There are some fees we just love to hate and so we try to avoid them at all costs. Whether it’s bank fees, credit card annual fees, or late fees at the library, the idea of voluntarily paying a fee is anathema to anyone with a frugal mind.

But some fees can be worthwhile if they can save you time and money in the end.

What makes a fee worth paying? To start, we want to get good value for our money, but that’s just marketing talk if the value can’t be measured in dollars saved. We might pay more for peace of mind, but it’s hard to put a price tag on how well we sleep at night.

Convenience comes into play – if you value your time then you’ll pay a little more to save it. There are also tangible benefits to getting impartial, unbiased advice before you make a major purchase or life decision, but that advice won’t come free.

Worthwhile Fees to Pay

When it comes to worthwhile fees, look no further than the legions of loyal shoppers who pay for the privilege to shop at Costco. More than 10 million Canadians hand over $60 per year to shop at the popular wholesale club and take advantage of bulk pricing and several products unique to the store. Is it worth the money? The company says nearly 90 percent of its members renew each year.

Related: Is the Costco Executive Membership Worth It?

Another prime example comes from Amazon. For just $79 annually, Amazon Prime members get free two-day shipping, plus access to Prime Video and Prime Music. Prime members also get exclusive discounts, and there’s a 30-day free trial to test it out for yourself.

Annual fee credit cards can be worth the money if you earn enough rewards to offset the fees and then some. A comparison website like CreditCardGenius.ca shows that when your monthly credit card spend totals $2,000, including $600 on groceries and $200 on gas, you’ll earn up to $250 more cash back rewards using the Scotia Momentum Visa Infinite than you would using the top no-fee cash back credit card, and that’s even after subtracting the Scotia card’s $99 annual fee.

What about peace of mind? More than six million people carry a CAA membership and for a $70 annual fee they can get immediate roadside assistance anywhere in North America.

Travel insurance is also a must if you visit the United States or abroad. You can get emergency medical coverage for as little as $25, which is a drop in the bucket compared to a hospital visit while you’re on vacation.

Frequent travellers to the U.S. might appreciate a way to expedite lengthy airport line-ups. A NEXUS pass might just be the ticket. The program allows members to conveniently bypass pre-border security screening at major airports by going through a designated security line. The NEXUS fee is just $50, and is valid for five years.

Sticker shock might be the appropriate term when you first see the fees charged for professional services, such as for tax advice, drafting a will, or creating a financial plan. These broader services can cost upwards of $1,000 or more to obtain, but you’ll be in good hands with the right professional help.

Paying upfront for financial advice seems odd at first blush, but more and more Canadians are turning to fee-only planners to get unbiased advice, not just about their investments but about their overall financial health. You might pay $150 to $250 per hour, but you’ll get a comprehensive and unbiased financial plan without the pushy product sales.

It can also make sense to pay a fee for unbiased advice before you buy an expensive product. A CARFAX report, for example, gives you detailed information about a vehicles history that can help you when deciding to buy a used car. One report costs $39.95, but the information it provides could save you from buying a lemon.

Consumer Reports is a non-profit organization and another good source of information for saving money and protecting consumers. A subscription to the magazine costs just $30 per year, and for $55 per year you get full access to the website, www.consumerreports.org.

Streaming music through apps like Spotify, Apple Music, or Google Play will cost $9.99 per month. The upside is an exhaustive catalogue of music to be enjoyed wherever you are, from any of your devices.

Finally, a list of worthwhile fees wouldn’t be complete without a shout out to Netflix. More than 13.3 million Canadians subscribed to Netflix in 2018. Its standard plan now costs $13.99 per month, but by investing heavily in content, including originals such as The Crown and Stranger Things, Netflix keeps its members coming back often to binge on the next new series.

Final thoughts

Some fees just can’t be avoided, but that doesn’t mean every fee is designed to rip you off. You can feel good about paying fees when they provide enough benefit to justify the cost.

Whether it saves you time, gives you peace of mind, or actually saves you money in the long run – in some cases you’re better off handing over the money.

Usually when someone reaches out looking for financial advice they want to jump right into investment selections or retirement planning. In many cases I walk them back to budgeting basics.

Specifically, how much income do you bring in and where does all your money go?

