Why You Should (or Shouldn’t) Defer OAS To Age 70

I’ve long advocated that anyone who expects to live a long life should consider deferring their Canada Pension Plan to age 70. Doing so can increase your CPP payments by nearly 50% – an income stream that is both inflation-protected and payable for life. If taking CPP at 70 is such a good idea, why not also defer OAS to age 70?

Many people are unaware of the option to defer taking OAS benefits up to age 70. This measure was introduced for those who retired on or after July 1, 2013 – so it is still relatively new. Similar to deferring CPP, the start date for your OAS pension can be deferred up to five years with the pension payable increased by 0.6% for each month that the pension is deferred.

OAS Eligibility

By the way, unlike CPP there is no complicated formula to determine your eligibility and payment amount. That’s because OAS benefits are paid for out of general tax revenues of the Government of Canada. You do not pay into it directly. In fact, you can receive OAS even if you’ve never worked or if you are still working.

Simply put, you may qualify for a full OAS pension if you resided in Canada for at least 40 years after turning 18 (when you turn 65).

To be eligible for any OAS benefits you must:

- be 65 years old or older

- be a Canadian citizen or a legal resident at the time your OAS pension application is approved, and

- have resided in Canada for at least 10 years since the age of 18

You can apply for Old Age Security up to 11 months before you want your OAS pension to start.

Your deferred OAS payments will start on the date you indicate in writing on your Application for the Old Age Security Pension and the Guaranteed Income Supplement.

There is no financial advantage to defer your OAS pension after age 70. In fact, you risk losing benefits. If you’re over the age of 70 and not collecting OAS benefits make sure to apply for OAS right away.

Here are three reasons why you should defer OAS to age 70:

1). Enhanced Benefit – Defer OAS to 70 and get 36% more!

The standard age to take your OAS pension is 65. Unlike CPP, there is no option to take OAS early, such as at age 60. But you can defer it up to 60 months (five years) in exchange for an enhanced benefit.

Deferring OAS to age 70 can be a wise decision. You’ll receive 7.2% more each year that you delay taking OAS (up to a maximum of 36% more if you take OAS at age 70). Note that there is no incentive to delay taking OAS after age 70.

Here’s an example. The maximum monthly payment one can receive at age 65 (as of 2024) is $713.34. Expressed in annual terms, that equals $8,560.08.

Let’s look at the impact of deferring OAS to age 70. Benefits will increase by 0.6% for each month of deferral, so by age 70 we’ll see a total increase of 36%. That brings our annual OAS pension to $11,641.71 – an increase of $3,081.63 per year for your lifetime (indexed to inflation).

2). Avoid / Reduce OAS Clawback

In my experience working with clients in my fee-only practice, retirees are loath to give up any of their OAS benefits due to OAS clawbacks. That means designing retirement income and withdrawal strategies specifically to avoid or reduce the OAS clawback.

The Canada Revenue Agency (CRA) calls this OAS clawback an OAS pension recovery tax. If your income exceeds $86,912 (2023) then the OAS recovery tax will claw back your OAS payments in the period between July 2024 and June 2025. For every dollar of income above the threshold, your OAS pension is reduced by 15 cents. OAS is fully clawed back when income exceeds $142,124 (2023).

So, does deferring OAS help avoid or reduce the OAS clawback? In many cases, yes.

One example I’ve come across many times is when a client works beyond their 65th birthday. In this case, they may want to postpone OAS simply because they’re still working and don’t need the income. In some cases, the additional income received from OAS would be partially or completely clawed back due to a high income. Deferring OAS to at least the next calendar year when you’re in a lower tax bracket makes a lot of sense.

Aaron Hector, financial consultant at Doherty & Bryant, says there is a clear advantage to postponing OAS if someone expects their retirement income to push them into the OAS clawback zone.

“Not only will postponement provide them with an enhanced OAS income, it will also in turn provide them with a higher clawback ceiling,” said Mr. Hector.

