Investors should take great care to choose an investment strategy they can stick with for the long term – in both good times and bad.

The problem is we make our decisions about risk tolerance and asset allocation in a vacuum. Our retirement portfolio isn’t at stake when we fill out a questionnaire. Then markets open the next day and our original target mix gets immediately thrown out of whack.

Overconfidence and Risk Tolerance

It’s easy to feel overconfident about our risk tolerance and investing ability when markets are soaring. And, without proper rebalancing, there’s a good chance your portfolio was overweighted to stocks after markets climbed 20+ percent in 2019.

Then March 2020 happens and stocks fall 35 percent in just one month. Suddenly, investors were scrambling to “de-risk” their portfolios. But the damage had already been done.

I’ve answered many reader questions about changing investment strategies after a market crash. One asked if I still recommend my one-ticket investing solution, Vanguard’s VEQT, given the recent market turmoil. My answer: a resounding yes!

To be clear, I didn’t invest in an all-equity portfolio like VEQT thinking global stocks only go up in price. In the 30-year period dating back to 1990, U.S. stocks were up 21 years and down in nine of those years. That’s a 30 percent chance in any given year that stocks would fall in value.

Volatility

Investors also talk about volatility, and perhaps waiting on the sidelines until things return to normal. But I’d argue when exactly are things “normal” in the stock market? Volatility is the name of the game. In nine of the 30 years between 1990-2020, stocks were up more than 20 percent. In three of those years, stocks were down 16 percent or more. What’s normal?

I get it. Nobody wants to lose money in their investment portfolio. And losing 35 percent of your portfolio in such a short time is shocking to see. But stepping back to see the big picture reveals that Canadian stocks are down 17 percent on the year, while U.S. stocks are down just 13 percent. That’s hardly outside the normal distribution of short-term stock returns.

What I think I’m really hearing from investors is they were taking too much risk in their portfolio leading up to the recent market crash, and now they realize a more balanced portfolio is needed. That’s perfectly fine. It’s just that market crashes are a painful way to learn about your true risk tolerance.

Adding bonds is the best way to reduce the volatility in your portfolio. Vanguard’s VBAL, which represents the classic 60/40 balanced portfolio, fell less than 20 percent at the market low in March, and is now down just 7 percent on the year. That ride is easier on the stomach than VEQT, which fell 27 percent at the low and is still down 11.5 percent in 2020.

Changing Investment Strategies

One trend we saw after the 2008 market crash was for investors to break up with their mutual fund advisor and flock to self-directed investing. After all, active managers couldn’t fulfill their promise to deliver all the upside while protecting the downside. All investments got clobbered.

I can see this trend continuing when investors open their March investment statements and realize their actively managed mutual funds failed to guide them unharmed through the market crash caused by a global pandemic.

This is one time I will advocate for changing investment strategies amid a market crash. If paying high mutual fund fees didn’t deter you from switching to a low cost investing option, perhaps a portfolio decline in the 20+ percent range will be the catalyst.

Final thoughts

Investors shouldn’t be changing investment strategies based on market conditions. We know the expected range of outcomes in both the short and long term.

First, we need to ensure that we’re invested in a risk appropriate asset mix that will allow us to sleep at night. If you can’t stand the thought of portfolio falling 30 percent or more in the short term, then you need to dial back the risk and add more bonds.

Next, in the face of stock market corrections, crashes, or crazy volatility, we need to be able to weather the storm and stick to our plan. That could mean ignoring the news, reducing the number of times you check on your portfolio, and continuing with your regular contribution schedule.

Finally, avoid market timing and trying to guess which direction markets are headed. Your active manager can’t do it, and neither can you. Switch to a passive investing approach, with an appropriate mix of stocks and bonds, that will capture the market returns minus a very small fee.

If I panicked and sold VEQT at its low in March I would have missed out on the ensuing gains made over the following month. And if I step back and look at the big picture, I know my investments were up 20+ percent last year, and they’re only down 11.5 percent so far this year.

