I’ve written before about my modified pursuit of FIRE (Financial Independence, Retire Early). The twist is that I’m striving for FIE – to be a Financially Independent Entrepreneur. It’s an idea that I haven’t been able to get out of my head lately. Here’s why:

For as long as I’ve been writing this blog I’ve had a goal to achieve financial freedom by age 45. I’ve also declared a goal of reaching $1M in net worth by the end of 2021, the year I turn 41.

I’m on pace to achieve that, perhaps slightly ahead of schedule. More importantly, though, is a realization that my so-called side hustle – the online income earned from blogging, freelance writing, and financial planning – has far surpassed my full-time salary. Simply put, I could leave my day job tomorrow and still pull in enough income to meet our spending and savings goals.

So what’s holding me back? A few things. The security of a full-time job with benefits. A wife and two children who depend on my income. A $200,000 mortgage. The angst of where my next freelance contract will come from (and when it will be paid). Navigating the constantly changing online world while trying to earn a living. Having enough of a cushion in the bank in case things go sideways.

I think about all of those things. But the reality is my business has grown by nearly 50 percent this year. I’ve never been busier, and I know there’s plenty of opportunities I’m leaving on the table because I can only do so much on evenings and weekends.

If you’re familiar with Dragon’s Den pitches, the dragons always ask the entrepreneurs if they’re into their venture 100 percent, or if they’re still entrenched in their day job just in case their big idea doesn’t pan out. Invariably, the dragons pass on pitches where the entrepreneur isn’t fully committed to his or her venture. They want the founder to be all in.

I’m not saying that I’ll be taking my talents to Dragon’s Den anytime soon. The point is, as an entrepreneur, there comes a time when you need to be all-in to realize your full potential. It’s funny, but I’m scared to go all-in right now, even though I know that I earn enough income on the side to replace my salary and continue to live the same lifestyle.

What I’m trying to wrap my head around is the additional earning potential if I can dedicate even 10-15 more hours a week to my online business. The more I think about that, the more sure I am that I can make this work financially.

I like to wrestle with big financial decisions by talking them out here on the blog. It’s a great platform for these kinds of discussions. And while I won’t throw out a date or deadline as to when I plan to make this transition, know that it’s been on my mind for some time and I’m getting very close to pulling the trigger.

Financially Independent Entrepreneur. I like the sound of that.

This Week’s Recap:

This week I collaborated with Erika Toth, a director at BMO ETFs, to dispel the myth that passive investing is in a bubble.

Over on the Young & Thrifty blog I shared a beginner’s guide to index funds.

I went to Seattle this week to explore the city and take in the Seahawks vs. Rams game (which was an amazing game to see live!).

My wife and I are off to Vancouver next week to celebrate our anniversary. Hopefully we luck out with the same great, sunny weather!

Promo of the Week:

Interest rates on savings accounts have been ticking down at most big banks and credit unions. Once a market leader, Tangerine recently dropped its interest rate to a pitiful 1.15 percent. If you want to earn a higher rate on your savings then you need to look outside the big banks and consider an online bank.

EQ Bank has offered one of the best interest rates in the country since it launched in 2016. Its EQ Bank Savings Plus Account, which has also has some chequing account functionality, pays a healthy 2.30%* interest. That’s double Tangerine’s savings account and nearly triple what some of the big banks currently offer (short term promos aside).

What I like about EQ Bank is that it doesn’t mess around with short term promotions and teasers. It pays an everyday high interest rate – currently 2.30%* – on every dollar (up to a maximum of $200,000).

If you’re the type of person who likes to hold a large amount of cash, whether it’s an emergency fund or a short-to-medium term savings goal – do yourself a favour and start earning higher interest on that savings. Sign up for an EQ Bank Savings Plus Account here.

*Interest is calculated daily on the total closing balance and paid monthly. Rates are per annum and subject to change without notice.

