While all motorists are required by law to have car insurance, most people couldn’t be bothered to shop around and make sure they’re getting the right coverage at the best price. If you’re anything like me, you might not have even changed insurance companies since you first started driving!

How do you know when it’s time to change car insurance providers? Many people are dissatisfied with their car insurance premiums, but surprisingly few are doing anything about it.

When it’s time to shop around for car insurance

Here’s a simple test: When you receive your annual renewal notice in the mail and discover your premiums have increased by 10% (or more) – don’t just grumble and file it away – it’s time to shop around.

The average consumer can reduce the cost of their car insurance premiums just by shopping around every 1-2 years and getting new quotes. It’s easy to search car insurance quotes online through a rate comparison site.

Take some time to evaluate your own driving situation to see if anything has changed. For example, you might want to remove collision coverage on an older vehicle or increase the deductible to the max if you wouldn’t bother with a small claim. Maybe you’re a veteran and would like to use that to your advantage by getting cheaper insurance and even USAA roadside assistance, among other benefits.

How else can you save money on car insurance? Look at other discounts and see if they apply. Would you move your house insurance to take advantage of a multi-product discount? You might save 5-10% on your premiums just by bundling your home and auto insurance policies. It’s shocking how many people aren’t doing this!

Similarly, if you’ve purchased winter tires you may qualify for a discount. Or you might qualify for a group discount if you happen to work for a preferred employer group.

Instead of waiting until your renewal date comes up to check for car insurance rates, keep in mind that there are other opportunities to review your policy throughout the year.

Whether you’re getting married, buying a new car, adding a teenager to your policy, or moving, there are opportunities to examine your policy and check for discounts. Take advantage of these opportunities to make sure you are always getting the best rates and that you have appropriate coverage.

If you do decide that it’s time to move on from your current car insurance provider, make sure you have your new policy in place before cancelling your old policy – you don’t want any gaps in coverage.

Beware that most insurance companies charge penalties if you cancel your policy mid-year. Unless you’re getting a big discount to switch immediately it probably makes more sense to wait until your policy is up for renewal.

Final thoughts

Basic car insurance policies are standardized to some degree, however it’s still important to compare policies as the range of coverage may differ between providers. Some types of coverage – such as accident benefits coverage – are not mandatory in every province.

Is the coverage comparable on each quote you receive? What is the company’s procedure if you have an at-fault claim? Under what circumstances would your insurance not be renewed?

Make sure you compare apples-to-apples when it comes to different policies. Weigh the cost of premiums against the coverage provided. Your main objective should be to buy the right amount of coverage at an affordable price.

One of the founding fathers of personal finance blogging – J.D. Roth – returned to his roots this week to celebrate the 10th anniversary of Get Rich Slowly. J.D. hits the highlights in taking readers through his own journey to financial freedom, starting 10 years ago buried with $35,000 in consumer debt and living paycheque to paycheque, and quickly mastering money and the psychology behind it to reach financial independence just a few short years later.

What appealed to his readers, and ultimately led to the massive growth of Get Rich Slowly, was J.D.’s personal narrative and obsession with the behavioural aspect of money management:

“I had always stressed the importance of psychology; but as my financial philosophy matured, I became even more convinced that smart money management was all about mindset, not math.”

I have tremendous respect for J.D. and the community he built at Get Rich Slowly. We started Boomer & Echo in 2010, and I thought writing 5 days a week for two years straight was a lot of work (and there are two of us!). J.D. wrote every single day for three straight years, creating more than 1,000 articles in that time. Unreal.

Congratulations to J.D. and the Get Rich Slowly team! You can follow J.D.’s new blogging venture at Money Boss.

More on the psychology of money

The New York Times published a special section of Your Money with insights into behavioural finance and investing:

How buyers react when prices rise and fall.

Credit card encourage extra spending as the cash habit fades away.

Getting workers to save more for retirement

Does your stockbroker draw complaints? Here’s how to find out.

This week(s) recap:

Last Monday I explained why indexing doesn’t mean settling for average returns.

Last Wednesday Marie shared all the reasons why you should become a member of your local library.

And last Friday a guest post by Daniel at Urban Departures gave us a Star Wars guide to investing.

