The Retirement Risk Zone

I often recommend deferring CPP until age 70 to secure more lifetime income in retirement. It’s also possible to defer OAS to age 70 for a smaller, but still meaningful, increase in guaranteed income.

While the goal is to design a more secure retirement, there can be a psychological hurdle for retirees to overcome. That hurdle has to do with withdrawing (often significant) dollars from existing savings to fill the income gap while you wait for your government benefits to kick-in.

Indeed, the idea is still to meet your desired spending needs in retirement – a key objective, especially to new retirees.

This leads to what I call the retirement risk zone: The period of time between retirement and the uptake of delayed government benefits. Sometimes there’s even a delay between retirement and the uptake of a defined benefit pension.

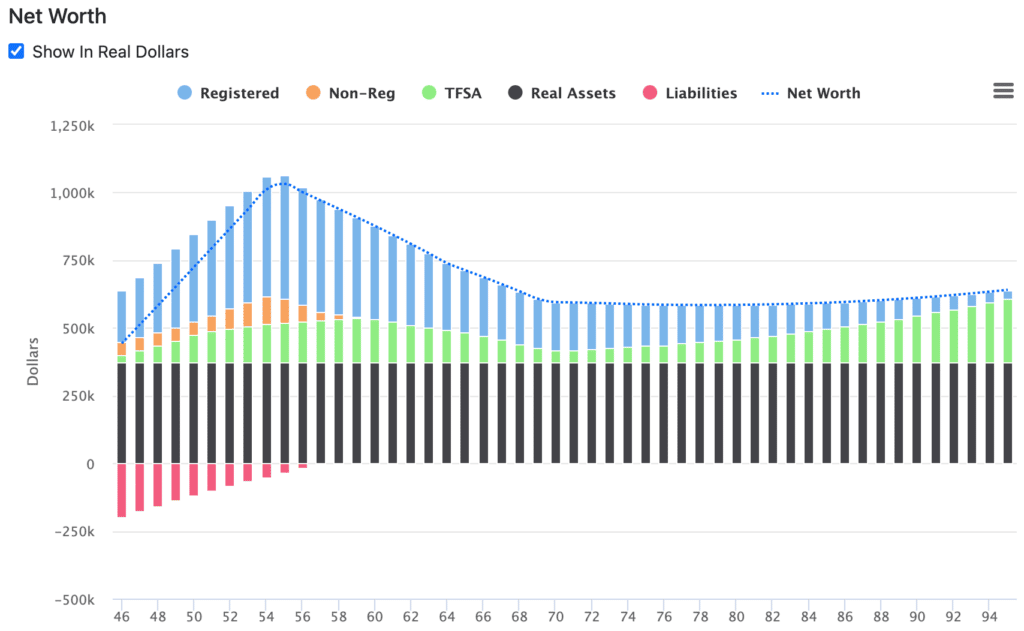

Retirement Risk Zone

The challenge for retirees is that even though a retirement plan that has them drawing heavily from existing RRSPs, non-registered savings, and potentially even their TFSAs, works out nicely on paper, it can be extremely difficult to start spending down their assets.

That makes sense, because one of the biggest fears that retirees face is the prospect of outliving their savings. And, even though delaying CPP and OAS helps mitigate that concern, spending down actual dollars in the bank still seems counterintuitive.

Consider an example of a recently divorced woman I’ll call Leslie, who earns a good salary of $120,000 per year and spends modestly at about $62,000 per year after taxes (including her mortgage payments). She wants to retire in nine years, at age 55.

Leslie left a 20-year career in the public sector to work for a financial services company. She chose to stay in her defined benefit pension plan, which will pay her $24,000 per year starting at age 65. The new job has a defined contribution plan to which she contributes 2.5% of her salary and her employer matches that amount.

Leslie then maxes out her personal RRSP and her TFSA. She owns her home and pays an extra $5,000 per month towards her mortgage with the goal of paying it off three years after she retires.