Investing is a long-term game and we shouldn’t make investment decisions based on short-term results.

The recent stock market crash and plunging interest rates may have some investors scrambling for safe havens. Stocks fell by as much as 35 percent (before recovering about half of those losses), while the interest rate on GICs and savings accounts in particular have dropped in lock-step with the Bank of Canada’s emergency rate cuts.

Everyone’s situation is unique. First, we all need to be mindful of our personal finances to ensure we have enough cash flow to get through this crisis.

Investors still in the accumulation stage with several years or even decades to go before retirement can confidently stick to a risk-appropriate investing plan.

Those nearing retirement should consider building a safety buffer of cash and GICs to cover their spending needs in the first years of retirement.

Retirees have different goals, such as balancing current income needs with the need to continue growing their portfolio to cover future spending.

One caution for investors of any age is to avoid chasing yield. We’re in extraordinary times, when banks and energy companies have dividend yields in the 7-10 percent range.

As attractive as those yields look to income-hungry investors, it’s not hard to imagine any of these companies, even our treasured banks, suspending, cutting, or even eliminating dividends at some point in the future. There’s a long list of nearly 50 companies that have already done so since March of this year.

On the fixed income side, we know that cautious savers want their money to at least keep up with inflation. One reader asked whether market-linked GICs were worth a look:

“With the GIC rates dropping again, and not being interested in investing in the stock market at our age, what is your opinion on market-linked GICs? Your principal is safe and there’s good upside potential if markets perform well.”

To be blunt, I’m not a fan of market-linked GICs. In fact, you’re most likely better off with plain vanilla GIC.

Remember you cannot have reward without taking risk. The promise of “some market upside” with these products is often mis-sold to investors who think they can have their cake and eat it too.

Banks have pushed market-linked GICs for years as interest rates plunged to historic lows. With this clever marketing gimmick, investors are guaranteed to get back their principal if markets go down, but also get to participate in some of the stock market growth if things go well.

The actual interest rate is linked to stock market returns through a complex formula that requires an advanced degree in mathematics to figure out.

Here’s an example from a few years ago that still holds true today:

This Week’s Recap:

Here are my posts from the past two weeks.

Should you postpone retirement amid the coronavirus crisis?

Last weekend I opened up the money bag to answer reader questions about moving to Questrade, investing in energy stocks, and more.

On Wednesday I listed the top ETFs and model portfolios for Canadian investors.

Over on Young & Thrifty I looked at whether now is a good time to invest in stocks.

The market crash last month may give investors an opportunity to crystallize capital losses in their taxable investing accounts. I’m working on a new piece with Wealthsimple to show how the robo advisor handles tax loss harvesting for its clients. Stay tuned for that in the coming week or two.

Promo of the Week:

I’ve received a lot of feedback from readers who are interested in switching to a discount broker like Questrade or Wealthsimple Trade.

You might want to do so if you’re already a self-directed investor with one of the big bank brokerages and are tired of paying fees for every trade (that’s why I switched from TD Direct to Wealthsimple Trade earlier this year).

Another reason to switch is to simply take control of your finances. Many investors are still heavily invested in expensive actively managed mutual funds with a bank sales person or investment advisor, paying 2 percent or more each year on their investments.

By switching to a discount broker and investing in low cost ETFs, investors can slash their fees to the bone.

Nervous to take the plunge? Try investing in an asset allocation ETF like Vanguard’s VBAL or VGRO, or iShares’ XBAL or XGRO. These one-ticket solutions take the guesswork out of investing because they are automatically monitored and rebalanced behind the scenes so you can focus your time and energy on other activities besides your investment portfolio. Truly a set-it-and-forget-it option.

Wealthsimple Trade is Canada’s first and only zero-commission trading platform where investors can trade stocks and ETFs for free in an RRSP, TFSA, or non-registered account. Sign up for Wealthsimple Trade today.

