The past 10 years have been a lost decade for savers as interest rates plummeted and stayed at historic lows. A so-called high interest savings account at one of Canada’s big banks pay next to nothing for interest. Meanwhile those looking for higher rates on their deposits have to chase short-term promotional offers at online banks and out-of-province credit unions just to stay ahead of inflation.

Luckily the tide is starting to turn thanks to the Bank of Canada raising its key interest rate on five occasions in the past 15 months. While debtors bemoan the 1.25 percent increase over that time, savers are cheering for higher rates on their deposits.

High Interest Savings Account Comparison

It had been some time since I surveyed the market to compare high interest savings accounts rates. What I found was much of the same from Canada’s big banks, whose best rates range from a paltry 0.5 percent to 1.2 percent on a high interest savings account.

RBC’s eSavings account is easily the best of the bunch for everyday deposits, paying a decent 1.2 percent on every dollar with no monthly fees or minimum deposits required. The account also includes one free ATM cash withdrawal per month.

| Bank | Account | Interest rate % |

| RBC | High Interest eSavings Account | 1.20 |

| Scotiabank | Momentum Plus Savings Account | 1.05 |

| CIBC | eAdvantage Savings Account | 1.05* |

| BMO | Smart Saver | 0.80 |

| TD | High Interest Savings Account | 0.50* |

* $5,000 minimum balance required

In the middle of the rate pack you’ll find online banking pioneers Tangerine and Simplii Financial (formerly PC Financial), plus other household names such as Manulife and Canadian Tire Bank.

At the top of the online competitors we have EQ Bank, which pays a healthy 2.30%* everyday interest rate on its savings deposits. The EQ Bank Savings Plus Account comes with no monthly fees, no minimum balance, and acts as a chequing account with unlimited transactions, including free bill payments and unlimited free Interac e-Transfers® per month.

| Bank | Account | Interest rate % |

| EQ Bank | EQ Bank Savings Plus Account | 2.30* |

| Alterna Bank | High Interest eSavings Account | 2.25 |

| Canadian Tire | High Interest Savings Account | 1.50 |

| Manulife Bank | Advantage Account | 1.40 |

| Simplii Financial | High Interest Savings Account | 1.25 |

| Tangerine | Savings Account | 1.25 |

Finally, I’d be remiss not to include a section on credit unions, which for years have offered some of the highest interest rates on savings accounts in the country. The trouble is that savers often need to look beyond their provincial borders to take advantage of these higher rates.

Indeed, some of the best interest rates today are offered by little known Manitoba credit unions. Topping the list (and the country) is Manitoba’s largest credit union, Steinbach, which pays an incredible 2.65 percent on its regular savings account. Not too far behind is Winnipeg’s AcceleRate Financial, which pays 2.35 percent on its high interest savings account.

The Deposit Guarantee Corporation of Manitoba guarantees all deposits. Canadian residents outside of Manitoba can open an account with a Manitoba credit union by becoming a member and providing additional supporting documentation with their application.

| Manitoba Credit Union | Account | Interest rate % |

| Steinbach | Regular Savings | 2.65 |

| AcceleRate | High Interest Savings | 2.35 |

| Achieva | Daily Interest Savings | 2.15 |

| Outlook | High Interest Savings Account | 2.15 |

| Implicity | High Interest Savings Account | 2.15 |

Ontario also has its share of credit unions that offer competitive rates on savings accounts among other products. Pacing the field is Alterna Bank, an online offshoot of Alterna Savings, which has 33 locations across Ontario. Alterna offers a high interest eSavings account at 2.25 percent.

| Ontario Credit Union | Account | Interest rate % |

| Alterna | High Interest eSavings | 2.25 |

| Meridian | High Interest Savings | 1.50 |

| IC Savings | Investment Savings | 1.25 |

The verdict

Many of the above listed banks, online banks, and credit unions typically offer promotional interest rates upwards of 3 percent or more for short periods of time. A savvy customer with the time and inclination could stay ahead of the curve by moving their savings around every few months.

A less complicated solution is to park your money with a bank that consistently offers an everyday high interest rate at or near the top of the market with no hassles. For my money today, that’s the EQ Bank Savings Plus Account at 2.30% interest*.

*Interest is calculated daily on the total closing balance and paid monthly. Rates are per annum and subject to change without notice.

