Weekend Reading: High Mutual Fund Fees Edition

We've been beating this drum for years now but a new study by the Canadian Centre for Policy Alternatives suggests that high mutual fund fees could cause Canadians to delay their retirement by as much as 11 years or else leave them with 40 per cent less money for their retirement.

The study compares the management fees charged by mutual funds and pension plans. It finds that in 2014 annual average pension plan fees were 0.38% of assets while comparable mutual fund fees were 2.1%.

Senior Economist David Macdonald, the author of the report, says that Canada has the highest equity mutual fund fees in the world.

“They’re so high that in order to offset those fees the average mutual fund investor will have to work until age 72 to match what a pension plan holder made by age 65, even with identical contributions.”

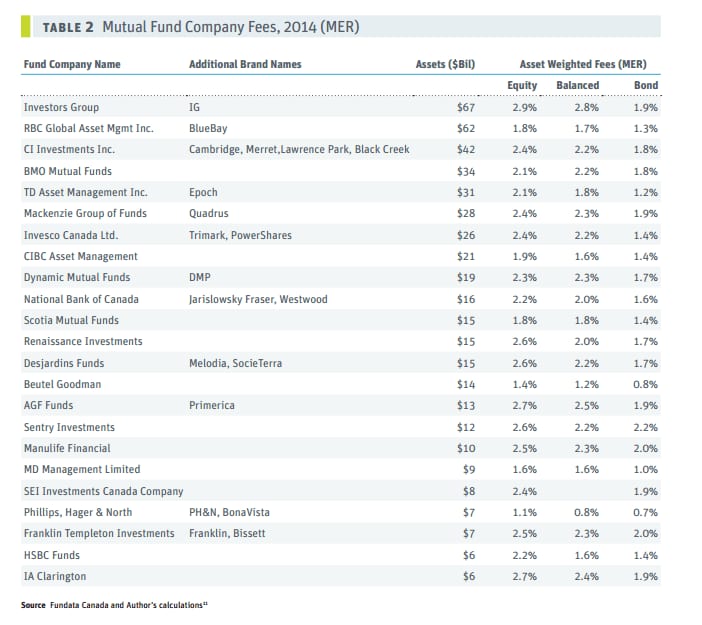

Canadians hold more than $1 trillion in mutual fund investments. This chart shows the largest mutual fund providers in terms of assets under management and compares the average MER of their funds:

This follow-up piece by Amanda Lang says it's up to Canadians to speak up and demand to stop being fleeced by the financial services industry.

This week's recap:

On Monday I wrote about taking a long-term view of your finances. What will the next 20+ years look like financially?

On Wednesday Marie challenged investors to determine their true risk tolerance.

On Friday, Sandi Martin came up with one simple test for your financial advisor.

And on Rewards Cards Canada I'm conducting a poll to determine the top travel rewards credit cards on the market. Go on over and vote for your favourite.

We chatted with Robert Brown, author of Wealthing Like Rabbits, about the joys of RRSP season over on the Because Money show last week. Watch the episode below or go here to read the full transcript.

Weekend Reading:

Ron Lieber, author of The Opposite of Spoiled, says most parents get allowances wrong by starting too late, handing over too little money and responsibility, and tying the money to chores. He says:

“Give your kids just enough so that they can get some of what they want but not so much that they don’t have to make a lot of difficult trade-offs.”

Here's how to do allowance right, according to Lieber.

We all heard the amazing story of Ronald Read, the 92-year-old janitor from Vermont who passed away with an $8 million estate. It inspired this post about whether an average person can gain an incredible net worth through investing.

One way to get there might be to use an investment strategy like the Dogs of the TSX.

Someone who'd know a thing or two about how frugal living leads to a wealthy life is Mr. Money Mustache, the blogger who claims to have retired by 30 to live the good life with his family in Colorado.

Which pays off more: Getting a University degree or investing the tuition money? Jason Heath explains in this Financial Post article.

More Money for Beer and Textbooks author Kyle Prevost shared his view on whether University or College is worth the investment. His advice: Be careful who you listen to.

Everyone can beat the market, according to this Dilbert cartoon.

Speaking of RRSPs, the Blunt Bean Counter explains two tax traps when it comes to RRSP withdrawals.

Michael James takes apart the argument that Canadians are double-taxed on income and capital gains earned in non-registered accounts.

We've all heard of the behaviour gap – the difference between investment returns and actual investor returns. Ben Carlson looks at a Vanguard fund where investors actually outperformed the index.

Financial Post columnist Garry Marr says that even the fathers of the TFSA can't agree on whether to rein in accounts or hike contribution limits.

This advisor heard enough about robo-advisors and decided to try the service out for himself to see how it works.

Finally, Ellen Roseman explained how TD broke its promise by adjusting fees on older Canada Trust accounts and how customers can fight back.

Have a great weekend, everyone!

It’s nice to see that Investors Group hasn’t lost its mojo. Thanks for the mention.

Good old TD Bank. The people’s bank…NOT! I did whatever I had to do to get away from TD.

Try PC Financial, I’ve been a client for the last 16 years (since I got away from TD). There are no additional fees or bank balance requirements. I am a preferred client without maintaining a large balance in my bank account. No interact fees unless withdrawing from an ATM other than CIBC and the list goes on. I can also make a deposit by using my telephone. PC Financial has saved me thousands in bank fees over the years. Check it out.

Thanks

Mia, your story is exactly the same as mine. I loved Canada Trust, they’ve always made me feel valued despite my very small bank account. When the merger happened, we were promised that all Canada Trust customers were going to be grandfathered in but I kept getting nickled and dimed to death and my account was changed without prior notice and lost half my money.

PC was the best move that I’ve ever made and don’t regret it to this day 🙂

Great helpful piece Robb, thanks. If readers want one more credible study to add to their store of knowledge, the “$25 Billion Dollar Pension Haircut” (how much retail fund investors are overpaying when compared to institutional investors) is a good short from Keith Ambachtsheer, global pension expert at the U of T. @RecoveredBroker

https://drive.google.com/file/d/0BzE_LMPDi9UOYTJiY2NmMDEtM2Y4ZS00OTBjLWE3ZjUtNGYxODAzZjkyOTkw/view?usp=sharing

Thanks for sharing this, Larry!