For most robust investing needs, including for LIRAs, Margin, and Corporate accounts, Questrade is still the king of low-cost investing in Canada. You can purchase ETFs for free and trade stocks for as little as $4.95. Take your savings further with a registered account at Questrade.

Weekend Reading:

Bank of Canada governor Stephen Poloz shares his thoughts on the current pandemic and laying a foundation for the road to recovery.

Rob Carrick is helping his readers through the pandemic with a weekly personal finance update. His latest explains why you should clean out your big bank savings account that’s paying next to nothing in interest.

My Own Advisor blogger Mark Seed explains how he’s preparing his finances for a global recession.

A stark reminder that home equity lines of credit are actually callable loans that can be taken away by your bank in times of trouble.

Carleton associate professor Jennifer Robson offers a great explanation to those of us asking why can’t the government just send everyone a stimulus cheque.

Preet Banerjee has done a great job keeping Canadians informed of federal government stimulus measures, including the most recent changes to the CERB:

Another Carleton professor, Frances Woolley, explains the behavioural economics of the Marie Kondo method. Marie Kondo is the guru behind the best-selling Life-Changing Magic of Tidying Up and Spark Joy.

Morgan Housel asks two big questions – one economic, one more social – that seem crucial to pay attention to as we think about recovery.

Here’s a brilliant thread on Twitter – a Q&A with Costco founder Jim Senegal:

for my marketing class this morning the founder of Costco(!!!) Jim Senegal is speaking & doing a Q&A. does anyone have any questions?

ps Jim is one of the sweetest and most humble people I’ve ever met.

— Paige Doherty (@paigefinnn) April 16, 2020

The latest Canadian Portfolio Manager podcast with PWL Capital’s Justin Bender sheds light on his “Light” model ETF portfolios that include the asset allocation ETFs offered by Vanguard and iShares.

Seniors who don’t need all of their RRIF money this year should consider this workaround.

Here’s Millionaire Teacher Andrew Hallam speaking to retired Canadian investors about what to do with the investments during the COVID-19 market crash:

Michael James on Money uses a personal example to explain how rebalancing does its job.

Finally, is it your dream to work from home full-time? Our friends at Credit Card Genius share 20 ways to work from home.

Have a great weekend, everyone!

Welcome to the Money Bag, where I answer questions and address comments from readers on a wide range of money topics, myths, and perceptions about money. No question is off limits, so hit me up in the comments section or send me an email about any money topic that’s on your mind.

This edition of the Money Bag answers your questions about moving investments to Questrade, investing in energy stocks, government bailouts, and managing investments during uncertain times.

First up is Lisa, who would like to move her investments to Questrade to lower her investment costs and take control of her portfolio. Take it away, Lisa:

Moving to Questrade

“Hi Robb, my investments are currently held in mutual funds at one of the big banks. I’m tired of paying fees, and want to take control of my own portfolio by opening a self-directed account at Questrade.

Can you tell me how to move my RRSP and TFSA investment accounts over to Questrade? Do I need to speak with my current advisor?”

Hi Lisa, first of all, know that you don’t need to break up with your current financial advisor or even speak to him or her at all. Simply open an RRSP and TFSA account at Questrade, request the transfer, and they’ll initiate the transfer for you.

Here’s what I mean:

