What’s Your Home Equity Release Strategy?

The majority of retirees want to remain in their homes and age in place as long as possible. Indeed, most of the financial plans for my retired clients project them to stay in their home, or a home of equivalent value, for their entire lives.

That makes perfect sense if you plan on leaving your paid-off home to your beneficiaries upon your death.

But, for many retirees, a fully paid-off home represents untapped equity that will lead to underspending throughout retirement, or at least a serious reduction in standard of living as they age.

The solution is to consider a home equity release strategy – a term I first heard last month when Dr. Preet Banerjee wrote about biases around house rich, cash poor homeowners.

Below are the seven different home equity release schemes that were listed:

- Reverse mortgages

- Home Equity Lines of Credit (HELOCs)

- Second mortgages

- Refinancing

- Selling to downsize into a smaller owned home

- Selling to move into a rental home

- Selling to lease-back the same home

Unlocking all or a portion of your home equity can significantly improve your retirement outcome, and yet many retirees are not even considering their own home equity release strategy as part of their retirement plan.

Below I'm going to share an example of a recent retired couple, Joe and Linda Davola, who live in Ontario and retired at the end of last year at ages 63 and 60, respectively.

They have combined assets of $1.4M saved across their RRSPs, TFSAs, non-registered savings, and Joe's LIRA. They also have a paid-off home worth $1.1M for a total net worth of $2.5M.

Joe and Linda would like to spend $100,000 per year after-taxes throughout retirement. They work with an advice-only financial planner to see what's possible.

