I’ve long advocated that anyone who expects to live a long life should consider deferring their Canada Pension Plan to age 70. Doing so can increase your CPP payments by nearly 50% – an income stream that is both inflation-protected and payable for life. If taking CPP at 70 is such a good idea, why not also defer OAS to age 70?

Many people are unaware of the option to defer taking OAS benefits up to age 70. This measure was introduced for those who retired on or after July 1, 2013 – so it is still relatively new. Similar to deferring CPP, the start date for your OAS pension can be deferred up to five years with the pension payable increased by 0.6% for each month that the pension is deferred.

OAS Eligibility

By the way, unlike CPP there is no complicated formula to determine your eligibility and payment amount. That’s because OAS benefits are paid for out of general tax revenues of the Government of Canada. You do not pay into it directly. In fact, you can receive OAS even if you’ve never worked or if you are still working.

Simply put, you may qualify for a full OAS pension if you resided in Canada for at least 40 years after turning 18 (when you turn 65).

To be eligible for any OAS benefits you must:

- be 65 years old or older

- be a Canadian citizen or a legal resident at the time your OAS pension application is approved, and

- have resided in Canada for at least 10 years since the age of 18

You can apply for Old Age Security up to 11 months before you want your OAS pension to start.

Your deferred OAS payments will start on the date you indicate in writing on your Application for the Old Age Security Pension and the Guaranteed Income Supplement.

There is no financial advantage to defer your OAS pension after age 70. In fact, you risk losing benefits. If you’re over the age of 70 and not collecting OAS benefits make sure to apply for OAS right away.

Here are three reasons why you should defer OAS to age 70:

1). Enhanced Benefit – Defer OAS to 70 and get 36% more!

The standard age to take your OAS pension is 65. Unlike CPP, there is no option to take OAS early, such as at age 60. But you can defer it up to 60 months (five years) in exchange for an enhanced benefit.

Deferring OAS to age 70 can be a wise decision. You’ll receive 7.2% more each year that you delay taking OAS (up to a maximum of 36% more if you take OAS at age 70). Note that there is no incentive to delay taking OAS after age 70.

Here’s an example. The maximum monthly payment one can receive at age 65 (as of 2024) is $713.34. Expressed in annual terms, that equals $8,560.08.

Let’s look at the impact of deferring OAS to age 70. Benefits will increase by 0.6% for each month of deferral, so by age 70 we’ll see a total increase of 36%. That brings our annual OAS pension to $11,641.71 – an increase of $3,081.63 per year for your lifetime (indexed to inflation).

2). Avoid / Reduce OAS Clawback

In my experience working with clients in my fee-only practice, retirees are loath to give up any of their OAS benefits due to OAS clawbacks. That means designing retirement income and withdrawal strategies specifically to avoid or reduce the OAS clawback.

The Canada Revenue Agency (CRA) calls this OAS clawback an OAS pension recovery tax. If your income exceeds $86,912 (2023) then the OAS recovery tax will claw back your OAS payments in the period between July 2024 and June 2025. For every dollar of income above the threshold, your OAS pension is reduced by 15 cents. OAS is fully clawed back when income exceeds $142,124 (2023).

So, does deferring OAS help avoid or reduce the OAS clawback? In many cases, yes.

One example I’ve come across many times is when a client works beyond their 65th birthday. In this case, they may want to postpone OAS simply because they’re still working and don’t need the income. In some cases, the additional income received from OAS would be partially or completely clawed back due to a high income. Deferring OAS to at least the next calendar year when you’re in a lower tax bracket makes a lot of sense.

Aaron Hector, financial consultant at Doherty & Bryant, says there is a clear advantage to postponing OAS if someone expects their retirement income to push them into the OAS clawback zone.

“Not only will postponement provide them with an enhanced OAS income, it will also in turn provide them with a higher clawback ceiling,” said Mr. Hector.

It might also allow the opportunity to draw down RRSP/RRIF assets between 65 and 70 which would reduce future expected retirement income (lower RRSP/RRIF assets = lower mandatory withdrawals between age 72 and death).