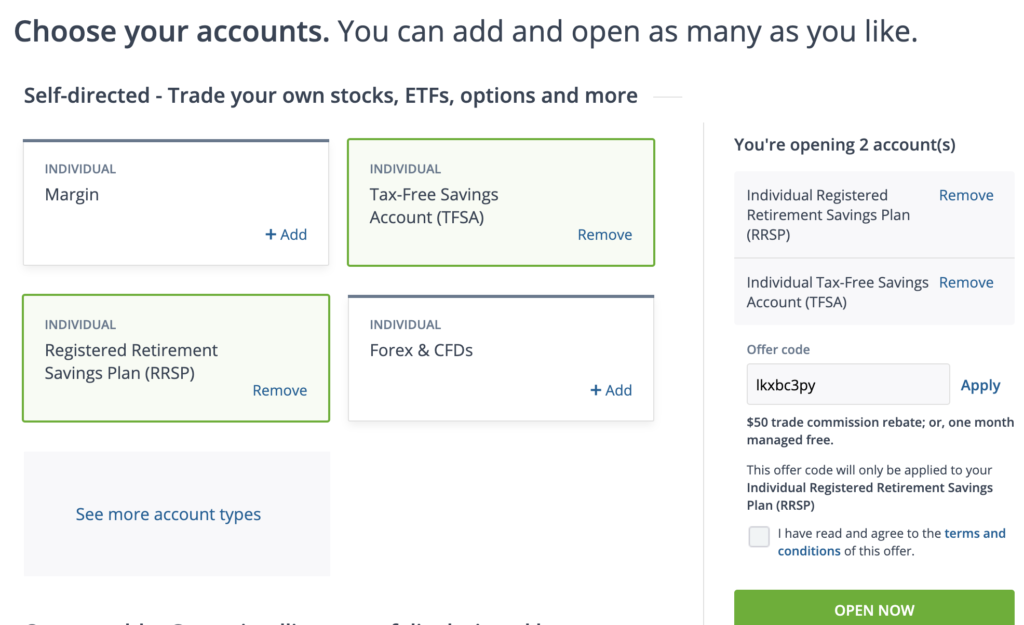

- Go to Questrade

- Click “Open an Account”

- Select ‘TFSA’ and ‘RRSP’

Click ‘Open Now’

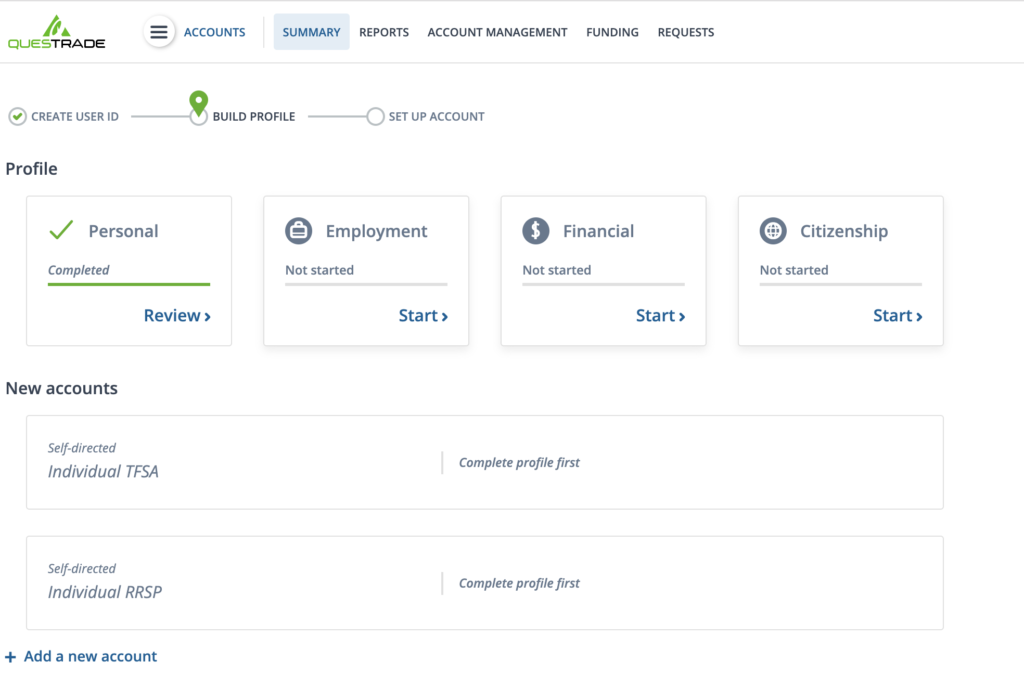

It’ll ask you to create a user ID and profile. Fill out your name, email, and phone number, and click ‘Continue’.