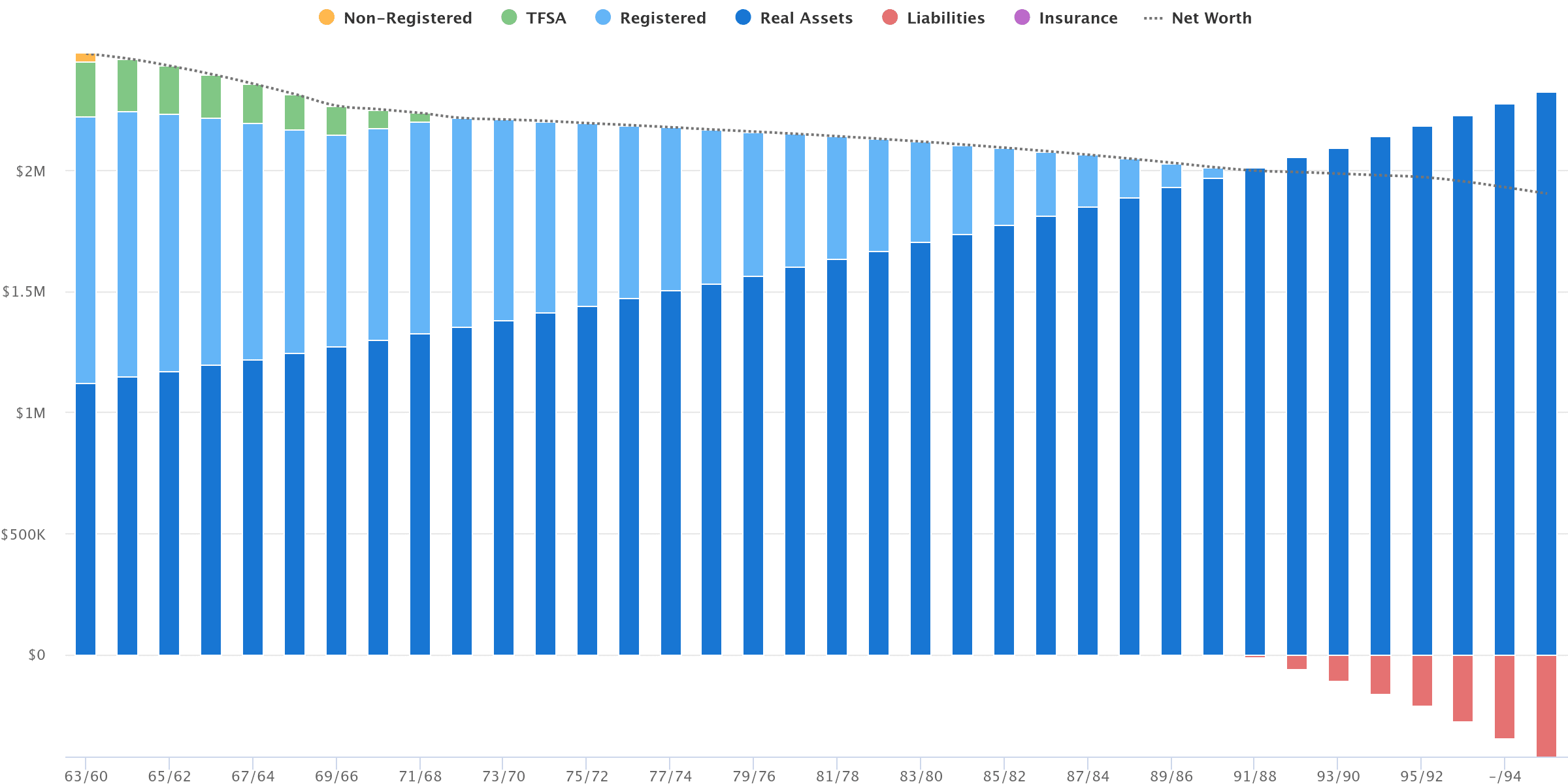

The planner runs a projection that shows after-tax spending of $100,000 per year, rising with inflation at 2.1% annually until Joe's age 75 year, and then increasing by just 1.1% annually until Joe's age 95 year.

In this scenario, Joe and Linda remain in their paid-off home and don't touch the equity. Unfortunately, they run out of money in Joe's age 91 year.

In addition to this less than ideal outcome, the planner also points out that life doesn't always move in a straight line. In fact, they will most certainly incur one-time costs such as home renovations, vehicle replacement, bucket list travel, or financial gifts to their children or grandchildren throughout retirement.