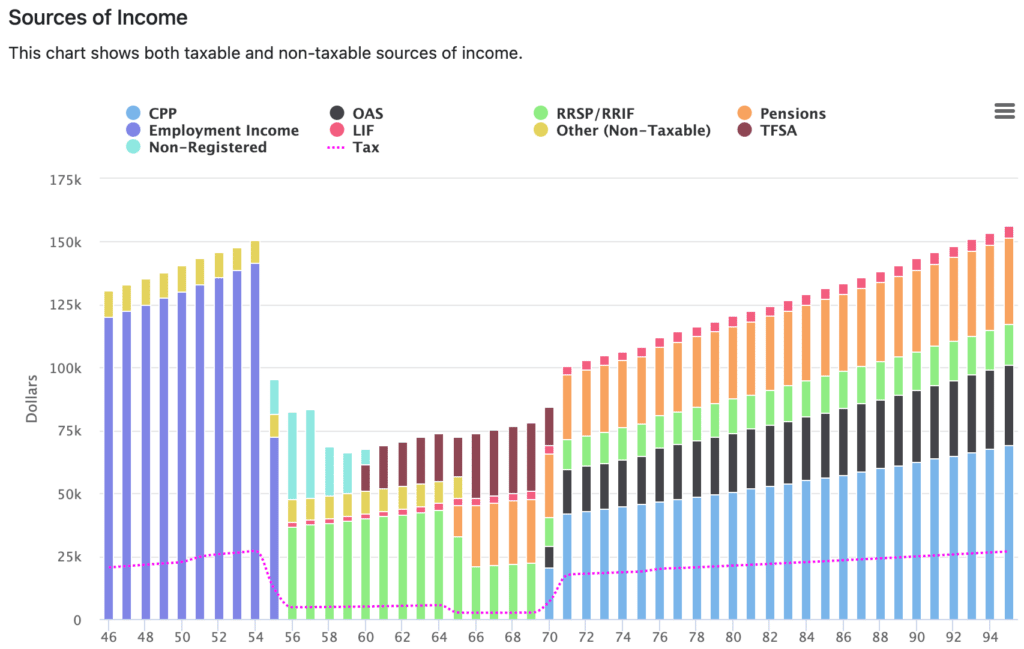

Because of her impressive ability to save, Leslie will be able to reach her goal of retiring at 55. But she’ll then enter the “retirement risk zone” from age 55 to 65, while she waits for her defined benefit pension to kick-in, and still be in that zone from 65 to 70 while she waits to apply for her CPP and OAS benefits.

The result is a rapid reduction in her assets and net worth from age 55 to 70:

Leslie starts drawing immediately from her RRSP at age 56, at a rate of about 7.5% of the balance. She turns the defined contribution plan into a LIRA and then a LIF, and starts drawing the required minimum amount. Finally, she tops-up her spending from the non-registered savings that she built up in her final working years.

When the non-registered savings has been exhausted at age 60, Leslie turns to her TFSA to replace that income. She’ll take that balance down from $216,000 to about $70,000 by age 70.

Now, we know that withdrawing 7.5% of a portfolio is not sustainable over the long term. But Leslie has a magic trick up her sleeve. She can cut her RRSP withdrawals in half at age 65 when her defined benefit pension kicks in. By age 70, when CPP and OAS benefits begin, Leslie can start drawing the minimum amount required from a RRIF (5%).

Even with the reduction in RRSP/RRIF withdrawals, Leslie’s income from her pension and government benefits is now high enough to stop making withdrawals from her TFSA, and in fact start contributing to the tax-free account again.

This makes for a nice tax-free estate for Leslie’s only child, but also gives her a pot of money for any planned or unplanned expenses or spending shocks that may occur throughout retirement.

Finally, of note, once Leslie’s mortgage is paid off at age 58 she increases her after-tax spending by $5,000 to enhance her retirement spending. Her after-tax spending budget increases by 2.1% per year to keep pace with inflation over the long term.

Final Thoughts

While this is one unique example of the retirement risk zone, I see similar scenarios play out all the time for clients who retire between 55 and 65 and have a delay in taking their pension and/or government benefits.

It’s not even unique to those deferring CPP and/or OAS to 70. The retirement risk zone can happen anytime between retirement and the traditional uptake of government benefits.

Early retirees want to maximize their ability to spend and may also have one-time expenses like a new vehicle, home renovations, a bucket list trip, or financial support to their young adult children.

Related: Your Retirement Readiness Checklist

For these reasons it can be difficult, psychologically, to defer taking your pension and/or government benefits (even though it makes the most mathematical sense) while spending down existing savings.

That’s why it’s helpful to see the big picture with a retirement plan that shows how all of these different income puzzle pieces fit together over the long term.

