The reason I put so much emphasis on low investment fees is because it’s one of the few key areas that investors can control (the others being asset allocation, rebalancing, and savings rate). Yet most investors focus on the area they cannot control – their portfolio returns.

While it’s reasonable to expect investment returns in the 4 – 8 percent range over the very long term, the actual distribution of those returns can vary widely. Indeed, over the two decades investors have seen annual returns ranging anywhere from a 30 percent loss to a 30 percent gain. That’s a wide distribution of outcomes, yet the end-result over that 20-year period for a balanced portfolio of Canadian, U.S., and international stocks and bonds is about 5.80 percent.

Part of an advisor’s job is managing investor expectations. Beware of any advisor promising returns of any kind in the short term, especially the old “protection on the downside” advice.

As much as I preach about ditching your expensive mutual funds to move to a low cost portfolio of index funds, whether that’s through a robo-advisor or on your own with a discount broker and a one-ticket balanced ETF, I am extremely aware that we have been in a bull market for the last 10 years. When the inevitable market correction happens, and it will, investors will panic about their returns and look to blame someone.

Switching to a low cost, passive investing approach is not a panacea that will protect you from market downturns. By definition your portfolio will deliver market returns, minus a very small fee. Sometimes, like in late 2018, the markets will dive and your portfolio will lose money.

But here’s one investing truth you can take to the bank: A low fee, globally diversified portfolio of ETFs will beat a high fee actively managed investment approach nine times out of 10 over the very long term. And since you cannot identify the one outlier in advance, you can be confident that your investment performance will beat 90 percent of active strategies.

For further reading, Canadian Couch Potato blogger and investment advisor Dan Bortolotti skillfully answers a question about managing investor expectations in this excellent MoneySense piece.

This Week’s Recap:

I was incredibly honoured to join the selection panel this year for MoneySense’s 7th annual best ETFs in Canada series. We looked at Canadian, U.S., International, fixed income, and all-in-one ETFs from a universe of 833 funds, narrowing down the list to rank the top 25. Each panelist also included a “desert island” pick – a single ETF we’d feel comfortable holding for the long term.

Over on the Toronto Star I reviewed the three best hotel rewards programs in Canada.

Back here on Friday I offered a step-by-step guide on how to transfer your RRSP to Wealthsimple.

Promo of the Week:

You guys are loving KOHO, the no-fee, pre-paid, and reloadable VISA card and full-service account on your phone. Join KOHO and use the referral code BOOMECHO to get up to $60 ($20 when you make your first purchase, and an additional $40 when you add a direct deposit (payroll, government cheque, etc.).

The there’s STACK, the prepaid MasterCard that you can use world-wide wherever MasterCard is accepted. Get $20 when you download and activate your STACK card through my referral link <— (note that you’ll need to click the link via your mobile device for it to work, since it’s an app and only available via the App Store and Google Play).

Weekend Reading:

Wealthsimple’s Money Diaries series features interesting people telling their financial life stories. This edition highlights Philadelphia Flyers goaltending legend Bernie Parent, who entered the NHL making $20,000 per year.

Here’s a must read money series that features Abigail Disney (granddaughter of Roy) explaining what it’s like to grow up with more money than you’ll ever spend:

“If I were queen of the world, I would pass a law against private jets, because they enable you to get around a certain reality. You don’t have to go through an airport terminal, you don’t have to interact, you don’t have to be patient, you don’t have to be uncomfortable. These are the things that remind us we’re human.”

Morgan Housel on why luck is the flip side of risk: You cannot understand one without appreciating the other.

Here’s a tough question: If you had $1 million in 1919 (100 years ago), what could you have invested in back then to preserve its purchasing power until today?

Mike Moffatt wrote a very interesting post on the mass exodus out of Toronto – what he describes as the number one issue for the province over the next 20 years.

Preet Banerjee is back with another episode in his Learn About Investing series, this time with a look at investment funds:

Million Dollar Journey blogger Frugal Trader updates his financial freedom goals with an impressive $48,200 in dividend income.

