I love sending readers and clients on a mission to test their financial advisor. I get them to ask about lower cost portfolio options such as index mutual funds or ETFs. The responses are typically hilarious – so much that I wrote an entire post on the sh!t my advisor says.

A reader I’ll call Michelle emailed me about a recent conversation with her advisor about switching to ETFs.

Hello Robb, I love your articles. Thank you!

I spoke to my advisor about switching to a low cost ETF strategy for my RRSP. She told me there can be liquidity issues with ETFs and that she always sells them with limit orders and it can take time. Is this true? I own one with CI First Asset that she recommended.

Also, she was trying to scare me that I’d be responsible for ensuring I drew down my RRSP properly, implying this was a difficult task that I might not be able to manage. I will have to start drawing down in 10 years.

Your thoughts would be much appreciated.

Michelle’s advisor is right in that limit orders are useful when buying and selling ETFs. That’s because the liquidity of an ETF is best measured by its bid-ask spread. The smaller the spread, the more liquid the ETF. Bid-ask spreads on large, liquid markets like the S&P 500 will be very tight at all times. Spreads will be wider in less liquid, more “niche” exposure ETFs.

Stocks with higher trading volume tend to be more liquid. But an ETFs liquidity reflects the liquidity of the underlying stocks or bonds it holds.

When in doubt, avoid trading too close to the market’s open or close, and always use a limit orders. Stick to broad-market ETFs. Look for all-in-one solutions like Vanguard’s VBAL, VGRO, or VEQT. It’s never been easier to be a do-it-yourself investor.

The advisor’s other comment – about Michelle drawing down her ETF portfolio – is nonsense. First of all, retirement is 10 years away. Why stay in expensive, actively managed mutual funds for the next decade on the assumption that Michelle’s advisor will do a good job assisting in the portfolio drawdown at that time?

Yes, retirement withdrawals can be complicated, and many investors will need guidance. But Michelle can pay for that guidance when the time comes, rather than overpaying for advice through product fees today. Or, she can take control of her DIY portfolio and follow a total return strategy to generate retirement income. Or, she can switch to a robo-advisor who can assist in portfolio withdrawals for a fraction of the cost of a full-service advisor.

There are plenty of reasons why commission-based advisors want to prevent their clients from switching to low cost index funds and ETFs. The most obvious is that actively managed mutual funds simply pay more commission to the fund dealer and advisor.

If we believe that, then it’s easy to paint commission-based advisors as devious and evil. But a recent paper titled, ‘The Misguided Beliefs of Financial Advisors‘ suggested that most advisors actually mean well, they just simply don’t know any better.

“Advisors give poor advice precisely because they have misguided beliefs. They recommend frequent trading and expensive, actively managed products because they believe active management, even after commissions, dominates passive management. Indeed, they hold the same investments that they recommend.”

If you work with an advisor at a bank or investment firm, don’t be afraid to challenge or question their advice, especially when it comes to fees on the products they recommend. For every high-fee, actively managed product there is a low-fee, passively managed equivalent that is most likely better suited for your portfolio. Insist on the low fee option.

This Week’s Recap:

This week I wrote about our tendency to kick debt down the road.

From the archives: How to create your own financial plan with these eight steps.

Over on Rewards Cards Canada: What’s the difference between Air Miles Cash Miles vs. Dream Miles?

Friday was my last official day in the office – hopefully forever!

Quit my job to blog full time. Am I retired?

— Boomer and Echo (@BoomerandEcho) December 7, 2019

Finally, a quick update on life insurance as a few readers asked if I had the option to convert my group insurance to a private policy. It turns out I can, but only to a maximum of $200,000. I’m happy with my decision to go with a new $600,000 15-year term life policy.

Promo of the Week:

One of the top no annual fee cash back cards on the market is Tangerine’s Money-Back Credit Card. Cardholders can earn 4 percent money-back on purchases in up to three categories for their first three months (2 percent thereafter), and 0.5 percent back on all other purchases.

Our partners at Credit Card Genius have a great promo offer for this card right now where you’ll get a $75 Amazon e-gift card on approval.

This Week’s Recap:

An economist tackles a big question – will the stock market crash in 2020?

A Wealth of Common Sense blogger Ben Carlson explains why bull markets last much longer than you think.

Rob Carrick shares some lessons from your fellow Canadians on how to be successful with TFSAs.

Mr. Carrick also shares an important piece on how investment firms are ducking responsibility for bad advice that costs clients:

“The investment industry talks endlessly about the value of the advice it provides. But no loophole goes unexplored in finding ways to avoid taking responsibility when that advice goes wrong.”

PWL Capital’s Ben Felix is back with his latest Common Sense Investing video about investing in IPOs:

Nick Magguilli (Of Dollars and Data) shares his psychological tricks for worry-free spending.

