**This is a review of CoPower Green Bonds** While cannabis stocks got much of the attention from investors this year, a different type of green investment is beginning to emerge in global markets. Green Bonds are used to fund environmental and climate-friendly projects such as renewables, energy efficiency, water efficiency, bioenergy, low carbon and green buildings, to name a few.

This rapidly expanding sector is expected to issue $250 billion in Green Bonds in 2018 according to Moody’s, up from $155 billion the previous year. The Climate Bonds Initiative expects annual Green Bond issuance to reach $1 trillion as soon as 2020.

Investors in Green Bonds are typically large institutions or governments, but retail investors like you and me can also take advantage of this growing sector while helping to make a measurable impact on the environment.

CoPower Green Bonds

Enter CoPower. Their Green Bonds include a 6-year bond that offers 5 percent annually and a 4-year bond that offers 4 percent annually. Did that pique your interest? Mine, too!

Investors can choose to receive quarterly interest payments (simple interest) deposited directly into their bank account with the principal repaid at maturity, or allow interest to be re-invested into Green Bonds, earning interest on all interest accrued as well as on their principal investment (compounding interest).

The minimum investment is $5,000, and bonds can be purchased in $1,000 increments thereafter. Investors can purchase bonds directly through CoPower or by opening an RRSP or TFSA at a discount brokerage such as Questrade. Check with your financial institution or advisor to see if CoPower Green Bonds are an eligible investment inside your portfolio.

It’s important to note that CoPower Green Bonds are private investments so they are not traded on any public exchange and cannot be easily sold or traded on a secondary market. Investors should be prepared to hold their bonds to maturity.

In what type of projects does CoPower invest?

