I recently made a bold change to de-risk my portfolio, which now consists of just 35% globally equities and 65% short-term bonds.

This wasn’t in response to tariffs and global trade wars, or my gut feeling about stock markets crashing in the near term.

No, this was a predetermined change in a specific account type to more appropriately align the investments with the expected time horizon of withdrawals.

I’m talking, of course, about our kids’ RESP portfolio!

(I’m still 100% invested in VEQT in my RRSP, LIRA, TFSA, and corporate account – in case you’re wondering how I invest my money).

An RESP is the most difficult account for investors to manage. First of all, the time horizon for contributions and growth is relatively short (17-24 years, in most cases). Second, the withdrawal period is *really* short (typically 4-6 years). And third, you actually *want* to run out of money at the end – meaning you’ve withdrawn all of the funds for your kids’ post-secondary expenses.

Imagine the lifetime of your RRSP being condensed to making contributions between the ages of, say, 43 to 60, and then withdrawing all of the funds from ages 61-65 – intentionally exhausting the account (or risk incurring a tax hit or leaving the funds trapped and unspent).

That’s what it means for parents who are managing RESP funds for their child(ren).

In my experience working with clients and hearing from readers, most parents do not hold an appropriate asset mix in their RESP accounts. Either their investments are too risky (like me, having far too much equity exposure for far too long), or their investments are dreadfully conservative and held predominantly in bank deposits, GICs, and monthly income mutual funds.

Worst of all, there is no strategic thought to shifting this asset mix over time – particularly as their children get into their high school years and beyond.