It might also allow the opportunity to draw down RRSP/RRIF assets between 65 and 70 which would reduce future expected retirement income (lower RRSP/RRIF assets = lower mandatory withdrawals between age 72 and death).

One could also stash any unspent RRSP/RRIF withdrawals into their TFSA. Growing their TFSA in retirement gives retirees the valuable ability to withdraw money tax-free any time and not have that income affect their means-tested benefits (such as OAS).

3). Take OAS at 70 to Protect Against Longevity Risk

It’s counterintuitive to defer taking pensions such as CPP and OAS (even with an enhanced benefit for waiting) because it forces retirees to tap into their personal savings – depleting their nest egg earlier and faster than they’d prefer. Indeed, people are reluctant to spend their capital.

But this is a good thing, according to Retirement Income For Life author Fred Vettese. Deferring CPP and OAS increases the amount of guaranteed income you will have for the rest of your life, while also reducing your long-term investment risk because you are spending your savings first.

“Spend your risky dollars first because they may not be there for you in your 80s, depending on how your investments do. A bigger CPP (or OAS) cheque, however, will definitely be there for you.”

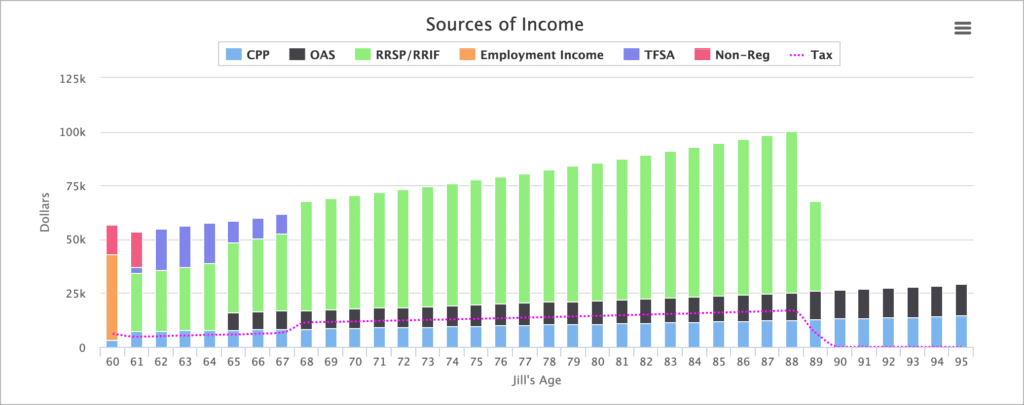

In one example I looked at a single 59-year-old woman – Jill Smith – who plans to retire on July 1st when she turns 60. Jill requires $48,000 in after-tax spending each year to meet her retirement goals.

She has $775,000 saved in her RRSP, plus $75,000 in her TFSA and $30,000 in cash. She’ll qualify for 80% of the CPP maximum and is fully eligible for OAS.

If Jill takes CPP right away (July 2) at age 60 and takes OAS at the standard age 65 she’ll have enough personal savings to last until she’s 89. Her CPP and OAS pensions make up 30.39% of her total annual income in retirement.

Now let’s compare this scenario with deferring CPP and OAS to age 70.

Not only does Jill increase the viability of her retirement plan – her personal savings now last until age 92 – but she has increased the portion of index-protected, paid-for-life government pensions to 54.25% of her total annual income.

Mr. Hector says that someone who fears running out of money in old age would be wise to postpone OAS to guarantee a higher base level of income when they are very old.

So those are three great reasons to take OAS at 70 – to enhance your annual OAS benefit, to reduce or avoid OAS clawbacks, and to protect against longevity risk.

Now let’s look at four reasons why you might not want to defer your OAS pension past 65.

1). The OAS Enhancement Is Less Enticing Than CPP

The actuarial adjustment you receive for deferring OAS to age 70 is much less than it is for deferred CPP to 70. It is just 36% compared to 42% for CPP. That makes a big difference, considering you’re foregoing your pension for five years. You want to make sure it’s worthwhile.

