Investing has often been an expensive and/or complicated endeavour for Canadians. The vast majority of investors put their money into mutual funds sold by their bank or investment firm – funds which typically charge 2% or more in fees and leave Canadians with less money for retirement. Then along came exchange-traded funds (ETFs), then robo-advisors, and then single-ticket asset allocation ETFs to help transform the investment landscape and drive down costs for the average investor.

What’s been missing is an elegant way for do-it-yourself investors to adjust their risk tolerance over time. It’s easy enough to say that you’ll go from the all-equity VEQT, to the 80/20 VGRO, and then to the 60/40 VBAL as you head into retirement. But when exactly do you pull the trigger and make the switch? Five years before retirement might be too soon. The year before retirement might be too late. Murphy’s Law says you’ll probably get the timing wrong, no matter what you decide. Not to mention the complexities of having a taxable account and triggering capital gains on your entire non-registered portfolio when you make the switch.

I’ve struggled with this type of market timing myself with my kids’ RESP account. I started investing in TD e-Series funds with the 1/3 in each of the Canadian, U.S., and International equity funds. My kids will turn 13 and 10 this year so it’s no longer appropriate to be in an all-equity portfolio. But that means I need to make active decisions on the timing and the allocation towards bonds or cash or GICs. As a passive investor it’s not something I’m comfortable with. I can only imagine how retirees feel as they near their retirement date.

Meanwhile, mutual funds have had the answer to this question for decades with something called a target date fund. Immensely popular in U.S., target date funds are typically only available inside workplace savings programs like a Group RRSP or defined contribution pension plan.

Here you’ll find low cost target date options like BlackRock’s excellent LifePath funds. Pick your retirement date, like the BlackRock LifePath Index 2040 Fund, contribute regular amounts off your paycheque throughout your career, and the target date fund will slowly and automatically adjust the equity allocation in your portfolio as you get closer to retirement. No tinkering required.

So what’s a regular investor to do if he or she doesn’t have access to a workplace savings program? Enter the Evermore Retirement ETFs.

Evermore Retirement ETFs: Canada’s First Target Date ETF

A new solution has been built for Canadian investors called Evermore Retirement ETFs. They’re Canada’s first target date ETF. Investors can choose from eight different retirement paths, starting with the Evermore Retirement 2025 ETF for investors on the cusp of retirement, and moving all the way out to the Evermore Retirement 2060 ETF for young investors with ~40 years of accumulation in front of them.

What got me excited about this suite of products is not just the target date solution, which is much needed in the Canadian landscape, but also that Evermore Retirement ETFs are built with best-in-class, low-cost ETFs from Vanguard, iShares, and BMO. Here’s what’s under the hood of Evermore’s Retirement 2035 ETF:

| Name | Symbol | Total % |

|---|---|---|

| iShares Core S&P/TSX Capped Composite | XIC | 19.20% |

| iShares Core S&P Total US Stock Market ETF | ITOT | 28.80% |

| iShares Core MSCI EAFE IMI Index ETF | XEF | 12.40% |

| BMO MSCI Emerging Markets Index ETF | ZEM | 3.00% |

| Vanguard Canadian Aggregate Bond Index ETF | VAB | 21.60% |

| Vanguard Total Bond Market ETF | BND | 10.80% |

| Vanguard Total International Bond ETF | BNDX | 3.60% |

| Cash | 0.70% | |

| TOTAL | 100% |

These Evermore products launched in February, so they’re brand new to Canadian investors and have only gathered a few million in assets to date. But the building blocks that make up their Retirement ETFs have a proven track record as excellent low cost, passive market tracking products.

They come with a management fee of 0.35%, and after accounting for fund expenses Evermore believes the total MER will be around 0.45%.

This product fills a much needed gap in the market by offering a target date solution for do it yourself investors. I see them fitting in-between a robo advisor and an asset allocation ETF.

- Evermore is cheaper than a robo advisor and uses products that more traditionally align with the efficient frontier of modern portfolio theory (as opposed to adding gold or low volatility like Wealthsimple does, or taking an active approach like Questwealth does).

- Evermore solves the one pain point that asset allocation ETFs fail to address – an appropriate glide path that makes your portfolio less risky as you approach retirement.

