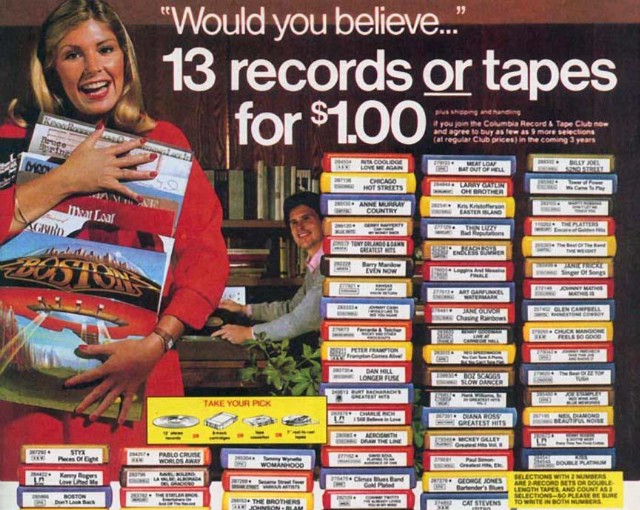

Anyone born before 1990 should remember Columbia House – the “world’s largest record club” – whose claim to fame was offering dirt-cheap music upfront to members who joined its mail-order subscription service.

The company made billions by using something called ‘negative option billing’, a process by which the customer agrees to have goods or services supplied automatically until a specific cancellation order is issued.

In the case of Columbia House, its members would receive discounted records, cassettes, or CDs – often up to a dozen for as little as one penny – and in the fine print agree to buy a limited number of items at full list price over a period of time.

On the surface, the deal seemed too good to be true. Basically free music! Then the offers kept coming and coming – I guess they really did want you to buy more albums after all. But at $25 a pop, plus shipping and handling, suddenly the deal didn’t look so appealing.

If you were like teenaged me, you ignored the offers until one day they stopped arriving in the mail. Something else arrived later on, though – a collection notice.

I’m sure we can all relate to that story – whether it was as a teenager with Columbia House, or some other subscription service that we got suckered into buying.

What’s your subscription addiction?

A similar offer caught my eye this past Christmas. Join the Disney Movie Club and get five Disney movies for $1. All I had to do was buy five more movies at regular price ($34.95 for Blu-ray, plus shipping) over the next 24 months.

I passed. Just because a product or service is cool, unique, or even free for a limited time, doesn’t mean you need to buy it. That’s doubly true when it comes to subscriptions.

Remember, the awesome power of automating your savings – setting it and forgetting it – is working against you when you sign up for a monthly subscription.

My personal budget shows that I paid $624 in subscriptions last year, including the Costco Executive Membership, Amazon Prime, Netflix, Google Play Music, and two annual fee credit cards.

I also paid $20 per month for DAZN, the on-demand live streaming sports service that carries the NFL Sunday Ticket so I could watch my beloved Cleveland Browns. I cancelled after the Browns missed the playoffs (again).

Finally, I signed up for the Dollar Shave Club last year and paid $6.82 per month to get four stainless steel four-blade cartridges in the mail each month. It’s a great deal, and the product is awesome, but I’m not going through the blades that quickly so they’re starting to pile up. I’m on the fence about whether to continue.

My biggest subscription failure was a 30-day free trial for access to 10 images a month from Adobe Stock that turned into a $29.99 per month subscription when I forgot to cancel on time. That was in U.S. dollars too, by the way, which might as well have been $50 CDN.

Then there’s Netflix, a boon for cord-cutters everywhere, but how many of us subscribe to the on-demand streaming service in addition to an expensive monthly cable package?

I’m guilty of this. My family watches Netflix almost exclusively, yet we still pay for a basic cable package – just in case. Meanwhile our cable package is so bare bones that we couldn’t even watch the ball (any ball!) drop at midnight on New Year’s Eve (I cancelled time-shifting).

Annual subscriptions for shopping at Costco and for services like Amazon Prime or Spotify must be evaluated regularly to ensure there’s value for money spent. We shop at Costco weekly, and you can try to pry our Amazon Prime subscription from my cold-dead hands.

