No, Passive Investing Is Not In A Bubble

There have been many ridiculous statements made about passive investing over the years. None have garnered as much media attention as hedge-fund manager Michael Burry’s claim that passive investments such as index funds and ETFs are the next bubble. He said these index-tracking investments are “inflating stock and bond prices in a similar way that collateralized debt obligations did for subprime mortgages more than 10 years ago.”

“When the massive inflows into passive vehicles reverse, it will be ugly.” – Michael Burry

Such a bold claim from someone who correctly called the subprime mortgage crisis is certainly cause for concern. But when you peel back the layers, Burry’s statement doesn’t make much sense. Looking for a smarter take than that, I reached out to Erika Toth, a Director of ETFs at BMO Global Asset Management, to explain why passive investing is not in a bubble.

Take it away, Erika:

Debunking Michael Burry’s Passive Investing Bubble Claim

I may not have had Christian Bale play me in a movie, and I did not make millions during the financial crisis, but I have spent years now studying market structure and eating, sleeping, and breathing ETFs. Burry’s comments that sparked a media frenzy (and let’s all agree that the financial media loves to sensationalize) echo some of the most common myths and misconceptions I have encountered on the ETF wrapper.

This “passive investing is in a bubble” argument assumes that all the money invested in passive indices has flowed in to the same indices, that hold the same stocks, in the same proportions. However, there are many different types of passive funds and ETFs – some track the S&P 500, some track indices built around low volatility, quality, value, or momentum filters. Some track specific sectors.

Related: What’s not to love about ETFs?

Different investors have different investment objectives and motivations. Some want to buy the market. Some require higher cash flow. Some require lower volatility. Some are searching to exploit market inefficiencies in order to generate alpha. Pension funds have to make sure their liabilities are funded. Some investors are searching for companies that meet the highest environmental, social, and governance standards. Some require certain tax efficiencies or credit qualities to be met. Therefore, it is impossible that the entire world stock and bond markets would move to 100% passive.

It’s also important to note that individual stock ownership by households (domestic and foreign) accounts for just over half of the equity market – the largest share, by far. Mutual funds (active and passive) own about 24%; ETFs own about 6%. Pension funds would represent about 10% (government and private); and about 8% is owned in other vehicles such as hedge funds. (This is according to data put together by the Federal Reserve Board – see here).

ETFs themselves are too small a slice of the overall pie to be able to cause a crash in the prices of the stocks they hold; they simply reflect those prices. Those statistics are for the equity market. ETF ownership of the global bond market is even smaller, roughly 2-3% by most estimates.

The theory that everyone will run to the exits at the same time in the event of a major downturn is incorrect, and 2008 is a good example of that. My favourite example comes from Ray Kerzehro, who is Director of Research at independent firm PWL Capital, in the still-very-relevant white paper he published in 2016.

Kerzehro examines how high yield bond ETFs in the U.S. traded during the height of the financial crisis. Keep in mind that high yield bonds are NOT a large cap equity index made up of the largest and most liquid stocks in the world – they are a riskier asset class of lower credit quality and are less liquid as well. So, even in this riskier and less liquid asset class, there was actually no massive exodus from those ETFs.

What happened is that trading VOLUME actually spiked. Buyers & sellers of the ETF units had different views for different reasons, and the ETF structure actually provided price discovery to an asset class where many of the underlying bonds had gone no-bid.

Another key point to make is that large ETF providers, who hold the majority of the market share both here and in the U.S., establish minimum trading volume criteria for every security they hold. This ensures that they will be able to offer a liquid market on that security.

The market makers themselves (the plumbing behind the whole ETF eco-system) are also in competition with each other to offer the most competitive bid-ask spreads, which helps keep markets liquid. They make money on transaction volume.