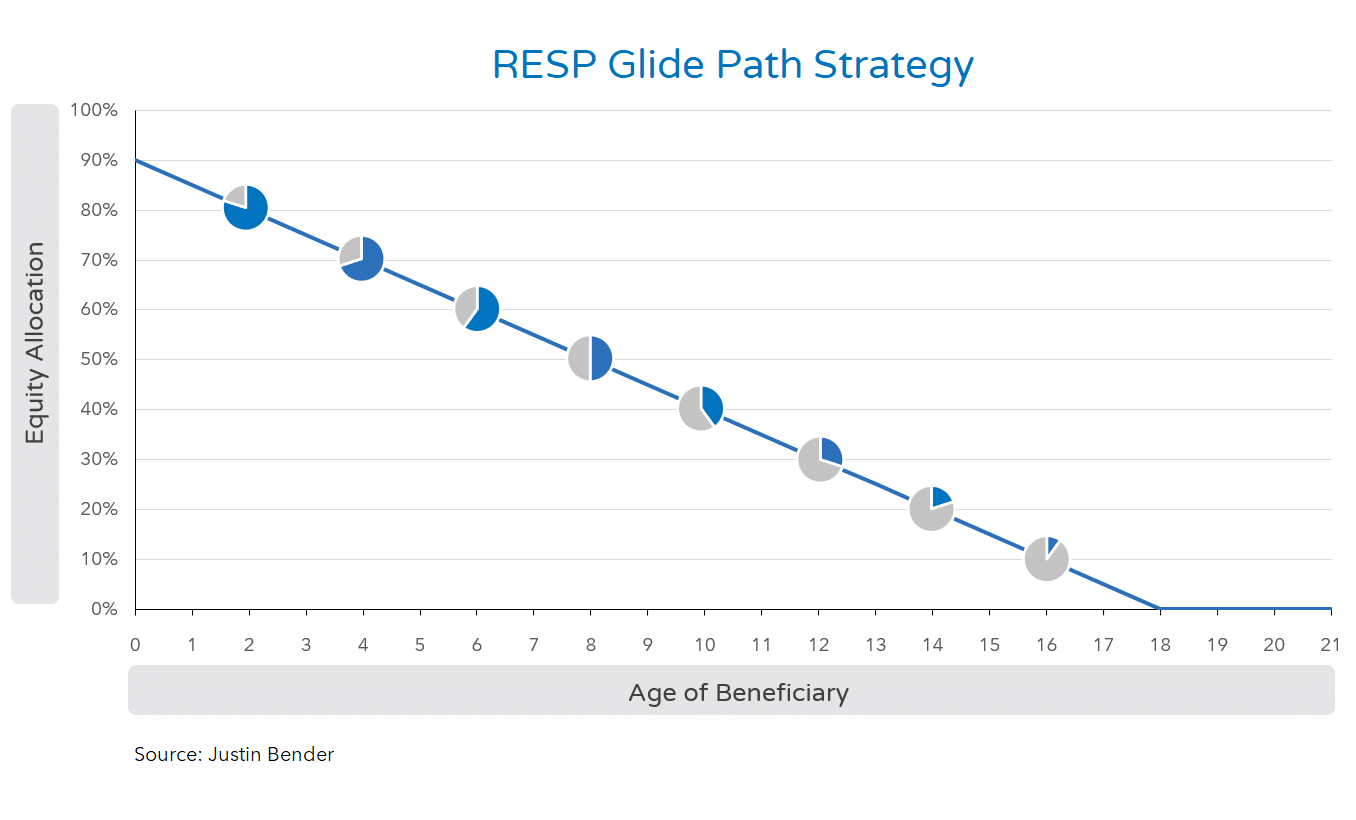

For all of these reasons, I highly recommend following the incredibly useful approach developed by PWL Capital’s Justin Bender for self-directed RESP investors.

The key to managing your RESP portfolio is to have a predetermined glidepath – a rebalancing schedule that you can blindly follow during the contribution and withdrawal years.

In this plan, Justin recommends starting with a portfolio of 90% equities and 10% bonds. Each year you gradually decrease the equity exposure by 5% so that by age 17 you have just 5% in equity and 95% in bonds. At age 18, presumably your child’s first year of post-secondary and of RESP withdrawals, shift the portfolio again to include an allocation to cash or money market funds (25% at 18, 33% at 19, 50% at 20, and 100% at 21).

During the contribution phase, make life easier on yourself and this rebalancing strategy by contributing the entire amount at once in January ($2,500 per child) and adjusting your asset mix for the year at that time.

In a family RESP with multiple children, Justin’s comprehensive article suggests the same approach, but splitting each child’s share of the RESP into different (but similar) ETFs to help parents keep track of each child’s glidepath and share as they age.

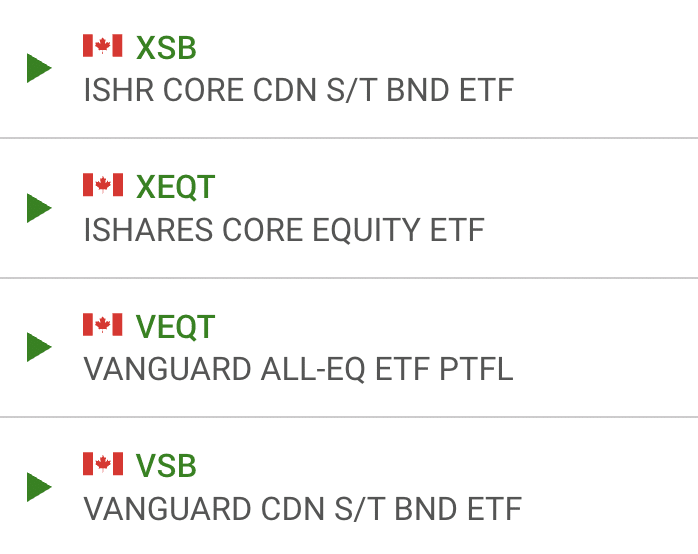

For instance, our oldest daughter is in her age 16 year and her share of the RESP account has 25% global equity in VEQT and 75% short-term bonds in VSB (Vanguard).

Our youngest daughter is in her age 13 year and her share of the RESP account has 40% global equity in XEQT and 60% short-term bonds in XSB (iShares).

Finally, follow the rules but feel free to make the strategy your own. For example, you may have noticed that I’m not following the exact recommended age glidepath from Justin’s article, but instead chose the asset mix for a 10 and 13 year old (rather than for a 13 and 16 year old).