On Monday this week I argued that stagnant wages shouldn’t get in the way of your financial goals.

On Wednesday Marie took a thoughtful look at you and money: what does it mean?

Finally, on Friday I reviewed the new TD Direct Investing WebBroker platform.

Over on Rewards Cards Canada I reviewed the Capital One Aspire Travel World Elite MasterCard.

I also guest-posted on the Modern Advisor blog with a guide to choosing an online financial advisor.

Weekend reading:

The Globe and Mail’s Rob Carrick is doing his best to reach out to millennials and that means taking the time to stop by Reddit to host an AmA (Ask me Anything). Read the full transcript here.

At the other end of the spectrum, Carrick looks at wants vs. needs and how actual retirees manage their money.

Regulators are taking a closer look at how investment firms manage conflicts of interest when it comes to how financial advisors are paid for the products they recommend to their clients.

The U.S. wants to prohibit conflicts of interest in retirement planning. Here’s how Obama’s conflict-of-interest rule could rattle investment giant Edward Jones.

These new rules, plus a shift toward passively managed funds points to how the financial industry is having its Napster moment.

All of this means that most financial advisors need to find a new value proposition:

“I personally find it hard to believe that there are advisers out there who are not yet aware of the evidence for not using active funds. Nor do I understand how advisers can study the evidence with any degree of thoroughness or objectivity and still maintain that trying to pick future star managers is the best way to go.”

Is life insurance the next frontier for robo-advisors? A new report from global consultancy firm EY says yes.

A cool, interactive look at where your tax dollars were spent in 2014-15.

Big Cajun Man Alan Whitton shares his tax reflections for 2016.

Jamie Golombek explains what we mean when we talk about the “tax rate” – and how to figure out what yours is.

The Panama Papers made headlines last week. Here’s how the world’s rich and famous hide their money offshore.

The CRTC is set to weigh in on whether high speed internet is a basic human right (Finland made universal access to minimum Internet speeds a legal right in 2009).

Are smart phone protection plans worth the money? Consumer advocate Ellen Roseman says a plan can be worth buying in some cases.

Michael James on Money with an insightful look at how much you have to learn to be a successful investor.

Barry Choi lists the 8 rules of personal finance.

Here’s how a simple credit error can ruin your home-owning dream.

Million Dollar Journey breaks down his 2015 expenses – less than $4500/month for a family of 4.

Gail Johnson explains the downside of downsizing in retirement: leaving your friends and neighbourhood behind.

Here are 10 crazy things people in finance believe, according to A Wealth of Common Sense blogger Ben Carlson:

“10. People in finance believe that advice has to be complicated to be effective.”

And finally, speaking of complicated, Carlson looks at Tesla – one of the hardest stocks to value over the last five years.

Have a great weekend, everyone!

I’ve been using TD’s discount brokerage since 2009 when I made the switch from mutual funds to DIY investing. At that time, the TD Direct Investing WebBroker platform left much to be desired. The legacy web design of TD WebBroker was clunky and difficult to navigate (with 55 different navigational links!), trades cost $29 each way, and the platform offered little in the way of personalized account reporting.

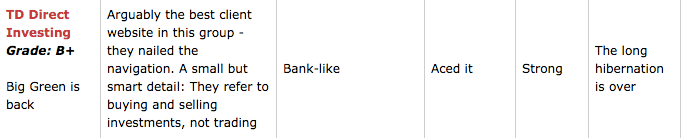

TD took a lot of heat over its lack of innovation as an online broker – most notably in The Globe and Mail’s annual ranking of discount brokers, where TD Direct Investing graded out as a mediocre C in 2013. After addressing the account reporting tools and adding U.S. dollar RRSP accounts, TD moved up a grade with a solid B, but that came with a caveat:

“There’s room for TD to move higher if it finishes the job of modernizing a website that still parties like it’s 1999.”

TD Direct Investing WebBroker Platform

That all changed at the end of 2015 when TD Direct Investing took its TD WebBroker platform to the next level. In fact, I’d say the new design rivals that of the nimble robo-advisor start-ups in terms of the overall user experience, simple navigation, and design.