One could also stash any unspent RRSP/RRIF withdrawals into their TFSA. Growing their TFSA in retirement gives retirees the valuable ability to withdraw money tax-free any time and not have that income affect their means-tested benefits (such as OAS).

3). Take OAS at 70 to Protect Against Longevity Risk

It’s counterintuitive to defer taking pensions such as CPP and OAS (even with an enhanced benefit for waiting) because it forces retirees to tap into their personal savings – depleting their nest egg earlier and faster than they’d prefer. Indeed, people are reluctant to spend their capital.

But this is a good thing, according to Retirement Income For Life author Fred Vettese. Deferring CPP and OAS increases the amount of guaranteed income you will have for the rest of your life, while also reducing your long-term investment risk because you are spending your savings first.

“Spend your risky dollars first because they may not be there for you in your 80s, depending on how your investments do. A bigger CPP (or OAS) cheque, however, will definitely be there for you.”

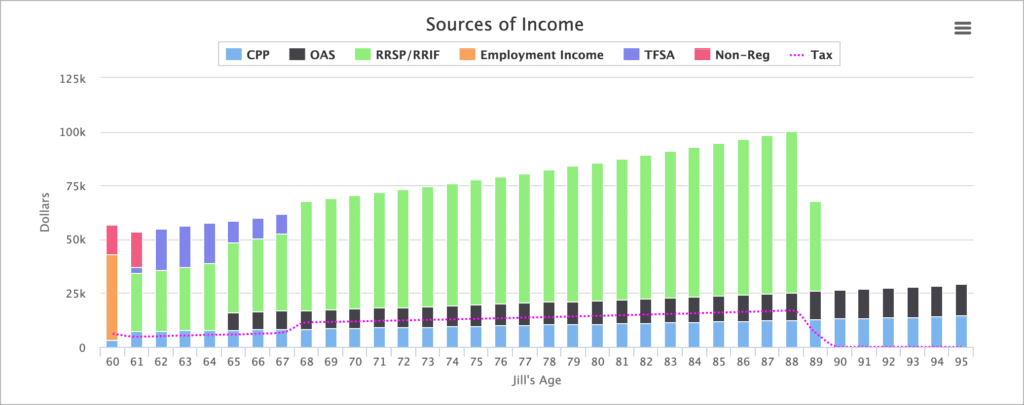

In one example I looked at a single 59-year-old woman – Jill Smith – who plans to retire on July 1st when she turns 60. Jill requires $48,000 in after-tax spending each year to meet her retirement goals.

She has $775,000 saved in her RRSP, plus $75,000 in her TFSA and $30,000 in cash. She’ll qualify for 80% of the CPP maximum and is fully eligible for OAS.

If Jill takes CPP right away (July 2) at age 60 and takes OAS at the standard age 65 she’ll have enough personal savings to last until she’s 89. Her CPP and OAS pensions make up 30.39% of her total annual income in retirement.

Now let’s compare this scenario with deferring CPP and OAS to age 70.

Not only does Jill increase the viability of her retirement plan – her personal savings now last until age 92 – but she has increased the portion of index-protected, paid-for-life government pensions to 54.25% of her total annual income.

Mr. Hector says that someone who fears running out of money in old age would be wise to postpone OAS to guarantee a higher base level of income when they are very old.

So those are three great reasons to take OAS at 70 – to enhance your annual OAS benefit, to reduce or avoid OAS clawbacks, and to protect against longevity risk.

Now let’s look at four reasons why you might not want to defer your OAS pension past 65.

1). The OAS Enhancement Is Less Enticing Than CPP

The actuarial adjustment you receive for deferring OAS to age 70 is much less than it is for deferred CPP to 70. It is just 36% compared to 42% for CPP. That makes a big difference, considering you’re foregoing your pension for five years. You want to make sure it’s worthwhile.

“When I compare the two side by side it really jumps out at you how there is a much greater incentive to deferring CPP than there is to defer OAS. This of course is due to the fact that there is a greater enhancement effect for CPP,” says Mr. Hector.

Ignoring income and clawback concerns, it is best to take OAS at age 65 for someone who is going to die between 65 and 79 for OAS, but for CPP the range shrinks to 65 to 77.

Taking OAS at age 70 gives the best outcome for those who live to age 88 and beyond.