“When I compare the two side by side it really jumps out at you how there is a much greater incentive to deferring CPP than there is to defer OAS. This of course is due to the fact that there is a greater enhancement effect for CPP,” says Mr. Hector.

Ignoring income and clawback concerns, it is best to take OAS at age 65 for someone who is going to die between 65 and 79 for OAS, but for CPP the range shrinks to 65 to 77.

Taking OAS at age 70 gives the best outcome for those who live to age 88 and beyond.

2). Emotional Factor

Fred Vettese is a big proponent of deferring CPP until age 70 but not as enthusiastic about deferring OAS. He says that starting CPP late is already forcing the average retiree to draw down their RRIF balance much faster than they planned on doing. It is still a good move, but one that makes people uncomfortable.

He says asking people to start OAS late as well will accelerate the RRIF drawdown and make people that much more uncomfortable.

3). You Need The Money

Deferring CPP and/or OAS is a luxury for those who have the means to fund their lifestyle while they wait. Repeat: This is not a strategy for those who need to access their government benefits right away to get by.

Mr. Vettese says you need at least $200,000 saved before even considering the deferral strategy.

4). Leaving an Inheritance

Deferring OAS and CPP until age 70 means spending down a good portion of your personal savings in your 60s. This could also mean it’s possible to spend down most if not all of your personal savings before you die.

Related: The Retirement Risk Zone

While this ‘die broke’ strategy may be ideal for some, others may wish to leave an inheritance to their loved ones or to charity.

As there is no survivor-OAS pension, someone who is concerned about leaving a large estate to their heirs may decide that they would rather take OAS earlier so that they can leave their investments intact.

“The investments will always have a value for their beneficiaries but that is not true for someone who opted to defer OAS,” says Mr. Hector.

Final Thoughts

There’s no clear-cut answer for deciding if and when to defer OAS.

When I’m working with clients, I always make sure they understand to at least postpone taking OAS until retirement, or the next calendar year after retirement to avoid OAS clawbacks and additional taxes in the final working year.

Then we look at OAS clawback amounts (if any) and see what can be done to avoid them. Sometimes that means taking more from their RRSP/RRIF in their 60s while deferring OAS until somewhere between ages 67 to 70.

But the bottom line is that deferring OAS to 70 is a bet that you’ll live a long life. And, like with an annuity, rather than worrying about what happens if we die early, we should give more thought to whether we’ll live longer than expected.

With that in mind, deferring OAS by 1-5 years can help transfer the risk from your personal savings to the inflation-protected, paid-for-life government pension program.

The more we can ‘pensionize’ our retirement income, the better off we’ll be if we happen to live an extraordinary long life.

Hi Robb; ” If your income exceeds $77,580 (2019) ” — is that taxable income or gross income?

Also, to avoid some potential clawback based upon too much mandatory RRIF withdrawals, there is the new 2020 ALDAnnuity option — which lets one buy up to 25% of one’s RRIF as an ALDA… thereby reducing the RRIF withdrawals by that 25% amount… which could keep one’s income below the clawback threshold.

We still don’t know what these ALDAs will cost, and what perms and coms they may offer… and therefore if they’ll be of benefit in this fashion.

Cheers!

Toby

Hi Toby, that amount is based on your net income.

Good point about the advanced life deferred annuity. I haven’t dug much into this option but I’m hoping to either interview an expert or have a guest post on the topic.

If you take OAS at 70, the maximum claw back cut-off income amount is slightly above $143,000.

I am 74 and receiving OAS & CPP. My spouse is 60 and is receiving a private pension. Combined we receive around $37000/yr in net income. I do not pay tax on my OAS & CPP, my spouse has income tax deducted monthly on her pension. When I look at the GIS eligibility it would seem to me that if I stopped receiving my OAS, we would qualify for the maximum GIS which would give us an additional $600 per month (approx). Am I wrong? Can I even defer my OAS now that I have been receiving it for 9 years.