Weekend Reading:

Stephen Weyman at Credit Card Genius shares the best credit card offers, sign-up bonuses, and deals for October.

Are wealth taxes a good idea? Here’s Nick Magguilli on the pros and cons of a net worth tax.

Some big thinking here by Morgan Housel on the three most important forces shaping the world:

“Find something that’s important to you in 2019 – social, political, economic, whatever – and with a little effort you can trace the roots of its importance back to World War II. There are so few exceptions to this rule it’s astounding.”

Speaking of FIRE, here’s why this couple ditched the FIRE movement and couldn’t be happier.

Advisors say this is the biggest behavioural bias driving investment mistakes.

Melissa Leong explains how to give yourself a fall money makeover.

Million Dollar Journey blogger Frugal Trader answers a reader question from a low income senior trying to decide between a TFSA and RRSP.

Erica Alini tackles the best way to generate cash from your investments in retirement.

In this video, PWL Capital’s Ben Felix offers his own take on the index investment bubble theory:

One of the biggest myths in investing is that you need to beat the market. You don’t — and you probably couldn’t if you tried.

The Evidence Based Investor blog offers five strategies that are better than timing the market:

“In summary, timing the market — while superficially an attractive idea — is fraught with danger. If you get lucky, great, but there’s no method to it. We’ve seen that not even the gurus are much good at it.”

A good piece by Ben Carlson on resulting: our tendency to equate the quality of a decision with the quality of its outcome.

The classic question of whether you should keep your company pension, or take a lump-sum pension buyout and invest it yourself.

Should you pay for your child’s university education? The Blunt Bean Counter blog explains how to tackle this problem.

Finally, Canadian Budget Binder explains how hoarding affects your children when you’re gone.

Have a great weekend, everyone!

There have been many ridiculous statements made about passive investing over the years. None have garnered as much media attention as hedge-fund manager Michael Burry’s claim that passive investments such as index funds and ETFs are the next bubble. He said these index-tracking investments are “inflating stock and bond prices in a similar way that collateralized debt obligations did for subprime mortgages more than 10 years ago.”

“When the massive inflows into passive vehicles reverse, it will be ugly.” – Michael Burry

Such a bold claim from someone who correctly called the subprime mortgage crisis is certainly cause for concern. But when you peel back the layers, Burry’s statement doesn’t make much sense. Looking for a smarter take than that, I reached out to Erika Toth, a Director of ETFs at BMO Global Asset Management, to explain why passive investing is not in a bubble.

Take it away, Erika:

Debunking Michael Burry’s Passive Investing Bubble Claim

I may not have had Christian Bale play me in a movie, and I did not make millions during the financial crisis, but I have spent years now studying market structure and eating, sleeping, and breathing ETFs. Burry’s comments that sparked a media frenzy (and let’s all agree that the financial media loves to sensationalize) echo some of the most common myths and misconceptions I have encountered on the ETF wrapper.

This “passive investing is in a bubble” argument assumes that all the money invested in passive indices has flowed in to the same indices, that hold the same stocks, in the same proportions. However, there are many different types of passive funds and ETFs – some track the S&P 500, some track indices built around low volatility, quality, value, or momentum filters. Some track specific sectors.

Related: What’s not to love about ETFs?

Different investors have different investment objectives and motivations. Some want to buy the market. Some require higher cash flow. Some require lower volatility. Some are searching to exploit market inefficiencies in order to generate alpha. Pension funds have to make sure their liabilities are funded. Some investors are searching for companies that meet the highest environmental, social, and governance standards. Some require certain tax efficiencies or credit qualities to be met. Therefore, it is impossible that the entire world stock and bond markets would move to 100% passive.

It’s also important to note that individual stock ownership by households (domestic and foreign) accounts for just over half of the equity market – the largest share, by far. Mutual funds (active and passive) own about 24%; ETFs own about 6%. Pension funds would represent about 10% (government and private); and about 8% is owned in other vehicles such as hedge funds. (This is according to data put together by the Federal Reserve Board – see here).

