Usually when someone reaches out looking for financial advice they want to jump right into investment selections or retirement planning. In many cases I walk them back to budgeting basics.

Specifically, how much income do you bring in and where does all your money go?

Without answering these two questions it’s nearly impossible to make any meaningful recommendations or changes to your financial plan to achieve your desired outcome or goals.

Monthly Income (more than you think)

Start with your monthly after-tax household income from every source. That means regular wages, pension or rental income, freelance earnings, and government benefits.

You can get creative here, too. For instance, you might use a cash-back credit card and earn $50 per month in cash-back rewards. That may not be taxable income (check with your accountant), but it’s income nonetheless.

Where I work we have to pay upfront for prescription drugs and other health-related spending and then apply for reimbursement through our health-spending plan. It averages out to about $200 per month. Make sure to include the reimbursements as income to offset the related spending.

Fixed Expenses (also more than you think)

Next I look at fixed expenses, which include housing costs such as rent or a mortgage payment, tenant or home insurance, property taxes or condo fees and utilities (which can vary from month to month but are pretty much unavoidable).

Transportation can be another fixed cost if you have a monthly car loan or lease payment, gas (again, variable but mostly unavoidable), car insurance and parking fees.

The cost of day care or elder care can also be treated as a fixed expense in your budget. Again, these costs are known in advance and can be budgeted for and planned. Kids’ activities, also a fixed expense. I know my kids’ piano lessons will cost $150 per month from September to June.

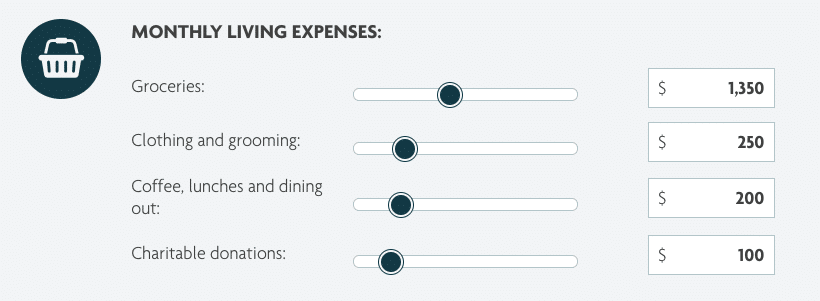

Now most people think of groceries as variable expenses, but it’s a fixed cost in our household. Here’s why:

I’ve tracked our household spending for a decade and one thing I’ve noticed is that our total grocery spend always falls somewhere between $1,250 and $1,450 per month.

Don’t get caught up in the number – we include toiletries and other sundry items in the “grocery” category. The point is it’s easy for us to budget for this category because it consistently falls within the same range every single month.

It’s a fixed expense for which I can easily budget $1,350 every month and be accurate to within +/- $100 every time.

Variable Expenses (or irregular expenses)

Variable expenses are irregular and mostly discretionary. Sure, you can decide not to buy any new clothes or put off your vehicle maintenance, but most of us do need new clothes from time to time and should take care of our vehicles to make sure they are safe and run properly.

Travel expenses, dining out and gift giving can also be considered variable expenses.

This is an important category that many soon-to-be retirees take for granted. It’s tricky to budget for because you can look at how much you’ve spent in the past but you also need to plan for the type of retirement you want and how important things like travel, recreation, dining, etc., will be to you in retirement.

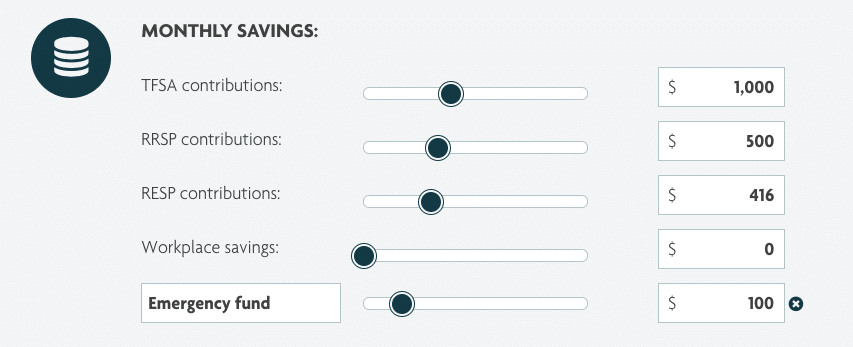

Savings Expenses (a good idea to start here)

The final step in building your budget is to include your savings expenses. That’s right, we treat savings as expenses. You wouldn’t dream of missing your mortgage or utility payment. Why should you treat your RRSP or TFSA contributions any different?