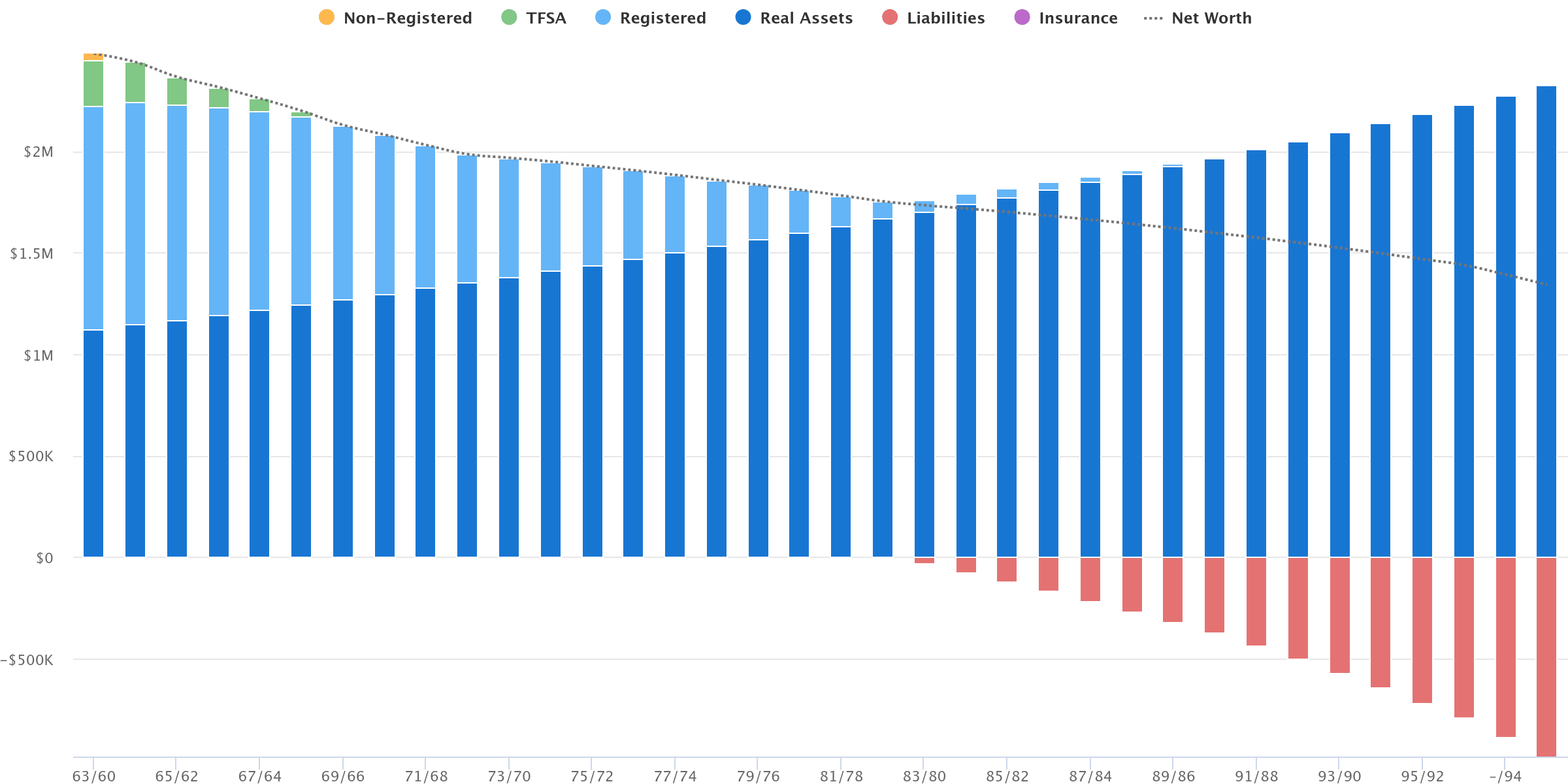

The planner meets with Joe and Linda and together they come up with a list of these one-time expenses that will or may occur over the next 5-10 years.

- Bucket list trip to New Zealand in 2025 – $20,000

- Kitchen renovation in 2026 – $40,000

- Finance a new vehicle from 2027 to 2030 – $12,000 per year

- Upgrade HVAC in 2031 and 2032 – $7,500 per year

When we add the one-time expenses into the plan, and keep spending constant at $100,000 per year, the outcome gets significantly worse. Now the Davolas run out of money at ages 83 and 80, respectively. That's eight years earlier than expected.

At this point it becomes crystal clear that in order to maintain their desired standard of living the Davolas will need a home equity release strategy.

They debate selling the house and renting, but Linda likes the peace of mind that comes with home ownership and worries about rising rental costs and the threat of having to move again.