You have to be receiving OAS to qualify for GIS and, also note that OAS received is not included in your income calculation to qualify for GIS. (It might be included, but then it’s deducted further down in the calculation, so in the end it’s not!)

It’s interesting that the issue of deciding to receive OAS at 65 in order to qualify for GIS is never included in the discussion.

Hi Tony, If I want to take oas at 70 when do I apply.

If you happen to die earlier than you anticipated then it mayters not whether you delayed or not…you will be dead! However if you live a long life you will really benefit from delaying. No brainer really….delay if you can afford to.

To be clear: The clawback is based on your “net income before adjustments”, which is line 234 on your income tax return. There are certain deductions that do not apply to this net world income. Income splitting, if available in your specific situation, can be applied before line 234. I point this out as there is more than one interpretation of “net” and “gross” income.

Excellent advice Robb! Sadly, very few other planners will give this kind of unbiased advice. Pretty much every commission-based advisor says to take CPP at 60 and not touch RRSPs until 72, which allows them to collect more commissions for a longer time period. I’m not sure if this is done with profit (theirs) in mind or not, but I do know that I agree with you completely when you say that delaying is in most people’s best interests.

Steve

Thanks Steve! It’s such a personal decision that’s based on everyone’s unique circumstances, so I don’t want to make blanket rules of thumb that everyone must follow. Instead, I like to present the options, discuss the facts, and show clients (and readers) how these decisions can impact their retirement situation (for better or worse).

For sure – at the end of the day it’s a personal decision, but financially it is usually (but not always) best to delay. Sometimes I see my job kind of like a doctor- the patient may really enjoy smoking and not want to quit, but it’s my job to show you that quitting is best for you and your family. Many people feel like taking CPP at 60 is what they WANT to do, but I see our job is to show them what’s best for them. Like you, I am agnostic when it comes to the best solution – at the end of the day it’s the numbers that will tell the story.

Ironically, as someone who intends on retiring early and will have a lot of CPP dropout years, I may end up taking my CPP at 60!

Can someone explain how having many CPP dropout years will affect whether I delay or not? I am 61, still haven’t taken CPP or OAS, didn’t intend to until 70. However, I have not worked since 58. Would appreciate further detail on this point. Thank you very much.

Marianne, I will defer to Robb but I would recommend hiring someone like Doug Runchey (contact him at DR Pensions) to run specific calculations for your personal circumstances.

Steve

I don’t understand the benefits of deferral. On is naively banking on a unknown mortality. Also ,when you defer you are leaving money on the table. For example 5 years worth of payments that if taken at 65 can be invested in the market toward property etc. When one waits to age 70, one is working backwards in that your higher benefits first have to go toward the monies lost for the 5 year deferral plus any investment income from that money. Only typically, according to a banker I know, approximately age 77 does either decision coincide, but at this point the benefits start to accrue in the postponement, but still at 77 the person receiving at 65 has a 12 year head start on the initial 5 year early payments received.

The government, of course loves deferrals as statistically many people will die earlier than expected; disease, accidents, you name it, just ask God. Hence the payouts cease and one is out of luck. I took my CPP at 60 and am still benefiting by the investment benefits of monies I would otherwise never have had.

I like to think of it this way: is it better to get a lesser lump sum of a lottery win or the full amount in installments? The answer, I believe is obvious, otherwise what is the stock market for?

If you do the math, by deferring taking your OAS until 70 rather than 65, you miss out on around $35,000 for the five years. You will be 84 before you get this money back by getting the $200 more monthly after you turn 70. So, the question is….Do you feel lucky? If you live past 84 you will likely not care about the extra $200 a month and it will be worth a lot less after 19 years of inflation…..

Jay, the other consideration is the tax savings you gain by deferring OAS and CPP. You can take out more of your RRSP/RRIF money at a lower tax rate if no other (or at least less) taxable income. This also helps estate planning, as large amounts left in RRIFs are taxed at death as income. This can be quite considerable and makes probate look like chump change.