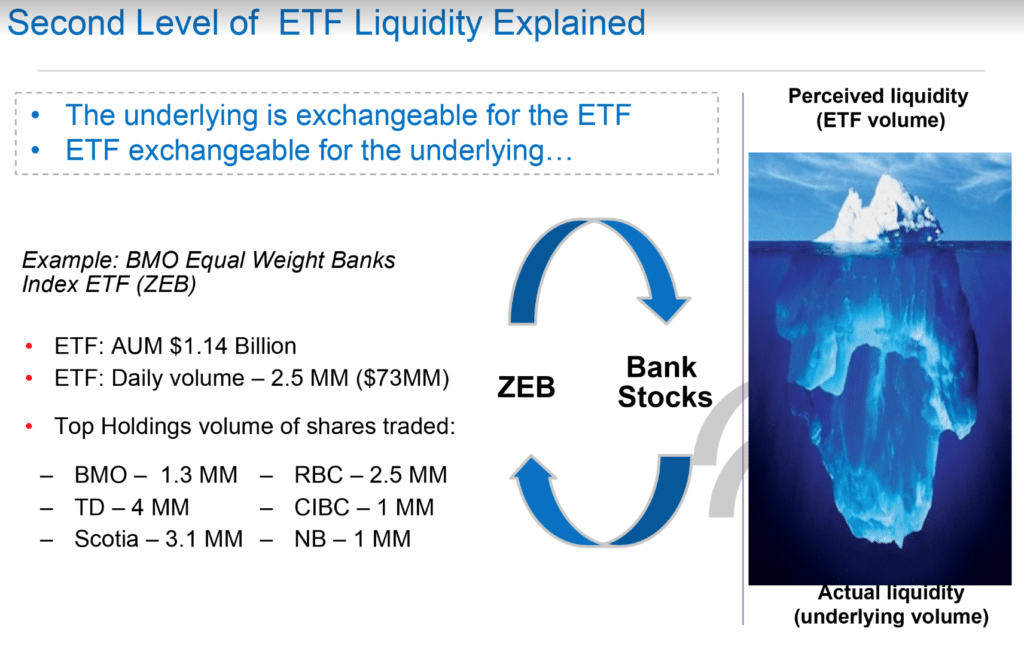

The ETF Liquidity Myth

Another common misconception is surrounding ETF liquidity. ETFs are like stocks in the sense that they trade on the stock exchange. For individual stocks, the higher the trading volume, the more liquid that stock is.

However, with an ETF, liquidity is best measured by its bid-ask spread. In general, an ETF’s liquidity reflects the liquidity of the underlying stocks or bonds it holds.

Related: VEQT – My new one-ticket investing solution

A good way to think of it is that the number of the ETF’s units you see trading are only the tip of the iceberg. The true liquidity is the trading volume of all the securities it holds.

Bid-ask spreads

The bid-ask spread is the difference in what you are able to buy the ETF for, versus the price you would be able to obtain if you are selling it.

This is the best indicator of how liquid an ETF is. A very liquid ETF will have a minimal difference between the two.

The spread represents the compensation to the market maker for assuming the risk and making a liquid market for that security. It is a component of the total cost of ownership of an ETF and is sometimes overlooked by investors. In general, the longer the holding period, the less significant this entry/exit cost is as a component of total cost. If you are more of a longer-term, buy and hold investor, in other words, this should not matter that much. However, if you trade more actively, this is something you should be more aware of.

*An important consideration, especially if the price per unit of that ETF is $50 or higher, is to calculate the bid-ask spread as a percentage of Net Asset Value (NAV). An ETF trading at $50 per unit may be just as liquid as an ETF trading at $25 per unit, even though it appears to have a bid-ask spread that is wider (3-4 cents, compared to 1 or 2 cents on a $25 NAV).

Bid-ask spreads on large, liquid markets such as the S&P 500, S&P/TSX or the FTSE Canada Universe Bond Index – will be very tight at all times.

When you start looking at overseas markets that may be closed during our market hours, it is normal to have spreads that are a bit wider. For European equities, the best time to trade would be between 10 and 11 a.m. Eastern Time. For Asian markets, there is actually no overlap with our market hours.

The best practice is simply to avoid trading too close to the open or the close, and to always use limit orders.

In more volatile markets, it is normal to see spreads widen.

Spreads will also be wider on less liquid areas of the market and on more “niche” exposure ETFs.