The retirement risk zone can seem extremely risky until you see the pension and/or government benefit dollars kick-in and raise your income floor by a substantial amount.

So, while it’s tempting to take your pension and benefits early to ease the anxiety you face during this retirement risk zone period, know that by doing this you’ll actually be losing income in your later retirement years.

Instead, consider taking on some part-time work, or delaying your retirement by 6-12 months, or spacing out some of your planned one-time expenses (or easing asset depletion concerns by financing a large purchase over a few years), to help bridge the gap.

Better yet, as I say to my clients, it’s helpful to wrap your head around the idea of transferring risk from the market to the government and/or your company pension plan – trading your own riskier investments for a guaranteed, paid for life, indexed to inflation source of income.

The goal all along, even during the retirement risk zone period, is to generate enough income to meet your spending needs in retirement.

Take comfort knowing that by the time your CPP and OAS kicks in at age 70, you’ll often end up with more income than you need to meet your desired spending in retirement. Tuck that extra income away in your TFSA to create a tax-free estate, a source of funds for large planned one-time expenses, or as a safeguard against unplanned spending shocks.

Great article! Retirement is all I think about.. 1 more year. Thank heavens for a defined benefit pension at age 56.

Hi Liliane, thanks for the kind words and good luck in your retirement journey.

Hi Robb,

More good info, thank you! You guys get all the goodies: do you know of any software packages – specifically for decumulation in retirement – available to non-CFP types to do these sorts of calculations/plans?

Cheers,

Another David.

I very much like delaying both QPP and OAS until 70 and drawing down RRSP and non-registered assets in a tax efficient way.

Hi Jean-Claude, it makes a ton of sense if you have the savings to support the retirement risk zone years and can get over the psychology of drawing down those savings while you wait.

Hi Robb,

Nice write up…

Would it be possible to show what happens if she instead took CPP and OAS at 65 instead of what you have shown? I’m guessing there is a break even point which is what a lot of people would benefit from seeing, especially if there is a history of early mortality in the family.

Thanks for your informative article as always!

David

Hi David, thanks! It’s tricky because you’re asking for three scenarios. One in which Leslie takes CPP and OAS at 65 and live to 95, another in which Leslie takes CPP and OAS at 65 and lives to, say, 85, and another in which she defers CPP and OAS to 70 and lives to 85.

As a planner I want to make sure you have enough money to last for a long life. FP Canada would like planners to use the 25% chance that you’ll live until a certain age. Using actuarial tables, if you’ve already reached age 60 there’s a 25% chance you’ll live until age 95.

Of course, if you have good reason to believe your life expectancy will be lower due to health or genetics then we would adjust the life expectancy in your plan and that would change decisions on when to take CPP and OAS.

You state with regard to a TFSA, “…to create a tax-free estate,…”

I was under the belief that it is a tax free transfer when transferred to the surviving spouse, however when passed on after the surviving spouse’s death, there are tax implications.

Or is this where the surviving spouse (or in the case above, she is a single parent) designates a child as the beneficiary. Thereby a tax free transfer?

Hi Jeff, I assume the TFSA will become part of the estate (tax free), which will then pass to the beneficiary.

You can only name your spouse or partner a successor holder.

Jeff – I think that you are confusing the tax treatment of TFSA and RRSP/RRIF. As there was no deduction for the amount deposited in the TFSA, there is no tax payable on the withdrawal or when it is collapsed. The only tax implication is that if the TFSA is being collapsed (because it is not passing to the spouse as a successor annuitant), the income earned from the date of death until the TFSA is distributed to the beneficiaries is taxable to the beneficiaries.

Maureen, I understand there are TAX differences between RRSP/RRIF and TFSA. What I was trying to say, apparently not clearly, was with respect to tax implications of an “estate” not going to a spouse. There may not be a tax free estate. So you are correct as with respect to a spouse – which should be successor annuitant – versus say a child, who is most likely deemed only as a beneficiary. The “estate” to a spouse (successor) is rolled over tax free, but the “estate” to say a child is not necessarily.

I may still be wrong, but I think we are basically agreeing on the tax implications.