Michael James talks about the idea of staying in the workforce to pad his retirement savings. I hear this a lot of my place of work and I’ve determined, as Michael did, that nobody has regretted taking the opportunity to retire early.

Why is it that people only seem to pay attention to personal finance when it elicits a harmful emotion? Ben Carlson says it’s because the topics tend to be too boring to talk about otherwise.

Here’s Dan Bortolotti on how to use ETFs in your child’s RESP. I’ll admit I have not done the math on this but I’m sticking with TD’s e-Series funds for my kids’ education savings – simply due to avoiding trading fees on our regular monthly contributions.

Rob Carrick shares a turbo-charged but dangerous way to earn more credit card reward points.

Finally, a retirement professional shares the secrets of a successful retiree. I love the focus on health, people, pursuits, and places.

Have a great weekend, everyone!

A client asked me to send step-by-step instructions on how to transfer your RRSP to Wealthsimple. He’s moving his $145,000 portfolio from Primerica over to Wealthsimple’s robo-advisor platform to save on fees.

My client’s existing “Asset Builder Fund” charges a management expense ratio (MER) of 2.30 percent – costing him $3,335 in fees each year. A similar portfolio at Wealthsimple is expected to cost just $957. That is comprised of a 0.40 percent management fee for a Wealthsimple Black account (a price break for funded accounts of $100,000 or more), plus an estimated 0.26 percent MER from the ETFs used to construct the portfolio.

Is my client thrilled with the idea of slashing his fees by nearly $2,400 per year? You bet!

It’s important to know that you don’t need to have a tough conversation with your current financial advisor before you transfer your funds to Wealthsimple (or any financial institution, for that matter). You simply ask your new financial institution to initiate the transfer on your behalf.

I’ve personally initiated this transfer several times with different institutions (big banks and online banks). In my experience, no bank handles this better than Wealthsimple. It was seamless.

Let’s walk you through the step-by-step process of how to transfer your RRSP to Wealthsimple:

How to Transfer Your RRSP to Wealthsimple:

First you need to open a Wealthsimple account. Use this referral link and you’ll get a $50 cash bonus when you open and fund an account with $500 within 45 days.

Click on “Get Started” and then enter an email address and a password to create an account.