ETFs themselves are too small a slice of the overall pie to be able to cause a crash in the prices of the stocks they hold; they simply reflect those prices. Those statistics are for the equity market. ETF ownership of the global bond market is even smaller, roughly 2-3% by most estimates.

The theory that everyone will run to the exits at the same time in the event of a major downturn is incorrect, and 2008 is a good example of that. My favourite example comes from Ray Kerzehro, who is Director of Research at independent firm PWL Capital, in the still-very-relevant white paper he published in 2016.

Kerzehro examines how high yield bond ETFs in the U.S. traded during the height of the financial crisis. Keep in mind that high yield bonds are NOT a large cap equity index made up of the largest and most liquid stocks in the world – they are a riskier asset class of lower credit quality and are less liquid as well. So, even in this riskier and less liquid asset class, there was actually no massive exodus from those ETFs.

What happened is that trading VOLUME actually spiked. Buyers & sellers of the ETF units had different views for different reasons, and the ETF structure actually provided price discovery to an asset class where many of the underlying bonds had gone no-bid.

Another key point to make is that large ETF providers, who hold the majority of the market share both here and in the U.S., establish minimum trading volume criteria for every security they hold. This ensures that they will be able to offer a liquid market on that security.

The market makers themselves (the plumbing behind the whole ETF eco-system) are also in competition with each other to offer the most competitive bid-ask spreads, which helps keep markets liquid. They make money on transaction volume.

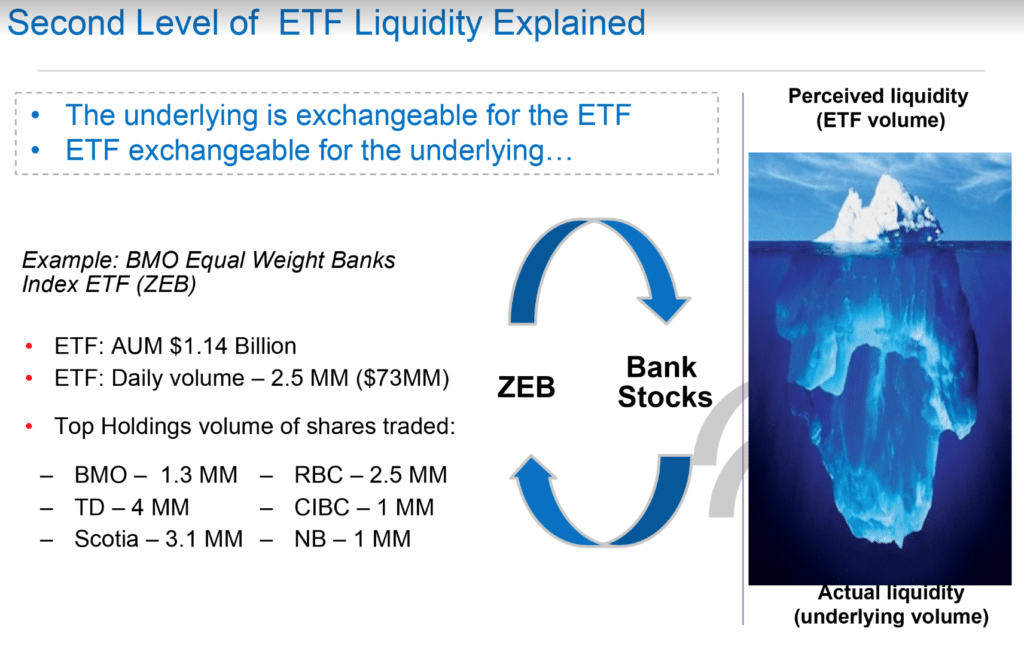

The ETF Liquidity Myth

Another common misconception is surrounding ETF liquidity. ETFs are like stocks in the sense that they trade on the stock exchange. For individual stocks, the higher the trading volume, the more liquid that stock is.

