It’s normal to compare your financial situation with others to see how your finances measure up. Indeed, if you’ve ever calculated your net worth, or even tracked your spending, you probably enjoy reading other net worth reports and spending journals.

The problem with this type of financial voyeurism is that we’re often comparing apples and oranges. Take net worth, for example. It’s supposed to be a snapshot of your financial health at a particular moment in time. But everyone seems to have their own variation or twist on what to include (and what not to include) in their net worth statement.

How to calculate net worth

There’s a simple formula to calculate net worth: Assets – Liabilities = Net Worth.

We all have different ideas on what’s considered an asset and a liability, however, which can lead to confusion when trying to compare results.

Here’s the thing: The correct formula for calculating net worth is the one you use consistently over time to measure progress. That’s it.

I track my net worth twice a year and often get questioned why I include – or don’t include – certain items in my calculations. Here are some common differences I’ve come across in net worth updates:

Value of RRSP

Some people insist on discounting the value of their RRSP to account for the taxes they’ll have to pay upon withdrawal.

For example, if you had $100,000 in your RRSP today, you might list its value at just $60,000 to adjust for taxes owing in retirement.

A question for those who track their RRSP this way: Do you also include the estimated present value of your CPP and OAS benefits in your net worth statement?

I include the full value of my RRSP in my net worth calculation for the simple reason that I’m looking at a snapshot of my current financial situation. I’ll adjust my net worth accordingly when I convert my RRSP into a RRIF and start withdrawing retirement income.

Value of RESP

We put $400 per month into RESPs for our two daughters. I include the RESP balance in my net worth calculation because that money legally belongs to the parents (subscriber) until it is paid out to the children (beneficiary).

Of course, we have no intention of keeping the money for ourselves, but we’ll adjust our net worth accordingly once it gets paid out.

I can see why some people don’t include RESPs in their net worth calculations, but I like to track it because the contributions are fairly significant – it’s savings for a future need.

Value of your home

Some people peg the value of their home at the initial purchase price and never adjust for market value. Others go off of their annual property tax assessment, while some more in-tune with the real estate market may value their home at the most current market estimate.

I started with the purchase price of our home and then simply adjusted it annually by 2.5%. We developed the basement a few years ago so I just used the cost of the renovation to bump up the market value by $25,000.

I’ve even heard of some net worth statements that don’t include your primary residence in the calculation. Accredited investors, for example, must have a net worth greater than $1 million, but their primary residence is not counted as an asset in the calculation.

Pension assets

How can you put a value in today’s dollars of a defined benefit pension plan designed to pay you a monthly income when you retire? And what if that’s years, or even decades away?

There are several ways you can account for your pension assets in a net worth statement.

You can add up and track all of your contributions to the plan, or you can include your contributions along with your employer’s contributions.

Finally, you can use the commuted value of the pension, which is the lump sum paid to you if you left the plan today. This amount should be listed in your annual or semi-annual pension statement.

Vehicles (include, or not?)

It can make sense to include the value of your vehicle(s) in a net worth statement, along with any corresponding loans, if applicable.

However, it can be a pain to track the value of a depreciating asset every time you prepare a net worth calculation.

I see our vehicles as an expense. Sure, I could add $15,000 – $20,000 to my net worth if I sold one today, but then I’d have to buy another car to replace it. If I sold my house, on the other hand, I could pocket the sale proceeds and just rent another place. That’s probably not realistic with a vehicle.

A word on budgeting

The same caveat goes for budgeting – maybe even more so. I often hear questions about how much one should spend on groceries in a month. The answer has so many variables that it’s impossible to give any useful advice without more information.

Are you single, or trying to feed a family of five? Do you live in Nunavut, downtown Calgary, or somewhere in the Maritimes?

Not to mention the loaded question about what constitutes “groceries”. Does that just include food, or do you lump other household items under the grocery category?

Related: Here’s a detailed look at my budget

For simplicity I include food and household items in the “grocery” category of my budget. That means when I shop at Safeway or Costco I’ll throw the entire bill into “grocery” expenses. Unless there’s something obvious like clothing, or a shovel, in which case I’ll split those off into separate categories.

Again, when comparing budgets you need to compare apples to apples before you draw any conclusions.

Final thoughts

Keep it simple, folks (and consistent). The right way to calculate net worth is to use the same formula every time. Don’t be swayed by how others track their results. The whole point of tracking net worth is to measure your progress over time.

Get excited because you moved the needle forward, not because you changed yardsticks halfway through the game and saw an increase.

Comparing results can be dangerous if you’re not playing by the same rules.

What a crazy week! First, perhaps taking a cue from my pro-CPP expansion article, the federal government and most provinces agreed on CPP reform, with premiums set to increase in 2019. This surprisingly quick compromise got the internet buzzing for a better part of the week.

Then Brexit happened.