I was caught by surprise when Daylight Saving Time ended this weekend but I’m thankful for the gift of time with an extra hour I didn’t know I had Sunday morning. Many jurisdictions have considered abandoning Daylight Saving Time, including the European Union. The EU Commission surveyed 4.6 million people and found that 84 percent called for ending the spring and autumn clock change.

That prompted the EU to do away with twice-yearly clock changes as of October 2019 and it has given member states until April 2019 to decide whether they’d permanently remain on winter or summer time.

Various parts of Canada and the United States do not observe Daylight Saving Time, including:

- Most of the province of Saskatchewan

- Peace River Regional District, B.C.

- Fort Nelson, B.C.

- Creston, B.C.

- Pickle Lake, Ont.

- New Osnaburgh, Ont.

- Atikokan, Ont.

- Quebec’s north shore

- Arizona

- Hawaii

I don’t have a strong opinion about observing Daylight Saving Time or not, but I feel like everyone should be on the same page and either adopt it or not.

I had a hard enough time last month trying to schedule a conference call in MST with someone in EST while I was travelling in PST. My Outlook calendar was just as confused as me and the poor guy from Ontario. I can’t imagine the chaos when more (but not all) provinces and countries decide to end Daylight Saving Time.

This Week’s Recap:

On Monday we had a guest post from Dale Roberts at Cut The Crap Investing who shared some year-end tax traps to avoid for mutual fund investors.

And on Wednesday I reviewed CoPower Green Bonds and their 6-year bond that pays a fixed return of 5 percent.

Next week I’ll have a piece on Financial Literacy Month and also look at the best options for high interest savings accounts in Canada.

Promo of the Week:

Here’s a great one. The cash back king, Scotia Momentum Visa Infinite, is offering an incredible 10%(!) cash back on everyday purchases for three months (up to $200 earned), plus your first year annual fee waived.

Best to apply for this one through Great Canadian Rebates and earn an additional $55 in cash back rebates from GCR. That’s a total of $255 in cash back for free if you can reach $2,000 in spending in three months.

Speaking of cash back, don’t forget to stop by Ebates.ca and Great Canadian Rebates this holiday season so you can earn cash back bonuses and discounts on your online shopping.

Weekend Reading:

Questrade rebranded its robo-advisor platform from Portfolio IQ to Questwealth and in the process dropped its management fee to an industry leading 0.25 percent. That all sounds great, but I’m skeptical of Questrade’s insistence on using actively managed investment strategies in its portfolios.

Some old pieces of financial wisdom aren’t as helpful as they used to be. Here are the new rules of personal finance.

The Bank of Canada wants rates back to normal – here’s what that means for your mortgage, line of credit.

Squawkfox Kerry Taylor says debt builds when we turn to thinking instead of doing.

Millionaire Teacher Andrew Hallam says that when stocks drop, the biggest threat is the person you face in the mirror:

“Plenty of people fear stock market drops, especially new investors. When stocks fall, many people sell. Plenty of others cease to add fresh money. They stop contributing to their investments. They choose to wait until things return to normal. But this is as crazy as eating sand for breakfast– because market drops are normal.”

Jason Heath shares how single seniors can plan for retirement.

Michael James on Money reviews the excellent Fred Vettese book, Retirement Income for Life.

Think saving for old age can’t be fun? Try making a game of it.

Jamie Golombek explains how to ensure you take advantage of all the tax benefits that come with being a landlord.

Consumer advocate Ellen Roseman says getting repairs made under warranty shouldn’t be so draining.

Dale Roberts also looks at CoPower Green Bonds. Changing your portfolio one LED light bulb at a time: Getting your investments into the green.

Finally, a shocking look at pro sports charities hoarding cash and overspending on fundraising. The Calgary Flames Foundation was particularly bad, donating a dismal 30 cents for every dollar raised. They also have $8 million in reserves despite spending less than $2 million a year on charitable giving.

Have a great weekend, everyone!

**This is a review of CoPower Green Bonds** While cannabis stocks got much of the attention from investors this year, a different type of green investment is beginning to emerge in global markets. Green Bonds are used to fund environmental and climate-friendly projects such as renewables, energy efficiency, water efficiency, bioenergy, low carbon and green buildings, to name a few.