The OAS is $614.14 monthly. The average CPP payment is $710.41 monthly. This leaves lots of room to take out RRSP or RRIF money before hitting OAS clawback or a higher tax bracket.

If somebody wants to give me $100.00, I will gladly give him back $20.00. I am still $80.00 ahead of having nothing…..Being able to split your income with a spouse is also a huge benefit. Putting off taking the OAS is like gambling, similar to an annuity or life insurance policy. You are placing a bet that you will live long enough to recoup the $35,000.00 lost.

Statistics are not favourable.

Way long past published date, but article came up in my feed so…GIS is a solid reason to take OAS at 65 and postpone CPP. With proper allotment of withdrawals from TFSA’s, cash on hand and (judiciously) RRSPs, one could qualify for the GIS even though one has substantial financial resources. Not saying whether this is right or wrong, ethically, but getting up to $900 plus OAS plus draining in taxable TFSA as needed and non registered cash reserves sounds pretty good to me.

Life expectancy for male Canada 2017 is 82.25 yrs. For male U.S. 78.54yrs.

https://lifeannuities.com/aldaquote.html

HI Robb;

This is the only site where I could find a firm offering to give a quote for an ALDA. I didn’t investigate yet, but you might want to check them out… based in Montréal which may have a Québec twist to it…?

Cheers!

Toby

The average life expectancy of a male Canadian is 82 years. However the life expectancy of a 65 year old Canadian male increases by 19.4 years (84.4).

Further a 70 year old Canadian male, average life expectancy increases to 85.3 years. These are just averages, so many are likely to live considerably longer.

Future investment returns are also expected to be much lower on account of the new low interest rate environment we’re in.

Also, I’d suggest doing a google and YouTube search of Boomer Retirement Crisis to see some pretty scary stats on retirees finances. As well as the forecasts about the significant underfunding of public and private pensions.

10,000 Baby Boomers are turning 65 years old, per day each and every day between now and 2030. In 2025, that increases to 12,000 Baby Boomers reaching 65 daily in the USA.

Hey Robb, how would the math shake out if you didn’t need OAS early but took it as soon as possible and invested it in something relatively conservative like VBAL. Say you obtained an average 5% return for those 10 years and lived to the average Canadian life expectancy of 82 years. How does this compare to the guy who delays until 70 and lives to the same age?

Scott

I never thought of that, what if the ROI on early or normal (65) withdrawal earned 5% (actually a good adviser should be able to average 6%) versus leaving it in there until 70?

Does that 1. mitigate those 36 and 42% increase in payments 2. reduce the risk of dying before at least breaking even?

I was leaning towards taking both at 70 and taking out that current estimated amount from my RRSP until then (to simulate taking it all at 65).

I await Robb’s answer and/or analysis with numbers.

The main reason I wanted to take it out at 70 was to have the biggest cushion possible for later years when who knows what happens generally and what happens to my saving/RRSP etc and if I still have the cognitive to handle my investing in as productive way as I do now (in FIRE since 54).

Right on Scott. Take the OAS and invest it inside a TFSA and you pay no tax and it grows tax free as well.

OAS and the average monthly CPP payment in Canada anounts to under $16,000.00 a year leaving lots of room to take out Retirement money – especially if you can income split.

I’m 66 and plan to move abroad and not to apply for CPP nor OAS until I’m 70. I will be applying for both from abroad.

Over the 4 years I’ll be living abroad and no longer working nor residing in Canada will my CPP amount increase by 8.4% a year and OAS by 7.2% year.

What gets missed in the OAS discussion is that it is funded from general government revenues, and benefits could change at the whim of the government. One real possibility: the government could ratchet down the clawback income level. Another reason to take the OAS money and run as soon as it is offered.

Thanks for the excellent article. I’m curious as to your total rate of return and inflation assumptions you used for your conclusions regarding running out of savings at 89. Thank you.