I’ll start shifting a portion of the account to cash in two years to help queue-up the first semester’s withdrawal needs for our oldest daughter.

Final Thoughts

RESPs can be a really challenging account type for investors to manage, especially on their own. It’s not as intuitive as, say, your retirement accounts where young parents might be perfectly comfortable investing in 80-100% equities, knowing that their time horizon is long and they want to maximize growth during their working years, but also into and throughout retirement.

To a risk-seeking investor it just doesn’t seem right to hold a 60/40 portfolio for their child who is under the age of 10.

And in your child’s high-school years, reality still might not have set in that they will be withdrawing from this portfolio in the near future. Pair that lack of awareness with a rising stock market and it certainly won’t feel good to take risk off the table and move to short-term bonds and cash. You want to squeeze every drop of return from the market before that happens.

The problem is, as we’ve seen earlier this year, markets can turn negative in a hurry and you could suddenly be faced with a 10-20-30% drop in value at the worst possible time.

In my mind, the RESP is all about maximizing the matching government grants (20% free money!) rather than trying to hit a home run with your investments. Because of the challenging time horizons of your contribution and withdrawal phase, I’d rather err on the side of being a bit too conservative so that I can avoid or minimize regret.

Remember, the phenomenon of loss aversion states that we feel the pain of a loss twice as much as we’d derive pleasure from an equivalent gain.

For years I’ve wrestled with the taxing decision of whether to pay ourselves dividends or salary (or some combination of the two). For background, my wife and I co-own and operate our corporation, which includes our financial planning business, this blog, and some freelance writing work.

We’ve always paid ourselves an equal amount of dividends from the corporation to fund our personal spending and saving needs. It was easy (no payroll), it kept our personal tax rate fairly low and predictable (dividends are taxed at a lower rate than salary), and we just invested whatever was leftover inside our corporate investment account.

But as our business has grown in revenue and our corporate investment account balance swelled, it was clear that a change might be needed to avoid potential tax traps in the future.

First, any income earned up to the small business deduction limit is taxed at a friendly 11%, but income earned above that limit jumps to 23%. That wasn’t an issue for many years, but it’s going to be this year and into the foreseeable future.

Second, if a corporation earns more than $50,000 in passive income (say, from VEQT distributions), the small business deduction limit is reduced by $5 for every dollar of passive income above that threshold.

That’s not an issue right now with a corporate investing balance of $500,000 earning perhaps $10,000 of passive income. But if we continue aggressively adding to our corporate investments for another 5-10 years this could easily spell trouble with a portfolio of $2M or more.

The problem with dividends is that, while easy and less taxing personally, they’re not deductible from our corporate income so we’ll end up paying more corporate tax (especially once revenue exceeds the small business deduction limit).

Salary is deducted from corporate income and, while taxed higher personally, also creates RRSP contribution room and allows us to pay into CPP.

Speaking of RRSP room, one more reason I’ve hesitated to switch to salary is that both of our RRSPs are fully maxed out. Paying salary creates RRSP room – but not until the next tax year.

So what did we decide? Starting May 1st we’ll each pay ourselves a salary of $9,000 per month ($72k for this year) and have set up the appropriate payroll deductions for taxes and CPP contributions. We’ll also continue to distribute dividends that will top-up our income to meet our personal spending and saving needs.

The $144,000 in salary can be deducted from our corporate income to keep our corporate taxes low. We’ll pay ourselves enough to keep up with our TFSA snowball approach (catching up on unused room over the next few years), and the trade-off for this change will be fewer dollars contributed to our corporate investments.

We’ll each generate $12,960 in RRSP contribution room for 2026, and that will give us more flexibility to increase our salary and resume RRSP contributions for the first time in six years.

I’m happy with this new mix of salary and dividends as it relates to our overall financial plan and goals.

I’m also grateful to Ben Felix and Dr. Mark Soth for creating the incredibly valuable Money Scope podcast for Canadian business owners, as well as to my friend Aravind Sithamparapillai for helping me think through this taxing decision.