Market-weighting versus Equal-weighting

Market cap weighting tilts your exposure towards the largest companies within the index. Equal weighting will give you more of a tilt towards the smaller companies within the index, versus owning the market-cap weighted index.

Over the long term, smaller- and mid-cap stocks may outperform since the risk level is higher. In times of market duress, one may prefer to have a market-weight orientation.

For certain areas of the market that are less diversified, such as Canadian sector equities, investing in a cap-weighted index may result in a very concentrated position in 2-3 stocks. In these situations, it may be preferable to access that sector with an equally-weighted approach.

Related: 3 ways to build an investment portfolio on the cheap

Some portfolio managers and investors prefer market-cap weighting on the other hand, as it provides “truer” exposure to that sector. It is a matter of preference.

Either way, it is important to look under the hood of an ETF and understand what you are owning and why. If you are considering taking an exposure to a particular sector, compare the market weighted version with the equal weighted version in order to determine the differences: long term performance, risk level (standard deviation), dividend yield, how it behaved in negative markets, and identify any concentration issues in certain stocks or sub-sectors.

Final Thoughts

Thanks so much to BMO’s Erika Toth for going under the hood to dispel ETF myths and misconceptions, and to explain exactly why passive investing in ETFs won’t cause a bubble. Bold claims from famous investors make for great headlines, but when we look to the evidence we often find these statements don’t hold water.

Here’s some further reading to help educate investors about the myths and misconceptions of ETFs:

- Debunking the Myths on ETFs

- ETF Due Diligence Checklist

- Understanding ETFs Part 1 – the Basics

- Trading and the True Liquidity of an ETF

BMO Global Asset Management – Understanding ETFs video series:

Robb, you took one sentence out of a larger statement on the subject and then made your argument based on that (through someone else). That’s hardly good journalism. Post the entire article so that we can compare and judge on our own. You are just showing your own personal bias to passive investing. I see enough of that on r/personalfinancecanada and it is so tiresome.

Matt, I think you’re confusing opinion with evidence. Yes, I promote passive investing and ETFs. That’s where the evidence supports the best long-term outcomes for investors. When myths and misconceptions persist, or when one famous hedge-fund manager whose opinion holds a lot of weight contradicts the evidence, I think it’s important to show readers why those statements aren’t fundamentally true (or demonstrably false).

Erika clearly explains why Burry’s claim (or what the media took away from Burry’s interview) that passive investing is in a bubble due to a preference for large cap stocks doesn’t make any sense. She then goes on to explain why other common misconceptions about ETFs (liquidity), and passive investing (price discovery / market inefficiency) don’t line up with the evidence.

When so many are going into the same investments – ETFs, it can cause trouble when those ETF need to unwind their underlying positions. I find it hard to believe that ETF are only such a small part of the stock market.

Weren’t ETF the main reason, the market dropped so far so fast end of last year.

I still think they are great for the average Joe and if you add options to the mix, a safer way to invest (versus black swans that occur more often on individeual stocks).

I guess the future will tell us if Burry or Erika is right. Almost everyone did not see the financial crisis coming.

When so many are going into the same investments – ETFs, it can cause trouble when those ETF need to unwind their underlying positions. I find it hard to believe that ETF are only such a small part of the stock market.

Weren’t ETF the main reason, the market dropped so far so fast end of last year.

We shall see in the future whether Burry or Erika were right.

Don’t get me wrong but ETF were a great invention for the average Joe and add options, it can help to beat the markets (with a little more work). Mutual funds the worse with those high fees and rarely beating the averages.

Calling passive investing a bubble is obviously nonsense, but if we look for some possible truth in Burry’s comments, it may be that we are in a stock market bubble, and the flood of money into passive ETFs has played its part the same as active money in the stock market. Beyond that, I can’t see anything that makes sense. And I don’t see anything passive investors should do other than hold for the long term.

I like this idea of looking at the (relative) bid-ask spread as an indicator of liquidity. I have usually looked to the size of the ETF as an estimate – if more dollars are invested in it, then more likely I’ll be able to sell it easily without impacting the price.