Deceptive and Misleading Advertisements

It drives me nuts when I see deceptive and misleading advertisements in the financial services and investment industry. Personal finance can be complicated enough without having to bring a lawyer and a magnifying glass with you to interpret the fine print of every deal. Worse, still, is that many consumers take the bait without fully understanding what it is they're signing up for.

We know Canadians, for whatever reason, trust their banks and advisors, often deferring to their professional knowledge and expertise when it comes to financial matters. But ads that claim superior investment returns with no risk, or that promise cheap short-term borrowing without revealing the actual interest rate, can do great harm to consumers who fall for them.

Related: Free seminar – Learn how to get ripped off

Here are a few examples of deceptive and misleading advertisements in the financial industry:

Payday loans

Payday loan shops have been more prevalent lately, moving from the seedy strip mall to more visible stand-alone locations. The annual percentage rate (APR) on these types of payday advances can be as high as 599.64%. But you won't see that posted on any of their advertisements. Instead you'll see a statement saying something simple like this: Borrow $300 for $20.

What the consumer sees: “Sweet, I can get $300 to help me get by until payday and all it will cost me is $20.”

What this really means: The normal cost of borrowing $300 for 14 days at a place like CashMoney is $69, with a total payback amount of $369 and an APR of 599.64%. The $300 for $20 offer means the cost of borrowing is $20, with a total payback amount of $320 and an APR of 173.81%.

Desperate borrowers would be better off (by far) taking a cash advance from their credit card than using a payday loan shop.

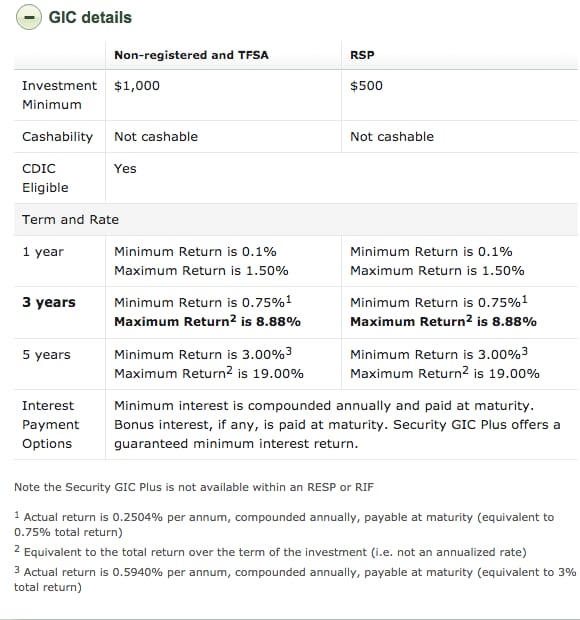

Market-linked GICs

Banks have been pushing market-linked GICs for years as interest rates plunged to historic lows. With this clever marketing gimmick, investors are guaranteed to get back their principal if markets go down, but also get to participate in some of the stock market growth if things go well.

Related: Are your elderly parents easy targets for financial scammers?

The actual interest rate is linked to stock market returns through a complex formula that requires an advanced degree in mathematics to figure out.

What the consumer sees: “Sweet, I can earn up to 8.88% PER YEAR on a GIC! Sign me up”

What this really means: The maximum possible “total” return over three years is 8.88%, which is closer to about 2.96% per year (if the stars align and you hit that target). If the markets tank, you'll get your principal back, plus a minimum of 0.25% per year on your money. Not a great gamble when you consider the best rate on a standard 3-year GIC is paying 2% a year, guaranteed.

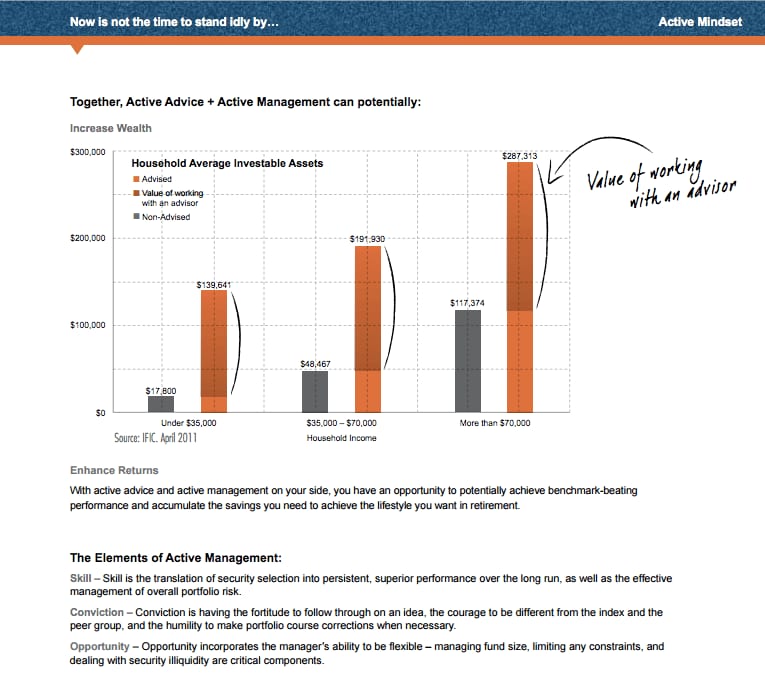

The value of advice

The investment industry took findings from the 2012 CIRANO study and beat investors over the head with claims about the value of working with an advisor, saying that across all income brackets, people who worked with a financial advisor had vastly more wealth – between 1.5 to 6.5 times more – than people who didn't.