2). Emotional Factor

Fred Vettese is a big proponent of deferring CPP until age 70 but not as enthusiastic about deferring OAS. He says that starting CPP late is already forcing the average retiree to draw down their RRIF balance much faster than they planned on doing. It is still a good move, but one that makes people uncomfortable.

He says asking people to start OAS late as well will accelerate the RRIF drawdown and make people that much more uncomfortable.

3). You Need The Money

Deferring CPP and/or OAS is a luxury for those who have the means to fund their lifestyle while they wait. Repeat: This is not a strategy for those who need to access their government benefits right away to get by.

Mr. Vettese says you need at least $200,000 saved before even considering the deferral strategy.

4). Leaving an Inheritance

Deferring OAS and CPP until age 70 means spending down a good portion of your personal savings in your 60s. This could also mean it’s possible to spend down most if not all of your personal savings before you die.

Related: The Retirement Risk Zone

While this ‘die broke’ strategy may be ideal for some, others may wish to leave an inheritance to their loved ones or to charity.

As there is no survivor-OAS pension, someone who is concerned about leaving a large estate to their heirs may decide that they would rather take OAS earlier so that they can leave their investments intact.

“The investments will always have a value for their beneficiaries but that is not true for someone who opted to defer OAS,” says Mr. Hector.

Final Thoughts

There’s no clear-cut answer for deciding if and when to defer OAS.

When I’m working with clients, I always make sure they understand to at least postpone taking OAS until retirement, or the next calendar year after retirement to avoid OAS clawbacks and additional taxes in the final working year.

Then we look at OAS clawback amounts (if any) and see what can be done to avoid them. Sometimes that means taking more from their RRSP/RRIF in their 60s while deferring OAS until somewhere between ages 67 to 70.

But the bottom line is that deferring OAS to 70 is a bet that you’ll live a long life. And, like with an annuity, rather than worrying about what happens if we die early, we should give more thought to whether we’ll live longer than expected.

With that in mind, deferring OAS by 1-5 years can help transfer the risk from your personal savings to the inflation-protected, paid-for-life government pension program.

The more we can ‘pensionize’ our retirement income, the better off we’ll be if we happen to live an extraordinary long life.

The investing landscape has certainly evolved for the better over the past two decades. Gone are the days when the only way to invest was to work with an expensive broker or mutual fund salesperson. Self-directed investing platforms, robo-advisors, and all-in-one ETFs have democratized investing – making it cheap and accessible for investors to build a portfolio at any age and stage.

Today, just as mutual funds dominated the investing scene in the 1990s, exchange-traded funds (ETFs) are exploding in popularity as investors flock to low cost passive investing products. The challenge for investors is to separate the wheat from the chaff. Indeed, according to the Canadian ETF Association (CETFA), there are now more than 1,100 ETFs offered by 40 ETF providers.

In this article, I’ll break out the top ETFs for Canadian investors to help you avoid analysis paralysis and make an informed decision about which ETFs to hold in your portfolio.

Then I’ll take it one step further and show you one simple portfolio to get started with a self-directed index investing portfolio, and one more complicated version to help investors with larger portfolios save on fees.

Top ETFs for Canadian Investors

First, let’s sort out the top ETFs from that list of 1,100+ funds. I’m going to stick with ETFs from the three largest ETF providers in Canada (stats from Jan 2023):

- BlackRock Canada: 143 ETFs and $104.9B in assets under management

- BMO Asset Management: 152 ETFs and $95.7B in assets under management

- Vanguard Canada: 37 ETFs and $59.7B in assets under management

I’m also going to screen out any ETFs that are actively managed or that focus on a specific sector (I’m looking at you, BetaPro Crude Oil 2x Daily Bull ETF).

Instead, we’re looking for ETFs that track as broad of an index as possible to give investors the ultimate diversification of global stocks and bonds. I’ve narrowed down the list to the top 20 ETFs on the market.

Canadian Equity ETFs

Each of these two ETFs offer exposure to approximately 200 of Canada’s top small, medium, and large companies for an ultra-low fee.

