The month of October was not kind to investors. A volatile stock market erased all of 2018’s gains and then some. My own portfolio plunged 5.72 percent in October after being up 4.73 percent from January to September. Time to panic? Not a chance.

In yet another example of why it’s best to ignore the headlines and stick with your plan (or why I say investors would be better off taking a Rip Van Winkle like 20 year nap) the market quickly returned all of those losses in just eight trading days.

Investors who panicked at the bottom of that dip locked in losses of nearly six percent, while investors who rode out the stock market volatility saw their portfolios get back to even.

A chart showing market returns over a few days, weeks, or even months can look like a stomach-churning rollercoaster. But as the months turn to years, and the years turn to decades, those returns smooth out and trend upwards. Yesterday’s headlines become ancient history, and ‘worst days ever‘ for the stock market become tiny blips on the radar over the long term.

The point is not to panic when markets get rocky. If your investing plan has a long term focus then it’s best to ignore the daily headlines and stick to your plan.

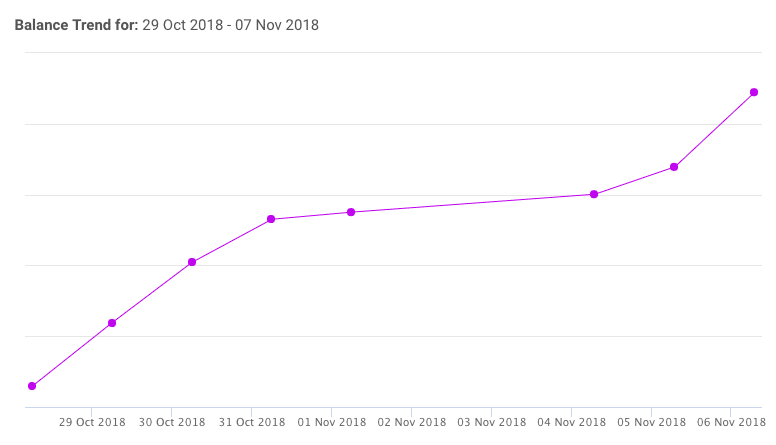

Here’s the power of ignoring the day-to-day market fluctuations and headlines, and sticking to your investing plan. Portfolio balance as of Oct 8: $231k. Balance as of Nov 8: $232k. Ignored in between: a low of $214k. pic.twitter.com/lBl4Xna9Va

— Boomer and Echo (@BoomerandEcho) November 8, 2018

This Week’s Recap:

On Wednesday I wrote about why past performance is not a good predictor of future investment returns. In fact, costs are a better predictor of returns.

In light of CBC’s recent coverage of the pitfalls of credit card insurance I looked at four big rip-offs that consumers should avoid.

Promo of the Week:

I’ve highlighted this before but if you have some upcoming spend planned for the holidays then this is an excellent opportunity to earn up to $200 cash back on your holiday spending.

That’s right, when you apply and get approved for the Scotia Momentum Visa Infinite Card you’ll earn an incredible 10 percent back on everyday purchases for the first three months, up to $2,000 in total purchases. Plus, your first-year annual fee is waived. This is a limited time offer so make sure to take advantage of it soon.

Weekend Reading:

The surprising retirement goal that 41 percent of Americans have? It’s to own a vacation home.

Will baby boomers destroy the stock market as they retire en masse? Ben Carlson examines some interesting trends and time lapses.

How Shane Parrish, a former Canadian spy, helps Wall Street mavens think smarter:

“Every world-class investor is questioning right now how they can improve,” he said. “So, in a machine-driven age where everything is driven by speed, perhaps the edge is judgment, time and perspective.”

Jonathan Chevreau highlights three online programs to help plan out your finances in retirement.

Personal finance 101: Some Canadian universities are offering practical personal finance courses.

Studies show that as we age, our brain becomes less able to detect fraud. Here’s a thoughtful post on how to safeguard your finances and protect your retirement savings.

Jason Heath explains how to avoid RRSP tax on your estate when you die.

Michael James has an excellent post explaining the value of delaying CPP and OAS until age 70. More people need to hear this message.

Last week I shared the “new rules” of personal finance. Million Dollar Journey blogger Frugal Trader looks at how these rules apply to his thinking on personal finance matters.

Dale Roberts explains the many lessons learned from a chart detailing the returns history of Tangerine’s five investment portfolios.