Michael James discovered an error in the rules-based spreadsheet he designed to manage his portfolio and now wrestles with a decision to fix his mistake.

The most dangerous of all people is the fool who thinks he is brilliant. Jason Zweig shares his own experience with overconfidence.

Million Dollar Journey compares bond ETFs, GICs, and high interest savings accounts in this fixed income investing summary.

Finally, travel expert Barry Choi shares eight hotel booking tips to ensure you get the best value when booking hotels online.

Have a great weekend, everyone!

Canadians started piling on the debt after the financial crisis in 2008. Back then our household debt-to-income ratio was sitting around 150 percent ($1.50 owed for every dollar of disposable income). Today that number hovers around 177 percent. We are kicking debt down the road, instead of kicking it to the curb.

It can be reasonable to take on debt for big ticket items such as a mortgage, vehicle, education, or for an investment. We often do so because it’s easier to pay off a loan over time than it is to save enough to pay the full cost upfront. That’s life.

But the pain of debt can be masked by the cheap cost of borrowing. Low monthly payments, interest-only payments, and long amortization periods give the illusion that our debts are manageable. We think a long overdue raise, promotion, tax refund, or some other windfall will solve our money problems, but until then the debts keep piling up.

We get trapped in an unending cycle of minimum monthly payments and creditors are happy to oblige if it means getting you into a bigger house with a new SUV and an annual trip to the Dominican.

Here are four ways we keep kicking debt down the road:

1.) Minimum payments on your credit card

A cardinal sin of personal finance. We’ve all seen the disclaimers on our credit card statements that say if we only make the minimum payment each month it’ll take a lifetime to pay off your balance in full.

My latest American Express statement had an outstanding balance of $1,086 and the minimum monthly payment was only $10. At that rate it would take 9 years and 1 month to erase the $1,086 debt, and I would have paid another $1,000 in interest charges along the way.

Yet many people do this every single month. It’s easy to see why when you’re living paycheque-to-paycheque and there’s no wiggle room in your budget. A $10 payment gets the credit card company off your back and gives you some breathing room today. Unfortunately it’s your future self who’s forced to pay the bill.

The average credit card debt is hovering around $4,200, according to TransUnion. Most credit cards charge 19.99 percent interest or higher, making this one of the most expensive forms of debt to carry over from month to month.

That’s why I recommend treating credit card debt like a four alarm fire emergency. Slash your spending, pause any savings plans, and divert any extra cash you can towards your credit card balance until it’s gone for good. This is one debt you cannot afford to kick down the road.

Related: Debt avalanche vs. Debt snowball

2.) Interest-only payments on your line of credit

The run-up in housing prices over the last decade has fueled a borrowing frenzy with Canadians tapping into their home equity at a record pace. Canadian home equity line of credit balances reached $230 billion earlier this year. That’s more than 3 million HELOC accounts open at an average outstanding balance of about $65,000.

One insidious feature of a HELOC is that it only requires a monthly interest payment. In fact, about 40 percent of HELOC borrowers don’t regularly pay down the principal.

Let’s say you have a $70,000 balance and the interest rate on your HELOC is 4 percent. Your monthly interest payment would be about $233 and each month that amount would be taken from your chequing account and applied to the HELOC balance.

But unlike other loan repayments there is nothing stopping a borrower from transferring that $233 right back to his or her chequing account – a move called “capitalizing the interest.” Also known as kicking debt down the road forever.

A big line of credit balance tends to linger until the mortgage comes up for renewal, in which case the borrower tries to roll the HELOC balance back into the mortgage, or until the homeowner sells the home and the balance is paid off from the sale proceeds.

A HELOC is not an ATM. It can be useful for a specific purpose, such as a home renovation or to buy a car. Using it to supplement your income, though, is a bad idea that will catch up with you eventually.

If you find yourself with a lingering line of credit balance make a plan to pay it off over a reasonable amount of time. Set up automatic transfers from your chequing account each month to match your target pay off date and start whittling down that balance today.

3.) Extending your amortization

You bought a house and took out a mortgage amortized over 25 years. When it comes time to renew in five years, instead of sticking with your amortization schedule at 20 years, your mortgage broker talks you into extending the amortization back to 25 years to keep your payments low.

While it might sound good in theory to give yourself the flexibility of a low payment in case of emergency, it’s too tempting to use that option to free up extra cash flow for lifestyle inflation and spending.

Extending your amortization means never getting any closer to paying off your mortgage. It prioritizes today’s cash flow over tomorrow’s freedom – not something your future self will appreciate when you have to delay retirement until that damn mortgage is paid off.

The smart move is to not only stick to the original amortization schedule on your mortgage but also to reduce it further by changing your payments to bi-weekly instead of monthly, increasing your payment by $50 or $100 when your budget allows it, and taking advantage of your pre-payment privileges when possible.