Home Equity Release Strategy

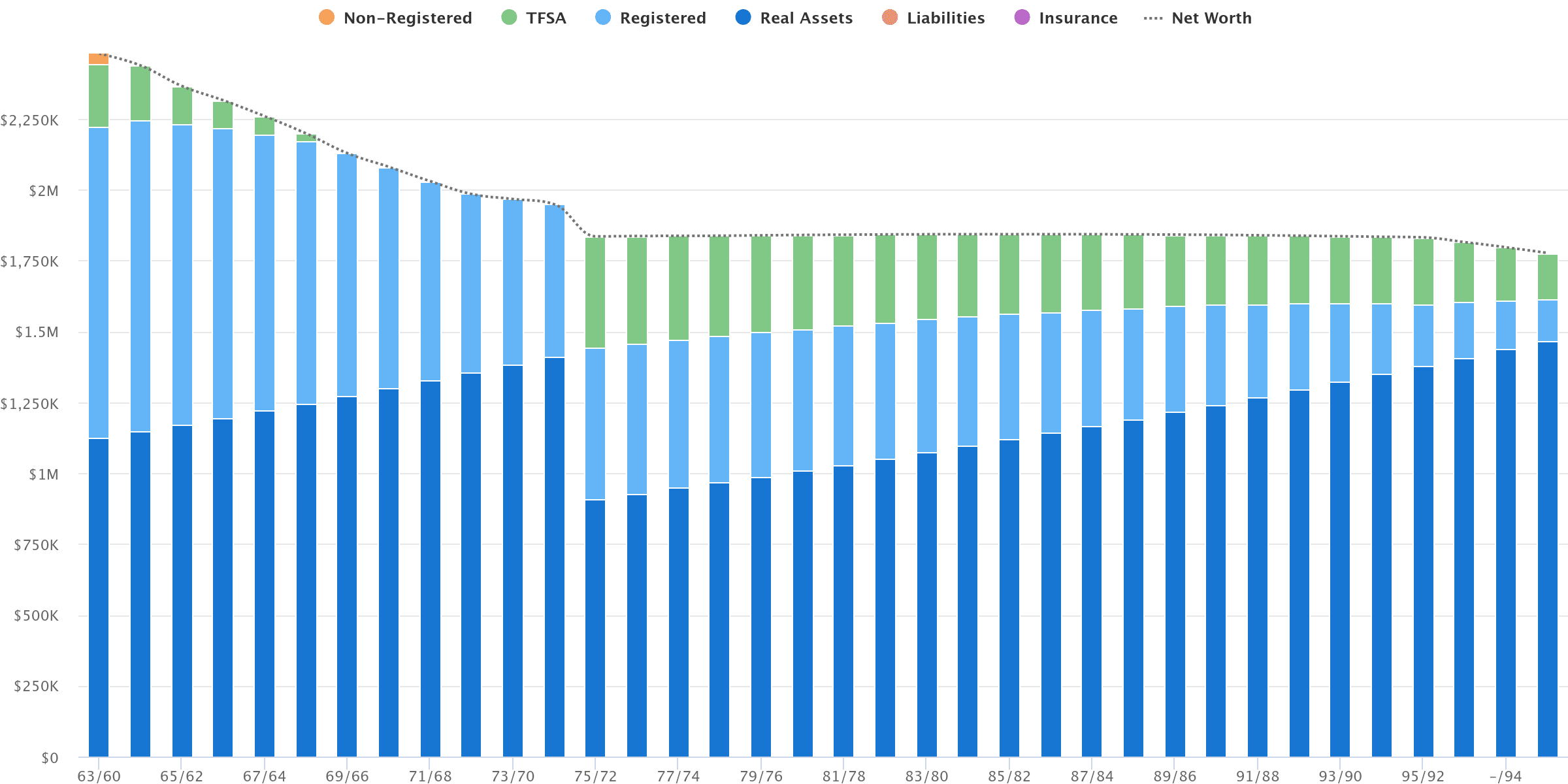

The Davolas decide the best course of action would be to downsize to a condo in 12 years (Joe's age 75 year). They'd sell their home for $1.4M and buy a condo for $900,000* – unlocking half a million dollars in home equity that can be used to maintain their standard of living.

*That $900,000 condo purchased in 12 years is the equivalent of purchasing a $700,000 condo today.

Their planner runs the numbers and suggests that not only can they continue spending $100,000 until age 95, but they can also give an early inheritance of $50,000 each to their two children from the proceeds of their house sale.

Here's what it looks like:

By “releasing” $500,000 of untapped home equity, the Davolas can fill up their TFSAs and give an early inheritance gift to their children.

They can maintain their desired lifestyle until age 95, and still leave an estate to their two children worth $1.73M. That's in future dollars, mind you, so it would be like leaving an estate worth $835,000 today – or the condo plus $135,000 in savings.

Final thoughts

The desire to remain in your home as long as humanly possible and avoid long-term care makes perfect sense. But life doesn't always turn out as planned, and it's wise to avoid making decisions when our options and mental capacity may be limited.

That's why it's smart to consider your home equity release strategy upfront at the beginning of retirement.

Can you honestly see yourself remaining in your family home into your 80s and 90s?

We also tend to drastically overestimate our ability to endure significant spending cuts. I hear all the time from retirees who think they'll just cut $20,000 per year or more from their spending at 75 or 80.

In reality, the decline in spending from the “go-go” years to “slow-go” years to “no-go” years is much more subtle. Like, instead of spending continuing to rise with inflation it rises by inflation minus 1% in your slow-go years, and then simply remains flat in your no-go years.

So, instead of relying on a drastic reduction in lifestyle spending (poor future you!), consider how using all or a portion of your home equity can fit into your retirement plan and allow you to maintain the standard of living that you'd like to enjoy.

And, for my lifelong renters, it's true that you won't have the margin of safety and options that home owners have in retirement, but I'd also argue that if you've prudently saved and invested the (often significant) difference between renting and home ownership, you're already on track to maximize your spending throughout retirement without leaving any untapped home equity on the table.