This rapidly expanding sector is expected to issue $250 billion in Green Bonds in 2018 according to Moody’s, up from $155 billion the previous year. The Climate Bonds Initiative expects annual Green Bond issuance to reach $1 trillion as soon as 2020.

Investors in Green Bonds are typically large institutions or governments, but retail investors like you and me can also take advantage of this growing sector while helping to make a measurable impact on the environment.

CoPower Green Bonds

Enter CoPower. Their Green Bonds include a 6-year bond that offers 5 percent annually and a 4-year bond that offers 4 percent annually. Did that pique your interest? Mine, too!

Investors can choose to receive quarterly interest payments (simple interest) deposited directly into their bank account with the principal repaid at maturity, or allow interest to be re-invested into Green Bonds, earning interest on all interest accrued as well as on their principal investment (compounding interest).

The minimum investment is $5,000, and bonds can be purchased in $1,000 increments thereafter. Investors can purchase bonds directly through CoPower or by opening an RRSP or TFSA at a discount brokerage such as Questrade. Check with your financial institution or advisor to see if CoPower Green Bonds are an eligible investment inside your portfolio.

It’s important to note that CoPower Green Bonds are private investments so they are not traded on any public exchange and cannot be easily sold or traded on a secondary market. Investors should be prepared to hold their bonds to maturity.

In what type of projects does CoPower invest?

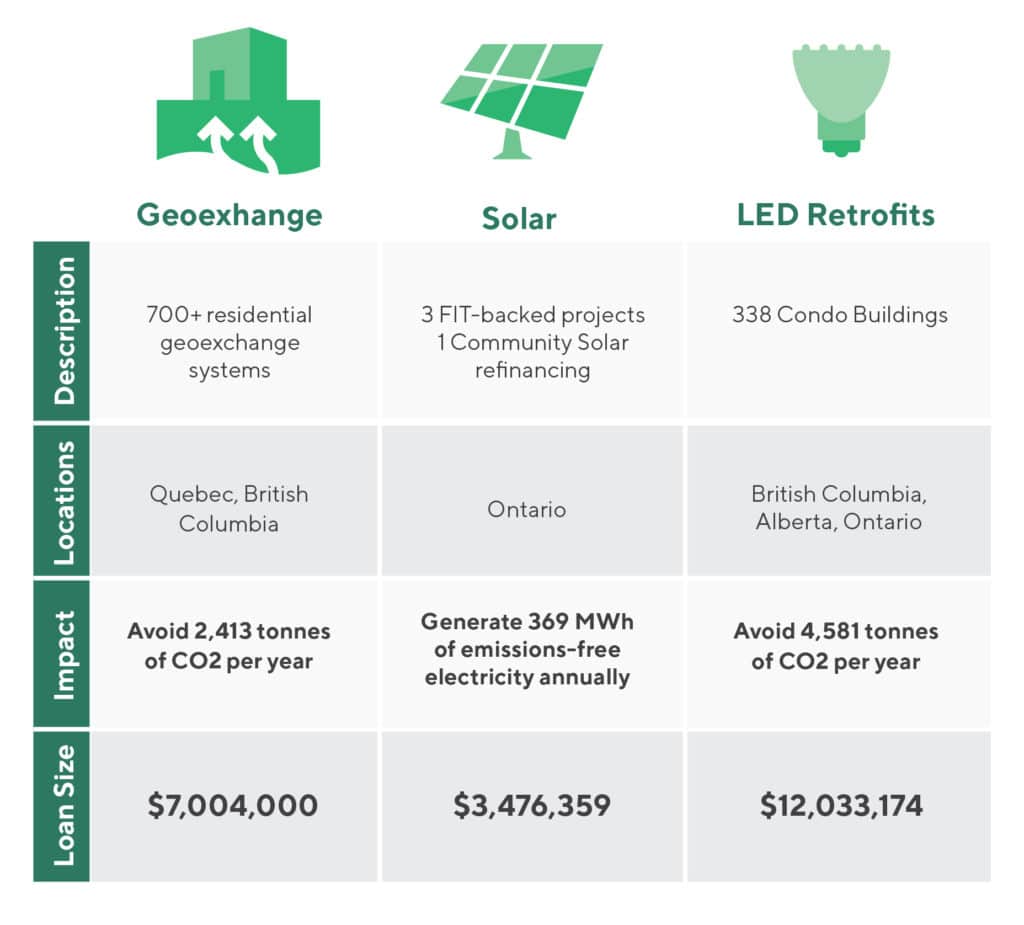

One of CoPower’s most recent investments was a $6.4 million portfolio of residential geothermal heating and cooling projects in Kelowna, BC. The system captures thermal energy from the ground and transfers it through the home’s existing heating and cooling system (reversing in the summer to remove heat and transfer it to the cooler ground).