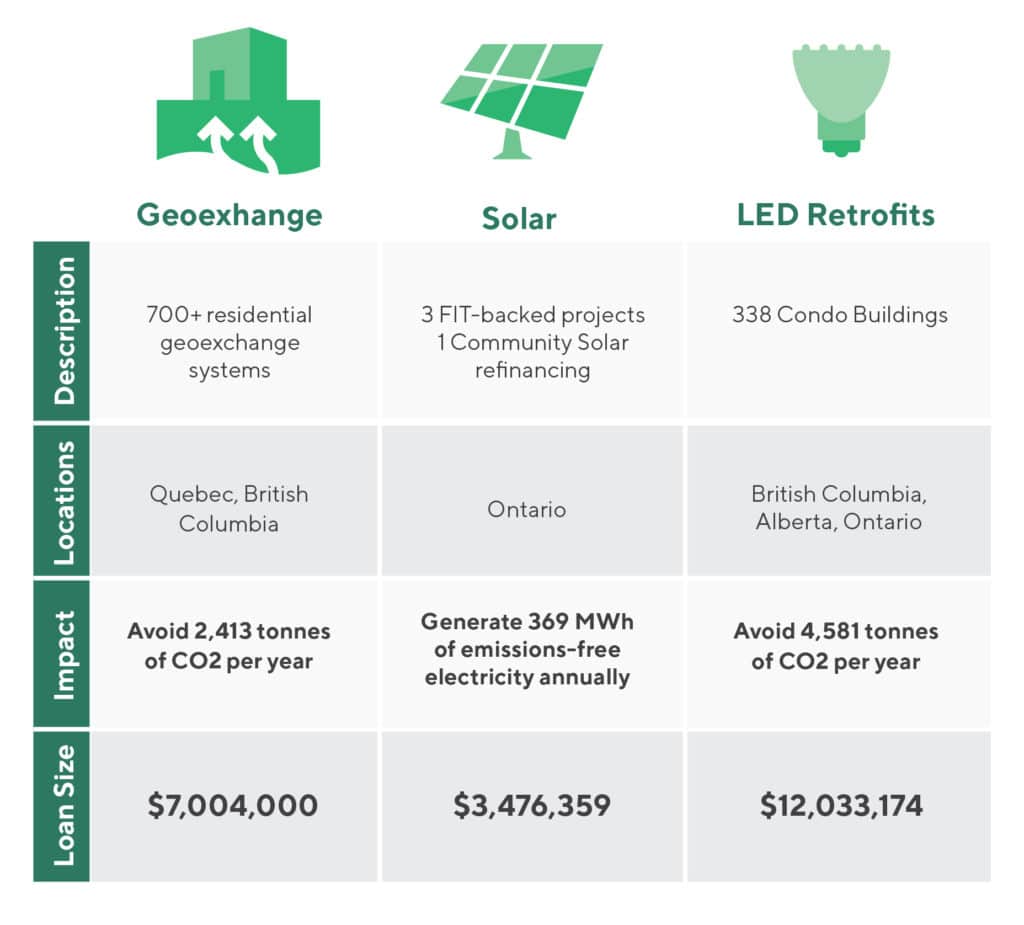

One of CoPower’s most recent investments was a $6.4 million portfolio of residential geothermal heating and cooling projects in Kelowna, BC. The system captures thermal energy from the ground and transfers it through the home’s existing heating and cooling system (reversing in the summer to remove heat and transfer it to the cooler ground).

Such a system could cost individual homeowners between $30,000 and $50,000 upfront to install. With CoPower’s financing, the project developer, GeoTility, installs the geoexchange systems and charge homeowners a fixed quarterly fee in return for the energy services.

CoPower believes the risk of default is low since heating and cooling is considered an essential service.

The feel-good story is that the 658 individual projects in this portfolio are expected to avoid more than 3,273 tonnes of CO2e annually. That’s the equivalent of each homeowner involved getting rid of their own car and their neighbours.

CoPower’s other project investments include several portfolios of LED lighting retrofits in condo buildings across Ontario, BC and Alberta, as well as solar projects in Ontario.

Who is investing in CoPower Green Bonds?

CoPower says its Green Bond investors include, “millennials making their first investment, grandparents investing on behalf of a grandchild, investment advisors making purchases for clients, and a major Canadian financial institution.”

I spoke with one of their millennial investors, Dr. Carl Durand, a 31-year-old optometrist.

Dr. Durand initially invested in 2017 with CoPower’s second round of Green Bonds, and has since invested in CoPower’s third round of Green Bonds released in 2018.

He said he heard about CoPower through Tim Nash of The Sustainable Economist.

“I had been looking for Green Bond options but found that most were only available to residents of certain provinces. Tim had suggested I look into CoPower which had just started at the time.”

Green Bonds are part of Dr. Durand’s portfolio of “couch potato” style ETF investments, which includes Canadian, U.S., and International equities, as well as REITs and preferred shares.

“I previously had Canadian bond ETFs (such as VAB) but I replaced those with my CoPower green bonds as the fixed income part of my portfolio,” he said.

Why invest in Green Bonds? For investors like Dr. Durand, it’s looking at what’s good for the planet but also good for his portfolio.

His initial motivation was to reduce his personal carbon footprint and directly fund the growing green economy. He felt that governments couldn’t be counted on to take action on climate change, so individuals needed to step up too.

When he did the math and saw that CoPower’s annual return was 5 percent (on its 6-year Bond), it meant that he could also improve the returns on the fixed income part of his portfolio by about two percent.

“I guess you could say I came for the environmental benefits and stayed for the returns,” he said.

Dr. Durand uses Questrade to hold his CoPower Green Bonds within his TFSA and RRSP, but when it comes to non-registered investments he opted to go directly through CoPower’s platform.

When it comes to risk, Dr. Durand considers himself to be fairly risk averse as an investor. Diversification reduces risk, which is why he invests in broad ETFs rather than individual stocks.

Even though private investments, like CoPower Green Bonds, are considered a riskier asset class, he considers them to be well-diversified “because of the number of different projects they are involved in (from solar to geothermal to energy efficiency) and that these projects are taking place in many locations across the country,” and is comfortable with the risk-reward equation given his financial and impact goals.

