When we moved into our new house my wife and I vowed to keep our home clean and clutter-free. We’re not minimalists, exactly, but the last thing we wanted was a basement or garage full of stuff we don’t need or use.

We’ve kept up that promise, for the most part, but as our kids grew up and out of their infant and toddler stages we ended up with a lot of quality items lying around that no longer had a place in our home.

A garage sale or yard sale sounded like a lot of work, and frankly, in today’s digital age, we knew that we could make money selling our stuff online in the secondhand economy.

Related: How I decluttered and simplified my life

A report released earlier this year by Kijiji found that nearly 85 percent of Canadians turned to the secondhand economy to buy or sell an item. Canadians sold 1.85 billion objects in 2015 and earned an average of $883 through those sales. The average amount saved by each Canadian thanks to the secondhand economy was $480.

Of course, we hear a lot about free classified websites like Kijiji and Craigslist, but don’t overlook Facebook as a great place to sell your stuff online. With 1.59 billion monthly active users, plus a proliferation of “Sale Groups”, the social networking giant is a must add when buying and selling items.

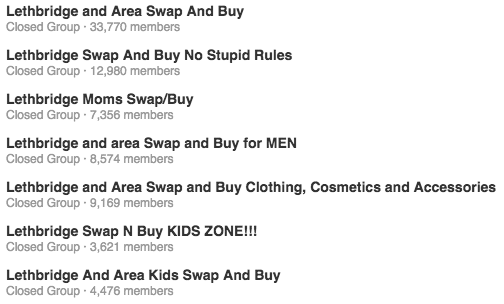

A quick search of “Lethbridge Swap and Buy” on Facebook yielded the following results:

There are almost 34,000 members in the main swap and buy group – not bad for a city of about 100,000 people – plus countless other niche swap and buy groups in the area.

Best ways to sell your stuff online

Consumer expert and secondhand goods connoisseur Kerry Taylor stopped by the Marilyn Dennis show recently to tout the benefits of selling your stuff online – not only on Kijiji, but also through sites like eBay, Etsy, and Shopify:

My wife was determined to unload some of our unused stuff (and earn some extra money in the process) so she made a list of all the items she wanted to sell, cleaned them up and got them ready for sale, then snapped a few pictures of each item.

She researched each of the items online to see if people were looking for them and what they were willing to pay. Once she set the prices she was ready to start selling. She listed a total of 14 items on Facebook and Kijiji and managed to sell every single one of them within seven days. Here were the results:

Facebook vs. Kijiji: Secondhand Economy Smackdown

| Item: | List price: | Sold on: | Sold for: |

| GoPro camera | $250 | Kijiji | $240 |

| Crib and mattress | $200 | $150 | |

| Stroller | $100 | $100 | |

| Sideboard | $90 | Kijiji | $70 |

| Breast pump | $80 | Kijiji | $80 |

| High chair | $75 | $75 | |

| Play yard | $50 | $50 | |

| Diaper bag | $50 | $50 | |

| Nintendo DS | $50 | $50 | |

| Crib bedding | $25 | $25 | |

| Tricycle | $20 | Kijiji | $15 |

| Keyboard | $20 | Kijiji | $20 |

| Swaddlers (x4) | $20 | $15 | |

| Booster seat | $15 | Kijiji | $15 |

Selling stuff on Facebook:

My wife sold a total of eight items and earned $515 using the Lethbridge and Area Swap and Buy group on Facebook.

Pros: There’s always a certain level of anxiety when interacting with a prospective buyer, but most Facebook Swap and Buy groups are closed, meaning you have to request and get approved by a moderator to join the group.

On Facebook you can also ‘creep’ on individual profiles to help you determine whether this is someone you want coming to your home to pick up an item. In a few cases, my wife and the buyer had a mutual friend, which helped ease the comfort level for both the buyer and seller.

You can typically “bump” your listing every 24-48 hours until it sells.

Cons: Nearly everyone is on Facebook, and 1/3 Lethbridge residents are members of the city’s main Swap and Buy group. I realize Facebook is all about oversharing, but you might not want your friends and neighbours to see everything you’re buying and selling online.

Some Facebook groups have rules in place restricting how many items you can list, how often you can post, and even where to display pictures of the item. It’s enough to make the Soup Nazi appear reasonable and lenient.

Buying and selling tip: Facebook groups are great for finding and selling used baby items, including clothes and toys.

Selling stuff on Kijiji:

My wife sold a total of six items and earned $440 using Kijiji free local classifieds.

Pros: When people think of the secondhand economy, Kijiji is the first name that comes to mind. Items can be broken down into specific categories. For example, when searching for baby items you can find things like strollers, high chairs, toys, and even clothing sorted by size.