Another one to watch is your annual fee credit card. Do the rewards and perks justify the fee paid? Could you get the same value from a no-fee credit card? We like to travel and so we find the perks worthwhile on our annual fee cards. Your mileage may vary.

Take action: Look back at your expenses from last year and make note to get rid of those costly subscriptions that just don’t add much value to your life. And, if you haven’t done so, cancel that Columbia House subscription already!

Long before Marie Kondo had us magically tidying up our homes, keeping only the items that ‘spark joy’, the indigenous peoples of the Pacific Northwest Coast were giving it all away through an elaborate ceremony called a potlatch.

The literal word “potlatch” means “to give away,” and it was the desire of every chief to gather a large amount of property and then give a great potlatch feast in which all was distributed back to his friends and neighbouring tribes. Every present received at a potlatch had to be returned at another potlatch. A man who would not give his feast in due time would be considered as not paying his debts.

Indeed, the potlatch host would in effect challenge a guest chieftain to exceed him in his ‘power’ to give away or to destroy goods. If the guest did not return 100 percent on the gifts received and destroy even more wealth in a bigger and better bonfire, he and his people lost face and so his ‘power’ was diminished.

“The status of any given family is raised not by who has the most resources, but by who distributes the most resources. The hosts demonstrate their wealth and prominence through giving away goods.”

It was the distribution of large numbers of Hudson Bay blankets, and the destruction of valued coppers that first drew government attention to the potlatch.

Potlatching was made illegal in Canada in 1884 at the urging of missionaries and government agents who considered it “a worse than useless custom” that was seen as wasteful, unproductive, and contrary to ‘civilized values’ of accumulation. The ban lasted until 1951.

Give it away (a modern potlatch)

Modern society has an unhealthy obsession with the accumulation of “stuff”. And instead of giving it away or selling it, we store it in our basements and garages (or pay for storage units).

But research into behavioural psychology says that stuff doesn’t make us happy, that we should focus on experiences instead of buying more “things”.

That means downsizing, decluttering, and being deliberate with the number of possessions we allow into our home.

How to get started? You might not have the clout of a Kwakiutl chief to host a potlatch of your own, but today’s shared economy exists online through Craigslist, Kijiji, and Facebook local swap & buy pages.

Lethbridge hosts the Reuse Rendezvous, a city-wide free-cycling event that encourages residents to reuse unwanted items by making them available to others for free.

Of course there’s Freecycle, a grassroots, nonprofit movement of people who are giving (and getting) stuff for free in their own towns.

Millions of people are embracing minimalism and living a more simple life with fewer material possessions.

While we don’t need to burn all our possessions, quit our jobs, and sail around the world (<–oops), it couldn’t hurt to practice a little mindfulness about how much stuff we accumulate over time.

Final thoughts

My wife and I have made a conscious effort to keep the crap out of our basement and garage. We’ve been in our house for eight years and I’m proud to say we can still park our vehicles in the garage, and we’ve kept our basement from becoming a storage unit.

Are we practicing minimalists? No. But we try to purge our closets once or twice a year and donate or sell items we no longer use. We try (and mostly fail) to adopt the “one toy in, one toy out” rule for our kids. And we stay on top of the clutter before it ever gets out of hand.

We’re doing it for the kids.

We’ve witnessed our parents have to clean out our grandparents’ homes after they’ve passed away and it taking weeks, if not months, to sort through all the stuff that accumulates when you live somewhere for sixty years and never throw anything away.

So to all the chieftains out there who’ve acquired vast sums of wealth, property, and possessions, please consider a modern potlatch ceremony and give that sh!t away.

Want to know if money can truly buy happiness? How about a brutally honest and refreshing look at money and happiness? That’s what author Melissa Leong has in store with her new book called, Happy Go Money.

Melissa takes readers along her journey, from frugal beginnings growing up in Winnipeg, to covering the personal finance beat for the Financial Post, then leaving it all behind to spend more time at home only to end up with her husband in the psych ward under the crushing weight of depression.

How’s that for the opening chapter of a personal finance book?

Easy to read, yet packed with the latest studies on behavioural psychology, Melissa dives into head first into happiness research and tells readers to F*ck the Joneses, Stuff your Stuff, Invoke the Dollar Lama, and to Bullet-proof your Happiness.