Making mortgage payments is automation at its finest – forced savings that you won’t miss once it has left your account.

4.) Long-term car loans

Canadian auto debt continues to grow as the average consumer’s auto-loan balance climbed to $20,160 last year. I’m on record saying that Canadians’ obsession with having two brand-new trucks or SUVs in the driveway is killing our finances.

Blame the fact that six and seven year car loans are now the norm.

The trend towards longer term car loans is problematic for two reasons. One, people are getting talked into buying more expensive cars at the dealership. That’s because the focus is about the monthly payment rather than the total cost of financing the vehicle. Longer term loans keep monthly payments affordable and increase the chances of selling an expensive vehicle.

Two, consumers get trapped in a negative equity cycle when they want to trade-in their vehicle before it’s paid off. The existing loan balance gets rolled into the new car loan, and the now more expensive car loan cycle begins.

Related: Why does my car dealer want to buy back my car?

Breaking the cycle takes sacrifice. Drive your cars longer (10 years+), buy used, only buy as much car as you need, reduce your household vehicles from two to one, and save up and pay cash for your next one.

Final thoughts

Successful money management starts with being smart about debt. Kicking it down the road only prolongs the inevitable.

Tackle your credit card balance first, and be relentless. You’ll never get a better guaranteed return than paying down debt at 20 percent interest. Stop treating your home equity like an ATM and start paying down the principal. Don’t wait until you sell your home.

Stick to your amortization schedule and try to pay off your mortgage in 15-25 years. Extending your amortization or taking payment vacations is not a path to prosperity.

Finally, break that auto-loan cycle. Long term financing might make your monthly payments more affordable today, but it’s awfully expensive in the end, especially if you keep trading in your car every 3-5 years.

The last quarter of 2018 was a miserable time for investors. The S&P 500 had reached an all-time high on September 21, 2018. Three months later it had fallen nearly 13 percent – erasing 18 months of gains along the way. The TSX also fell more than 13 percent. Panic ensued, with many pundits predicting the beginning of the next stock market crash.

That didn’t happen. Instead, the S&P 500 proceeded to climb to new all-time highs. At market close on Friday, the U.S. market had gained an incredible 27.72 percent since its December 21st low. Not to be outdone, the TSX gained a healthy 24.15 percent in that time.

Welcome to market volatility.

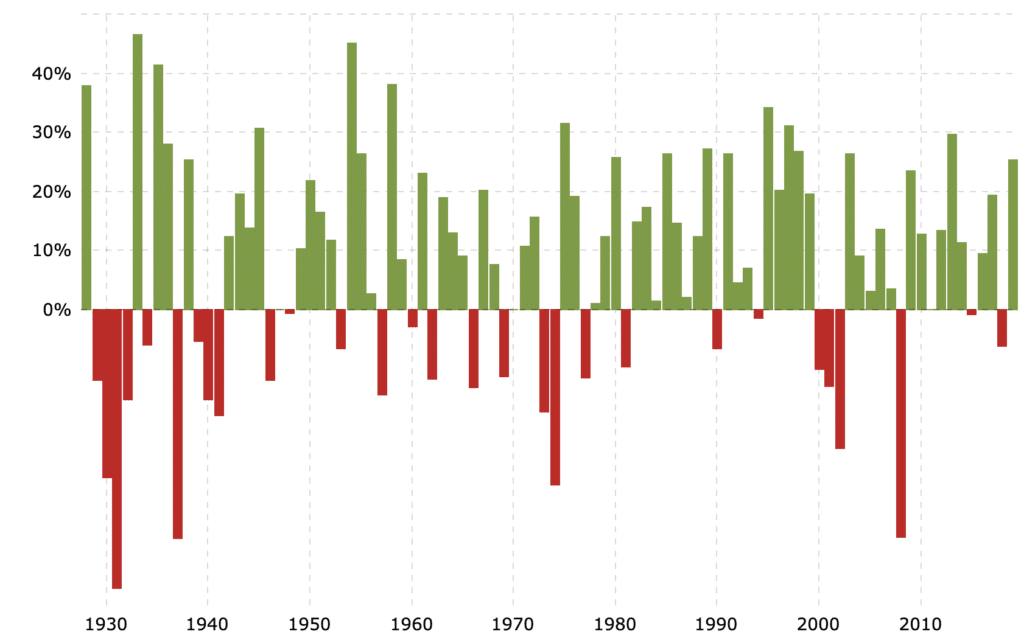

Most reasonable investors, depending on the make-up of their portfolio, can expect to earn market returns of 6-10 percent over the long term. But the dispersion of those expected returns can vary wildly, from 47 percent losses (1931) to 47 percent gains (1933) and everything in between.

Exactly how volatile is the stock market? From 1928 to 2019 (91 years), the S&P 500 posted annual returns of between 6 and 10 percent exactly six times (1959, 1965, 1968, 1993, 2004, 2016).