Finally, here’s Michael James again on whether it makes sense to hold U.S.-listed ETFs to save on MER and foreign withholding taxes. I’ve been thinking a lot about this lately and how it applies to my own two-ETF portfolio, in which I’ve chosen simplicity over cost savings. I’ll soon be at the point where the pendulum will swing towards cost savings.

Have a great weekend, everyone!

CBC Go Public continues to do excellent investigative reporting and this week they caught banks behaving badly again, this time misleading and upselling customers on pricey credit card insurance. Known as balance protection insurance, this product charges a hefty premium (typically around 99 cents per $100 balance) to “protect” cardholders from missed payments as a result of job loss, illness, disability, or death.

But as 72-year-old Jolante Groves found out, the coverage comes with so many exclusions that it can be difficult to make a successful claim. Jolante’s husband George suffered a stroke in February that left him incapacitated and unable to make payments on his outstanding credit card balance. The card issuer, Canadian Tire, demanded payment and refused to allow Jolante to make an insurance claim on her husband’s behalf because the card was in his name alone.

CBC’s Marketplace took their hidden cameras into some of Canada’s big banks in Toronto to investigate how bank employees marketed balance protection insurance when a customer signed up for a new credit card. If you’ve seen Marketplace’s or Go Public’s previous bank investigations before then the results will shock but not surprise you.

A BMO employee offered balance protection insurance but when questioned about it seemed to have little grasp of the product she was selling. A Scotia employee inaccurately claimed the coverage would pay off an entire credit card balance if someone lost their job. And a CIBC employee added balance protection to a credit card before the customer had a chance to decline the insurance.

That was also my experience with CIBC this summer when I applied in person for the CIBC Aventura Visa Infinite card. We never discussed balance protection at all. Several weeks later, before receiving the credit card, I got a letter from CIBC and Sun Alliance Insurance describing the balance protection coverage already enabled on my card. I immediately called to cancel it, but it made me wonder if this was common practice at CIBC.

CIBC also added balance protection insurance to my Aventura card without my permission. Shameful practice. https://t.co/dEi1VPFf5T

— Boomer and Echo (@BoomerandEcho) November 6, 2018

Several anonymous bank customer service representatives revealed to CBC how they are under pressure to make sales targets and sell balance protection insurance to everyone who takes out a credit card. They’re misleading clients and often signing them up for the coverage without their knowledge.

Balance protection insurance is part of a list of useless products that are designed to enrich banks and dupe unsuspecting customers. It should be banned along with other insidious products such as mortgage life insurance, extended warranties, and deferred sales charges.

This Week’s Recap:

This week I compared the best high interest savings account options at Canada’s big banks, online banks, and credit unions.

Over on Rewards Cards Canada I described my CIBC Aventura Card adventure in further detail.

Weekend Reading:

Is there a problem with the way we envision retirement? An MIT study’s results were surprising and a little concerning.

The “Financial Independence, Retire Early” advocates are using assumptions about future market returns that are unrealistic.

A group of younger workers, devotees of the FIRE movement, are seeking ways to duck mistakes made by prior generations. (Wall Street Journal subscribers)

You’ve heard of stocks for the long run, but there are 30-year periods where bonds have outperformed stocks. Michael James answers the question of what we do with that information.

The Wealthy Barber David Chilton has partnered with RBC Wealth Management to raise awareness about estate planning options – specifically the idea of taking advantage of corporate executors:

“I am a big believer in the benefits of corporate executorship. In fact, I refuse to take on the executor role for even my closest friends’ wills. If you’re wondering why, you’ve probably never been an executor,” says Chilton.

If you have both a mortgage and an investment portfolio you might have wondered if it makes sense to use some of your investments to pay off your mortgage. Ben Felix explains what’s optimal and realistic in his latest common sense investing video:

Rob Carrick says this is a definitive sign you have overborrowed and owe too much.

Surprisingly, Carrick then makes the case for 30-year mortgages as a financial stress reliever for new home buyers. There is a sensible argument inside:

“Here’s a compromise if you’re gagging on the idea of paying that extra interest: Set up the mortgage with a 30-year amortization, but make extra payments so that you end up paying the amount you would have if you went with 25 years.”

Michael Batnick explains that where the market goes in your first ten years can have a disproportionate impact on how you think about investing for the remainder of your life.

Finally, one of my favourites – read Martin Short’s nine categories for self evaluation.