Create a user ID and password.

Once you’ve set up your individual profile and get to the main dashboard, you’ll want to click on ‘Account Management’ at the top of the screen:

- Then click ‘Upload Documents’

- Complete all fields. For Document type, select ‘Rebate’

- Click ‘Upload’

Questrade will even rebate any transfer fees charged from your current financial institution up to $150. To get your fee rebate, send a copy of the statement from your financial institution showing the transfer fee you were charged within 60 days of submitting your transfer request to Questrade.

One important note: As we covered in the last edition of the Money Bag, there are two types of account transfers.

- An in-kind transfer means your investments move over from your current institution to Questrade exactly as is.

- An in-cash transfer has your financial institution liquidate your investments and send Questrade the cash.

Another important note: Assuming you are transferring an account such as an RRSP or TFSA, the transfer will happen within those tax-sheltered containers. Meaning, there will be no tax implications at all. You’re simply moving money to another institution – you’re NOT making an RRSP or TFSA withdrawal.

That’s it. Questrade will initiate the transfer and you’ll have the money within two weeks or so (banks are slow at transferring).

Use my referral link to open your Questrade account. I’ll get a small commission, and you’ll get $50 in free trades.

Investing in Energy Stocks

Next up is Jeremy, who wants to take a flyer on some energy stocks and wonders about the best way to make this investment:

Hi Robb, I have a question. I would like to buy some energy stocks with some money I have sitting around. What is the cheapest, best way to do this?

I am aware of how energy stocks have done and I am also not a stock picker and believe in broad based investing. This is just a small amount of money and I am going to take a flyer on just a few energy stocks.

Hi Jeremy, I don’t advocate for buying individual stocks, and even if I did I’m not sure energy stocks would be at the top of my list. The past five years have not been kind to energy stocks compared to the broad market.

Vanguard’s energy ETF (VDE) is down 61.39 percent over the last five years. Meanwhile the S&P 500, despite its recent turmoil, is up 31.74 percent in that same period.

That said, I can’t begrudge an investor who wants to bet a small portion of his portfolio on individual companies or sectors. As long as it’s money you can afford to lose.

I get the appeal. It doesn’t take a huge stretch of the imagination to see a future where oil prices return to their previous highs.

Individual energy stocks:

Let’s say you want to take 5 percent of your portfolio and invest in energy stocks. A number of dividend paying energy stocks look attractive with yields above 8 percent (i.e. Canadian Natural Resources, Enbridge, Suncor).

Be careful about chasing high dividend yielding stocks. The company may choose to reduce, suspend, or eliminate its dividend, a move which often sends share prices down.

A safer bet might be to look at energy stocks whose price-to-earnings ratio has fallen. These stocks may or may not pay a dividend, so investors would be betting on share prices returning to their former oil-boom glory. Cenovus and Imperial Oil would fit the bill.

Energy ETFs:

How should you invest in energy with little money? Instead of picking one or two individual stocks, the smart play might be to invest in an ETF that tracks the energy sector.

There’s the iShares ETF called XEG. This ETF aims to track the performance of the S&P/TSX Capped Energy Index. If you want to invest in Canadian energy, this isn’t a bad way to do it.

This ETF, like the entire energy sector, has gotten killed over the past five years, but still has net assets of more than $426M. XEG also pays an attractive distribution of 5.6 percent. It comes with a MER of 0.61 percent, which is expensive compared to broad market ETFs but is a reasonably cheap way to invest in 22 Canadian oil and gas companies with just one fund.

Or, look at a similar ETF such as BMO’s Equal Weight Oil & Gas Index ETF (ZEO). It holds 11 large-cap oil companies using an equal weighted approach, rather than XEG’s market-cap weighting. It charges the same MER of 0.61 percent. ZEO’s concentrated approach has led to better returns than XEG, but it’s still down 66 percent over the past five years.