Current strategy is to have employment income end in year I turn 70 (June) as current income places me well in the recovery tax zone and money isn’t needed. Can I wait to apply until following January so both CPP & OAS are be paid retroactive to my 70th birthday? In this way income in subsequent tax year is under $80,000 even with 1 1/2 years of enhanced OAS/CPP in my 71st year as other sources are tax free and/or preferred.

If a new resident person qualifies for 10 years of residence by the age of 68. Would the personal also receive a 21.60% increase on the partial 10/40 OAS payment?

If somebody decides to defer OAS till 70 (because of increased benefit), he/she lose the GIS supplement too, right? But is this lose forever, or only for the period for his/her deferral of OAS ? And when he/she starts receiving OAS at 70, then he/she becomes eligible for the GIS supplement too? Please clarify. Thanks for response in advance.

You need to be collecting the OAS to be eligible for the GIS. Deferring your GIS payments for 5 years, or any time after age 65, would not be wise as you would be giving up so much more than your increased OAS would pay you. Delaying CPP may however prove beneficial as it would also enhance your GIS benefit.

This was a great article , gives lots to think about. My question is I worked for the provincial government and when I reach 65 and receive OAS my provincial pension drops , if I defer the OAS how will that affect my provincial pension , will it still drop even though I am not collecting OAS?

I deferred my OAS until July 2021, but then I sold my house and my OAS will be subject to clawback. So my question is, Can I defer my OAS again…this time to July 2022?

I am wondering about the inflation consideration.

Helicopter money from all Governments will probably ignite inflation.

OAS and CPP are indexed to inflation. Your bond and stock portfolio’s are probably not. Low future returns coupled with inflation could be problematic for some. If your close to retirement you’ve been around long enough to know markets go down as well.

Delaying until 70 would maximize indexed income if inflation is a concern…..and you can tap

other income sources to get there.

Just a consideration in the calculation.

Totally agreeing with Ralph about inflation ahead…

This is very much my concern now and knowing the OAS is indexed is comforting for me, as a very healthy 60 year old female. The challenge will be bridging until then, as my income isn’t high and I don’t have another pension.

Great article and a helpful, refreshing perspective. Thanks

If you take OAS at 70 in 2021, maximum income before all clawback is used is more than $129,581. It is north of $140K.

Rob, can you please provide the calculation as to what that number north of $129,581 is?

Is the husband’s income considered in the computation of the wife’s OAS if he is still working and the wife isn’t.

I know this is an older post but, I thought my comments might be of interest to anyone currently planning their retirement.

We plan to take the CPP at 66 but we will defer the smaller OAS until 70. Our pension, employment and investment income are high and with a combined large RRSP, we will be in a position to have all the OAS clawed back. We’ll start to slowly deaccumulate our RRSP’s to keep our incomes at below the highest tax bracket and then when we reach 70, we’ll apply for the OAS which will be 36% higher.

Why are we not deferring the larger CPP? Both CPP payments are near the maximum and we are concerned that there are no survivor benefits for a surviving spouse if one of us prematurely dies. So if one of us dies, we lose one entire CPP payment.

One small factor this article failed to mention, regarding the clawback or CRA pension recovery tax, yes your payments increase by 36% but the clawback threshold also increases by 36%. This changes the clawback from $79,000 – $129,000 (approx) to a future $107,000 – $175,000 (approx). Delaying our OAS allows us to start our RRIF’s at 71 without a total loss of our OAS. Yes, we will also lose an entire OAS if one of us dies but it’s a smaller amount than the CPP, even if we defer our OAS until 70.

Hi Wally. Why would the clawback threshold change if you defer? Both my wife and I have healthy DBPs as well as other significant income in the year I will turn 65. So this is an issue that I have been trying to nail down. I am thinking I should defer at least one year, but if you are always going to be in the clawback range and you defer will your increased OAS not be partially clawed back forever.