Without answering these two questions it’s nearly impossible to make any meaningful recommendations or changes to your financial plan to achieve your desired outcome or goals.

Monthly Income (more than you think)

Start with your monthly after-tax household income from every source. That means regular wages, pension or rental income, freelance earnings, and government benefits.

You can get creative here, too. For instance, you might use a cash-back credit card and earn $50 per month in cash-back rewards. That may not be taxable income (check with your accountant), but it’s income nonetheless.

Where I work we have to pay upfront for prescription drugs and other health-related spending and then apply for reimbursement through our health-spending plan. It averages out to about $200 per month. Make sure to include the reimbursements as income to offset the related spending.

Fixed Expenses (also more than you think)

Next I look at fixed expenses, which include housing costs such as rent or a mortgage payment, tenant or home insurance, property taxes or condo fees and utilities (which can vary from month to month but are pretty much unavoidable).

Transportation can be another fixed cost if you have a monthly car loan or lease payment, gas (again, variable but mostly unavoidable), car insurance and parking fees.

The cost of day care or elder care can also be treated as a fixed expense in your budget. Again, these costs are known in advance and can be budgeted for and planned. Kids’ activities, also a fixed expense. I know my kids’ piano lessons will cost $150 per month from September to June.

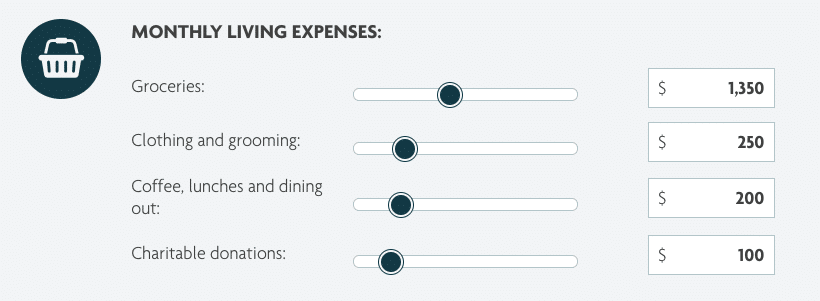

Now most people think of groceries as variable expenses, but it’s a fixed cost in our household. Here’s why:

I’ve tracked our household spending for a decade and one thing I’ve noticed is that our total grocery spend always falls somewhere between $1,250 and $1,450 per month.

Don’t get caught up in the number – we include toiletries and other sundry items in the “grocery” category. The point is it’s easy for us to budget for this category because it consistently falls within the same range every single month.

It’s a fixed expense for which I can easily budget $1,350 every month and be accurate to within +/- $100 every time.

Variable Expenses (or irregular expenses)

Variable expenses are irregular and mostly discretionary. Sure, you can decide not to buy any new clothes or put off your vehicle maintenance, but most of us do need new clothes from time to time and should take care of our vehicles to make sure they are safe and run properly.

Travel expenses, dining out and gift giving can also be considered variable expenses.

This is an important category that many soon-to-be retirees take for granted. It’s tricky to budget for because you can look at how much you’ve spent in the past but you also need to plan for the type of retirement you want and how important things like travel, recreation, dining, etc., will be to you in retirement.

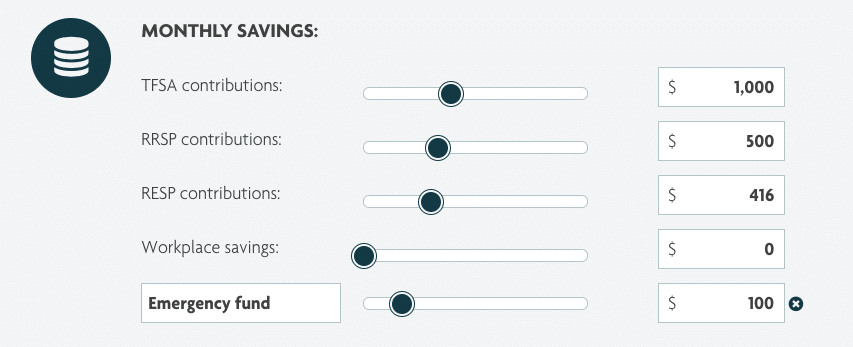

Savings Expenses (a good idea to start here)

The final step in building your budget is to include your savings expenses. That’s right, we treat savings as expenses. You wouldn’t dream of missing your mortgage or utility payment. Why should you treat your RRSP or TFSA contributions any different?