For reference I found this article by Jamie Golobek:

https://www.cibc.com/content/dam/personal_banking/advice_centre/tax-savings/tfsa-holder-dies-en.pdf

Jeff – I think that Robb’s comment about a “tax-free estate” was solely with respect to the TFSA. If there are non-registered assets at death, and they are not being passed to a spouse, there is a deemed disposition and potentially capital gains tax. There can also be probate tax. Note that you can name anyone as a beneficiary of a TFSA and if you do, then it will pass outside of your estate and avoid probate taxes (which can add up if you are in provinces with higher probate fees like Ontario or BC). So the balance in the TFSA at death will pass “tax-free” to the beneficiaries.

Thanks Maureen. From your first post that proceeds (FMV at death) from the TFSA pass tax free. I think I read that any increase from FMV after death maybe taxed.

So if I understand it now, if a widower parent dies and has designated his daughter as a beneficiary, then the FMV at his death of the TFSA passes tax free to the daughter. If there is any increase it may be subject to taxes unless she has some unused TFSA room… maybe I understand it better.

Just for some further clarity Jeff, when a spouse passes their TFSA transfers to the surviving spouse’s TFSA and there is no taxable event. This is true no matter what happens between the death of the spouse and the actual time of the transfer (i.e. if the value of the TFSA increases it doesn’t matter).

However, when the remaining spouse passes the *proceeds* of the TFSA will pass to the beneficiary tax free – but the proceeds will be removed from a TFSA account first.

This money passes tax free, but it can only end up in the beneficiary’s TFSA if they have the room available. But basically, the beneficiary gets a cheque and they do what they want with that cheque. It does not increase their TFSA room, or affect the beneficiary’s TFSA room in any way.

The “taxable” event will occur if, between the time of the TFSA account holder’s passing, and the time that cheque gets cut there is an increase in the value of the TFSA, that increase in value is treated as a capital gain and must be paid by the estate of the deceased. If the value is constant, or drops, there is no taxable event. (I’m not sure if there’s a loss, if it can be used as a capital loss).

As an example, when my mother passed, her TFSA was automatically transferred into my father’s TFSA. Three months later he passed, and the TFSA was emptied, and cheques were cut for my sister and I and we received that money tax free. In our case the TFSA dropped a little bit in value so there was to capital gains to deal with.

When someone dies with a TFSA, the spouse can only take over the deceased spouse’s TFSA if they were designated as the “successor annuitant”. If they were not (and I have seen this happen), then there is an opportunity for the spouse to make a “qualifying contribution” to their TFSA (even if they don’t have room) of the value of the TFSA as of the date of death. When there is no spouse, the beneficiaries will be taxed on any increase in the value of the TFSA from the date of death to the date of distribution – but it is taxed as regular income and reported on a T4A slip – it is not treated as a capital gain. And it is irrelevant whether the beneficiaries have TFSA room – the increase will be taxed regardless. If there were no beneficiaries named, then the TFSA passes to the estate and the estate will be taxed on the increase.

I couldn’t figure out how to reply to Maureen’s update to my comment – but she is correct. Also, in my reply I assumed the spouses set each other up as successor-holder to permit the TFSA account to flow as I described.

Why do all these scenarios seem to include DB plans – that just isn’t the norm…what if there is NO DB plan? How much would one need to convert to an annuity that would in fact give a person a DB plan of their own – not a company one? This would be a great write up to consider – hope to read it soon! Thanks.

Hi Gail, 4.5 million Canadians are covered by a defined benefit pension plan.

Let’s assume there’s no DB plan. All the more reason to defer CPP and OAS to secure more guaranteed lifetime income. And, we’d assume, a larger pot of savings in RRSPs and non-registered accounts for private sector workers.

Annuities won’t typically make sense until age 70-75, so not relevant for this discussion on the retirement risk zone between age 55-70.

Question related to your response above. If a DB pension has been wound up and options are presented for A) company purchased annuity for your pension value or B) a locked in retirement account or C) take commuted value and buy your own annuity…what are the “gotcha’s” to consider? I’m not ready to retire yet but have to decide. You stated above that annuities don’t make sense till your 70s but option A above would protect my benefit as if it were a pension. Just trying to figure out how to figure it out!!

Great article with lots to consider. I was always under the impression that deferring CPP but not contributing (between 60&65) would negatively affect your pension and that if you weren’t contributing there was no reason not to take it.