This Week’s Recap:

Markets rallied this week with global equities surging ahead by 6%. I’m sure that was a welcome reprieve for investors who undoubtedly were shaken after their portfolios fell sharply the week prior.

It’s yet another reminder that stock returns are random and unpredictable, and the best advice is to stay the course with a sensible low cost, globally diversified portfolio.

I said as much in my last edition of Weekend Reading – is “stay the course” helpful advice?

Promo of the Week:

This week I’m highlighting an often forgotten rewards credit card pair, the Marriott Bonvoy American Express Card and the Marriott Bonvoy Business American Express Card.

These cards have been staples in our wallets for many years. Why?

Unlike most rewards credit cards, which I will happily churn (apply, collect the welcome bonus, and then cancel before the card anniversary and annual fee kick-in), the Bonvoy American Express Cards come with an annual free night certificate with a room redemption rate worth up to 35,000 points.

The personal Bonvoy card comes with an annual fee of $120, but the free night redemption alone can easily be worth $350 depending on when and where you redeem it.

The business Bonvoy card comes with an annual fee of $150, but again the free night certificate more than offsets the fee.

That’s not all. New applicants can sign-up for the Marriott Bonvoy American Express card and earn 55,000 points after charging $3,000 to their card in the first three months.

New applicants for the Marriott Bonvoy Business American Express Card can earn 60,000 points after charging $5,000 to their card in the first three months.

As mentioned, my wife and I each have a personal AND a business card (as the primary holders, none of this supplementary card nonsense), and so we each get two free night certificates to use at Marriott’s worldwide.

These come in handy when booking travel. For instance, if we have an early flight departing from Calgary we’ll use a free night certificate to stay at the in-terminal Marriott the night before and then just roll our bags out the door to international departures the next morning.

We’ll also use a free night this summer in Glasgow, where we’re staying overnight and then taking a train to London before our return flight home.

We’ve also used free night certificates for a weekend away in Calgary or Vancouver.

It’s not often a rewards credit card carries value from year-to-year once the welcome bonus disappears, but with these two Bonvoy American Express cards you can easily extract value from the annual free night certificates. They’re worth a look!

Weekend Reading:

Steadyhand’s Tom Bradley echoes my sentiments exactly by saying the best advice for investors right now is to do nothing. Really.

The late Peter Bernstein said it best: “In calmer moments, investors recognize their inability to know what the future holds. In moments of extreme panic or enthusiasm, however, they become remarkably bold in their predictions.”

Heather Boneparth shares an excellent piece – how does your partner cope when the sky is falling?

Many Canadians are confused about how capital gains work. Jason Heath explains how to reduce capital gains with RRSP contributions (a good reminder to those who plan to sell rental properties in the future).

Mark McGrath and David Chilton looked at the TFSA vs. RRSP debate with an insightful 15 minute discussion:

Why market volatility feels different this time – but it probably isn’t.

Finally, one interesting development taking shape since the U.S. launched a global trade war is the soaring loonie – which has now climbed above 72 cents USD. Unfortunately for our travel plans, the loonie is not holding up that well against the Euro or Pound sterling.

Have a great weekend, everyone!

Global stocks fell sharply on Thursday and Friday after US President Donald Trump’s so-called Liberation Day tariffs went into effect.

Whether the President is being deliberately obtuse about the economic upheaval these tariffs will cause, or if he’s playing chess while the rest of the world is playing checkers is anyone’s guess.

What investors want to know is whether they should do something with their own portfolios.

Once again I find my inbox and DMs flooded with messages from anxious investors:

“I am a bit confused and concerned with the US tariffs if it is still a good plan to leave the money in those ETFs (VGRO/VBAL) long-term? I just wanted to check in with you in case a change of plans might be advisable?”

and:

“Hi Robb, hope all is well amidst this madness! Any ETF tweaking needed?”

and:

“Robb, my investments are plummeting. Should I do something about this, and if so, what?”

Interestingly, a few brave investors wondered about buying the dip:

“Would this be a good time to buy some ETF’s at low prices for my non-registered account?”

and:

“With the recent market declines, do you think it makes sense to take $20-$25k from my emergency fund, put in the market now and pay myself (emergency fund) back over the next few months?”