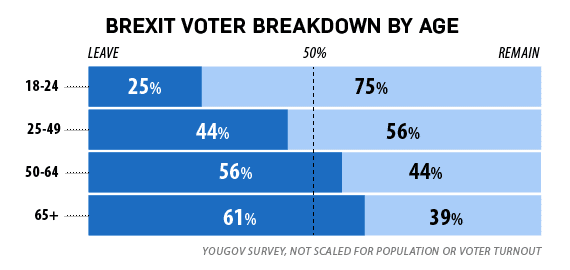

Brexit, or British exit, referred to Thursday’s referendum by British voters to leave the European Union. Voters were split, according to most polls, in the weeks leading up to the referendum. The youth vote was hoping to remain in the EU, while the 50+ crowd wanted to leave the EU and its free flowing migration and trade.

Pundits were shocked late Thursday night as it became clear that Britain had voted to leave the EU. What happens next is anyone’s guess, although that didn’t stop every news outlet, political commentator, and economist from adding their two cents about the new and scary future.

Sure, the markets (over) reacted as they always do to news of this magnitude. But for those of us saving and investing for a future that’s decades away, Brexit is just one of many small setbacks we’ll see throughout our journey.

Morgan Housel summed it up best: The pundits may panic. Don’t follow their lead.

Momentum Twitter Chat

Speaking of saving and investing, I’m thrilled to partner with Scotiabank to host the Momentum Twitter Chat on Monday night (June 27th) at 7:00 p.m. EST using the hashtag #ScotiaSavings.

I love talking about money and this Twitter Chat will be especially fun (and timely) since we’ll be chatting about how to build momentum with your savings. We’ll touch on a number of topics, including:

- How to make savings a priority when there are so many other things competing for your money

- Saving in a low interest rate environment

- The best place to park cash for short-term goals

- Tips to get started on a savings plan

- Where to invest your first $1000

In light of all the macro-economic activity in the news this week, the fact is that CPP expansion and Britain leaving the EU probably won’t impact your personal finances in the short term. You still have to execute your financial plan and focus on the areas that you can control.

I enjoy reading about behavioural economics and consumer behaviour and one trend that I hope can help boost the savings habits of Canadians is the gamification and incentivization of products to lead to better outcomes.

For example, I’ve written before about the Momentum Savings Account that rewards inertia. Clients earn bonus interest when they keep a balance of $5,000 or more for longer than 90-days. It’s incentives like this that keep customers engaged and thinking about ways to save and earn more money.

This week’s recap:

On Monday I wrote about Canada Pension Plan expansion and why it matters.

On Wednesday Marie explained why a savings plan is like starting a diet.

And on Friday we had the Travelling Boomer stop by and share 5 ways to visit Europe on a budget.

Over on the Lowest Rates blog I looked at co-signing a car loan for your teen.

And The Globe and Mail’s Paul Attfield was kind enough to include my answers in this automated investing FAQ: Answers to six questions about robo-advisors.

Weekend Reading:

John Heinzl reveals his brilliant post-Brexit investing plan.

“Get ready for the bull market in opinions.” – Ben Carlson, A Wealth of Common Sense.

How the historic CPP deal came together so quickly.

Canadian Federation of Independent Business president and chief curmudgeon Dan Kelly says the CPP expansion is just a bailout for people who take a trip to Mexico.

Is CPP a disaster for Canadian business? That’s selling it too hard.

MoneySense calculated how much more you’ll get from CPP changes and determined that some could see around 50% more pension.

CBC also took a detailed look at what the CPP boost means for the average Canadian worker.

Why expand the CPP? Rob Carrick says just take a look at house prices.

A fascinating look into the world of Generation Z – the anti-Millennials.

Speaking of Millennials. This guy is 31, makes $130,000/year, still lives with his parents, and feels that buying a house will cut into his extravagant lifestyle. Ugh.

Why Generation X is squeezing baby boomers out of cottage country as retirement looms.

Why does the government keep spoiling your online bargains? A new study looks at what would happen if the feds raised the threshold for charging cross-border duties and taxes.

The federal government is putting together a working group to “discuss” housing affordability problems in B.C. and Ontario.

Meanwhile, Vancouver is ready to forge ahead with a vacant home tax, with or without support from the province.

Here’s why your daily commute might be destroying your happiness.

Preet Banerjee interviewed Nest Wealth founder Randy Cass about automated online advice, aka robo-advice, in his latest podcast.

“Why pay a percentage of assets when you can pay a flat rate for investment advice instead?”

Canadian Couch Potato Dan Bortolotti compares the cost vs. convenience of owning ex-Canada ETFs like VXC and XAW.

Do you compare your portfolio’s returns to an appropriate benchmark? Michael James goes through several scenarios where benchmarking makes good sense.

Finally, want to get married for $427? Don’t say the W-word – and other tips.

Have a great weekend, everyone!

This is a guest post by Paul Marshman, The Travelling Boomer, on how to visit Europe without breaking the bank.

Most travellers agree – Europe is a great place to visit, especially in summer. Problem is, it can be an expensive place to travel. Staying in downtown London or dining on the Champs Elysees in Paris can leave your credit card with a major hangover.

However, it doesn’t have to be like that: there are ways to enjoy Europe’s bright lights without leaving your bank account drained.