The Kijiji audience is broad and sellers are more apt to find someone interested in more specific items, such as the keyboard and sideboard that we sold.

Kijiji can also be more private for the seller – unlike Facebook where everyone in your group can see what you’re up to.

Cons: Stranger danger. Interactions between buyers and sellers is anonymous on Kijiji, so there’s always an element of caution when meeting up to exchange money for goods. The anonymity also led to more people ‘flaking out’ and not showing up after messaging about an item.

Sellers can’t “bump” their listing on Kijiji unless they pay a fee to promote it and keep it on the front page. That means your item can quickly get buried in a busy buy and sell category.

Buying and selling tip: Set-up a meeting in a neutral location and make the transaction in a public place. Only accept cash. Don’t give out your home address unless you have to (i.e. the item is too large to transport).

Final thoughts

Our experience with the secondhand economy was positive, using Facebook and Kijiji to get rid of a bunch of items we no longer needed and earning close to $1,000 worth of extra cash in the process.

Related: How I turned a blog into a profitable online business

With a garage sale or yard sale you have to put in a lot of time and effort to set-up and to advertise. There’s always the risk of bad weather and nobody showing up. And the ones who do show up are often looking for a bargain-basement deal, offering you a fraction of the list price on many items.

My wife sold these 14 items on Facebook and Kijiji in seven days with little effort and received a total of $955 out of the $1,045 that she asked for. And she’s not done yet. She’ll continue using the secondhand economy to earn extra money and declutter our home as our kids get older.

Readers: Do you use Facebook or Kijiji to buy and sell stuff online?

It’s always a bit sad when someone unsubscribes from our newsletter, especially when a long-time reader moves on. But I couldn’t help but get a warm feeling this week after receiving a notification that one of our loyal readers unsubscribed:

“You helped inspire me toward retirement with good financial planning over a several year period. I’ve been retired two years now & find many articles no longer interest me. I spend more time reading about my hobbies than money – a good thing! Thank you for the education and information.”

We also get quite a few emails from readers who have passed along our newsletter to their children (or parents!), and for that we are grateful.

There’s always going to be a period in your life when you’re laser-focused on something related to personal finance, whether it’s digging yourself out of debt, preparing for a major event such as a career change, maternity leave, or a move, or as you buckle-down and get ready to retire.

As personal finance bloggers, we’re thrilled to be part of that journey – no matter what age and stage you’re in.

A Boomer & Echo meet-up

Blogging has been a great way for my mom and I to stay close and keep the communication lines open, but with over 800 kilometres separating Kelowna B.C. from Lethbridge, AB, we don’t get a chance to see each other that often.

That’s why it was great to have my mom over to visit and take part in a busy week of activities with our family.

We capped off the week with a trip out to Waterton Lakes National Park – a great way to spend Earth Day on a gorgeous April day in the park with family.

Investing with Wealthsimple

If you’ve been reading Boomer & Echo for a while you’ll know that I’m a big fan of simplifying your finances by investing in a low cost, broadly diversified basket of index funds or ETFs. One of the best ways to do this is by using a robo-advisor – an online automated investing service that takes all of the guesswork out of investing.

We’ve partnered with one of Canada’s leading robo-advisors – Wealthsimple – to offer an incentive where Boomer & Echo readers get a special $50 bonus when they open up a new Wealthsimple account.

This week’s recap:

On Monday I urged readers to shop around for car insurance instead of blindly accepting increases to their premiums every year.

On Wednesday Marie explained the ins and outs of income trusts, including the famous Halloween massacre.

And on Friday Marie outlined a scenario on how to withdraw money from your retirement nest egg.

Remember, you can keep up with the latest articles and tips on Boomer & Echo by subscribing to our newsletter, liking us on Facebook, and following us on Twitter.

Weekend reading:

The Million Dollar Journey blog looks at airport lounge passes and wonders whether this perk is worth the cost.

Dan Wesley at Our Big Fat Wallet describes how he negotiated to waive his annual credit card fee (with Capital One).

Norm Rothery generated a lot of interest in a recent MoneySense article with the hot potato investing strategy – an active twist on the traditional coach potato approach.

John Robertson takes a closer look at the hot potato and says “proceed with caution”.

Speaking of couch potatoes, Dan Bortolotti says target date funds are a reasonable alternative to random mutual funds, but with one caveat: watch the fees.

(In case you missed it: My take on using target date funds inside your RESP).

Jonathan Chevreau says robo-advisors and ETFs prove it’s time for a new financial advice fee structure.

The rise of the most powerful idea in investing – the shift from active to passive investment management.

Did you know: Up to 1.1 million disabled Canadians are eligible for free money from Ottawa?

The skinny basic cable idea is flopping by every measure.

Another iconic musician passed away suddenly when Prince died in his recording studio on Thursday. Here’s a great read on how Prince rebelled against the music industry.