The Retirement Glide Path

Evermore’s Retirement ETFs start as with as much as 95% in equities for investors who are 30-40 years away from retirement. The equity component starts decreasing between 30 and 20 years away from retirement until it gets to 80% equities. There’s a steeper decline in equities from 20 to 10 years away from retirement. The 2035 Retirement ETF allocates 64% to equities, while the 2030 Retirement ETF allocates 53.7% to equities. The 2025 Retirement ETF still has 50% in equities.

The glide path continues until you’re five years into retirement when it reaches its minimum of 45% allocated to equities. Note this is considerably higher than many similar target date mutual fund glide paths, which often end up with just 30% of the portfolio in global stocks.

Another interesting change that Evermore makes to their Retirement Income ETFs when the investor is into their retirement years is that it pays out monthly distributions rather than quarterly distributions.

How do you get income from a target date fund? By taking a total return approach, you would spend from the monthly distributions and then sell the number of units needed to meet your income needs. Your portfolio will remain exactly balanced to your time horizon.

When it comes to geographic location, Evermore allocates 30% of its equities to Canadian stocks, 45% to U.S. stocks, 15% to International stocks, and 5% to emerging markets. This is a similar mix to Vanguard’s asset allocation ETFs.

For fixed income, Evermore allocates 60% to Canadian bonds, 30% to U.S. bonds, and 10% to international bonds.

Final Thoughts

Evermore has brought the sophistication of target date investing to everyday Canadian investors with their suite of Evermore Retirement ETFs. Now investors can build a low cost, globally diversified portfolio of ETFs with just a single product and not worry about the right time to rebalance or adjust their asset mix as they get closer to retirement (or in retirement).

Readers, you know I’m a big fan of the saying that investing has been solved with low cost index funds and ETFs. But there are still several ways to build that type of portfolio. Which one is right for you?

Optimizers will want to construct their own portfolio of individual ETFs, paying the lowest cost in exchange for the most effort. Simplifiers will gravitate towards one-ticket solutions like an asset allocation ETF that automatically rebalances.

Hands-off investors may choose to open a robo-advisor account and let the digital advisor manage their portfolio. And, those wary of leaving the big bank environment may opt for the bank’s portfolio of index funds – paying the highest cost for peace of mind and security.

Evermore’s Retirement ETFs add another excellent choice to the mix for investors who want a low cost, single-ticket solution that automatically adjusts the asset mix using a declining equity glide path over time.

They’ll give robo advisors a run for their money in terms of cost and portfolio construction. They also solve a key problem for investors who use asset allocation ETFs (like me!): When and how do I decrease my equity exposure as I get closer to retirement? At some point you need to decide (and time the market) to sell, say, VEQT and move to VGRO, and then sell VGRO and move to VBAL. These Evermore Retirement ETFs take that decision away from investors, which is a good thing in my opinion.

Building on my evidence based investing guide, this article further explores why we invest. When we think of investing it’s only natural to dream about discovering the next Microsoft or Amazon stock or about becoming a world-class investor like Warren Buffett. But why invest in the first place? Is it the thrill of building wealth? Bragging rights at cocktail parties? Or is there a more practical reason to invest?

The truth is most of us invest our money to build a nest egg for when we retire. Our human capital (years of earning paycheques) has been depleted and so we need to replace it with financial capital (savings and investments) to fund our spending in retirement.

Another key reason to invest is because of the silent wealth destroyer known as inflation. If inflation didn’t exist, we could literally stuff our savings under the mattress and use it to fund future expenses. But inflation increases the cost of living, typically by 2-3% each year (yeah, I know). That means something that costs $100 today will cost $300 in 40 years from now.

By investing our money, we hope to earn a rate of return that exceeds inflation (hopefully by a lot) so that we can maintain the same purchasing power over time.

Why Invest Early?