Hi Donna, thanks! CPP expert Doug Runchey says you’ll always get more CPP by waiting. That’s because the age deferral credit is greater than the penalty for another “zero contribution” year.

Donna, my wife and I stopped contributing/retired before age 60, plus we didn’t start work in Canada until we were in our mid-30s, so we’re really down on contribution years, and yet, our CPP will be higher for each year that we delay! However, the increases between years are less than someone who has no years missing prior to reaching age 60. Lookup something called ‘dropout provisions’ and see if that helps address your concern – I’m sure Robb will have something on his blog about this.

Great post, Robb! It’s too bad that so many people are so resistant to these ideas.

Thanks, Michael! It is helpful to show clients the benefits through big picture charts like these, and to emphasize that they can maintain their desired spending in that retirement risk zone.

I recently looked closely at how our plan would go in the event I or my wife died. In our case, whoever is the survivor, they will be okay, but the reduction in CPP (survivor’s benefit) was a little disheartening and more than expected due to a cap in the somewhat complex formula. If we were, and I’m not saying we will, to start drawing early, we would capture the full CPP amounts up to the point one of us dies, and then perhaps not even hit the survivor benefit caps. Just another fly in the ointment, perhaps!

I am six years older than my wife.

I started receiving both CPP and OAS at age 70.

My wife is deferring both CPP and OAS until she is 70.

My income is just before the OAS clawback. and the same will be true for my wife.

Once one of us dies, 100% of the OAS will be clawed back for the survivor.

How long do both of us have to live for the benefits of delaying OAS for my wife makes sense?

Thanks.

Martin

You’ll also lose 100% of your wife’s OAS and at least 40% of her CPP, and perhaps even as much as 100% of her CPP!

For me, these perspectives do not encourage me to take CPP early. If one of us dies the income requirements drop significantly. Travel, food, cars, just to name a few things, all get reduced.

I can’t avoid a plan that assumes we both live to 90 and ensuring the utmost stability in such a plan. In the absence of any concrete proof there is a significant mortality risk for either of us I will continue to plan to defer CPP.

I can come with lots of scenarios where we benefit from the higher CPP and lots of risks if we take CPP earlier than 70.

Great article, I have a question if you do not need the government pension at 65 to cover daily expenses would it not make sense to take the money and invest it instead of waiting until 70?

Hi Anja, the challenge is that you’ll get a guaranteed 8.4% per year more (plus inflation adjustments) for delaying CPP. Do that over five years and it’s a 42% increase to your CPP benefits (which works out to about 50% when you factor in inflation adjustments). So how do you invest and beat that guaranteed return?

And it’s even more difficult to beat a net 8.4% annual return after the investment income is taxed.

I find the whole “break even” discussion to be so mundane. I worry about how I fund retirement to age 90 or beyond, not whether I’m going to “break even” by age 84, etc.

I think the only thing worse than planning to take CPP at age 70 and dying at age 69 is taking CPP at age 60 and living on a pittance at age 90.

My mantra will always be if I NEED CPP before 70 because I was unable to save suitably for retirement then I’ll take it, but I’m going to do everything in my power to transfer that risk to CPP by taking it at age 70. I might take OAS before 70, that’ll depend mostly on if I’ve had a poor sequence of returns from age 60-65.

Well said, James. I used to think in terms of break-even age, but eventually came around to its irrelevance.

So have a scenario where both my spouse and I are two time cancer survivors, so far! To me if just doesn’t seem to make sense to delay taking CPP, as there is no guarantee of a tomorrow.

Both of us are now early retirees and are both taking our CPP, we are not yet eligible for OAS.

I think my health concerns would be as vital as evaluating how much I was able to save.

My parents both died of cancer, my mom, a smoker from age 17 to age 44, had a radical hysterectomy around age 62 as well as several incidents of melanoma. My dad also had melanoma earlier in life and got gall bladder cancer, passing within 18 months as it was caught very late (it burst and it was only discovered then). But, both my parents made it to age 89.

If I were to be stricken with cancer, or another life shortening illness before age 70, I would no doubt revaluate my stance on waiting to age 70, but based on both my parents longevity, even with cancer, and the fact that I’m relatively confident I can support a fruitful retirement from age 60-70 (I’m 55) I am still inclined to hold off.