The market lost ground in 29 of those 91 years (roughly one-third of the time), with six of those years posting losses of 20 percent or more.

Investors should accept this volatility to capture the market risk premium – the difference between the expected return on a market portfolio and the risk-free rate – over the long term.

But, behaviourally, we’re prone to panic when markets fall and to feel elated when markets rise. We know this behaviour is to our detriment, yet we do it time and time again. Markets fall, investors sell. Markets rise, investors buy back in.

The winning investor is the one with the fortitude to stay invested during turbulent times. Yes, markets can fall. They tend to do so one-third of the time. This is fully expected. But panic-selling at the bottom also tends to miss the inevitable recovery, which often comes quickly.

How do we curb our bad investing behaviour? We start with an appropriate asset mix of stocks and bonds. How do you know what’s appropriate? Take a close look at the above chart and decide how much money you’d be prepared to lose in a given year.

Adding bonds smooths out market volatility and delivers a tighter dispersion of returns.

The biggest one-year loss posted by a portfolio with 40 percent stocks and 60 percent bonds has been -11.82 percent. The classic balanced portfolio of 60 percent stocks and 40 percent bonds lost 19.61 percent in its worst year, while an all-equity global portfolio has posted a one-year loss of -34.85 percent*.

*Source: CPM Model ETF Portfolios

Another trick is to simplify your portfolio to the point where you can ignore it for long periods of time. That’s why Rip Van Winkle would have made a great investor. Automate contributions and rebalancing whenever possible. This can be done through a robo-advisor or, for DIY investors, an asset allocation ETF.

That’s exactly where I’m at with my all-in-one investing solution (VEQT). I didn’t even realize markets were down last quarter until I heard it on a podcast in mid-December.

Finally, making smaller, more frequent contributions helps eliminate the desire to hold off until things “settle down” or “feel safer”. Automate and ignore.

This Week’s Recap:

Speaking of bad behaviour, this week I wrote about how to trick your lizard brain into saving more money.

Over on Young & Thrifty I went back to my dividend roots and looked at the pros and cons of a dividend investing strategy.

It’s my last official day of work next Friday! I’ll continue to keep you posted on my transition to full-time entrepreneur. My life insurance policy was approved and is now in place. That means an overlap in coverage and twice the death benefit if I die in December. My wife is weighing her options.

Next up is a look at my pension, and the decision whether to leave it in the plan and take a deferred pension at 55 (or older), or transfer the commuted value of the pension into a LIRA. I have a good idea what I’d like to do, but I’m waiting for the official documents from the pension board before I make my decision.

Promo of the Week:

I’ve fielded quite a few questions from retirees about moving their portfolio to Wealthsimple to save on fees and to help with automating retirement income withdrawals. First, I send them to this excellent case study on using Wealthsimple in retirement.

Transferring to Wealthsimple is about as easy as it gets. I know because I’ve helped my wife transfer her RRSP to Wealthsimple and it was a breeze.

Finally, to open a Wealthsimple account, use this referral link and you’ll get your first $10,000 managed free.

Weekend Reading:

The federal government announced the new TFSA contribution limit in 2020 will remain the same as 2019 at $6,000. That brings the total contribution limit to $69,500 for an eligible Canadian who has never contributed to his or her TFSA.

I’m sure many of you have seen the Laurentian Bank’s digital arm (LBC) offering a 3.3 percent high interest savings account. Rob Carrick asks if you should jump on this rate, while cautioning readers that this rate is highly unlikely to remain this high, despite what the bank says. We’ve seen this movie before from EQ Bank, which entered the market at 3 percent before eventually settling in at a still reasonable 2.3 percent.

Did you shop on Black Friday? Here’s why lawmakers in France are trying to ban Black Friday to help stop waste.

Why the pain of a failed investment can be the best teacher of all:

Those who have never experienced large market declines are at a distinct disadvantage to those who have. Many investors today don’t even remember the near-collapse in 2008, the bear market of 2000 to 2002 or the white-knuckle abyss of 1987.

A Wealth of Common Sense blogger Ben Carlson explains why market all-time highs are both scary and normal.

Carlson and his Animal Spirits podcasting cohort (Michael Batnick) debate whether day care is the next student loan crisis:

As people live longer than ever, there’s danger in counting on an inheritance to fund retirement.

Rob Carrick has a message to the 42 percent of credit-card holders who do not pay their balance in full every month: Stop using your card and switch to debit.

Dale Roberts explains why you don’t have to be the perfect investor trying to build the perfect portfolio. It’s more than OK to be a great investor.

On the My Own Advisor blog, Mark Seed and Steve Bridge debate whether the 4 percent safe withdrawal rate still makes sense.

Finally, credit expert Richard Moxley explains how your cell phone bill can keep you from getting the best mortgage rate.

Have a great weekend, everyone!