the journey. But GPS isn’t always fool-proof. Ask the countless number of drivers who’ve followed their car’s GPS directions only to end up in a lake.

Sure, my wife also used Google Maps to help guide us to our destinations. But instead of blindly following the voice commands (like I would do), she would use the satellite view and her keen sense of direction to keep us on course.

Having an expert navigator along for the ride gave me the confidence to do something I never thought I’d be able to do. I’ll be honest, driving in Scotland and Ireland was nerve-racking at times. But it was also a lot of fun, and I’m grateful for the experiences we had thanks to getting out of our comfort zone.

It’s because of those experiences that we had no qualms about renting a car in Italy when we visited in April. We picked up a car in Arezzo and drove to a little hilltop town in Tuscany to stay for a week. Like in the Scottish Highlands, we thought a car would be a must so we could explore all the medieval towns and villages in the region. Unlike in Scotland, we could drive on the right side of the road in Italy.

How Does This Apply To My Finances?

Some people are blessed with a strong sense of direction (like my wife). Others, like me, need help from technology and/or a trusty navigator to guide them to their destination.

When it comes to personal finance and investing, some people have a knack for it, while others need a helping hand.

Related: Your financial plan is a compass

Those with a strong financial compass understand exactly where their money goes, know how much to save, and have enough knowledge to invest on their own.

Unfortunately, some people either have no desire to learn about personal finance, or simply cannot comprehend how to make their money work for them. Like the poor traveller who’d get lost in a phone booth (me again!), those lacking in financial acumen likely need a trusted guide to help them reach their retirement destination, and navigate through all of life’s financial milestones along the way.

Most people, however, seem to fall somewhere in between. They know enough to nail the basics:

- Spend less than you earn

- Save a percentage of every paycheque

- Prioritize your financial goals

- Invest for the future

One solution for these in-betweeners is to pair technology – in this case a robo-advisor, with a navigator – in this case an unbiased fee-only financial planner.

The robo-advisor acts as the GPS, automatically monitoring and even rebalancing your investments to ensure you meet your retirement goals. Robo-advisors aren’t perfect, so while they may not steer you into a lake, most charge a fee in the 0.50% range to take the wheel and manage your investments.

Alternatively, those with a little more confidence in their investing prowess can save money by opening a discount brokerage account and purchasing a single ETF (an asset allocation ETF). With this approach, investors can build a low cost, globally diversified, and mostly hands-off investment portfolio.

So that’s how to manage your investments, leveraging technology to save on fees and build a diversified portfolio. But your investments are really just a small part of your financial plan.

A Financial Navigator

The bigger picture means asking yourself questions like, what are my financial goals for the short and long term? When should I retire? When can I afford to retire? How much do I want to spend in retirement to allow me to live comfortably? Should I take CPP at 60, or wait until 65 or even 70? Do I want to sell my house at some point and downsize, or even rent in retirement?

For answers to these questions you might find comfort talking to an unbiased financial planner. Someone who charges you by the hour or by the project, not based on how much you invest with them.

This type of accountability relationship is a lot like having a trusted navigator by your side. Someone to point you to a potential shortcut, or to avoid the road construction ahead. Perhaps someone to point out when you’re about to turn into a lake.

Are you blessed with a clear sense of direction when it comes to your finances? Or do you need a financial navigator to help guide the way?