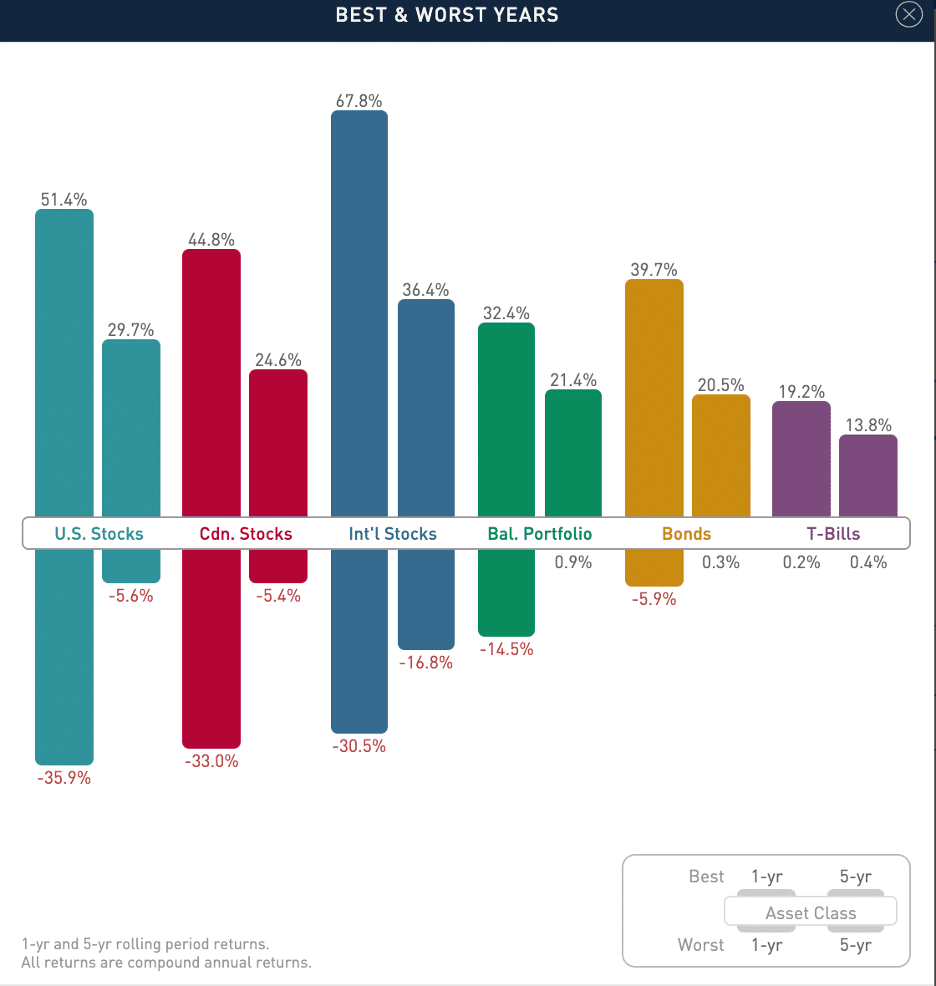

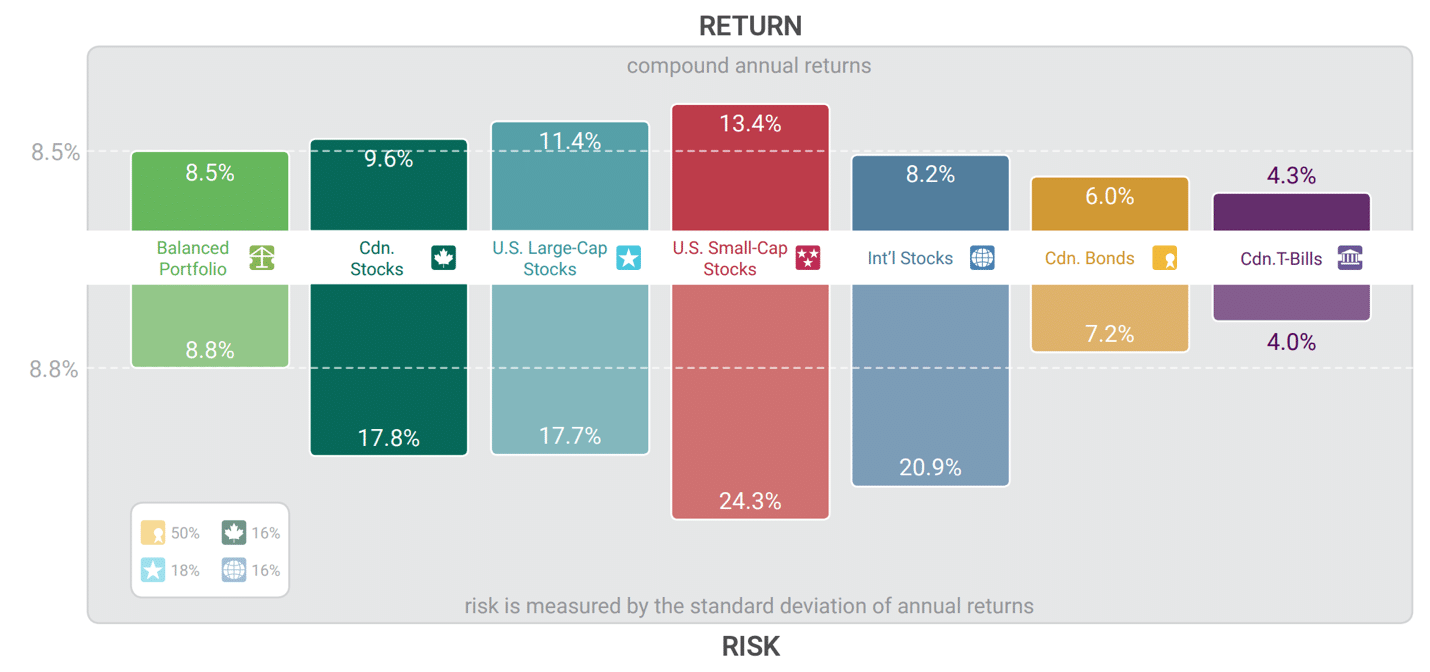

There’s a world of investing options from which to choose, including stocks, bonds, real estate, gold, cryptocurrency, and more. Stocks have been the best and most reliable performing asset class over the long term. Here’s a look at annual stock and bond returns since 1935:

- U.S. stocks – 11.69% per year

- Canadian stocks – 9.74% per year

- Balanced portfolio* – 8.87% per year

- International stocks – 8.29% per year

- Government bonds – 6.00% per year

- Treasury bills – 4.27% per year

- Inflation – 3.41% per year

*A balanced portfolio contains 50% stocks and 50% bonds

Do you see why investing is so important? Let’s say you have $5,000 to invest today and you plan to add $5,000 per year for the next 30 years. How much would you have in your retirement portfolio?

Assuming your investments returned 8.87%* per year for 30 years you would have a retirement portfolio worth more than $729,000. Think about that for a minute. You only contributed $155,000 of your own savings (your initial $5,000 plus 30 years of $5,000 contributions) but because of the magic of compounding investment returns you will have a retirement portfolio worth nearly five times that amount.

That’s the awesome power of investing and also why it’s so important to start investing early.

*We should probably lower our expectations for future returns. Bonds can’t repeat their historical performance with interest rates so low today, and stocks haven’t seen a meaningful correction (yet) since 2008-09. That combination should reduce the expected future returns of stocks to ~6% and for bonds to ~2.5%, which would mean an expected return of 4.25% for a 50/50 balanced portfolio. With that in mind, we should also aim to save and invest more to make up for lower returns.

Risk and Return