Add in their best-in-class performance reporting, research, and educational tools (including expert webinars and videos), and you can see why TD leaped ahead of every other big bank brokerage in last year’s online broker rankings.

I switched from the old WebBroker platform to the new one back in December, so I’ve had a chance to play around with the tools and features for a few months now. Here’s what I like:

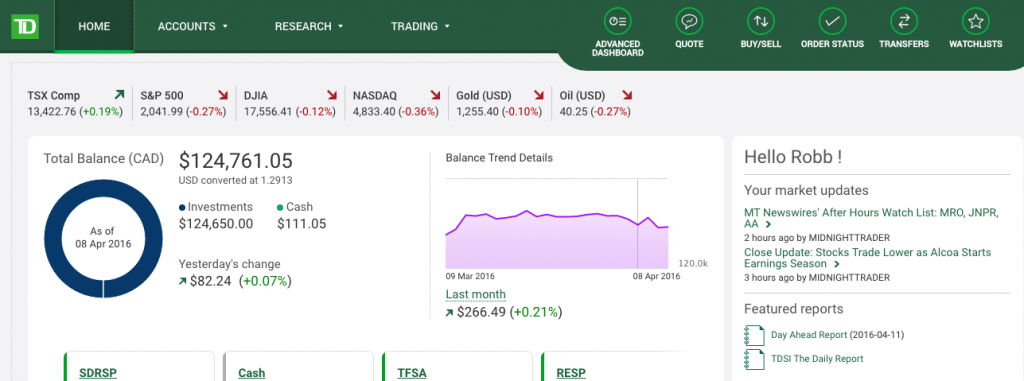

New and simple home screen design

It was a nice transition going from 55 navigational links on the home screen down to just a handful of buttons on a dashboard. You get a snapshot of today’s market activity at the top, plus some notes and featured reports along the sidebar. The main box shows you all of your accounts, total balance, yesterday’s change, plus a nice graph that depicts your balance trend for the past month.

From there you can breakdown your accounts into four main categories: holdings, activity, performance, and gain & loss:

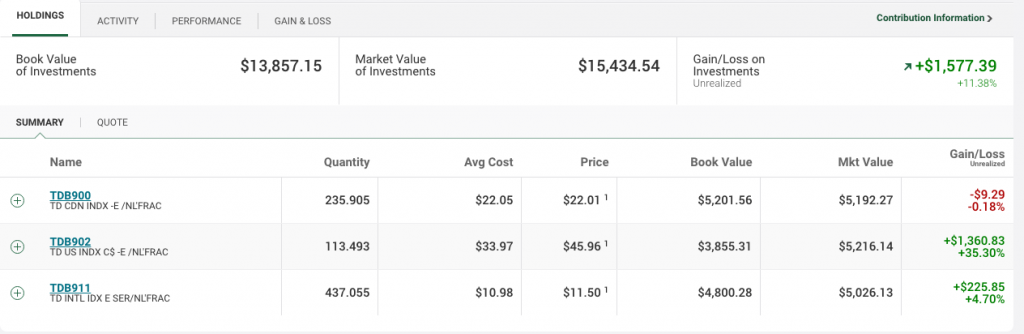

Holdings

A typical looking dashboard and overview of holdings that you’d expect to find from an up-to-date online broker. Here you can find the number of holdings in your account, along with details such as the number of shares, average cost, market price, book value, market value, plus your overall gain or loss by security.

Account Activity

Breaking down your account by activity allows you to view the details and history of each transaction. In the above example, you can see a monthly contribution, the purchase of mutual fund, a dividend reinvestment, and a deposit of the Canada Education Savings Grant based on the $400 contribution (split into two deposits because this is an RESP family plan for two children).