Getting started with Wealthsimple

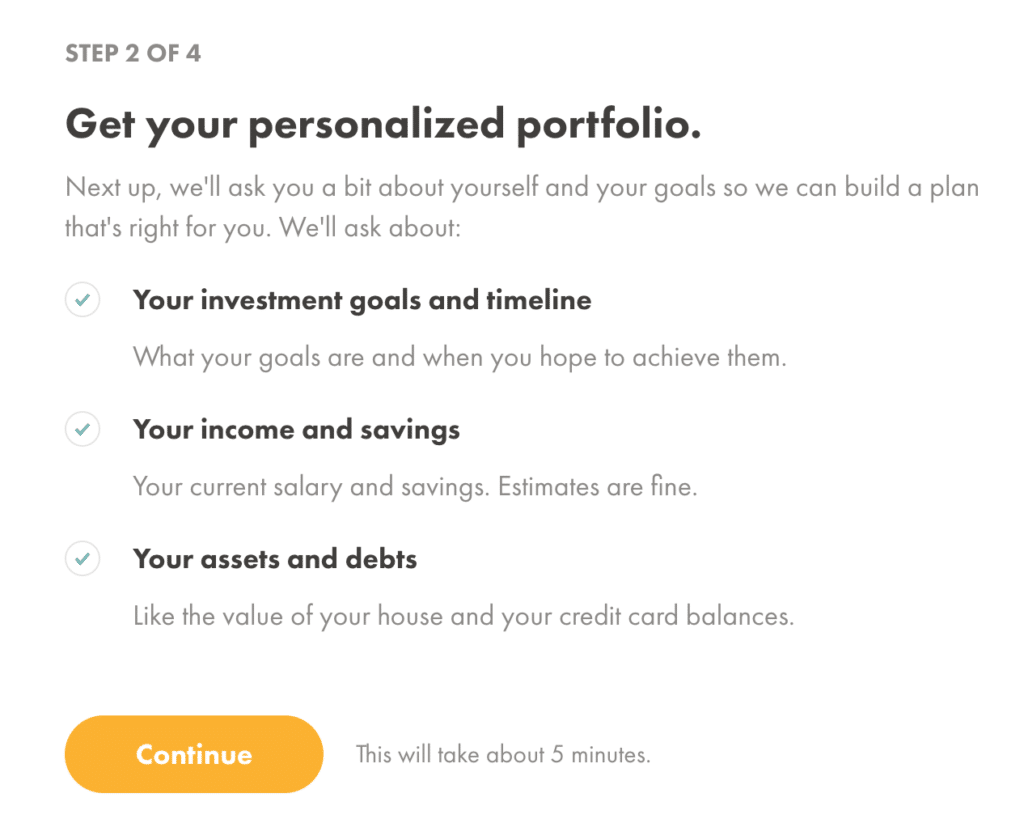

Click “Get Started” again and you’ll be prompted to enter basic personal information such as your name, phone number, employment information, and mailing address. This will take approximately three minutes and is designed to verify your identity and secure your account.

Your Personalized Portfolio

Next you’ll answer questions about your investing experience, goals, and time horizon. You’ll also enter your current salary and monthly savings rate (estimates are fine). Finally, you’ll list your existing assets such as your RRSP balance and estimated home value, plus any liabilities such as a mortgage or outstanding credit cards.

The goal with this section is for Wealthsimple to learn about you and recommend a personalized portfolio. This section takes five minutes to complete.

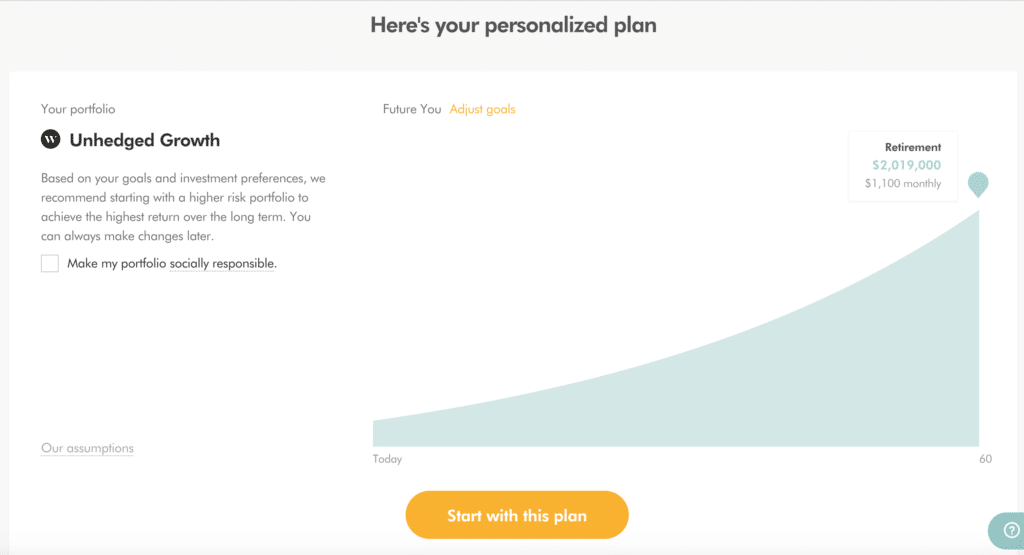

Answer the questions and you’ll get a personalized portfolio like the one recommended below. It’s an “Unhedged Growth” portfolio, which is a mix of 80 percent equities and 20 percent bonds. Portfolios range from conservative to balanced, and aggressive.

If you’re happy with the portfolio it suggests for you then go ahead and click “Start with this plan”. (You can always change it later).

Funding Your Wealthsimple Account

In step number three you have the option to transfer an existing account or to open a brand new account. Since we’re transferring an existing RRSP account from Primerica we’ll select the option to transfer an existing account.