Also, he adds, the sheer number of stakeholders involved in the projects such as the thousands of condo owners in the LED retrofit projects, and hundreds of homeowners in geothermal projects, spreads out the risk a lot more, “which puts my mind at ease.”

Final thoughts

A major climate change report issued recently by 91 scientists from 40 countries warned of catastrophic effects of climate change arriving as soon as 2040 without drastic action to reverse course.

Investing a small portion of your portfolio in Green Bonds seems like an appropriate action to take in order to make an impact on the environment while at the same time boosting returns on the fixed income side of your portfolio.

Did I mention the 5 percent fixed return on CoPower’s 6-year bond?

If helping the planet doesn’t warm your heart, at least the investment can pad your wallet. Whether you’re a socially conscious millennial looking to make an impact, or an income-hungry retiree looking for reliable fixed income, CoPower’s Green Bonds are worth a look.

Learn more about the Green Bonds issued by CoPower here.

This post has been brought to you in partnership with CoPower. All views are my own. Full details are available in the CoPower Green Bond III Offering Memorandum.

Who wants to give away their monies to government agencies? Raise your hand. Obviously there should be no hands going up right about now. The cliché is that you work hard for your money. You don’t want to give that money away, needlessly.

As Canadians we can pay some very high tax rates on income and we pay considerable taxes when we purchase items by way of sales taxes and surtaxes. We likely all pay our fair share like ‘good Canadians’ but let’s not go overboard on the charity here. Let’s limit the amount that we hand over, all in above-the-board legal fashion of course.

Year End Tax Traps for Mutual Funds and ETFs

As we are now into late October we’ll start with the year-end tax trap for mutual funds and ETFs and perhaps even individual stocks. I had touched on this in my recent Mutual Funds 101 post.

A mutual fund will usually and mostly pay a distribution once a year in late December. That distribution represents the income in the fund from bonds and stock dividends. If you hold these funds in a taxable (non-registered) environment that income is taxable. There are no concerns if you hold that fund in an RRSP, TFSA or RRIF as the income is not taxable.

Here’s the tricky thing with a mutual fund distribution; it represents the bond income and dividend income that has already arrived in the fund throughout the year. There is no value added or created on distribution day. The mutual fund price will drop in equal proportions to the income delivered. That said the full amount of the distribution is taxable.

And here’s the trap. It you buy a mutual fund in November and the fund delivers a distribution in December (representing the full year’s fund income) you will pay tax on the full year’s income even though you’ve only been in the fund a few weeks.

We want to limit our taxes paid and we certainly do not want to pay taxes on monies we did not receive. This tax trap can exist in ETFs as well, given that ETFs can pay distributions on an annual, semi-annual, quarterly or monthly basis. Of course, the shorter the period the less effect of the trap of paying tax on income that you did not receive.

Unexpected Capital Gains

Thanks to fee-for-service financial planner Jason Heath who explains how we can also see capital gains show up in the year end tax trap.

Mutual fund and ETF trusts distribute their income – interest, dividends and realized capital gains – to investors. They may not literally distribute the income in the form of cash, as it may be reinvested in the fund, but the income is considered distributed for personal income tax purposes. That’s why on a T3 tax slip that reports trust income you see a box for capital gains. This isn’t capital gains you had from selling your fund, but rather, it’s for capital gains realized by the fund itself on underlying investments it sold during the year that get allocated to you.

The risk of an unexpected capital gains distribution is more significant for an actively managed mutual fund or ETF that may be selling a position it has owned for years or that has appreciated significantly. A passive ETF will typically just be rebalancing over the course of a year and small tweaks are less likely to result in a large year-end capital gains distribution. You may be able to check with a mutual fund or ETF company towards year-end to see if they can provide an estimated capital gains distribution for the year.

So when should we ignore the tax trap?