- Vanguard FTSE Canada All Cap Index ETF (VCN)

- iShares Core S&P/TSX Capped Composite Index ETF (XIC)

U.S. Equity ETFs

Each of these two ETFs offer exposure to the entire U.S. stock market by tracking the CRSP US Total Market Index.

- iShares Core S&P US Total Market Index ETF (XUU)

- Vanguard U.S. Total Market Index ETF (VUN)

International and Emerging Market ETFs

Vanguard’s VIU and iShares’ XEF offer exposure to thousands of stocks in the developed world outside of North America (Europe and the Pacific), while VEE and XEC, respectively, give investors exposure to thousands of stocks from emerging markets around the globe.

- Vanguard FTSE Developed All Cap ex North America Index ETF (VIU)

- Vanguard FTSE Emerging Markets All Cap Index ETF (VEE)

- iShares Core MSCI EAFE IMI Index ETF (XEF)

- iShares Core MSCI Emerging Markets IMI Index ETF (XEC)

Global Equity ETFs

Investors can avoid holding individual ETFs for U.S. equity, international equity, and emerging markets by choosing one of these two global equity ETFs (All World, ex Canada).

- iShares Core MSCI All Country World ex Canada Index ETF (XAW)

- Vanguard FTSE Global All Cap ex Canada Index ETF (VXC)

Bond ETFs

These popular Canadian bond ETFs give investors exposure to the broad universe of Canadian government and corporate bonds.

- BMO Aggregate Bond Index ETF (ZAG)

- Vanguard Canadian Aggregate Bond Index ETF (VAB)

All-in-One ETFs

Vanguard, iShares, and BMO all offer all-in-one balanced ETFs that come in several different flavours depending on your risk tolerance. These one-decision ETFs circumvent the need to hold multiple ETFs.

Vanguard

- Vanguard All-Equity ETF Portfolio (VEQT)

- Vanguard Growth ETF Portfolio (VGRO)

- Vanguard Balanced ETF Portfolio (VBAL)

iShares

- iShares Core Equity ETF Portfolio (XEQT)

- iShares Core Growth ETF Portfolio (XGRO)

- iShares Core Balanced ETF Portfolio (XBAL)

BMO

- BMO All Equity ETF (ZEQT)

- BMO Balanced ETF (ZBAL)

- BMO Growth ETF (ZGRO)

Model ETF Portfolios (Putting It All Together)

I’ve pulled out the top 20 ETFs, but that’s still a lot for investors to sort through when deciding which ones to use for their own portfolio. Now I’m going to break things down even further by showing you an ideal model ETF portfolio depending on the size of your account(s).

Along the way you may need to make trade-offs that include simple versus complex, low cost versus even lower cost, and automatic monitoring and rebalancing versus a more hands-on approach to portfolio construction.

The need for these trade-offs becomes more apparent as your portfolio grows over time.

One-Fund ETF Portfolio vs. 3-Fund ETF Portfolio

First, we’re going to look at an example of a young investor with an initial $10,000 to invest. We’ll assume the appropriate asset mix for this investor is a portfolio with 80 percent equities and 20 percent bonds.

Keep the process as simple as possible when you’re building an ETF portfolio. That means you should likely choose one of the asset allocation ETFs (one ETF solutions), such as iShares’ XGRO or Vanguard’s VGRO.

One-Fund ETF Portfolio ($10,000)

| Ticker | MER | % Allocation | $ Allocation | $ Fee |

| XGRO | 0.21% | 100% | $10,000 | |

| Total | 0.21% | 100% | $10,000 | $21 |

The trade-off for a slightly higher fee is the simplicity of these products. They automatically adjust your allocation behind the scenes, so you don’t have to monitor or rebalance on your own.

Select a self-directed investing platform, fund your account, and then purchase the single ETF. It’s that easy.

I’d recommend choosing Questrade, which offers free ETF purchases, or Wealthsimple Trade, the mobile-only investing platform that offers zero-commission ETF trades.

Since you’ll likely be adding new money regularly, and likely in smaller amounts, a one-ETF solution is ideal to avoid having to tinker and rebalance your portfolio with every contribution.

As you can see by the model portfolio breakdowns for the more complex portfolios, you’d be tweaking each individual ETFs amount with every purchase to try and stay true to your original asset mix.