I’ve visited several of Europe’s great cities in the past few years, from Copenhagen to Budapest, and I’ve found a few strategies that can help keep your travel costs in check. Here are The Travelling Boomer’s five ways to visit Europe on a budget.

Skip the hotel

Finding a low-cost hotel in many European can be a challenge, especially in mid-summer, when prices are at their highest. How to find an affordable place to stay?

The Champs-Elysees at night in Paris, France

Try the alternative accommodation sites, such as Airbnb, WIMDU and VRBO. While these aren’t always the cheapest way to go in North America, a recent survey shows that they’re almost always cheaper than a comparable hotel in Europe. As well, you often get the use of a kitchen, so you can self-cater a few meals and save more money.

The cheapest deals typically rent you a room in someone’s home. But you can get whole apartments for substantially less than the price of a hotel room. In fact, sites like Tripping.com specialize in apartment and home rentals. Some specialize in one city, like Paris Address and Nostromondo in Rome. If you have a long time horizon, you can even try doing a home exchange.

You have to join the service you choose, but it’s free, and the process isn’t too onerous. But book early: the better places tend to book up fast, especially in high season.

Have breakfast in bed

Speaking of self-catering, one expense you can avoid is the hotel breakfast. Most European hotels offer breakfast, but in many cases it’s not included in the price of your room. You can find yourself paying 10 to 15 euros to have breakfast in the dining room every morning – and over the course of a trip, that adds up.

You can go to a coffee shop if there’s one nearby, but that may not be cheap, either — coffee is expensive in Europe. Better to pick up some pastries, or some bread and cheese, and have breakfast in your room in the morning.

You may still have to spring for a take-out coffee, but there’s a way around that too: bring along one of those immersible water heaters and make your own tea or coffee in a cup (Starbucks makes a decent instant coffee, if you’re a fan).

Buy a pass

Paying transit fares and tickets to museums, castles and such can leave you with empty pockets by the end of the day. But you can save some money by purchasing one of the discount cards most European cities sell.

For example, the London Pass gives you entry to attractions like the Tower of London, Westminster Abbey, Kew Gardens and Thames River Cruises; other cities include free rides on the local transit and train services. These cards can save you time, as well, since you can often skip the ticket line.

These cards aren’t cheap, but they can make sense if you’re going to see a few attractions during your stay. Most European museums charge more than $10 for admission, so it doesn’t take many to exceed the cost of the card. If that doesn’t work for you, consider a transit pass, which can save you money if you’re moving around town a lot.

One last suggestion: if you’re visiting for just a day or two, try the Hop-on, Hop-off (HoHo) bus. For a reasonable price – typically $20 to $30 — you can see most of the main attractions in as little as a half-day. You get the lay of the land, and there’s a guided tour thrown in.

Get off the main street

Dining in that lovely piazza in the middle of Rome can be so romantic – and so expensive. The restaurants in European cities’ most famous spots are there to cater to tourists, and that means they’ll charge you tourist prices.

It’s tempting to sit at one of those marble tables overlooking the historic church, but do yourself a favour and just have a drink. When it’s time to eat, look for a place in a less famous spot.

In most cities, you can enjoy great food and avoid the great big bill by looking for a restaurant a block or two off the main square. You’ll likely get more authentic food, and maybe even meet a few of the locals.

In Britain, for example, neighbourhood pubs serve some of the most economical meals. And ethnic neighbourhoods often have some of the best values. If your heart is set on the high-profile restaurant, go for lunch, when prices are often substantially lower.

A couple of other tips: In some places the portions are big enough to share an entrée, if you’re not big eaters. Or you can order a salad with meat in it as your main course. And in cities like Paris where the tap water is safe, ask for plain water instead of expensive bottled water. It’s free.

Go shopping

This seems like strange advice when we’re talking about saving money, but shopping at local stores can save you big-time. Pop into the neighbourhood shops and markets to do your souvenir shopping: you’ll often find the same things you saw in the tourist shops, for half the price. A few years ago I found an Ikea-style alarm clock in a store in Bruges, Belgium for 3 euros; I’ve been using it ever since.

Local food stores are a great resource, too. You can pick up some breakfast fare (see above), put together a picnic, or find some great local food products you can take home — at lower prices than in the airport duty-free shops.

It’s also fun to see what the natives eat, and what they pay for it; I rarely leave a city without browsing through a food store. If nothing else, I pick up some snacks to save me stopping at one more expensive café.

Those are a few suggestions that can help you visit Europe on a budget. Of course, you can save more by staying outside the heavy tourist zones, or by choosing a different destination. Smaller cities are generally cheaper than big ones, and Central European cities like Prague and Budapest are cheaper than more famous places like Paris and Rome.

Finally, if you don’t have to travel in summer, try visiting in the spring and fall: the weather may not be ideal, but the prices can be a lot more comfortable.

In any case, don’t let the prices keep you from seeing Europe. It’s one of the world’s great destinations, full of beauty and culture and history. And if you use some of these tips, you can do it without taking out a second mortgage.