The key to good savings habits is to make your savings automatic through payroll deduction or automatic transfers from your chequing account into your savings account, RRSP and/or TFSA on the day you get paid.

I like to start with my savings goals in mind and then build my budget around those goals.

For example, I knew I wanted to catch up on unused TFSA contributions this year and save $1,000 per month. I also wanted to max out my RRSP contribution room this year, which was about $500 per month. Finally, I’d max out the kids’ RESP contributions and save $416.66 per month towards their education.

Related: RRSP Over Contribution Limit and Carry Forward Rules

So right off the top of my monthly paycheque I wanted to whisk away about $2,000 to fund my savings goals.

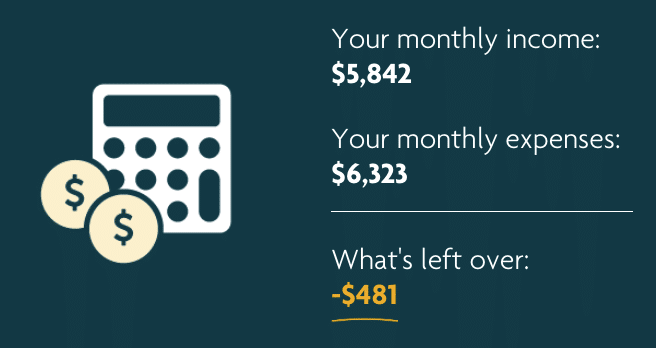

Putting it all together

At the end of this mostly painless exercise we can determine how much is left over. A large surplus means opportunities to fund new savings goals or double up on existing ones.

It might also mean you haven’t accounted for all of your expenses – something’s missing in your budget and you might need three to six months’ worth of data before you start to see the whole picture.

A shortfall, on the other hand, means an opportunity to review your budget and find ways to improve your cash flow. Perhaps your savings goals are too ambitious and need to be pared back until your debts are paid off or until that raise or promotion kicks in at work.

Or maybe there’s an opportunity for you to earn more on the side through freelance work or some other side hustle that uses your expertise.

In some cases you might just need a cold dose of reality: You’re spending too much and need to find ways to save money on your variable and fixed expenses.

Final thoughts

The right tools can make budgeting a lot more palatable and, dare I say, exciting for the average Canadian who’s looking to improve his or her finances.

This useful budget calculator at Sun Life allows you to input everything I mentioned above, toggle your monthly income and/or expenses to view different outcomes, save your results online for later, or download and print a copy for yourself.

A good budget is the starting point for your financial plan and it can help drive many of the decisions around your savings and retirement goals. Don’t neglect your budget!

One of the benefits of tracking our expenses each year is that we can identify spending trends and highlight any areas of concern. One troubling area is our overall household spending, which is on the rise. Those of you with growing families know that there’s the Consumer Price Index (CPI), which has hovered around 2.3 percent this year, and then there’s true household inflation.

Of note, our grocery spending increased 7.7 percent this year (even with a conscious effort to eat less meat). Our clothing budget stayed the same at just under $200 per month, thanks to having two girls (hand-me-downs!). We spent 8.5 percent more at restaurants this year, which is most likely a testament to our busier schedule. Perhaps related, we also spent 100 percent more on alcohol this year!

One often overlooked area that I touched on in my recent rent vs. buy post is concerning household maintenance. Last year we spent about $1,900 on this category, which broadly includes lawn care, supplies, maintenance, and improvements. This year that amount surged to $2,630, an increase of 38.5 percent.

Our house is now eight years old and showing signs of wear. First, a television dies. Then random buttons stop working on the microwave. Ducts need cleaning. Windows and doors need better sealing. The washing machine stops spinning. It all adds up.