Performance

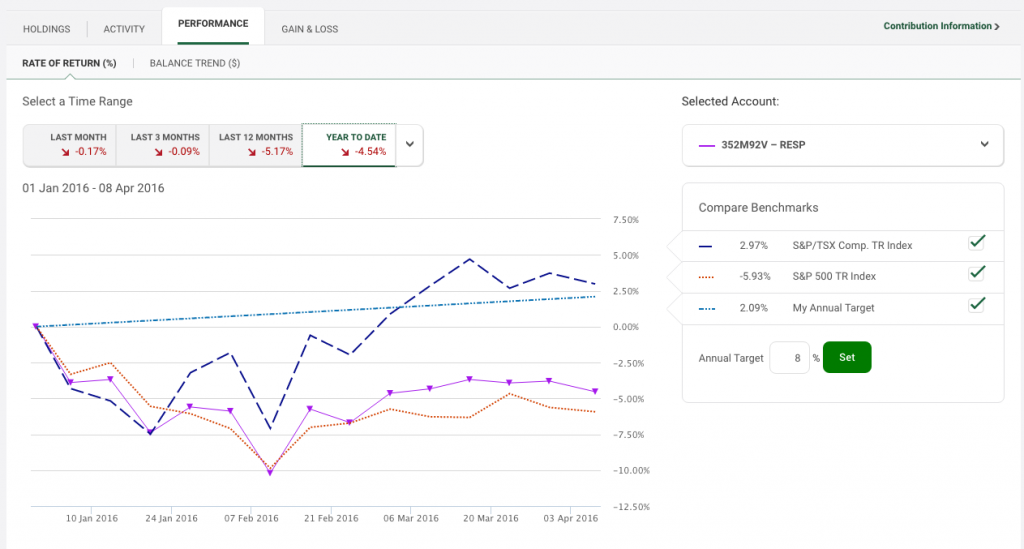

Without a doubt the coolest and most useful tool in the TD Direct Investing WebBroker platform is the performance section. Here you can see your rate of return by account, broken down into common time-periods such as last month, last 3 months, last 12 months, and year-to-date. You can also set a custom date range or view the account and its rate of return since inception:

The only downside to the custom date range feature is that the data only goes back to December 31st, 2010.

I like that I can set my own annual target rate of return – in this case, it’s 8% – and then compare your actual rate of return to not only your target rate, but also other benchmarks such as the S&P/TSX Composite Total Return Index and the S&P 500 Total Return Index.

As you can see above, my RESP portfolio is up 52.86% since inception, and that works out to 10.55% on an annualized basis. Those results handily beat the TSX (9.53%) and my annual target (38.48%) over that timeframe, but can’t keep pace with the roaring S&P 500, which was up 101.63% since 2012.

Balance Trend

If you want to see the impact that deposits or withdrawals have on your portfolio and its rate of return then just toggle over to the “balance trend” view. As you can expect with an RESP portfolio, especially in the early stages, the majority of the growth is coming from new deposits rather than changes in market value or dividends.

It’s worth noting that TD Direct Investing uses the time-weighted rate of return method to calculate investment returns. This method takes into account any deposits or withdrawals that affect the portfolio.

Balance trend is a nice touch for those who prefer to see the value of their portfolio grow in dollar terms rather than in percentages.