However, with an ETF, liquidity is best measured by its bid-ask spread. In general, an ETF’s liquidity reflects the liquidity of the underlying stocks or bonds it holds.

Related: VEQT – My new one-ticket investing solution

A good way to think of it is that the number of the ETF’s units you see trading are only the tip of the iceberg. The true liquidity is the trading volume of all the securities it holds.

Bid-ask spreads

The bid-ask spread is the difference in what you are able to buy the ETF for, versus the price you would be able to obtain if you are selling it.

This is the best indicator of how liquid an ETF is. A very liquid ETF will have a minimal difference between the two.

The spread represents the compensation to the market maker for assuming the risk and making a liquid market for that security. It is a component of the total cost of ownership of an ETF and is sometimes overlooked by investors. In general, the longer the holding period, the less significant this entry/exit cost is as a component of total cost. If you are more of a longer-term, buy and hold investor, in other words, this should not matter that much. However, if you trade more actively, this is something you should be more aware of.

*An important consideration, especially if the price per unit of that ETF is $50 or higher, is to calculate the bid-ask spread as a percentage of Net Asset Value (NAV). An ETF trading at $50 per unit may be just as liquid as an ETF trading at $25 per unit, even though it appears to have a bid-ask spread that is wider (3-4 cents, compared to 1 or 2 cents on a $25 NAV).

Bid-ask spreads on large, liquid markets such as the S&P 500, S&P/TSX or the FTSE Canada Universe Bond Index – will be very tight at all times.

When you start looking at overseas markets that may be closed during our market hours, it is normal to have spreads that are a bit wider. For European equities, the best time to trade would be between 10 and 11 a.m. Eastern Time. For Asian markets, there is actually no overlap with our market hours.

The best practice is simply to avoid trading too close to the open or the close, and to always use limit orders.

In more volatile markets, it is normal to see spreads widen.

Spreads will also be wider on less liquid areas of the market and on more “niche” exposure ETFs.

Market-weighting versus Equal-weighting

Market cap weighting tilts your exposure towards the largest companies within the index. Equal weighting will give you more of a tilt towards the smaller companies within the index, versus owning the market-cap weighted index.

Over the long term, smaller- and mid-cap stocks may outperform since the risk level is higher. In times of market duress, one may prefer to have a market-weight orientation.

For certain areas of the market that are less diversified, such as Canadian sector equities, investing in a cap-weighted index may result in a very concentrated position in 2-3 stocks. In these situations, it may be preferable to access that sector with an equally-weighted approach.

Related: 3 ways to build an investment portfolio on the cheap

Some portfolio managers and investors prefer market-cap weighting on the other hand, as it provides “truer” exposure to that sector. It is a matter of preference.

Either way, it is important to look under the hood of an ETF and understand what you are owning and why. If you are considering taking an exposure to a particular sector, compare the market weighted version with the equal weighted version in order to determine the differences: long term performance, risk level (standard deviation), dividend yield, how it behaved in negative markets, and identify any concentration issues in certain stocks or sub-sectors.

Final Thoughts

Thanks so much to BMO’s Erika Toth for going under the hood to dispel ETF myths and misconceptions, and to explain exactly why passive investing in ETFs won’t cause a bubble. Bold claims from famous investors make for great headlines, but when we look to the evidence we often find these statements don’t hold water.

Here’s some further reading to help educate investors about the myths and misconceptions of ETFs:

- Debunking the Myths on ETFs

- ETF Due Diligence Checklist

- Understanding ETFs Part 1 – the Basics

- Trading and the True Liquidity of an ETF

BMO Global Asset Management – Understanding ETFs video series:

It seemed like I was everywhere but here this week. The Canadian Financial Summit launched on Thursday and my 30-minute retirement readiness interview with host Kyle Prevost was included in Friday’s line-up. There’s still time to catch Saturday’s sessions and/or get the All Access Pass for instant lifetime access to all three days (25+ sessions) for just $97.