Hi Ron, this article from Aaron Hector can help shed some light on the OAS clawback threshold ceiling: https://www.tewealth.com/oas-clawback-secrets-for-the-high-net-worth/

“So, while the clawback floor is a fixed number which is set each year by the CRA, the clawback ceiling is not a fixed number. Rather, it’s a sliding number based on the amount of OAS that you actually receive. Sure, if you take OAS at age 65 (like most people), your clawback ceiling for 2019 is going to be the stated $125,937. But if you’re receiving higher payments due to postponing your start date, you’ll have a higher clawback ceiling. For example, if you delay your OAS to age 67, you’ll actually have a ceiling of nearly $133,000, and if you delay your OAS to age 70, your clawback ceiling will exceed $143,000.”

Hi Ron,

The key for us in delaying the OAS is the 36% increase on the clawback threshold. We also have healthy DBPs. I’m currently 63, and if I take the OAS at 65 we’ll both loss 100%. However, if I delay, I’m confident we’ll receive something by the time we reach 70. Inflation will increase OAS payments and also increase the clawback. First world problems here, but the OAS clawback at 100% is a tax too far. On the clawback, here is an article in the Financial Post:

https://financialpost.com/personal-finance/retirement/the-oas-clawback-ceiling-isnt-as-firm-as-you-thought-and-heres-how-you-can-take-advantage

All good points, Robb, but the fact is that no decision regarding uptake of CPP or OAS should be made in isolation. One’s income from other sources and the nature of those sources (ie: registered or unregistered, DB pension, employment, etc.) and the resulting taxation must be estimated for each year of retirement. CPP and OAS uptake combinations can be run in various scenarios (as can age to convert registered savings plans to registered income plans or other options). I have not seen a case when, for those who can fund the delay, that taking CPP at age 70 is not the optimum, by a significant amount. The calculations tend to point to age 70 as the optimum to take OAS as well, but they do not result in a significant change in what I call “terminal balance” (the amount left after a reasonably optimistic life span). You have pointed out scenarios when delaying OAS to 70 would be wise, but generally, people should take their OAS at 65. This will help alleviate feelings of “missing out” if they have not started their CPP yet. As a rule, people should not take their CPP before age 66 as they will give up significant income, but after that the return-to-potential-longevity starts to decline, so it isn’t a slam-dunk to start at 70. If it makes a person more comfortable, they are not giving up much to start CPP at 67 or 68.

BTW – Early retirement (eg: 55) is no reason not to delay CPP until age 70. You will still get significantly more by delaying even if it means adding years of zero contributions.

If you are a US resident, is there a clawback of OAS?

I am trying to figure out one thing about OAS.

I turned 65 in August 2022 and planning on retiring by the end of the year.

I came to Canada in 1996 when I was 39 years old so if I was to take my OAS when i turned 65 it would’ve been 26 years of Canadian residence so 26/39 of the max OAS.

Now if i defer my OAS with one year let’s say do i get 7.2% increase for 12 month deferral and another 1/39 for one extra year of residence or is that considered double dip?

If so which one will apply?

I would appreciate if anybody can shed some light. Thanks

Hi Sermet, sorry I missed this comment. Your decision to delay will give you either the age deferral credit OR an extra year of residence (whichever is greater). No double-dip.

I realize this is an old article but I think the question is relevant. If you defer OAS til you are 70 you should receive 36% more. Is that 36% more than the amount you would have got at the age 65 or is it 36% more than the amount that is currently being given (to a 65 year old) when you are 70?

Hi Norm, it’s 36% more than the amount you would have received at 65 – plus the inflation-adjusted increases.

Thanks Robb!

So, in effect if I turned 70 today, and started to collect, I would get 36% more than what would be paid to a 65 year old that started to collect today. Is today’s rate not what it was five years ago “– plus the inflation-adjusted increases”?

Hi Norm, no that’s not right. If you turned 70 and started to collect today, you’d get 36% more than what you would have received at 65 – plus the annual inflation adjustments.