The key to good savings habits is to make your savings automatic through payroll deduction or automatic transfers from your chequing account into your savings account, RRSP and/or TFSA on the day you get paid.

I like to start with my savings goals in mind and then build my budget around those goals.

For example, I knew I wanted to catch up on unused TFSA contributions this year and save $1,000 per month. I also wanted to max out my RRSP contribution room this year, which was about $500 per month. Finally, I’d max out the kids’ RESP contributions and save $416.66 per month towards their education.

Related: RRSP Over Contribution Limit and Carry Forward Rules

So right off the top of my monthly paycheque I wanted to whisk away about $2,000 to fund my savings goals.

Putting it all together

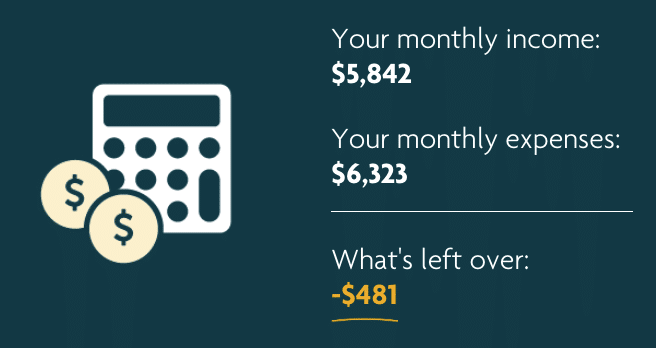

At the end of this mostly painless exercise we can determine how much is left over. A large surplus means opportunities to fund new savings goals or double up on existing ones.

It might also mean you haven’t accounted for all of your expenses – something’s missing in your budget and you might need three to six months’ worth of data before you start to see the whole picture.

A shortfall, on the other hand, means an opportunity to review your budget and find ways to improve your cash flow. Perhaps your savings goals are too ambitious and need to be pared back until your debts are paid off or until that raise or promotion kicks in at work.

Or maybe there’s an opportunity for you to earn more on the side through freelance work or some other side hustle that uses your expertise.

In some cases you might just need a cold dose of reality: You’re spending too much and need to find ways to save money on your variable and fixed expenses.

Final thoughts

The right tools can make budgeting a lot more palatable and, dare I say, exciting for the average Canadian who’s looking to improve his or her finances.

This useful budget calculator at Sun Life allows you to input everything I mentioned above, toggle your monthly income and/or expenses to view different outcomes, save your results online for later, or download and print a copy for yourself.

A good budget is the starting point for your financial plan and it can help drive many of the decisions around your savings and retirement goals. Don’t neglect your budget!

One of the benefits of tracking our expenses each year is that we can identify spending trends and highlight any areas of concern. One troubling area is our overall household spending, which is on the rise. Those of you with growing families know that there’s the Consumer Price Index (CPI), which has hovered around 2.3 percent this year, and then there’s true household inflation.

Of note, our grocery spending increased 7.7 percent this year (even with a conscious effort to eat less meat). Our clothing budget stayed the same at just under $200 per month, thanks to having two girls (hand-me-downs!). We spent 8.5 percent more at restaurants this year, which is most likely a testament to our busier schedule. Perhaps related, we also spent 100 percent more on alcohol this year!

One often overlooked area that I touched on in my recent rent vs. buy post is concerning household maintenance. Last year we spent about $1,900 on this category, which broadly includes lawn care, supplies, maintenance, and improvements. This year that amount surged to $2,630, an increase of 38.5 percent.

Our house is now eight years old and showing signs of wear. First, a television dies. Then random buttons stop working on the microwave. Ducts need cleaning. Windows and doors need better sealing. The washing machine stops spinning. It all adds up.

While I have nothing specifically budgeted to replace in 2019 I know I should plan for at least $2,500 in household maintenance next year. That’s in addition to factoring in higher household inflation for food, clothing, and kids’ activities. To counter that, we’ll try to reign in our restaurant spending and aim to cook more meals at home.