I also hosted my first AMA (ask me anything) on Reddit this past Thursday. What a fun experience answering practical money questions from the Personal Finance Canada community that boasts more than 131,000 members. You can read the entire AMA thread here.

Both the Summit and AMA sent over dozens of new subscribers, so thanks for joining our community here and welcome!

As many of you know, I also post a ‘Money Bag‘ feature from time-to-time where I answer reader questions. I’m hoping to publish another one in early October so I’d love to hear your burning questions about personal finance, investing, or retirement. Go ahead and ask me anything in the comments here and I might feature your question in the next edition of the Money Bag.

Speaking of questions, my latest Toronto Star column on getting the best mortgage deal generated a bunch of feedback from readers. Not surprisingly, the angriest and most critical replies came from mortgage brokers – who I suggested you could side-step by using a rate comparison site. It brings to mind this famous Upton Sinclair quote:

“It is difficult to get a man to understand something, when his salary depends on him not understanding it.”

On a personal note, I’ve got some upcoming travel that will have me leaving behind this unpleasant southern Alberta snow storm and heading to Seattle for a couple of days. I’ll be at the Los Angelas Rams vs. Seattle Seahawks game Thursday night, watching my first live NFL game in 20 years. Should be fun!

The following week my wife and I are off to Vancouver to celebrate our anniversary with a kid-free weekend. Thanks to the RBC WestJet World Elite MasterCard’s latest $250 welcome bonus (and first-year free) and companion voucher the flight cost just $99+ tax.

Despite the busy travel schedule I’ve got a great line-up of posts to share here next week, including a look at the ridiculous claim that passive investing is in a bubble, plus we’ll take a look at preparing for the next recession.

Weekend Reading:

Stephen Weyman at Credit Card Genius shares seven things you’re paying too much for while travelling.

Canadians might be finally getting the message about low cost investing. ETF sales eclipsed mutual fund sales in August. Despite the positive sales, we still have a long way to go. Mutual fund assets sit at $1.57 trillion compared to ETF assets of $186 billion.

Mark Seed interviews Jonathan Chevreau to discuss how active and passive investing can exist in retirement harmony.

And here’s another good one from Mark about why you should consider downsizing:

“Downsizing can open up a new chapter for you, too. Whether you are an empty-nester, single, a couple with no kids or you’re simply aspiring to start fresh – downsizing can offer a host of environmental, physical, mental and financial benefits.”

Bridget Casey wound up with an unexpected LIRA after a temporary work contract ended. Here she digs into what exactly a LIRA is and what to do with it.

Tax credits, tax rates, and tax deductions. Desirae Odjick decodes the 2019 election promises.

Nick Magguilli (Of Dollars and Data) explains why there are no secrets and no easy answers in investing.

Rob McLister (RateSpy) gives a thorough explanation of how much you can borrow with a reverse mortgage.

One of the biggest complaints about the Canada Pension Plan is its meagre survivor’s benefit. Rob Carrick digs into that and argues the cost of a strong CPP is that the survivor’s benefit is pretty bad.

- Did you know the average CPP payment in 2019 is $679.16 per month (or about $8,150 per year)?

Jonathan Chevreau explains how to avoid tax nightmares when RRIF withdrawals start.

An interesting first person account on how long it takes to get used to being retired:

“I did not miss work, but I did miss the camaraderie with my peers a great deal. So, I became a social animal going out for far more coffee klatches and two-hour lunches with friends and ex-colleagues than I could afford on my reduced income. As time passed, it became boring and purposeless to do this several times a week anyway.”

Finally, a shocking claim from Telus that a former senior manager used her corporate credit card for more than $180,000 in personal expenses. Wow.

Have a great weekend, everyone!