Three-Fund ETF Portfolio ($10,000)

| Ticker | % MER | % Allocation | $ Allocation | $ Fee |

| VCN | 0.06% | 25% | $2,500 | |

| XAW | 0.22% | 55% | $5,500 | |

| VAB | 0.09% | 20% | $2,000 | |

| Total | 0.15% | 100% | $10,000 | $15 |

That’s why I highly recommend a one-ETF solution for new investors who plan to invest a small amount to start, and want to add small, frequent contributions with every paycheque.

Adding Complexity to Save on Fees

When you’re first starting your investing journey it makes sense to value simplicity over fees. That’s because in the early stages of investing your savings rate and contributions will have much more of an impact than fees.

But when your portfolio grows to the six-figure range, perhaps even around $200,000, these extra costs can certainly add up. At this point it can make sense to add some complexity, such as unbundling a one-ETF solution in favour of adding some lower fee U.S. listed ETFs.

U.S.-listed ETFs come with lower MERs and less foreign withholding taxes. But they require you to invest using U.S. currency. Since it can be expensive to convert currency, investors perform a manoeuvre known as Norbert’s Gambit to convert CAD to USD and vice-versa.

The good news is that if and when you’re ready to do this, a discount brokerage platform like Questrade can support USD and the Norbert’s Gambit move.

Let’s now look at model ETF portfolios for an investor with a $200,000 portfolio.

One-Fund ETF Portfolio ($200,000)

| Ticker | MER | % Allocation | $ Allocation | $ Fee |

| XGRO | 0.21% | 100% | $200,000 | |

| Total | 0.21% | 100% | $200,000 | $420 |

The one-ETF solution is still incredibly cheap compared to any mutual fund or actively managed portfolio.

But let’s show how low our costs can get when we dissect the portfolio into three ETFs.

Three-Fund ETF Portfolio ($200,000)

| Ticker | MER | % Allocation | $ Allocation | $ Fee |

| VCN | 0.06% | 25% | $50,000 | |

| XAW | 0.22% | 55% | $110,000 | |

| VAB | 0.09% | 20% | $40,000 | |

| Total | 0.15% | 100% | $200,000 | $308 |

With a $200,000 portfolio you’ll save $112 per year by using the three-ETF model portfolio.

Let’s take things one-step further with a five-ETF solution courtesy of PWL Capital’s Justin Bender and his “ridiculous” model ETF portfolio.

Lowest Fee ETF Solution (RRSPs – $200,000)

| Ticker | MER | % Allocation | $ Allocation | $ Fee |

| VAB | 0.09% | 20% | $40,000 | |

| VCN | 0.06% | 24% | $48,000 | |

| VTI | 0.03% | 31.83% | $63,660 | |

| VIU | 0.22% | 18.00% | $36,000 | |

| VWO | 0.10% | 6.17% | $12,340 | |

| Total | 0.09% | 100% | $200,000 | $180 |

With this low-fee solution our investor would save $240 per year by unbundling the one-ETF solution in favour of this five-ETF portfolio.

- Vanguard Canadian Aggregate Bond Index ETF

- Vanguard FTSE Canada All Cap Index ETF

- Vanguard Total Stock Market ETF (U.S.-listed)

- Vanguard FTSE Developed All Cap ex North America Index ETF

- Vanguard FTSE Emerging Markets ETF (U.S.-listed)

Two of the ETFs are U.S.-listed, meaning you’ll need a USD account and USD currency to purchase the funds. As mentioned, you’ll also need to perform the currency conversion move called Norbert’s Gambit to exchange CAD and USD and avoid currency conversion fees.

The extra tinkering, monitoring, and rebalancing may not be worth it for some investors (me included), but as your portfolio grows the cost savings may become too tempting to ignore.

Final thoughts

When you’re starting out with $5,000 or $10,000 to invest it doesn’t make a ton of sense to slice-and-dice your portfolio into a handful of different ETFs.

A one-ticket ETF is all you need at this stage while you build up your investment portfolio. Later on, as your portfolio grows and the fees start to creep up, then consider a more complex portfolio that can help you save on MER and foreign withholding taxes.