All of this to say that we’ll once again have to get creative with our finances to combat rising household inflation. Cutting back only takes you so far. We need to find ways to generate more income. I explained how we do that when I shared my financial goals for 2019.

What was your personal inflation rate this year? Was it higher than CPI?

This Week’s Recap:

Earlier this week I wrote about 4 ways we keep kicking debt down the road.

I also posted a new Money Bag feature and answered questions about how best to invest $1M, the risks of labour sponsored investment funds, and compared VGRO with my two-ETF investment solution.

Promo of the Week:

We’re going to Scotland and Ireland for 32 days next summer. We saved big on accommodations in Edinburgh through the Marriott / SPG hotel rewards program. When you book five nights at a Marriott property with points, you get the fifth night free. We’re staying at the Sheraton Grand Hotel & Spa – all booked on hotel points!

How did we save up enough points to do that? The quickest way is to sign up for The Starwood Preferred Guest Credit Card from American Express (use my referral link). Both my wife and I signed up this summer and each quickly earned 50,000 Marriott Points. We combined those points (you can transfer up to 100,000 points per year to another member) and I also applied for the SPG Business Card for an additional 50,000 points, plus transferred over another 40,000 Membership Rewards points from American Express.

Armed with 200,000 Marriott points we were able to book our five night stay at the Sheraton Grand Hotel & Spa in Edinburgh. Rates at that hotel during the summer time are typically $500 CDN per night, giving us tremendous value for our rewards.

Even with the annual fees ($120 x three cards) we still got $2,500 worth of luxury accommodations for $360. By the way, SPG cardholders also receive an Annual Free Night Award after their anniversary each year.

If you’re into hotel rewards then you’ve got to become a Marriott Rewards member and use The Starwood Preferred Guest Credit Card from American Express (use my referral link) to accelerate your points earnings.

Weekend Reading:

Our intuition is usually wrong. At the World Business Forum, Daniel Kahneman explained when people can trust their intuitive judgment and when they shouldn’t.

Billionaire Warren Buffett shares some wisdom on how to boost your earnings – by honing your communication skills, both written and verbal:

“If you can’t communicate, it’s like winking at a girl in the dark — nothing happens. You can have all the brainpower in the world, but you have to be able to transmit it.”

Newly retired Michael James churned out some great articles this week:

First, he looks at when permanent life insurance makes sense (hint: rarely).

Then he dives into the popular dividend tax credit to determine whether it’s as beneficial as some say it is.

Finally, he tackles the controversial CPP expansion and picks apart the bad arguments against enhancing CPP.

Lots of talk lately about a recession and specifically how robo-advisors will fare in a market downturn. For the record, I think they’ll perform better than expected.

Today’s seniors are healthier, better educated, and more productive than ever. So let’s retire the idea of retirement.

Pre-retirees, here’s what people already retired can tell you about your future standard of living

A concerned reader wants to know if $600,000 is enough to cover retirement expenses for her 92-year-old mother after she sold the family home.

She paid the insurance premiums for 13 years, but his new spouse got the payout — until the court intervened.

Preet’s going vegan and he explains how even a small shift in your diet can add up to big savings:

A very technical yet solid explanation of deferring Old Age Security benefits past age 65.

Dale Roberts on retiring early and waiting for your spouse. The waiting is the hardest part.

Here’s a fun look at the 11 types of financial friends.

Living like a fancy Millennial, she used all the best stuff for a week and it nearly broke her.

Looking to do some financial goal setting for the New Year? Des Odjick explains why you need focus areas, goals, and tactics to make a successful plan.

A young investor asks: Can I put 90% of my investments into equities?.

Margaret wants to know how to avoid losing some of her pension if she transfers it into an RRSP at retirement.

An honest look at the gender wage gap:

“Women experience the negative effects of the pay gap from their very first paycheck to their very last Social Security check. They often need a bigger retirement nest egg, thanks to their longer life expectancy. Yet the career wage gap makes it harder for women to save as much as men do.”

Finally, here’s Frugal Trader at Million Dollar Journey explaining how his family collected $1,560 in cash back rewards this year. Well done!

Have a great weekend, everyone!