Such a system could cost individual homeowners between $30,000 and $50,000 upfront to install. With CoPower’s financing, the project developer, GeoTility, installs the geoexchange systems and charge homeowners a fixed quarterly fee in return for the energy services.

CoPower believes the risk of default is low since heating and cooling is considered an essential service.

The feel-good story is that the 658 individual projects in this portfolio are expected to avoid more than 3,273 tonnes of CO2e annually. That’s the equivalent of each homeowner involved getting rid of their own car and their neighbours.

CoPower’s other project investments include several portfolios of LED lighting retrofits in condo buildings across Ontario, BC and Alberta, as well as solar projects in Ontario.

Who is investing in CoPower Green Bonds?

CoPower says its Green Bond investors include, “millennials making their first investment, grandparents investing on behalf of a grandchild, investment advisors making purchases for clients, and a major Canadian financial institution.”

I spoke with one of their millennial investors, Dr. Carl Durand, a 31-year-old optometrist.

Dr. Durand initially invested in 2017 with CoPower’s second round of Green Bonds, and has since invested in CoPower’s third round of Green Bonds released in 2018.

He said he heard about CoPower through Tim Nash of The Sustainable Economist.

“I had been looking for Green Bond options but found that most were only available to residents of certain provinces. Tim had suggested I look into CoPower which had just started at the time.”

Green Bonds are part of Dr. Durand’s portfolio of “couch potato” style ETF investments, which includes Canadian, U.S., and International equities, as well as REITs and preferred shares.

“I previously had Canadian bond ETFs (such as VAB) but I replaced those with my CoPower green bonds as the fixed income part of my portfolio,” he said.

Why invest in Green Bonds? For investors like Dr. Durand, it’s looking at what’s good for the planet but also good for his portfolio.

His initial motivation was to reduce his personal carbon footprint and directly fund the growing green economy. He felt that governments couldn’t be counted on to take action on climate change, so individuals needed to step up too.

When he did the math and saw that CoPower’s annual return was 5 percent (on its 6-year Bond), it meant that he could also improve the returns on the fixed income part of his portfolio by about two percent.

“I guess you could say I came for the environmental benefits and stayed for the returns,” he said.

Dr. Durand uses Questrade to hold his CoPower Green Bonds within his TFSA and RRSP, but when it comes to non-registered investments he opted to go directly through CoPower’s platform.

When it comes to risk, Dr. Durand considers himself to be fairly risk averse as an investor. Diversification reduces risk, which is why he invests in broad ETFs rather than individual stocks.

Even though private investments, like CoPower Green Bonds, are considered a riskier asset class, he considers them to be well-diversified “because of the number of different projects they are involved in (from solar to geothermal to energy efficiency) and that these projects are taking place in many locations across the country,” and is comfortable with the risk-reward equation given his financial and impact goals.

Also, he adds, the sheer number of stakeholders involved in the projects such as the thousands of condo owners in the LED retrofit projects, and hundreds of homeowners in geothermal projects, spreads out the risk a lot more, “which puts my mind at ease.”

Final thoughts

A major climate change report issued recently by 91 scientists from 40 countries warned of catastrophic effects of climate change arriving as soon as 2040 without drastic action to reverse course.

Investing a small portion of your portfolio in Green Bonds seems like an appropriate action to take in order to make an impact on the environment while at the same time boosting returns on the fixed income side of your portfolio.

Did I mention the 5 percent fixed return on CoPower’s 6-year bond?

If helping the planet doesn’t warm your heart, at least the investment can pad your wallet. Whether you’re a socially conscious millennial looking to make an impact, or an income-hungry retiree looking for reliable fixed income, CoPower’s Green Bonds are worth a look.

Learn more about the Green Bonds issued by CoPower here.

This post has been brought to you in partnership with CoPower. All views are my own. Full details are available in the CoPower Green Bond III Offering Memorandum.