The link between risk and return is one of the most important lessons for investors to learn.

Stocks may have the highest expected returns of any asset class over the long term. But in the short-term stocks can be highly volatile. That means stocks have the potential to lose money in the short term. Indeed, any investment made in an individual stock comes with the risk of losing all of your money if the company goes out of business. This happens fairly regularly as strong companies survive, and weaker companies fail.

The lowest average annual returns come from treasury bills, but this asset class has never lost money in a single year. It’s the definition of a risk-free return. Only the most conservative investors who simply cannot handle the ups and downs of the stock market would invest in treasury bills, although retirees may hold a higher percentage of cash in their portfolio to help meet their spending needs.

Bonds are considered to be a safe and secure asset class but in its worst single year bonds lost 5.9% in value (although bonds have never lost money over a five-year period). Bonds are crucial building blocks for your investments and indeed most investors should have some bonds to help reduce the volatility in their portfolio and for rebalancing when stocks fall in value.

To highlight this, a balanced portfolio of 50% stocks and 50% bonds saw a single largest one-year decline of 14.5% and has never lost money over a five-year period. When stocks have fallen, a balanced portfolio has always declined less than a portfolio made up of 100% stocks.

Meanwhile, U.S. stocks have the highest annual average returns over the long term and as you might guess also have the largest single-year decline in value (losing 35.9%). Even the worst five-year period for U.S. stocks saw declines of 5.6% per year, suggesting that stock investors truly need to be invested for the long-term to enjoy higher expected returns.