What the consumer sees: “I must have to work with a trusted financial advisor in order to get wealthy.”

What this really means: A confusion of correlation and causation. Just because wealthy people use advisors and poorer people do not, doesn't mean that advisors are responsible for the difference in wealth. Don't forget, the industry touting these claims charges the highest fees in the world – fees that can erode investment returns by as much as two-thirds over the very long term.

Related: Ban on embedded commissions coming, despite industry objection

CIRANO president and CEO Claude Montmarquette was interviewed for an article in The Globe and Mail and had this to say about the financial industry overselling the value of advice:

“We need a better study and a better paper before I would be comfortable with the way they are saying what they are saying.”

That was over three years ago, yet the investment industry continues to trumpet false and misleading claims about the value of advice. Not only that, the industry continues to try and equate advice with investment outperformance, instead of accepting academic research which clearly shows that active management does not add any value.

Investment returns that are too good to be true

With the massive run-up in real estate prices in cities such as Toronto and Vancouver, it's common to see ads for new condo developments promising huge returns on investment without any downside risk. Using phrases like, “be the first in”, “one-day only”, and “guaranteed income”, these developers try and pre-sell condo units before they're even built, in hopes to take advantage of housing prices that have been rising faster than they can slap up four walls and a roof.

What the consumer sees: “Whoa! A 40% annual return on my investment! Count me in!”

What this really means: A last ditch effort to pre-sell condos at the tail-end of a real estate boom.

Back in 2014, The Globe and Mail warned investors to beware of investment condo ads selling massive returns. The article stated that the rules governing advertisements for real estate investing either seem to be less developed, or not enforced. That's why you often don't see disclosure of commissions and other fees, or any indication that returns are not guaranteed and past performance may not be repeated.

If there's a chance – not even a guarantee, but a chance – that this investment returns 40% a year, why wouldn't the developer and its insiders snap up every single unit and flip them later?

Final thoughts

So how do we protect ourselves against misleading and deceptive advertising? While we all should take personal responsibility for making smart choices and not getting duped, the financial industry doesn’t make it easy for us – designing complicated products, charging outrageous fees, and using high-pressure sales tactics to separate us from our hard-earned money.

For those who say, so what – buyer beware – The Globe and Mail’s Rob Carrick shared this brilliant response on his Facebook page a while back:

“Buyer beware? That’s a little Darwinian for me. I’d prefer not to live in a financial world where you get your bones picked clean if you fail to read the fine print.”

It is the age old story. If it looks to good to be true it usually is. And one thing to remember is that companies are in business to make money, not for you but for them!

I noticed the condo ad above is using the Dragon’s Den logo, I wonder if there is an actual connection or if they just blatantly used it without permission…

If it’s too good to be true, then it is deceptive. Ads are business and if they offer somethings that is hard to resist, think again. You must be careful when engaging in this kind of business because your hard-earned money is at stake.

Instead of putting all the need for “carefulness” on the shoulders of the client – why do we not just restore the notion that when offering something, especially in the financial realm, that there must be no hint of any kind of deception? These 8.88% rate of return offers are blatantly false – but they are symptomatic of the self-regulating deregulated governance that is poisoning the sale of securities in Canada. Clients are entitled to have a system that they know will not be fooling them. That can happen under a system of public regulation – where the common law of contract rules and the criminal code are the first regulatory tools.

The rate of annualized interest that can be charged at payday loan outfits – last I saw in BC is 644% per annum. Remember the days when it was a crime to charge over 50% per year? If we have postal banking revived, we could have this service made available even in the remote rural areas – where economic hardship is sometimes quite severe. Canadians need to focus their minds on these facts – and understand that these extremely unaffordable rates are being imposed on those in the lowest economic quintile.

My pet Pee re misleading advertising … Lottery draws…. 1 in 3 odds of winning a dream home… That is a lie, anyone who knows about how odds are calculated, know the odds of winning the major prize in a lottery is not true. I wrote government and they told me to take it up with organization running the lottery

new website design looks good

I’ve recently started to notice some of those real estate ads. They make mutual fund salespeople look good. The numbers in this example add up to a 4.5% return on the purchase price (plus leverage and wildly unrealistic price gains). I’m not familiar with real estate investing but I believe the pros won’t come close to touching a deal like that.

The bigger the lie in the financial world, the more folks believe it. What about “negative equity” in car leasing? Holy cow, I heard a co-worker talk about it, and I asked if they knew what it meant, they didn’t!

These are “SHARKS”. Period

Anyone with iota of common sense would know that they should be nowhere near these suckers

Robb,

Thanks for posting this. I especially appreciate your “outing” some of the offenders. There’s not enough information like this in the media.

My “trusted” advisor at TD Bank once tried (unsuccessfully) to sell me market-linked GICs.

When you think of how difficult and complicated it is for we consumers to navigate through the world of personal finance, it’s disgusting that these operators are allowed to get away with what they do. We really need more regulation to protect consumers !!

Great article

Got duped with market-linked – any suggestions on where/what to invest when matures?