Transferring Funds To Wealthsimple

Here’s where Wealthsimple really shines and makes it easy for new customers to transfer over their existing accounts to their platform. With other banks, you need to fill out a complicated transfer authorization form (like this one from TD. Seriously, you can’t even save the completed form onto your computer – you need to print it off and bring it to a branch).

With Wealthsimple, my wife followed these steps to transfer a small RRSP from Tangerine to Wealthsimple and the online process could not have been more straightforward.

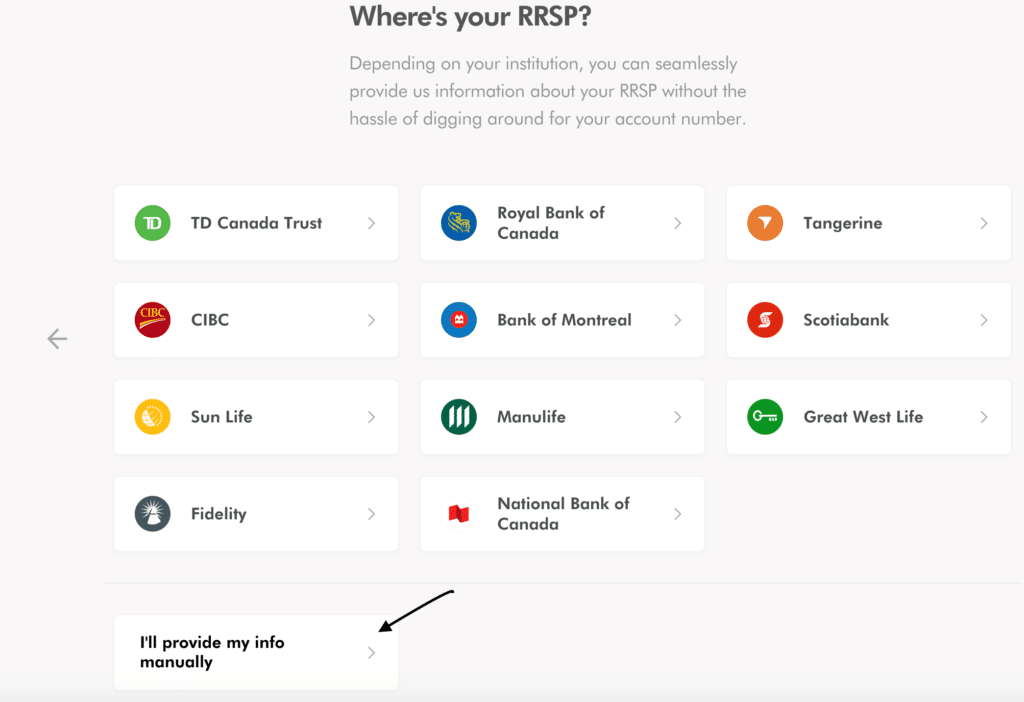

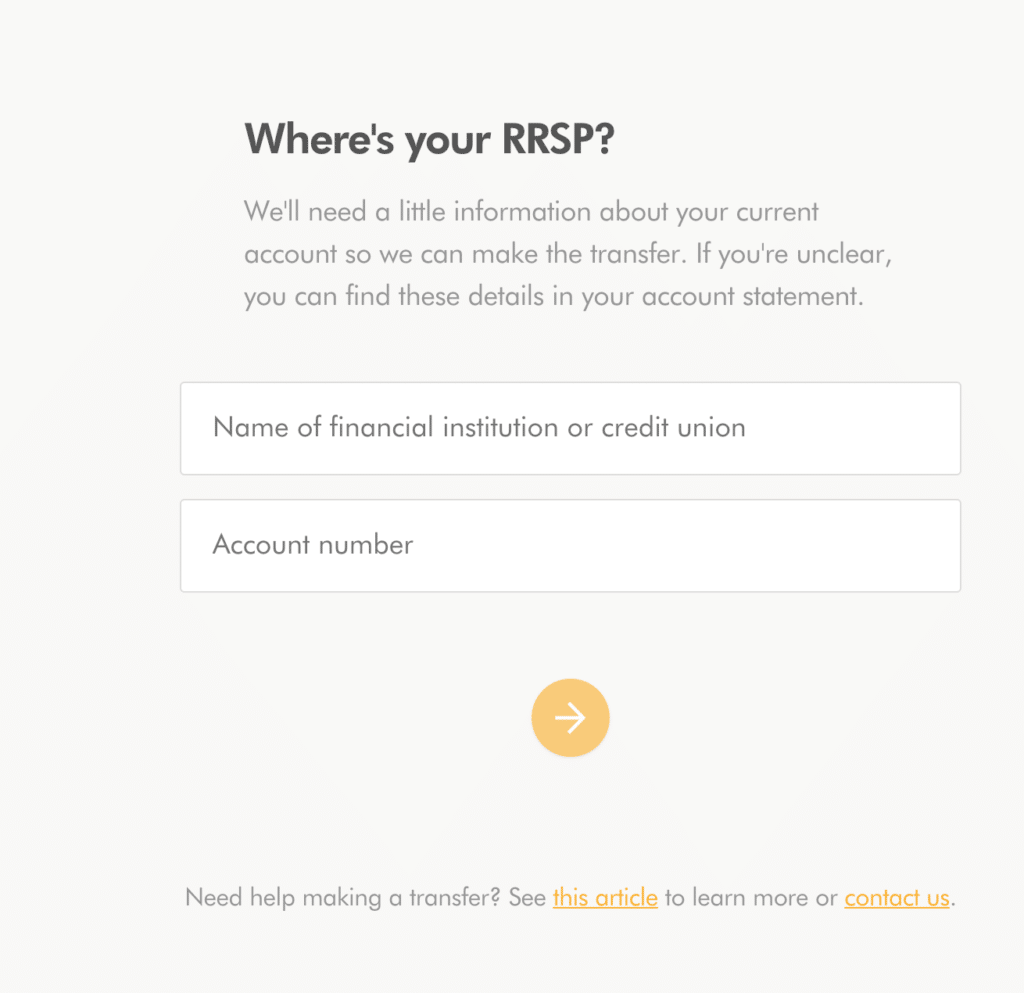

If your existing RRSP is held with one of the 11 institutions in the image below then you can make a simple process even more seamless without the hassle of digging out a statement.

Since Primerica is not one of those institutions we’ll have to provide the information manually (which sounds more difficult than it will actually be).

Find a recent investment statement, enter the name of the institution from which you’re transferring the RRSP, and then enter your account number.