It’s also important to note that only a small number of stocks drive the vast majority of stock market returns. This is not a new phenomenon, but something that has persisted throughout history. Since 1926, four out of every seven U.S. stocks have lifetime buy-and-hold returns less than one-month treasury bills. That means more than half of U.S. stocks failed to beat the returns you could get just by holding cash.

The “risk-free” rate of return is what you can expect to earn from a guaranteed investment like a GIC. Today that’s about 1.8% on a 1-year GIC.

By definition, any investment that offers higher expected returns must come with some degree of risk. There are simply no guarantees beyond the risk-free rate of return, and if anyone tries to sell you on a high guaranteed rate of return, turn around and run the other way!

Finally, there’s also a measure of risk within each respective asset class. For example, small stocks are more volatile than large stocks but also come with higher expected returns. International stocks come with special risks such as fluctuations in currency, foreign taxes, political and liquidity risks. Corporate bonds are riskier than Canadian government bonds, which are backed by the full faith and credit of the federal government.

Again, risk and return are joined at the hip. In general, the riskiest investments may also come with the highest expected returns. But an investor needs to carefully manage their own risk tolerance to build a sensible portfolio. It wouldn’t make sense for 100% of your retirement portfolio to be invested in the riskiest and most speculative asset class. The goal should be to balance risk and reward as sensibly as you can to achieve your desired rate of return.

Final Thoughts

Investing in sensible portfolio of stocks and bonds has proven to build wealth over the long-term, which can fund your retirement spending and allow you to maintain your purchasing power over a long period of time. Stuffing your money under the mattress isn’t an option. You need to invest to beat inflation.

At the same time, you need to understand the trade-off between risk and reward. The riskiest investments can be highly lucrative but also may cause stomach churning anxiety in the short-term (you may be feeling this right now). On the other hand, the safest investments might not keep up with inflation, so you need to find a careful balance that fits your risk tolerance.

I write a lot about investing. My goal is to help you build your knowledge base so you can decide an appropriate asset allocation, which investments make the most sense for you, and exactly the type of investor you want to be so you can build a portfolio that achieves your retirement goals. That’s why you invest.

Nobel Prize winner Harry Markowitz famously said that “diversification is the only free lunch in investing.” For investors, that means diversifying their portfolio across different asset classes, different sectors, and different geographies. The goal is to reduce risk without sacrificing return. Sounds easy, right?

Investing can be simple, but it isn’t always easy. Think about building a globally diversified portfolio of stocks and bonds. You’d want to have Canadian equities, U.S. equities, plus stocks from international and emerging markets. You’d also want a mix of Canadian and foreign government and corporate bonds. That’s at least seven different funds to hold inside your portfolio.

Thankfully, there’s a better way for investors to build a balanced portfolio without sweating over the individual details. All-in-One ETFs, also known as asset allocation ETFs, hold all the building blocks of a diversified portfolio inside a single fund.

All of the major ETF providers have their own suite of asset allocation ETFs, including Vanguard, iShares, BMO, Horizons, TD, Mackenzie, and Fidelity.

Under the hood you’ll typically find seven or eight individual ETFs representing different asset classes and geographic regions. That means holding thousands of global stocks and bonds in one convenient basket, making it easy for investors to get their free lunch and eat it too.

By the way, the opposite of diversification is called concentration. It’s when your entire portfolio consists of meme stocks, or crypto, or Canadian bank stocks, or just Canadian stocks for that matter.

Sure, there’s always a tiny chance you’ll get lottery-like returns with a concentrated portfolio. But there’s also a better than average chance your portfolio will lose money, at least compared to the overall market. Stocks can go to zero (looking at you, Nortel).

Build a balanced, diversified portfolio with an all-in-one ETF and you’ll sleep easy at night knowing your investment strategy is likely to lead to the best long-term outcomes with less short term pain.

Holding a risk appropriate asset allocation ETF is like driving five kilometres per hour under the speed limit in the right lane of a highway during a winter storm. Sure, it might be boring. But there’s a good chance you’ll get where you need to go, on time, and without much risk of getting into an accident or getting a speeding ticket.

Meanwhile, the left lane may be full of traffic speeding, perhaps aggressively or erratically, towards their destination. Vehicles end up in the ditch, or pulled over for speeding, or paralyzed with fear and driving even slower than the vehicles on the right. Risks abound.