Everyone needs to do their own assessment including modelling retirement budgets and income streams but I will always lean towards a plan that works to at least age 90. My parents required significant care towards the end and their resources were strained to support their needs. I am reluctant to put that burden on my children. Having a higher CPP and maybe OAS is one approach to mitigating that possibility.

Thanks for the thoughtful post! What software do you use to do your modelling? Can it handle Monte Carlo simulations? Is it available to non-planners? I appreciate the insights 🙂

Hi Chantal, thanks! I use Snap Projections to model projections for my clients. You can use it to stress test plans based on historical and randomized scenarios.

It’s not meant for non-planners to use (too expensive and you’d need the right knowledge and skills to ensure your inputs and variables are entered correctly).

Interesting read. Wouldn’t the OAS be entirely clawed back based on the total retirement income shown?

Hi Bob, good observation but remember that Leslie’s age 70 year is 23 years away. The income you’re seeing is in future (inflation adjusted) dollars. The OAS clawback threshold is also indexed.

The threshold starts at $79,845 from July 2022 to June 2023, and will increase to $81,761 from July 2023 to June 2024.

In 20 years, the threshold is likely to start at $100k or more.

Finally, while singles may need to carefully manage their retirement income to avoid OAS clawbacks, couples have the advantage of being able to split eligible pension income (from RRIFs or defined benefit pensions), which makes it easier to stay under the OAS clawback threshold.

I see you have her taking TSFA income from 60-70, yet she still has RIF available and is paying low income tax. Wouldn’t it make more sense from both an income tax smoothing and non taxable estate to defer TFSA withdrawals until the RIF is depleted?

I’m 70, I retired at 50 (had to!), no company pension plan either. CPP is calculated according to your “best” paid income years. I had no income after 50, meaning that if I had deferred CPP to 70 years, I would have lost too much. (Average income would have gotten lower with every passing years.) That’s why I took CPP at 60 years old. And never regretted it because I had no choice!

Can Canadians really start withdrawing from an RRSP as early as 56? I thought it was 59.5 or is that outdated or incorrect info?

For clarity, you can withdraw from your RRSP at any time. Withdrawn funds will incur withholding tax, which may or may not cover the entire tax liability.

Perhaps you were asking if there is a minimum age to convert your RRSP to a RIF? There is no longer a minimum age. Converting to a RIF enables one to withdraw the minimum amount without any withholding tax. But, there are lots of considerations to determine when to convert to a RRIF and how much to convert ( it is possible to move some, and not all, of one’s RRSP to a RRIF).

Hi James (and MJ), the 59.5 year rule is from the US (for 401k plans, and others). It has never applied to RRSPs.

Love the article. I’m in the retirement risk zone. What I find is missing from a lot of these analysis is the big $ spend outside of the usual budget items. The anaylsis looks at the income requirements but doesn’t take into account things that require either bigger lump sum payments or taking out new loans. Given that we’re talking about this person living off existing savings from age 55 to 70 (with a defined pension kicking in at age 65 that many of us won’t get), that’s 15 yrs. How do the models handle things like: a) purchase of 1 or more vehicles during the 15 yrs, b) major house expenses (roof replacement, renos, appliance replacements), etc. Banks don’t like to loan out money for people with only investment income. I ran into this when I suddenly had to replace a vehicle when it unexpectedly died. I had lots of assets but low income. Ended up selling investments to purchase the vehicle. Still holding off on CPP but I’ve started OAS. I think a lot of people have these larger $ purchases and end up starting CPP & OAS earlier than 70.

Thanks for the article and all its insights.

Our plan includes never touching TFSAs and also making the yearly contributions for both my wife and I. We expect to retire in 4 years. I’ll be 60. If we have unplanned expenses we will draw down the TFSAs so that those expenses don’t also hit us with a tax bill. We might be able to top them back up again, but if not, that’s okay – end goal is for them to be our estate (plus our home, if we still own one at the end).

Hi Brian, thanks for your comment and sharing your experience as someone squarely in the retirement risk zone.

I did mention:

“Early retirees want to maximize their ability to spend and may also have one-time expenses like a new vehicle, home renovations, a bucket list trip, or financial support to their young adult children.”

It’s a big reason why this period of time can be so risky (or why it feels risky). My example case study may have had to completely exhaust TFSA and non-registered sources due to those one-time expenses, which may not have felt good and may have tempted her to take CPP and/or OAS earlier than anticipated. Happens all the time.