Hi. Great article. But what about the folks that are going to run out of money (defined contribution pension) and don’t have $millions of equity in their house (ie 600,000). Is there a reverse equity/mortgage idea better than another? We’d like to take some equity in our house while we’re still able to travel and maybe buy a car but not have the bank eventually take the house while we’re still in it. No one to leave it to.

Hi Wendie, thanks! Any of the seven home equity release strategies could be appropriate, depending on your situation. If downsizing isn’t an option, then a line of credit or reverse mortgage would be something to consider.

I think a line of credit is more of a temporary (short-term) financing option, while a reverse mortgage would be more appropriate to help fund a longer-term structural cash flow deficit – allowing you to stay in your home and maintain a certain lifestyle.

Keep in mind with the reverse mortgage you can only borrow up to 55% of the value of your home, and as long as you keep the home maintained, insured, and pay your property taxes then there’s no danger of losing your home.

I didnt notice if CPP and OAS were added into these calculations?

Good catch, Jim!

Yes – CPP is assumed at 75% of maximum for Joe and 55% of maximum for Linda. Both qualify for 100% OAS.

They delay both of these benefits to 70.

“Good catch, Jim!

Yes – CPP is assumed at 75% of maximum for Joe and 55% of maximum for Linda. Both qualify for 100% OAS.

They delay both of these benefits to 70.”

OR

Take both CPP and OAS at 65 which is about 3500/month and invest that in VEQT :))

No Risk No Reward

Great website and I always look forward to a great read

Hi Jim, in this case I would only recommend taking CPP and OAS at 65 if they needed it for cash flow to sustain their spending before the downsizing.

They didn’t, in this case, so best to take the guaranteed 42% and 36% enhancement (before inflation adjustments) by delaying to give them more lifetime income.

With no pension income, I think the best course of action is to increase their guaranteed sources of income to protect against longevity risk.

Yes I was also wondering about CPP and OAS too. Also, I am also hoping that the projected 2.1% inflation mentioned in the article is going to come true. There are many economists / experts out there that believe that those 2% days are gone. Maybe future automation and demographics changes that. Guess we’ll see.

Hi James, the 2.1% inflation figure comes from FP Canada’s projection and assumption guidelines (publicly available on their website and recently updated last month).

Keep in mind these are assumptions about the average inflation rate over the next 30 years, not the last two.

The latest inflation print came in at 2.7% and were trending towards the 2% target by year-end.

While it was not as transitory as central banks would have liked, the pandemic fuelled inflation surge (exacerbated by war when Russia invaded Ukraine) is largely behind us.

Some planners use 2.5% or 3% inflation in their projections. I use the FP Canada assumptions (2.1%), and prefer to be more conservative on future investment return assumptions.

Great article! What Rate of Return is factored in for Joe and Linda? The ‘boomer generation’ is clearly different than the ‘silent generation’. My parents are of the ‘silent generation’ and life was simple (debt for housing and a car only), single income (defined benefit plan for dad (plus CPP, OAS (x2)), and savings (so many CSB’s!! (now GIC ladders)), now both in their 90’s living an assisted life with a mid six-figure net worth and monthly income that covers their expenses. As a ‘boomer’ we have so much more to consider. Robb, I look forward to contacting you for your services.

Hi Ken, thanks! I agree that retirement is more complicated today. A planner can help you fit all of the different puzzle pieces together for your unique situation and retirement goals – so I’m glad to hear you’re thinking about reaching out!

For investment returns I assumed they earned an average of 5% annually across all accounts.

Some condos are more suitable for seniors…like no stairs, low maintenance, close to good healthcare, air quality, transit etc. There are also senior rentals available and subsidies for lower income.

Restaurant prices here have gone up ~30% last 2 years…feels way more than reported inflation. I think if you’re eating out at restaurants or travelling then you need to use higher inflation than CPI.

Hi Bob, it’s a fair point – but those prices are baked in now, and our projections have to be forward looking. In any case, it’s smart for any retiree or near-retiree to track their spending so they have a baseline starting point. Obviously higher spending on travel and dining will come out in the data you’re using.

These are also extremely discretionary categories and easy to cut back on if needed.