It looks like Norm is right unless there is an increase beyond the inflation adjustment which is not likely.

Would like to add a thought to those who beleive in taking CPP at 60 and investing it to come out ahead. By not taking it you have a garanteed 7.2% yearly return on your investment. So if you believe you can do better in the stock market over 10 years….

Great conversation thread. I’m a little late to the party, but I have a quick question. Hypothetical situation and question: My monthly benefit is the maximum for 2023 ($691.00), and I am eligible to take the OAS in January, 2023. If I delay my OAS to January, 2024, would my benefit be the $691.00 plus 7.2% (12 months of 0.6% increase) for a total of $740.75, or would it remain at the ‘maximum’ of $691.00?.

In other words, is the ‘maximum OAS’ stated on the CRA website actually the ‘maximum OAS when you turn 65’, and if you defer your OAS, the ‘maximum OAS’ would be increased by 0.6% for each month you defer the OAS?

Hi Robb,

Thanks for helping all of us!

I’m 63 and my wife is 68, my wife collects GIS and OAS. (Under GIS table 3)

I turn 65 in April 2025, would it be possible to delay My OAS until Jan 2026, then my wife would be able to still

Collect GIS for one more year for year 2026 ( under table 3 ) due to me not taking OAS that year.

Then in 2027, we would then fall under GIS table 2

Hope this make sense and you can offer some help in this matter.

Thank you,

Perry

If OAS is deferred to age 70, when one turn 75 is the extra 10 % received at that age calculated on the larger deferred OAS amount or the basic, smaller, OAS amount one would’ve received at 64?

My DOB is 9 March 1960. I became a resident of Canada in Feb 1993. Hence at 65 teas of age I will only have 32 years of residency in Canada and will only get 32/40 of the max benefit I believe. If I defer until age 70, do I get the benefit of a further 5 years of residency ? Am I able to make use of my residency in New Zealand until age 33 ?

Hi Robb,

Would Deferring OAS to age 70 also affect the 10% enhancement at age 75? ie: would you also get an additional 10% on the larger (deferred) amount vs. the base amount assuming you took it at age 65?

Hi Jen, yes – the 10% boost at 75 is in addition to the age-deferral credit. It’s a 10% boost to whatever your OAS income was the year previous.

The interesting thing about this is the way it interacts with the OAS clawback.

Someone who has too much RRIF income to receive any OAS at 65 could see a significant increase in their benefit if they defer claiming until age 70 and then get the 10% increase at 75. It could be better than claiming from 65 to 71.

That is very interesting for sure, thanks Robb!

Hi Robb, I will have lived in Canada for 25 years when I turn 65 so I will be eligible for a partial (25/40th’s) pension. Would deferring my OAS to age 70 give me another 5 years of eligibility i.e. an increase to 30/40th’s? Thanks.

Hi Andrew, you’d get the age-deferral credit (0.6% per month you defer past 65) OR the additional eligibility. Not both.

And the age-deferral credit is greater than increasing your years of eligibility.

For instance, 25/40 years gets you 62.5% of the OAS max pension (or $5,457.53 out of a possible $8,732.04).

Increasing your eligibility by one year gets you 26/40, or 65% of the OAS max pension (to $5,675.83).

But the age deferral credit increases your OAS pension by 7.2% per year (or to $5,850.47).

Thank you so much, it’s hard to find that information – even on the Government website! Do you know if it’s the same for CPP? I plan on working until age 70 and will still be contributing the maximum amount to CPP, so, presumably, those extra years will count – over and above the 42% increase because of the deferment.

Hi Andrew, my pleasure!

Ahh, I wish CPP was that straightforward. It’s not! Here’s a guide to CPP for those aged 65 and older and still working: https://retirehappy.ca/cpp-for-the-over-65-and-still-working/

The author is one of THE experts on CPP in Canada and he has a small business where for a nominal fee he’ll calculate your expected CPP benefit and help you make decisions about when to take your benefits.