While I have nothing specifically budgeted to replace in 2019 I know I should plan for at least $2,500 in household maintenance next year. That’s in addition to factoring in higher household inflation for food, clothing, and kids’ activities. To counter that, we’ll try to reign in our restaurant spending and aim to cook more meals at home.

All of this to say that we’ll once again have to get creative with our finances to combat rising household inflation. Cutting back only takes you so far. We need to find ways to generate more income. I explained how we do that when I shared my financial goals for 2019.

What was your personal inflation rate this year? Was it higher than CPI?

This Week’s Recap:

Earlier this week I wrote about 4 ways we keep kicking debt down the road.

I also posted a new Money Bag feature and answered questions about how best to invest $1M, the risks of labour sponsored investment funds, and compared VGRO with my two-ETF investment solution.

Promo of the Week:

We’re going to Scotland and Ireland for 32 days next summer. We saved big on accommodations in Edinburgh through the Marriott / SPG hotel rewards program. When you book five nights at a Marriott property with points, you get the fifth night free. We’re staying at the Sheraton Grand Hotel & Spa – all booked on hotel points!

How did we save up enough points to do that? The quickest way is to sign up for The Starwood Preferred Guest Credit Card from American Express (use my referral link). Both my wife and I signed up this summer and each quickly earned 50,000 Marriott Points. We combined those points (you can transfer up to 100,000 points per year to another member) and I also applied for the SPG Business Card for an additional 50,000 points, plus transferred over another 40,000 Membership Rewards points from American Express.

Armed with 200,000 Marriott points we were able to book our five night stay at the Sheraton Grand Hotel & Spa in Edinburgh. Rates at that hotel during the summer time are typically $500 CDN per night, giving us tremendous value for our rewards.

Even with the annual fees ($120 x three cards) we still got $2,500 worth of luxury accommodations for $360. By the way, SPG cardholders also receive an Annual Free Night Award after their anniversary each year.

If you’re into hotel rewards then you’ve got to become a Marriott Rewards member and use The Starwood Preferred Guest Credit Card from American Express (use my referral link) to accelerate your points earnings.

Weekend Reading:

Our intuition is usually wrong. At the World Business Forum, Daniel Kahneman explained when people can trust their intuitive judgment and when they shouldn’t.

Billionaire Warren Buffett shares some wisdom on how to boost your earnings – by honing your communication skills, both written and verbal:

“If you can’t communicate, it’s like winking at a girl in the dark — nothing happens. You can have all the brainpower in the world, but you have to be able to transmit it.”

Newly retired Michael James churned out some great articles this week:

First, he looks at when permanent life insurance makes sense (hint: rarely).

Then he dives into the popular dividend tax credit to determine whether it’s as beneficial as some say it is.

Finally, he tackles the controversial CPP expansion and picks apart the bad arguments against enhancing CPP.

Lots of talk lately about a recession and specifically how robo-advisors will fare in a market downturn. For the record, I think they’ll perform better than expected.

Today’s seniors are healthier, better educated, and more productive than ever. So let’s retire the idea of retirement.

Pre-retirees, here’s what people already retired can tell you about your future standard of living

A concerned reader wants to know if $600,000 is enough to cover retirement expenses for her 92-year-old mother after she sold the family home.

She paid the insurance premiums for 13 years, but his new spouse got the payout — until the court intervened.

Preet’s going vegan and he explains how even a small shift in your diet can add up to big savings:

A very technical yet solid explanation of deferring Old Age Security benefits past age 65.

Dale Roberts on retiring early and waiting for your spouse. The waiting is the hardest part.

Here’s a fun look at the 11 types of financial friends.

Living like a fancy Millennial, she used all the best stuff for a week and it nearly broke her.

Looking to do some financial goal setting for the New Year? Des Odjick explains why you need focus areas, goals, and tactics to make a successful plan.

A young investor asks: Can I put 90% of my investments into equities?.

Margaret wants to know how to avoid losing some of her pension if she transfers it into an RRSP at retirement.

An honest look at the gender wage gap:

“Women experience the negative effects of the pay gap from their very first paycheck to their very last Social Security check. They often need a bigger retirement nest egg, thanks to their longer life expectancy. Yet the career wage gap makes it harder for women to save as much as men do.”