The most cost-effective way to invest in either energy stocks or ETFs is to open a self-directed investing account at either Questrade – which offers free ETF purchases – or with Wealthsimple Trade, a mobile-trading platform that offers zero-commission stock and ETF trading.

Unintended Consequences from Government Bailouts

Wilson would like to know what I think about the unintended consequences of government stimulus during this COVID-19 crisis:

Hi Robb, what are your thoughts on the massive amounts of government bailouts in both the U.S. and Canada? There are people like Ray Dalio and Charlie Munger who suggest that while it may be necessary, the end result is the rich get richer and the wealth gap widens, not to mention inflation, etc.

Ray Dalio was suggesting some kind of paradigm shift coming even before this pandemic.

Hi Wilson. That’s a tough question. In short, I’m in favour of governments doing everything possible to hand out stimulus to individuals and small businesses to help them through this crisis. It must be done, and it must be done quickly.

In fact, I’d be in favour of sending every single person a stimulus cheque, regardless of their circumstances, until the crisis subsides. We can sort out the consequences later, at tax time next year, by clawing back up to 100 percent of the stimulus for those who earn over a certain threshold.

*Note: Here’s a really good argument for why sending everyone a stimulus cheque would not be faster and would not actually reach everyone.

Central banks have proven they can keep inflation under control. Critics thought the massive amount of stimulus injected into the economy during the 2008 financial crisis would lead to hyper-inflation – but that never happened.

I do agree that the wealth-gap is only going to widen. That’s a big problem. But I think the paradigm shift is going to lead to more acceptance of a universal basic income and a larger investment in healthcare.

It’s not the time to worry about how we’re going to pay this bill. People need money now, and I’m glad a large portion of the bailout is going to regular people on Main Street rather than just to corporations on Bay Street and Wall Street.

Managing Investments in Uncertain Times

Finally, Meaghan wants to check in to make sure her personal finance and investing strategy still makes sense during the coronavirus crisis:

Hi Robb, I wanted to touch base with you about the current situation in financial markets. Our current strategy is:

- Keep our focus on our long term retirement goals and not worry (too much!) about short term losses.

- Ensure we have 6-12 month’s emergency cash savings

- Keep my regular diversified investments into RRSPs etc going (with the hope of reducing my cost average)

Is there anything obvious we are missing?

Hi Meaghan, I think you’ve hit the nail on the head. Don’t worry about short term losses. We’ve just seen the largest one-month decline in history. Markets hate uncertainty, but once we see the light at the end of the tunnel then markets should price in the eventual recovery and things could climb just as quickly (as we might be seeing already).

Cash is king, so you’re right to focus on a large emergency cash savings buffer.

One tip might be to divert anything you’re not spending on right now towards your cash savings. For example, we put our gym memberships on hold, saving $118/month. We’re likely not going to be spending as much on dining / take out and instead just preparing meals at home – which will likely save a few hundred bucks a month. We had prepaid a bunch of travel (trip to Italy in April) which has now been cancelled so that refunded money has been put into our emergency savings.

Avoid the urge to put a large amount of money to work in the market right now and instead stick to your regular contribution plan. I know it’s tempting when you see “stocks on sale” but no one has any idea how long this will last and putting a lot of money into the market right now goes against the idea of building up your cash savings.

Rebalance. I’m in the unfortunate position of being 100 percent invested in equities (VEQT) and having used up all of my RRSP contribution room. So I can’t rebalance by selling bonds and buying equities, and I can’t even add to my account because I am all out of room.

That’s okay. I’ve got a long time horizon and I know markets will recover eventually. But it’s a good reminder to be mindful of your true risk tolerance and to ensure you have an appropriate asset mix that you can live with in good times and bad.

Holding bonds, while reducing some of your upside in the long term, is certainly beneficial at times like this because you can rebalance “into the pain” and buy more stocks at lower prices without having to come up with more cash to invest. That’s a good thing.

I hope that provides some comfort. It sounds like you’re in a good position to ride out this period of uncertainty and come out in good shape on the other side. It’s just going to take some time.