If you are doing the prudent thing and investing on a regular schedule or by way of an automatic investment plan – stay the course. Both Robb Engen and me will also give you a standing ovation. That consistency is a staple of wealth creation. You’ve made purchases throughout the year, you will benefit from the income that was delivered throughout the year. And if you’re considering making a smaller purchase there might be little by way of tax consequences.

We will pay attention to the tax trap when we are making large year-end purchases that will create a meaningful tax event. That said, there’s more than the income consideration for an investor. In an environment when stocks and funds have been falling in price in considerable fashion, an investor might decide to take the tax hit to buy the stocks or funds as they ‘go on sale’. They might feel that there is great long term value. That is a personal decision, but make sure you do understand the tax consequences.

It may also be a time to sell your funds or stocks. It might be time to say ‘so long’ to your investments that are under water. Bye bye losers.

Tax-Loss Harvesting

On tax loss harvesting Jason offers …

Tax loss harvesting may be a suitable strategy. I say “may” because it depends. If you have non-registered investments that have declined in value from their purchase price, you may have a capital loss you can realize for tax purposes. If you have realized capital gains in the current year, or taxable capital gains in the previous 3 years, you can claim current year losses to offset them. You have to claim current year losses against current year gains and be in a net loss position for the year before you can carry any current year losses back to a previous year. And if you have net losses for the year that you don’t carry back, they can be carried forward indefinitely.

And Jason also warns against the situations where it might not make sense to sell your losers. After all, we are only pushing the eventual tax burden down the road.

Some people aim to minimize income or tax payable at all costs, but purposely realizing a loss when your income would have been pretty low anyway may provide little benefit if you expect your income to be much higher in the future. That capital loss that you may have to claim against current year capital gains may be better used in a future higher income year to offset capital gains in that year.

And as we head into November and December here are a few other year-end tax pointers courtesy of James Gauthier, the Chief Investment Officer at robo-advisor Justwealth. I will also expand on some of the topics that James offers for consideration.

Pension Tax Credit RRIF withdrawals ($2,000) for tax year need to be withdrawn (if applicable). These apply to those who are 65 years old and above.

Ensure you have all desired retirement income settled from all sources for current calendar year. Ensure that trades settle a few days before year-end. The trades go by full settlement not trade entry dates. And keep in mind that in January of 2019 you can, of course, create retirement income that will be attributed to the 2019 calendar year.

RESP withdrawals count in the calendar year of settlement. To cover the full year of schooling for 2018/2019 it might be more advantageous to create some RESP income in 2018 and some in 2019. Know your RESP rules as income from government grant portions is treated differently (for tax purposes) compared to your personal RESP contributions. The grant portion is taxable as income in the student’s hands, the contribution amount is not taxable (for once the government realizes that you’ve already paid income taxes on those monies).

I like this brief page from RBC as an RESP primer.

RRSP contributions for calendar year 2018 can be made up to the first 60 day period in 2019. There’s no rush, but you’re already investing on a regular schedule, right?

If you are turning 71 this year your RRSP’s need to be converted to a RRIF or annuity. You have that last chance to make an RRSP contribution before calendar year-end to reduce 2018 taxes. RRIF payments will begin in 2019.

If you are considering a late year investment keep in mind that you will get another $5,500 of Tax Free Savings Account contribution space on January 1, 2019. And of course we do not lose any unused TFSA room, that is carried forward.

You will be granted additional RESP contribution space in January of 2019.

Personal Finance Housekeeping

And James offers a simple and wonderful reminder. This is a good time to do some personal finance housekeeping.

Related: Your year-end financial planning checklist

Do you have beneficiaries set up on all of your registered accounts? Do you need to change any of your beneficiaries?

I’ll add that you might check in on other basic personal finance musts.

Do you have proper insurance? Do you have your will created, or in proper order? Did you make all desired charitable contributions? Do you need a financial plan? Or you on track to reach your personal financial goals. If you don’t have a plan, get one. While we always want to pay attention to fees, you can access a fee-for-service financial planner.