Finally, here’s Frugal Trader at Million Dollar Journey explaining how his family collected $1,560 in cash back rewards this year. Well done!

Have a great weekend, everyone!

Today I’m answering reader mail for a feature I call the Money Bag. I’ll answer questions and address comments from readers on a wide range of money topics, myths, and perceptions about money. No question is off limits, so hit me up in the comments section or send me an email about all the money things you’re dying to know.

To start, we’ve got a question from Lawrence who’s looking for the best way to invest $1M and get a decent return.

Best way to invest $1M and get a decent return

“Hi Robb, I’m 62 years of age, married and both of us are retired. Our income in mostly derived from our investment portfolio. Like many people, I’m disappointed in how our investment portfolio has performed this past year. Of course the markets are largely to blame.

Our portfolio is managed by one of the big bank’s private investment counsel, for a fee of course (1.5 percent annually). Our portfolio – a mix of non-registered, RRSP, LIF and TFSA accounts – is currently valued at about $2.1M. Very recently I’ve become interested in moving about $1M of our non-registered funds away from their management and invest it myself by way of our discount brokerage account. I am looking for the best and easiest methods/vehicles to obtain a decent average return. I’m not looking for home runs – I would be quite content with an average annual return of 7-8 percent.

Is your investment portfolio still parked in two ETFs? i.e. Vanguard’s VCN (Canadian equities) and VXC (the rest of the world). If so, how has that gone for you at this stage? Are you staying the course? Would you perhaps recommend the same strategy for me with $1M?

Our advisor recently recommended that we move $1M of our non-registered funds into a segregated fund, which has a 1 percent annual management fee PLUS a separate $2,500/year active-management fee. I’m becoming weary of all these fees by wealth management firms. The returns never match expectations and “promises” made. I believe at this point that I could no worse investing on my own, if I’m very careful of course.”

Hi Lawrence, thanks for your email. I understand you’re not pleased with how your investments are performing and I wonder if fees are more to blame than market performance? Do you feel you’re getting value for the 1.5 percent fee?

Just doing the math on $2.1M and that’s $31,500 per year! Has that ever been expressed to you in dollar terms? Paying for advice can be worthwhile if you are receiving major financial planning, tax, and estate planning advice. So the question is, are you receiving that, and, is it worth $31,500 per year. I’m going to guess the answer is no.

To answer your question, my two-ETF portfolio is currently down about 2 percent on the year. I’m not panicking. This is perfectly normal. Remember, we’ve been on a nine year bull market run. I know we’re used to seeing double-digit gains in the market but that is not sustainable each and every year. Markets are volatile and we should expect to see them go down or sideways from time to time.

Since 2010 my portfolio has returned an average of 8.6 percent per year. That’s right where we’d hope to be for a long time horizon.

I would be weary of the segregated fund, which comes loaded with fees as you’ve discovered. Be careful with any advisor “promising” anything related to market performance. Nobody knows where markets are headed and so the best course of action with your investments is to stay globally diversified and keep your costs low.

Lawrence, it also sounds like you need to derive income from your portfolio and so I want to point you to this excellent article on how to generate retirement income from a portfolio of ETFs and GICs. It’s a must read for retirees. Read it all the way through, including the examples near the end about how to rebalance it all each year.

Have you looked into Nest Wealth for your stock/bond portion? They are a robo-advisor that can place you into an appropriate portfolio of index ETFs (stocks and bonds from around the world) and they charge just $80 per month. No percentage of assets. That makes them a huge bargain for investors such as yourself with more than $1M in assets to invest. If you slashed your investment costs and then hired an advice-only planner to assist with financial planning, estate, and tax planning for a one-time fee, you’d pay far less in fees, improve your investment outcomes, and get objective, unbiased advice on the rest of your financial needs.

Two ETF Portfolio vs. VGRO

Here’s Jennifer, who wants to know whether she’d be suitable for an all-equity portfolio of ETFs (like my own two-fund solution):

“Hey Robb,

I’ve just discovered you and your site from the Rational Reminder podcast. I’ve been so excited by what I’ve been learning and this fall I opened up a Questrade Account and have moved my TFSA, RRSP and RESP to this self-directed platform. Up until I’d listened to the podcast, I was on track to purchase Vanguard’s VGRO. I love the simplicity and the asset allocation even though I’m 48 and my husband is 44.