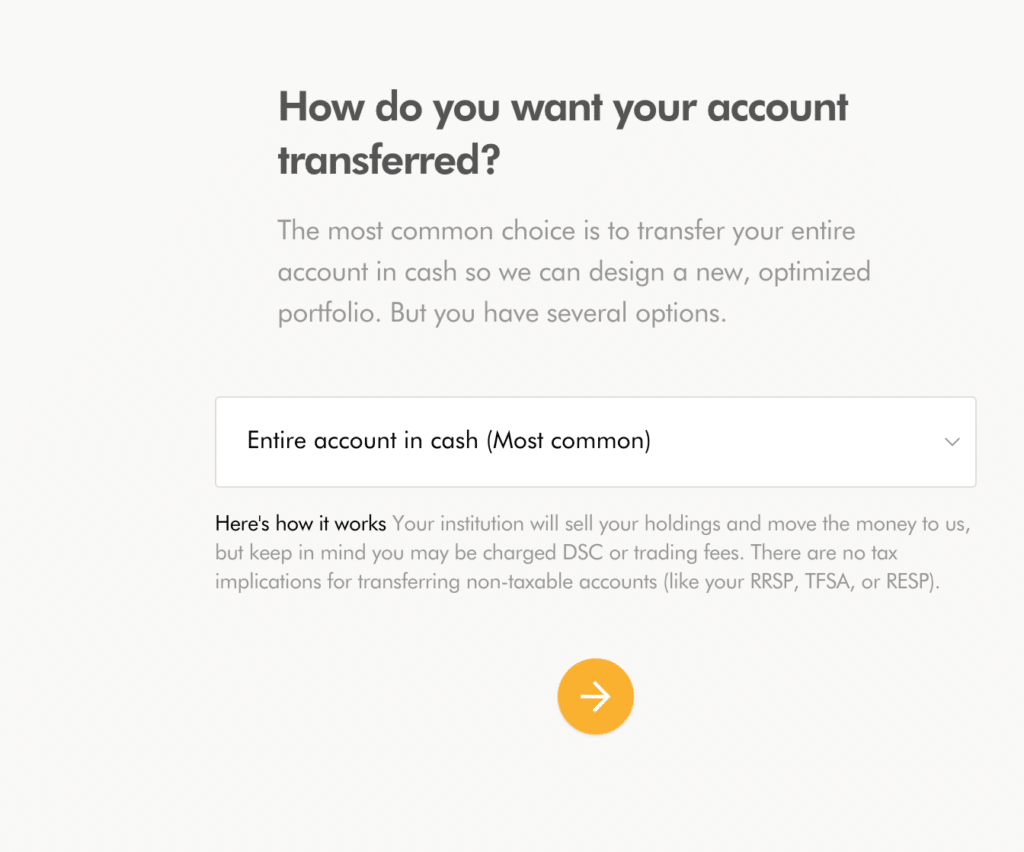

Next they’ll want to know how you want your account transferred. This can be done one of two ways. You can transfer your holdings “in-kind” which means your existing bank moves your investments “as-is” to the new institution without selling anything. This might occur if you held common stocks or shares in widely sold ETFs. The trouble is, most investment firms have proprietary funds that other institutions don’t sell (think: Tangerine Investment Funds).

The other, more common method is to transfer your account “in cash”. This means the existing bank sells your holdings and then moves the funds in cash to the new institution receiving the transfer. In some cases, due to the sale of mutual funds, you may be charged a deferred sales charge.

In many cases you will be charged a “transfer out” fee (ask if the receiving institution will cover these fees). Wealthsimple will reimburse transfer fees if you transfer more than $5,000 to your Wealthsimple account.

Finally, keep in mind that there are no tax implications for transferring non-taxable accounts such as your RRSP, TFSA, or RESP.

If you have an investment statement handy then simply upload a PDF copy (optional). Review and submit your transfer request and Wealthsimple will take it from there.

Wealthsimple will contact your financial institution to initiate the transfer and that’s all that’s required from you. You will see the estimated completion date in your Wealthsimple dashboard once they’ve sent off the transfer request.

You may notice that your funds have left your existing investment account but have yet to show up in Wealthsimple – this is completely normal and a good sign that your transfer is in its final stages. Most institutions send a cheque through the mail, and once received they will deposit the funds in your account and notify you immediately.

Final thoughts

I write a lot about why you should ditch your high priced mutual funds. I’ve done the math on your investment fees and showed you the ugly results. And I’ve beaten you over the head with reasons why indexing with low cost ETFs can lead to better investment outcomes.

What I haven’t done is written much about the actual mechanics of how to transfer your RRSP or TFSA to another institution to save on fees.

Many of you have got the message and have been waiting for clear direction on how to take action. I hope you found this step-by-step guide useful. Wealthsimple happened to be the example of the day, but you can do this with any of the robo-advisors in Canada. You can also open a discount brokerage account online or with a big bank and build your own DIY portfolio.

Do you have a question about moving your account from one institution to another to save on investment fees? Let me know in the comments and I’ll try to point you in the right direction.

We’re getting ready for our 32-day trip to the Scotland and Ireland this summer and our family could not be more excited about the itinerary we have planned. One thing that does concern me about the trip is the low Canadian dollar. The loonie hit an 11-day low on Friday, sinking to 74.53 cents USD.

We don’t need American dollars for our trip. Scotland takes the British Pound while Ireland is on the Euro. Unfortunately our Canadian dollar does not go very far in either country. We’ll only get 56 cents on the dollar in Scotland, and a slight uptick in Ireland at 66 cents per Canadian dollar.

Luckily our biggest ticket items will be paid up in advance, with our flights paid for courtesy of Aeroplan miles, and our hotels in Dublin and Edinburgh covered through Marriott rewards points. We’ve booked Airbnb’s for our other two major destinations, paying half in advance when we booked last summer and the remaining half due 30 days before arrival.