This Esquire piece is worth a read: 4 men with 4 very different incomes open up about the lives they can afford.

The post inspired A Wealth of Common Sense blogger Ben Carlson to write about why personal finance is personal.

This just in: Fancy juice doesn’t cleanse the body of toxins.

“People are interested in this so-called detoxification, but when I ask them what they are trying to get rid of, they aren’t really sure,” said Dr. James H. Grendell, the chief of the division of gastroenterology, hepatology and nutrition at Winthrop-University Hospital in Mineola, N.Y. “I’ve yet to find someone who has specified a toxin they were hoping to be spared.”

The secret shame of middle-class Americans: nearly half would have trouble finding $400 to pay for an emergency.

Helaine Olen can’t sympathize with the article above, which she calls, “A buzzy Atlantic essay details the dire financial straits of a journalist living in the Hamptons. Great work if you can get it!”

This resume for Tesla CEO Elon Musk proves you never, ever, need to use more than one page.

Children as young as five are getting their own debit and credit cards – When kids’ allowance goes digital.

Michael James offers 4 good reasons to pay cash for cars.

Finally, a tech blogger talks about tech fatigue:

At some point, everything new feels old, everything different feels dumb.

Have a great weekend, everyone!

You’ve been saving all your working life and now that you have entered your retirement phase, it’s time to start drawing from your savings. In some circumstances there will be people who will be able to live off their dividends and interest alone. Most retirees, however, will have to start spending the money they have saved.

Once you have decided on the amount of income you need annually for your retirement lifestyle and determined how much of it will come from your guaranteed pensions, the remainder must be withdrawn from your nest egg.

You may have multiple accounts and both registered and unregistered savings. Your investments could be stocks and bonds, ETFs and/or mutual funds. You might be in a position where you must withdraw a minimum amount from your RRIFs.

This example will show you how you can manage your retirement withdrawals, taking the total of all your accounts as a whole. It assumes dividends and interest will be reinvested, but you can use them as part of your yearly cash allotment if you so choose. You just have to adjust as necessary.

A model for retirement withdrawals

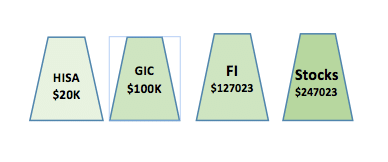

Meet newly retired Rodney and Pamela O’Brien. They have a retirement nest egg totalling $500,000. They have carefully worked out a budget taking into account their desired spending and the regular income they will receive. They have determined that they will require an extra $20,000 throughout the year, which will come from their savings.

The asset allocation the couple is comfortable with is a 50-50 split between cash/income and stocks. They made some adjustments to their portfolio in order to have $20,000 in a High Interest Savings Account, and structured a 5-year GIC ladder to pay out each year thereafter. Their remaining funds are in bond index mutual funds, Canadian dividend stocks and a Global Equity ETF.

Here is their portfolio at the beginning of Retirement Year #1 ($500,000)

Retirement Year #2 ($480,860)

At the beginning of the second year, the couple replenishes the HISA from the first maturing GIC. They now have to rebalance their portfolio. They find that their fixed income has increased to $142,610 and stocks have declined to $238,250. They sell $20,000 worth of fixed income to buy a 5-year GIC and another $2,180 to add to their stocks to maintain their original allocation.

Retirement year #3 ($494,046)

As sometimes happens, the past year was a great one for investment returns. The fixed income increased to $124,765 and the stocks increased to $269,281. This year the O’Brien’s rebalance by selling their stocks – $20,000 buys another GIC, and $8,725 goes towards their fixed income investments. The HISA is replenished with the next maturing GIC.

Retirement year #4 ($543,664)

Again, stocks had a great year and the couple’s stock investments surged to $318,166. Fixed income, however, dropped to $125,498 due to an interest rate increase. They sell some stocks for their new GIC and an additional $26,336 to top up their fixed income.

Retirement year #5 ($451,224)

In the past year stocks took a beating and the O’Brien’s equities dropped to $190,282. However, fixed income was up a bit to $160,282. They can rebalance as shown below, but they also have the option of not replenishing their GIC ladder this year, and even the following year, in hopes that the stock market recovers.

Final thoughts

The O’Brien’s will continue in this manner each year, adjusting their portfolio as necessary to maintain their asset allocation.

The GICs give them to have a good cash cushion that they can draw on in the event of a prolonged drop in the market so they don’t have to withdraw investments at a loss.

This is a simplified example, but it gives you an idea of how you can manage your retirement withdrawals.

If you are at, or close to, this stage I highly recommend you read Daryl Diamond’s Your Retirement Income Blueprint – now in its second edition – which provides detailed strategies to draw down retirement funds and help you to manage your retirement income.