Because I’ve come to the investing table later in life, I feel like I’ve got some catching up to do. Your asset allocation of 75 percent / 25 percent in VXC/VCN seemed amazing to me. Am I crazy at my age for considering it? My husband will have a teacher’s pension, but outside of that we have a paid for condo ($600,000), but only $25,000 combined in our RRSPs and TFSAs, and $60,000 in an RESP. Come January, we plan to contribute $1,000 per month to the TFSA.

I would love any input to know if we’re on the right track, and especially if you think it’s too late in life for us to try the two-fund portfolio? I’m not opposed to rebalancing on my own, but I know VGRO is pretty effortless.”

Hey Jennifer, thanks for your email. Vanguard’s asset-allocation ETFs came around after I had already set up my two-ETF portfolio and I haven’t bothered to switch. The main reason is because I prefer to be in 100 equities at this time (I’m 39), but I’m not opposed to switching to VGRO some time down the road. (VGRO is 80 percent stocks and 20 percent bonds).

When in doubt, I’d go with the simple solution and concentrate more on contributing as much as you can. Catch up on your investments by increasing your savings rate, not by trying to eke out an extra bit of return. Trust me, once you go down that path it’s a slippery slope to constantly second guess yourself and tinker with your portfolio far too often.

In fact, when you look at the 20-year returns of these various model portfolios it’s fair to wonder why anyone would go with a 100% equities portfolio when the returns of a more balanced portfolio are nearly identical with way less volatility:

*Update: Vanguard later introduced a 100% equity allocation ETF. I’ve now made the switch to VEQT in my own portfolio.

High Cost Funds in Saskatchewan

Here’s a question from Jonathan about investing in labour sponsored investment funds in Saskatchewan. Take it away, Jonathan:

“Hi Robb, I was recently talking with a family member about retirement savings plans and came across a Saskatchewan based firm called Golden Opportunities Fund (a family member was maxing out contributions into this) and also another called Sask Works Venture Fund. These funds are subsidized by government tax credits and support local Sask companies. I thought this might be interesting as its a significant up front tax credit that I can re-invest into something else.

Once I started to dig into the funds, I was quickly angered by crazy fees and 8 year commitment terms for the funds. The funds are extremely under diversified and high concentrated into select companies. One fund invests almost 19% into Aurora Cannabis, and these are supposed to be retirement plans for people!

As you can imagine, my stomach felt sick for my family member to be invested into this fund as a retirement plan. Governments also supports these funds with tax credits which I think is doing a disservice to investors.

My question to you is have you written a blog post in the past about these or know of anyone who has? I have searched but not come up with very much to show my family member another opinion besides the fund sales persons promise of quick cash back and a “retirement savings” plan.”

Hi Jonathan, thanks for your email. I’m glad you’re looking out for your family members. I had not heard of the Golden Opportunity Fund but it looks like a classic Labour Sponsored Investment Fund. It’s legitimate, but highly controversial and the program has been eliminated in some provinces, although obviously not in Saskatchewan. It was a way for governments to assist with riskier venture capital like mining and oil & gas exploration.

When you contribute up to $5,000 in a year you’ll receive a federal tax credit of $750 and a provincial tax credit of $875. As you discovered, your money is tied up for eight years. Selling early means forfeiting those tax credits.

Here’s a good explainer of the risks and costs associated with labour sponsored funds.

This particular fund has only returned 2.9 percent annually since inception in 1999. Not exactly the type of returns you’d be looking for from such a risky venture, and certainly not something I’d want to sink any sizeable amount into, let alone the bulk of my retirement savings!

I’d think of this sector more like the CoPower Green Bonds that I blogged about earlier this year; something to maybe put a small portion of your portfolio towards if you believe in supporting local businesses or whatever the case may be.

The bottom line: Labour sponsored investment funds do provide some tax advantages but not without several risks. This is definitely not a retirement plan, or a quick cash-back scheme at all.