Thanks again to Jason, James and Robb (for allowing me to share these tax planning thoughts with Boomer and Echo readers).

Please leave your comments. If I don’t know the answer, I’ll find someone who does.

Dale is a still-recovering former advertising writer and creative director. He then moved on to become an advisor on lower fee index funds. These days Dale helps Canadians find the many sensible lower fee investment options available by way of his site, cutthecrapinvesting.com

We partner with a comparison site called creditcardGenius to share the best rewards cards in Canada and keep you informed of the latest promotions and sign-up bonuses. I prefer it over other comparison sites because creditcardGenius offers an objective, math-based scoring system that sorts through 189 Canadian credit cards and recommends the best rewards card for your personal situation.

You can see it in action here on our credit card comparison page.

Free Gift Card Promo

I’m excited about their new promotion, which gives applicants the opportunity to earn $150 in Amazon e-Gift Cards when they sign up and get approved for the Scotiabank Gold American Express Card. This is one of the top travel rewards credit cards in Canada and pays 4x points on spending categories such as groceries, gas, dining, and entertainment (the most bonus spending categories of any Canadian credit card).

You’ll also get 15,000 in Scotia Rewards points when you spend $1,000 within the first three months. Those points are worth $150 in travel. The card comes with a $99 annual fee, which is lower than most premium travel rewards credit cards.

When you combine the early spend bonus with the $150 in Amazon e-Cards, and subtract the annual fee, that’s a net gain of $201. Now add in the opportunity to earn 4x points in those bonus spending categories and there’s potential to earn hundreds of dollars in rewards in a year.

Okay, you’ve heard enough. Here’s how to get the deal:

Visit creditcardGenius and click on ‘Get This Deal’. Then share the deal on Facebook to unlock the first $50 Amazon e-Gift Card. Upon approval you’ll receive a $100 Amazon e-Gift Card. Spend $1,000 in the first three months and you’ll receive 15,000 in Scotia Rewards points. It’s that simple.

Act quickly because this deal expires on October 31st, 2018.

This Week’s Recap:

On Thursday I reviewed Fred Vettese’s Retirement Income for Life and explained why a realistic retirement income target might be much lower than we think.

Next week we’ll have a guest post from Dale Roberts who shares some year-end tax planning for mutual fund, ETF, and individual stock investors. Plus, I’ll cover a very interesting investment opportunity that could be good for the planet and your portfolio.

Weekend Reading:

The Bank of Canada raised its key interest rate by 25 basis points to 1.75 percent. It’s the fifth increase since last July and the rate hikes are starting to put noticeable pressure on variable interest loans such as mortgages (mine!) and lines of credit.

Next year we could see a welcome government increase – in the form of higher TFSA contribution limits. The limit is expected to increase to $6,000 in 2019.

As you age, should you simplify your investment holdings for estate planning purposes? The Blunt Bean Counter has the answer.

Contrary to what Suze Orman believes, Mark Seed at My Own Advisor says early retirees don’t need $5 million to retire comfortably.

Jerry is 60, just lost his job, and has $580,000 in investments. Dan Bortolotti explains how he should invest to get $35,000 annually in income.

In his latest Common Sense Investing video Ben Felix explains how asset allocation works to build a diversified portfolio:

Michael James looks at getting even with big businesses like banks and telecoms by owning their stocks.

Million Dollar Journey lists the top 10 wealthiest Canadians, from the Thomson family to Jimmy Pattison.

Should you incorporate a business to save on taxes? We did, but only because we could stream dividends to my stay-at-home wife. Jason Heath explains why incorporating only makes sense if you can justify the initial and ongoing costs, and don’t need all the income for personal needs.

Finally, are financial literacy programs a waste of time? The evidence seems to point to “just-in-time” financial literacy tools that can teach concepts and provide the right nudges precisely when you need them.