Related: Need help setting up your own DIY investing portfolio? Check out my DIY Investing Made Easy video series.

I know that 1,000+ ETFs can be overwhelming, and you may not know where to start. Hopefully this guide can help you avoid analysis paralysis so you can start investing confidently in ETFs.

Decide on a model portfolio and an asset mix that’s suitable for your situation. Use a self-directed investing platform like Questrade or Wealthsimple Trade to save on transactional costs. Put your money to work regularly by setting up automatic contributions.

And, finally, stick to your investing plan through good times and bad. Passive investing through index ETFs is designed to deliver market returns, minus a small fee. That means your investment portfolio will go up and down with the direction of the market.

Over the long term, that risk has paid off handsomely.

Nobel laureate Harry Markowitz famously said that diversification is the only free lunch in investing. A portfolio concentrated in just a handful of stocks, or one that holds only Canadian or US stocks, may have a much wider range of outcomes than a more broadly diversified portfolio that includes stocks from every country. Most investors should also have some bond exposure to help reduce volatility. Bonds tend to hold their value when stocks fall (yes, 2022 was a notable exception), so when that happens a diversified investor can sell bonds to buy more stocks at a discount.

This concept of diversification and using an appropriate asset mix makes good sense, but it might also make things complicated for the average investor to build a properly diversified portfolio.

However, if investing has been solved with low cost index funds, then investing complexity has been solved with asset allocation ETFs, or all-in-one ETFs.

What are Asset Allocation ETFs?

An asset allocation ETF holds a pre-determined mix of Canadian, US, international and emerging market stocks, plus Canadian, US, and international bonds. It automatically rebalances this mix when markets move up and down, so you don’t have to worry about tinkering with your portfolio.

Let’s say you invest in Vanguard’s Balanced ETF (VBAL). This asset allocation ETF is made up of seven underlying ETFs representing stocks and bonds from around the world. Altogether it holds more than 13,000 global stocks and 18,000 global bonds.

Most major ETF providers offer their own suite of asset allocation ETFs. You’ll typically find the classic 60/40 balanced ETF, an 80/20 growth-oriented ETF, a 40/60 conservative ETF, and even an aggressive 100% equity ETF.

Related: How I Invest My Own Money

For this article, we’re going to stick with the two biggest names in the asset allocation space: Vanguard and iShares.

Vanguard’s asset allocation ETFs include:

- Vanguard’s Conservative Income ETF (VCIP) – 20% stocks and 80% bonds

- Vanguard’s Conservative ETF (VCNS) – 40% stocks and 60% bonds

- Vanguard’s Balanced ETF (VBAL) – 60% stocks and 40% bonds

- Vanguard’s Growth ETF (VGRO) – 80% stocks and 20% bonds

- Vanguard’s All Equity ETF (VEQT) – 100% stocks

iShares’ asset allocation ETFs include:

- iShares Core Income Balanced ETF (XINC) – 20% stocks and 80% bonds

- iShares Core Conservative Balanced ETF (XCNS) – 40% stocks and 60% bonds

- iShares Core Balanced ETF (XBAL) – 60% stocks and 40% bonds

- iShares Core Growth ETF (XGRO) – 80% stocks and 20% bonds

- iShares Core Equity ETF (XEQT) – 100% stocks

How to choose the right asset allocation ETF?

This isn’t like the old days when you would try to pick winning mutual funds by looking up their past returns. By nature, over the long term, an all-equity portfolio is going to outperform an 80/20 portfolio, which will outperform a 60/40 portfolio, and so on.

Choosing the right asset allocation ETF starts with determining the most risk appropriate portfolio for your age, time horizon, goals, and your capacity to endure the ups and downs of the market. Too often investors chase past winners and then abandon ship when those winners come crashing down to earth. Conversely, many investors flee to conservative investments after a downturn, only to miss out on the eventual recovery when stocks rise again.

What we want to do is select an asset mix that we can stick to for the long term, regardless of the current market conditions. For many people, that’s the tried-and-true 60/40 balanced portfolio. For others, who maybe have a longer time horizon or a larger appetite for risk, an 80/20 or even a 100% stock portfolio may be perfectly sensible.