I probably sound like a broken record when I say you shouldn’t change your investment strategy based on current market conditions (tempering those greedy or fearful emotions).

Telling my clients to stay the course while my own portfolio fell $60,000 in one day

— Robb Engen (@boomerandecho.bsky.social) 4 April 2025 at 07:13

Yes, it sucks to see your investments fall by 10% in two days. It’s tempting to do something, anything, to stop the bleeding and get to safety.

Yet we also know that while markets don’t go up in a straight line, their general trajectory is up-and-to-the-right over time. Staying invested in a properly diversified portfolio ensures that you capture those good long-term returns.

The alternative is jumping in and out of the market every time we’re faced with a scary headline. Indeed, there’s always going to be a reason to sell:

So, while “stay the course” is the correct advice, it can also seem maddeningly unhelpful. What do you mean, do nothing? Surely there’s something to do besides standing there and getting punched in the face?

First, we need to remind ourselves that our investment plan does not (or should not) expect positive double-digit returns every year. Stocks are risky if your timeframe is one day, one week, one month, one year, or even 3-5 years.

Also remind yourself that market returns in 2023 and 2024 were extraordinary. When prices are high today, we should expect future returns to be lower (and vice-versa).

If you were happy with your global equity portfolio value on August 12, 2024 – well, that’s exactly where we are today.

Finally, if you don’t know your risk tolerance, this is how you find out. Can you steel your nerves through a period of market declines? Or are you perhaps holding more equity exposure than you can stomach?

Want to hear how two of the best advisors in the business are communicating with their clients to keep them from panicking and making poor financial decisions amidst this market volatility? Listen to this excellent conversation between Michael Kitces and Carl Richards.

In the meantime, repeat after me:

I am an emotionless robot when it comes to investing.

I have a well diversified investment plan.

I will not change that plan based on current market conditions.

I will keep investing regularly according to my plan.

I’m going to put down my phone now and move on with my life.

This Week’s Recap:

My last weekend reading update reminded us why we diversify.

We filed our personal tax returns for 2024 and ended up with a refund of 20 cents. Now that’s tax optimization!

We are less than two weeks away from a trip to Italy over the Easter break. Last year I found a terrific deal on a business class flight from Calgary to Frankfurt to Florence for April 2025 so we’ve been looking forward to this trip for a while.

We’re staying in Florence for the long weekend and then taking a train to Cortona, picking up a rental car, and driving to a Tuscan villa to stay for a week. Fingers crossed for good weather, as there is an outdoor (heated) pool and a lovely patio area to relax and enjoy the Tuscan views.

We had an unfortunate change of plans for the return journey. We initially planned to return via the same route that got us there (Florence to Frankfurt to Calgary) but about a month ago we received a change notification that the Florence to Frankfurt flight got removed from the schedule.

So now we’re returning our rental car and taking the train south to Rome, staying one extra night, and flying home directly from Rome to Calgary. Not the end of the world to spend a night in the Eternal City.

Weekend Reading:

Introducing the Time of Your Life app – a calculator that will help you visualize how you will spend the rest of your life.

The 2025 paper Beyond the Status Quo: A Critical Assessment of Lifecycle Investment Advice suggests that investors should hold globally diversified 100% stock portfolios for their entire lives. It has been met with intense criticism:

I’ve also written about this a few months ago in my VEQT and Chill weekend reading update.

Millionaire Teacher Andrew Hallam answers the question, should you take higher risks if you are late to investing?

“People starting late are at greatest risk of chasing past performance. They want to make up ground. But instead, they should diversify with global stocks and bonds. You never know what market is going to end up winning, so it’s best to own them all.”

A Wealth of Common Sense blogger Ben Carlson shares a short history of tariffs.

Using something called “effective number of stocks”, PWL Capital’s Justin Bender explains why XEQT is actually more diversified than VEQT:

Finally, after a college basketball star made $2M in endorsements, the internet hotly debated whether the 23-year-old was already set for life.

Have a great weekend, everyone!