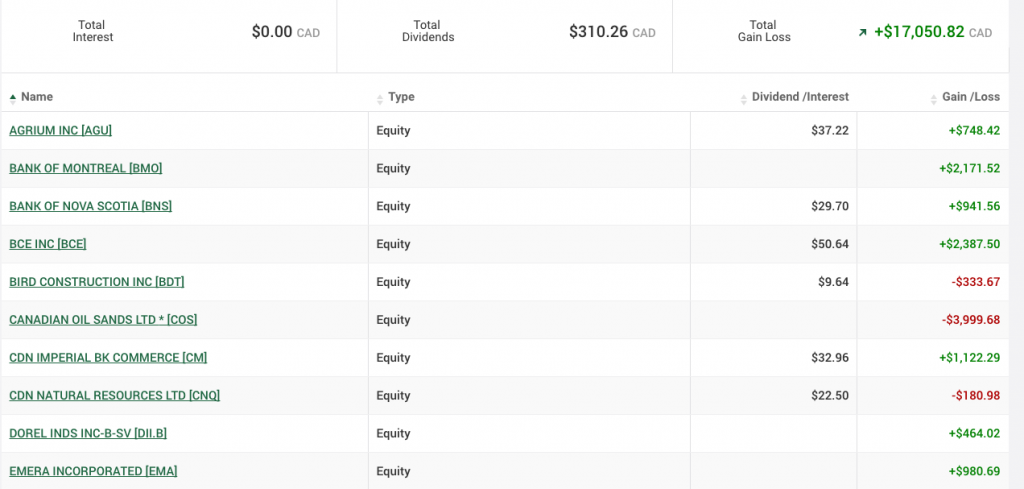

Gain & Loss

Another new and interesting feature in the newly updated TD WebBroker platform is the Gain & Loss section. Orion Szathmary, TD’s manager of investor education, told me that gain and loss reporting gives investors the opportunity to zero in on important information such as dividends and interest, as well as capital gains and losses. You can break this information down by individual security, by account type, or by registered vs. non-registered accounts.

Szathmary explained that when investors decide to sell a stock, for example, that information no longer appears on the main dashboard or holdings screen. Investors lose the ability to see the impact of that stock on their overall portfolio gains or losses. With gain and loss reporting, this information is readily available and easily sortable going back several years.

In the above example, you can see the gains and losses from my RRSP account in the year when I sold my dividend stocks. So now, anytime I get the itch to pick stocks again, I can just view this report and remind myself of the bath I took on Canadian Oil Sands stock in 2015. Problem solved.

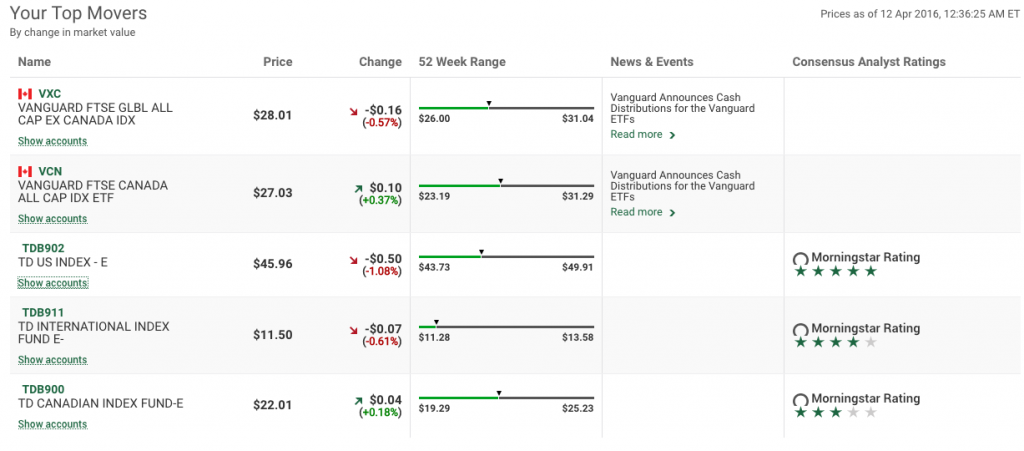

Top Movers

Finally, one section that stood out for me is called Your Top Movers and it sits on the home screen dashboard just below your account breakdown. This report shows you the individual securities that are having the biggest impact on your portfolio by change in market value. It highlights any news or events that may be affecting the security, and shows the current analyst ratings from Morningstar. I could see this snapshot being really useful when I owned dividend stocks and could follow the biggest winners and losers.

Final thoughts on the new TD WebBroker Platform

I’m just a simple index investor, so I know I’ve only scratched the surface of some of the new TD WebBroker features that are now available. Even with its clunky old platform, TD always prided itself on having top-notch research and screening tools. They’ve become more active in investor education – both for beginners and more sophisticated investors. For example, active traders, such as the ones who trade options, have a number of new tools at their disposal, including updated and powerful search features that make it easier to find option contracts.

I’ve become obsessed with transparency and simplicity when it comes to investing and financial planning, and that’s why I was really pleased to see the changes made to the TD Direct Investing WebBroker platform. It allows me to keep tabs on my indexing portfolios, track my performance, and compare them to several relevant benchmarks. The new dashboard gives me an excellent overview of my accounts – just enough to see what’s happening in my portfolio, relative to the market.

I’m not sure if TD, or any online broker for that matter, pays much attention to reviews or rankings in blogs and newspapers. For what it’s worth, I’d give TD’s newly revamped TD WebBroker platform an ‘A’ for overall experience.