You can get a decent sense of your risk tolerance by taking this investor questionnaire on the Vanguard website.

Follow that up by watching this excellent video by Shannon Bender on how to choose the right asset allocation ETF:

I like this video because it gives you an idea of the range of outcomes you can expect from the various asset mixes over time. Hint, you should probably be more conservative than you think over timeframes of less than 10 years.

I use the following assumptions for expected future annual investment returns in my financial planning projections:

Average return assumptions

- Low risk 20/80 portfolio = 3.30%

- Conservative 40/60 portfolio = 4.00%

- Balanced 60/40 portfolio = 4.70%

- Growth 80/20 portfolio = 5.40%

- Aggressive 100% portfolio = 6.10%

Keep in mind these are long-term projections. Investment returns can vary widely in a single year. PWL Capital’s Justin Bender back-tested returns for each of the Vanguard and iShares‘ asset allocation portfolios and found the worst 1-year return for each of them:

Worst 1-year return

- Low risk 20/80 portfolio = -12.18%

- Conservative 40/60 portfolio = -18.85%

- Balanced 60/40 portfolio = -25.49%

- Growth 80/20 portfolio = -31.79%

- Aggressive 100% portfolio = -37.74%

However, the annualized 20-year returns were a lot closer to my financial planning assumptions:

Annualized 20-year returns

- Low risk 20/80 portfolio = 4.24%

- Conservative 40/60 portfolio = 5.14%

- Balanced 60/40 portfolio = 6.01%

- Growth 80/20 portfolio = 6.82%

- Aggressive 100% portfolio = 7.58%

You can see that there isn’t a huge difference in long-term returns between these portfolios. The goal is to be in an asset mix you can stick with for the long term, so if chasing the highest return with 100% stocks is going to cause you stomach-churning anxiety throughout your investing life, then take comfort knowing you’re not giving up much by choosing a balanced or growth portfolio.

Remember, nobody failed to meet their retirement goals because they invested in a sensible low-cost balanced portfolio instead of a more aggressive portfolio.

Strike a compromise between FOMO and fear. What I mean is that you want an asset mix that makes you feel just a little bit of FOMO when stocks are soaring, and feel a little bit less afraid when stocks are falling.

Vanguard, iShares, others?

Okay, so once you’ve selected an appropriate asset mix, you’ll still need to decide which ETF provider to choose (Vanguard, iShares, BMO, TD, Horizons, Mackenzie, and Fidelity all offer a suite of asset allocation ETFs).

I’ll keep this part brief because there’s no need to overthink it.

For simplicity, if you want to narrow down your decision, the asset allocation ETFs offered by Vanguard and iShares are perfectly sensible options for your portfolio. There aren’t enough differences to lose sleep over the decision.

iShares’ asset allocation ETFs are slightly cheaper – they cost 0.20% MER compared to Vanguard’s 0.24% MER at the time of this writing.

In terms of geographical weighting, iShares holds slightly more US equity and international equity, while Vanguard holds slightly more Canadian equity and emerging market equity.

The iShares’ portfolios have also slightly outperformed Vanguard’s pretty much across the board over all time periods, likely owing to US and international equity outperforming Canadian and emerging market equity.

The differences are negligible, though, so pick one provider and stick with it – or hedge your bets by holding a Vanguard product in one account and iShares in another. Just don’t switch between them every year chasing past performance.

Final Thoughts

It has never been easier to be a successful DIY investor than it is today. That’s because new one-stop investing solutions like asset allocation ETFs have taken the complexity out of building and maintaining a portfolio.

They’ll also save you a bundle on fees. Where most mutual fund portfolios charge an average MER of 2%, you’ll pay 1/10th of that with an asset allocation ETF.

If you want to reduce the investment fees that you pay, diversify your portfolio into an appropriate mix of global stocks and bonds, and simplify your investments with an all-in-one automatically rebalancing ETF, then consider switching to a risk appropriate asset allocation ETF.

That’s exactly what my DIY Investing Made Easy video series is designed to do – show you exactly how to make the transition from an expensive and underperforming mutual fund portfolio and into a simple, low cost asset allocation ETF so you can cut your fees to the bone and move on with your life.