I enjoyed reading the research she included on life satisfaction and day-to-day happiness – the one that says after you make roughly $75,000 per year, any increase after that actually decreases your happiness.

Then there’s the Hedonic Treadmill, our tendency to quickly return to a relative stable level of happiness despite major positive or negative life events. It’s the reason why more money or more stuff is never enough. That quick dopamine rush wears off and we return to our normal state.

Or how about the idea that the worse off our neighbours are, the happier we’ll be? That’s right, studies show that people would prefer to earn $50,000 a year while their neighbours earn $30,000 a year, rather than earn $80,000 a year while their neighbours earn $100,000 a year.

Melissa explores all of these studies and more, while applying the research to her own life as she struggled through a career change and her husband’s mental health.

What she wrote about all of that hit home: More money wouldn’t have made things better or made her any happier. But she also was grateful they had their money house in order so that when sh!t hit the fan the last thing they had to worry about was paying the bills.

I highly recommend reading Happy Go Money – it might just change your perspective about money and happiness. If not, well the book is still a smart, witty, and fun read that you won’t be able to put down.

A Happy Go Money Giveaway

With that in mind, I’d like to give away two copies of Happy Go Money to a pair of lucky readers here on Boomer & Echo. All you have to do is leave a comment below and tell me about a recent money accomplishment.

Did you pay off a nagging debt? Open up a TFSA? Reach a savings milestone? Read a personal finance blog? Let me know in the comments and you’ll be entered for a chance to win one of two copies of Happy Go Money. The contest closes Friday January 18th at 5:00 p.m. EST.

Good luck!

PS – Don’t want to wait for the contest? Buy the book on Amazon here.

This Week’s Recap:

On Monday I wrote about how my wife will save money on taxes with a Wealthsimple RRSP.

And on Thursday I shared why you should disaster proof your life with easy and affordable term life insurance.

Weekend Reading:

Speaking of Happy Go Money, blogger Nick Maguilli shares a story about Eli Whitney, the inventor of the cotton gin who got a little too greedy when trying to sell his machine across the United States.

Attention headline writers across the financial news media. Stop taking otherwise sound articles like this one and putting ridiculous titles on them such as, “Is it time to jump back into the stock market?”

This week RBC and BlackRock teamed up to create an ETF giant – RBC iShares. It’s a massive merger, but index investing proponent Dan Bortolotti is sceptical it will have any real effect on investors:

“I suppose that’s a good thing, although any IIROC-licensed RBC advisor has always been able to use ETFs if he or she was so inclined. It’s not going to turn old-school active advisors into enthusiastic proponents of low-cost indexing.”

Ben Carlson at A Wealth of Common Sense updates his favourite investment performance chart for 2018. Of note, last year was the first time in a decade that cash outperformed all other asset classes, with a 1.7 percent return. The largest decline was felt by emerging markets, which fell 15.3 percent.

Not to be outdone, Dale Roberts posted his investing year in review and says 2018 was not financial Armageddon.

Frugal Trader at Million Dollar Journey shares a financial checklist to start 2019 strong.

Here’s everything you need to know about the enhanced CPP — from how much you’ll pay to how much you’ll get.

Is cashing in RRSPs now to maximize OAS and GIS a good idea for this New Brunswick couple when they retire next year?

Mark Seed at My Own Advisor shares some little known facts about Old Age Security that you need to know.

In his latest Carrick Talks Money Video, Rob Carrick says it’s okay to spend some savings in your healthiest retirement years:

Some excellent thoughts shared here by Morgan Housel on markets and investing:

“Underestimating adaptation and reversion to the mean is the greatest cause of pessimism. If you can stick around long enough to stomach the adaptations, optimism should virtually always the default assumption.”

Mortgage brokers behaving badly again? An alleged ‘shadow’ mortgage broker was implicated in dozens of shady deals, including altered tax documents that allegedly helped bump up a janitor’s annual income from $10,881 to $77,000.

Finally, Costco is selling a giant tub of Mac & Cheese it says will last for 20 years. The 27-pound tub contains 180 servings and despite the long shelf-life customer reviews say it tastes ‘delicious’. Ummm, no thanks.

Have a great weekend, everyone!