This Week’s Recap:

It’s been a minute since my last weekend reading update. Since then I’ve written the following articles:

- RRSP Loans: Why You Should (and Shouldn’t) Get One

- Lock-In or Ride It Out: The Variable Rate Mortgage Dilemma

- Tax Software For Your Unique Tax Situation This Year

- What Is A Non-Registered Account And How Does It Work?

I have four TurboTax codes to give away to four lucky readers who commented on that TurboTax review. A reminder that these can be used on any paid product (worth up to $279.99 if you go with Full Service Self-Employed).

The lucky winners are:

- Kathryn, who commented on February 24th at 11:00 a.m.

- JimG, who commented on February 24th at 4:01 p.m.

- Jamie, who commented on February 24th at 12:51 p.m.

- Jane Spratt, who commented on February 24th at 2:53 p.m.

Congratulations! I’ll send out your free product codes by email this weekend.

Travel Update

We recently got back from a seven night holiday in Maui. It was so nice to travel again and get a short reprieve from winter.

In just over a month we’ll head to Italy for three weeks, staying in Rome, Florence, and Venice (plus a week in a hilltop town in Tuscany). This is a re-booking of our cancelled 2020 trip.

Then we’ll travel to the U.K. in July, spending just over a week in England (London and Lake District) and two weeks in Scotland.

Finally, we plan to visit Paris for a week in October.

Yes, revenge travel season is upon us.

Promo of the Week:

One credit card that gets a lot of attention from travel and credit card comparison sites but does not get enough love from actual consumers is the American Express Cobalt Card.

This card has always paid 5x points on food and beverage, making it a must have card for groceries and dining out. But a recent change has made those points even more valuable. You see, American Express Membership Rewards points can be transferred 1:1 to other travel programs, including Aeroplan. Aeroplan miles are worth about 2 cents per mile.

Some quick math tells me if you spend $500 per month on groceries you can earn 2,500 points. In one year you can earn 30,000 Membership Rewards points from just $6,000 in spending.

Now transfer those 30,000 points to Aeroplan and you’ll have 30,000 Aeroplan miles. Redeem those miles for a flight at 2 cents per mile and you’ll save $600 on travel.

That $600 reward on $6,000 in spending is a 10% return – on spending you do anyway.

My wife and I each have a Cobalt card and try to charge $500 worth of food and/or beverage to the card every month. It’s an easy way to earn an extra 60,000 Aeroplan miles every year.

Sign up for the American Express Cobalt Card and start levelling up your rewards game.

Weekend Reading:

Our friends at Credit Card Genius have the goods on the new CIBC Costco Credit Card.

Few Canadian seniors are deferring their retirement benefits, even when doing so could mean tens of thousands of extra dollars:

If I recall correctly, the number of Canadians taking CPP at 70 used to be 1%, so I suppose 4% is a decent improvement.

Jason Heath continues his excellent series on what to do with money in a corporation – this one looks at corporate investments for retirees and how to withdraw with minimal tax implications.

Portfolio Manager Markus Muhs explains why dollar cost averaging is good for the soul.

A Wealth of Common Sense blogger Ben Carlson explains eight of the biggest investing myths.

Canadian Couch Potato blogger Dan Bortolotti says it’s a bad idea to retire with more money than you need.

Are you eager to start investing but also worried that the stock market might crash soon? Then you must watch this excellent video by Preet Banerjee to help you get started:

Morgan Housel shares the two things that must be experienced before they can be understood.

Are interest rates going to go up? Is the stock market going to crash? Michael James on Money answers big questions about personal finance and investing.

Millionaire Teacher Andrew Hallam explains how to find the right balance between happiness and spending:

“So here’s how to test whether a purchase might provide an experience that boosts your happiness or well-being. Ask yourself if it creates experiences you wouldn’t otherwise have. A new phone, purse, brand-name clothes, or car likely wouldn’t do it, simply because of hedonic adaptation.”

Erica Alini wrote that renting is supposed to offer mobility and flexibility. So why do so many tenants just feel stuck?

Canada’s housing market could crash or soar, but there’s a more likely third option that nobody is talking about (subs)

Finally, an absolute gem from Fred Vettese on which assets should be drawn down first in retirement (subs). Here’s the conclusion for those who can’t read behind the paywall: Retirees will generally be better off drawing down assets from multiple sources on an annual basis rather than trying to keep their RRSP intact for as long as possible.

Have a great weekend, everyone!