But let’s be honest: Food, drink, and attractions will make up a huge chunk of our travel budget while we’re abroad. I plan to use the

Of course, there are other options to exchange currency when travelling. The first that comes to mind is your local bank, but they typically charge excessive fees on the foreign currency conversion. The spread might be better at a foreign exchange office at the airport or in the tourism district at your destination, but your mileage may vary.

A new option called STACK looks like it could be the ticket to withdrawing cash at ATMs around the world without any fees. STACK is a prepaid MasterCard that you can use world-wide wherever MasterCard is accepted. You can access your cash anywhere without paying ATM withdrawal fees (you may incur a fee from the machine itself), and you won’t pay a transaction fee when making purchases outside of Canada.

Get $20 when you download and activate your STACK card through my referral link <— (note that you’ll need to click the link via your mobile device for it to work, since it’s an app and only available via the App Store and Google Play). Sign up through my link and I’ll get $5 too, which might get me half a pint of Guinness in Dublin 🙂

This Week(s) Recap:

Last week I wrote about CarGurus vs. Unhaggle in a battle of online car buying websites.

And this past Tuesday I opened up the Money Bag to answer reader questions about investing a lump sum and about finding the best credit card for everyday spending.

Thanks so much for sending in your questions for the Money Bag segment. I read every one and promise to get back to you by email or answer the question in a future post.

Weekend Reading:

The federal government put forth its 2019 budget this week and Rob Carrick breaks down the eight ways it will affect your personal finances.

One of those budget items is a proposed shared equity mortgage for first time home buyers in partnership with the government-backed Canada Mortgage and Housing Corporation (CMHC).

Collaborative Fund’s Morgan Housel muses on death, taxes, and a few other life guarantees.

Here are four reasons why you might not get that great mortgage rate you found online:

“Mortgage lenders offer better rates on high-ratio mortgages because of mortgage-default insurance. Lenders know they’re protected if you stop paying your mortgage, and that means they’re more willing to offer a good rate.”

A former industry executive reveals how badly customers are being ripped off on eyewear. The Italian optical behemoth, Luxottica, gobbled up dozens of luxury brands along with store fronts such as LensCrafters and Sunglass Hut. The mark-up for lenses and frames is approaching 1000 percent.

When I shared the article on my Facebook page, a few commenters suggested looking at Clearly.ca and a U.S.-based site called Zenni Optical to save big on eyewear.

Nick Magguilli explains why even the greatest investors are not immune from error.

The Irrelevant Investor Michael Batnick lists the twenty craziest investing facts ever. My favourite:

“Since 1916, the Dow has made new all-time highs less than 5% of all days, but over that time it’s up 25,568%.

95% of the time you’re underwater. The less you look the better off you’ll be.”

The deferred sales charge structure was created to preserve generous commissions for mutual fund sales. Dan Hallett explains why it’s time for DSCs to be banned.

Robo-advisors are catching on with a reported 1 in 3 Canadians who intended to open an RRSP account choosing to “go robo”.

He’s 65, his mortgage is paid off and he has $370,000 in savings, so why is he still worried about money?

Barry Choi has seen a large increase in income over the years, but here he explains why he still embraces frugal living.

Here’s what it costs to live in a retirement home – and the bottom line is less than you might think.

What the heck are ‘liquid alts’ and why are there so many of them, all of a sudden?

My Own Advisor Mark Seed explains just how and why to ditch your expensive mutual funds. I couldn’t agree more. I just finished looking at a client’s portfolio – $650,000 invested in a mishmash of high fee mutual funds and segregated funds costing him $13,000 per year in fees. Yikes!

Finally, Preet Banerjee on the emerging threat to personal finances in a cashless world. Paying with plastic doesn’t feel as painful as cash:

“There are two components to a transaction. Not only do you have the pain of payment, but you also have the pleasure of consumption. The tighter these two components are coupled, the more you feel that pain.”

Have a great weekend, everyone!