Have a great weekend, everyone!

The past 10 years have been a lost decade for savers as interest rates plummeted and stayed at historic lows. A so-called high interest savings account at one of Canada’s big banks pay next to nothing for interest. Meanwhile those looking for higher rates on their deposits have to chase short-term promotional offers at online banks and out-of-province credit unions just to stay ahead of inflation.

Luckily the tide is starting to turn thanks to the Bank of Canada raising its key interest rate on five occasions in the past 15 months. While debtors bemoan the 1.25 percent increase over that time, savers are cheering for higher rates on their deposits.

High Interest Savings Account Comparison

It had been some time since I surveyed the market to compare high interest savings accounts rates. What I found was much of the same from Canada’s big banks, whose best rates range from a paltry 0.5 percent to 1.2 percent on a high interest savings account.

RBC’s eSavings account is easily the best of the bunch for everyday deposits, paying a decent 1.2 percent on every dollar with no monthly fees or minimum deposits required. The account also includes one free ATM cash withdrawal per month.

| Bank | Account | Interest rate % |

| RBC | High Interest eSavings Account | 1.20 |

| Scotiabank | Momentum Plus Savings Account | 1.05 |

| CIBC | eAdvantage Savings Account | 1.05* |

| BMO | Smart Saver | 0.80 |

| TD | High Interest Savings Account | 0.50* |

* $5,000 minimum balance required

In the middle of the rate pack you’ll find online banking pioneers Tangerine and Simplii Financial (formerly PC Financial), plus other household names such as Manulife and Canadian Tire Bank.

At the top of the online competitors we have EQ Bank, which pays a healthy 2.30%* everyday interest rate on its savings deposits. The EQ Bank Savings Plus Account comes with no monthly fees, no minimum balance, and acts as a chequing account with unlimited transactions, including free bill payments and unlimited free Interac e-Transfers® per month.

| Bank | Account | Interest rate % |

| EQ Bank | EQ Bank Savings Plus Account | 2.30* |

| Alterna Bank | High Interest eSavings Account | 2.25 |

| Canadian Tire | High Interest Savings Account | 1.50 |

| Manulife Bank | Advantage Account | 1.40 |

| Simplii Financial | High Interest Savings Account | 1.25 |

| Tangerine | Savings Account | 1.25 |

Finally, I’d be remiss not to include a section on credit unions, which for years have offered some of the highest interest rates on savings accounts in the country. The trouble is that savers often need to look beyond their provincial borders to take advantage of these higher rates.

Indeed, some of the best interest rates today are offered by little known Manitoba credit unions. Topping the list (and the country) is Manitoba’s largest credit union, Steinbach, which pays an incredible 2.65 percent on its regular savings account. Not too far behind is Winnipeg’s AcceleRate Financial, which pays 2.35 percent on its high interest savings account.

The Deposit Guarantee Corporation of Manitoba guarantees all deposits. Canadian residents outside of Manitoba can open an account with a Manitoba credit union by becoming a member and providing additional supporting documentation with their application.

| Manitoba Credit Union | Account | Interest rate % |

| Steinbach | Regular Savings | 2.65 |

| AcceleRate | High Interest Savings | 2.35 |

| Achieva | Daily Interest Savings | 2.15 |

| Outlook | High Interest Savings Account | 2.15 |

| Implicity | High Interest Savings Account | 2.15 |

Ontario also has its share of credit unions that offer competitive rates on savings accounts among other products. Pacing the field is Alterna Bank, an online offshoot of Alterna Savings, which has 33 locations across Ontario. Alterna offers a high interest eSavings account at 2.25 percent.

| Ontario Credit Union | Account | Interest rate % |

| Alterna | High Interest eSavings | 2.25 |

| Meridian | High Interest Savings | 1.50 |

| IC Savings | Investment Savings | 1.25 |

The verdict

Many of the above listed banks, online banks, and credit unions typically offer promotional interest rates upwards of 3 percent or more for short periods of time. A savvy customer with the time and inclination could stay ahead of the curve by moving their savings around every few months.

A less complicated solution is to park your money with a bank that consistently offers an everyday high interest rate at or near the top of the market with no hassles. For my money today, that’s the EQ Bank Savings Plus Account at 2.30% interest*.

*Interest is calculated daily on the total closing balance and paid monthly. Rates are per annum and subject to change without notice.