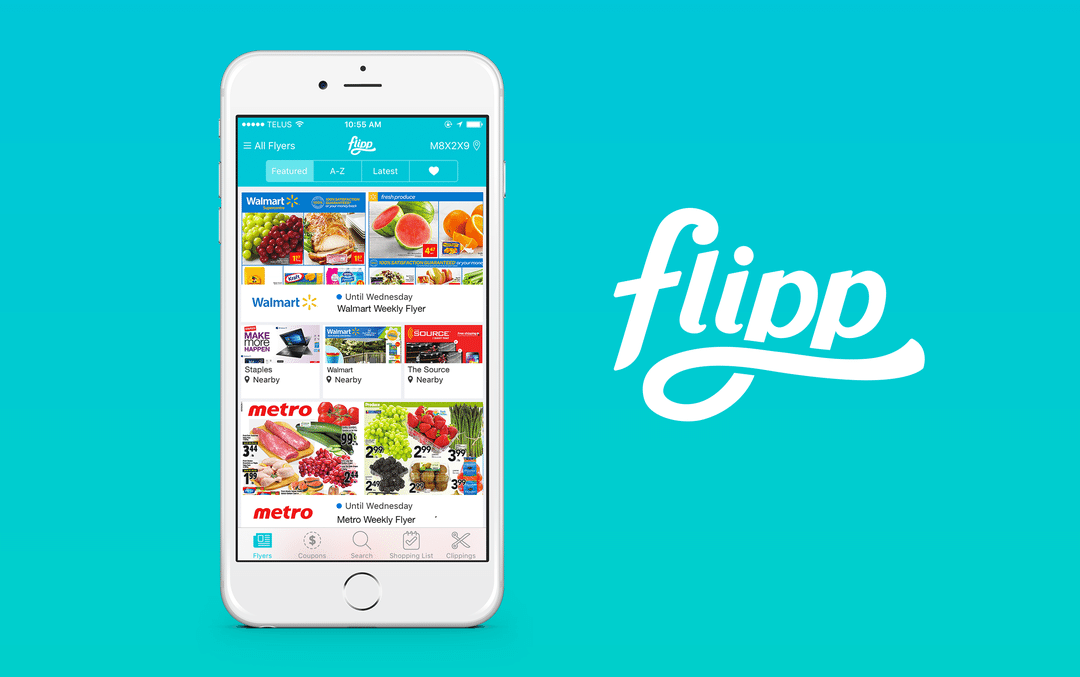

Scanning the weekly flyers and clipping coupons at the kitchen table will soon be a thing of the past as Canadians turn to their smart-phones to save money and find the best deals on groceries. At the forefront are two slick mobile apps – Flipp and Checkout 51 – which are designed to take the pain out of grocery shopping and save consumers time and money in the process.

Flipp and Checkout 51 help save you money on groceries and other household items by finding the best deals and organizing them into an easy to use mobile app. The upshot is that you don’t have to bother sorting and clipping coupons from home, or waste time driving from store-to-store looking for a price match or better deal.

Here’s how these two grocery apps compare:

Flipp vs. Checkout 51

|

|

|

| Origin | Formerly called Wishabi. Founded in 2007 in the GTA by a group of Waterloo graduates. | Founded in August 2012 in Toronto. The app went live to Canadian users in December 2012. |

| Number of users | It currently has more than six million downloads in Canada. | The app has 1.5 million users in Canada. |

| Available | For iOS, Android, plus a desktop version (www.flipp.com) | For iOS and Android, plus a desktop version (www.checkout51.com) |

| How it works | This digital flyer app aggregates 800+ flyers from both national and local retailers to help find the best local deals.

Save money on groceries, household goods, and electronics right at the check out. |

Browse your offers and buy products at any store. Upload your receipt using the Checkout 51 mobile app. They’ll confirm your purchase and credit your account.

When your account balance reaches $20, you can cash out and they’ll mail you a cheque. |

| Unique features | The only shopping app to offer coupon match-ups, which combine flyer deals with brand coupons for even more savings.

Clip flyer items with a single tap and create an in-app shopping list to help plan your weekly shop and stay organized. Once you enter an item into your shopping list, Flipp automatically pulls all the local deals for the item. Want to shop by discount? Use the discount slider to identify the best savings at a glance. |

Buy from any store, snap a photo of the receipt, and get cash back without having to use a single coupon.

New offers are released every Thursday and are valid until Wednesday of the following week. Save money with Checkout 51 offers at any retailer and every major consumer packaged goods brands. The more active member save hundreds, even thousands, of dollars every year. To date, the app has saved shoppers more than $25 million. |

The Verdict:

Saving money on groceries used to involve sorting through flyers, clipping coupons, and driving around from store-to-store looking to price-match. But with grocery apps like Flipp and Checkout 51, shoppers can do all of those things from the palm of their hand. If you want to access your favourite Windows applications on a mobile device, checkout the services from CloudDesktopOnline.com and CloudAppsPortal.com.

The case for Flipp:

Shoppers who are willing to go that extra mile to find the best deal will find Flipp to be the most useful. This app harnesses technology and takes flyer and coupon scanning to the extreme.

Enter your postal code and you’ll find flyers from just about every local retailer, plus coupons for top brands in groceries, baby supplies, health & beauty, and more.

The most unique feature is the shopping list. Enter an item such as cheddar cheese, or chicken breasts, and Flipp quickly scans the local flyers and puts the best deals in front of you to review.

The case for Checkout 51:

If you’re the sort of person who gets excited about a coupon but then forgets to take it with you to the grocery store, you’ll love Checkout 51. No coupons!

Simply scan your weekly offers on your smart phone, highlight the ones you think you’ll use, head to any grocery store, then snap a photo of your receipt to show you purchased those selected items and upload it through the app.

Save 50 cents on bananas, $1 on your favourite cereal, $1.50 on shampoo. Once your savings adds up to $20, Checkout 51 will mail you a cheque. The company says its more active members save hundreds of dollars every year, and to date the app has saved shoppers more than $25 million.

Have you tried a money saving grocery app like Flipp or Checkout 51? Share your experience in the comments below.

Your 70’s is the decade in which you’ll find yourself slowing down somewhat and you may want to simplify your lifestyle. This means your spending will likely slow down too.

Convert your RRSP

You’ve worked hard to build your RRSP. Now it’s time to take your money out.

By the end of the year you turn 71 you must close out your RRSP and convert it into either a RRIF or an annuity. Or, if you want, you can convert a bit to both. There’s no immediate tax consequence. You’ll pay tax only on the payments you receive from your annuity, or on the withdrawals you make from your RRIF.

Option #1 – RRIF

If you want to maintain control of your investments, you may want to put your retirement funds into a RRIF. You can use a RRIF to hold the same types of investments as in a RRSP; in fact you could just convert the existing portfolio. You can no longer make contributions, and you must withdraw a minimum amount each year. This minimum begins at 5.28% of the total in the year after your 71st birthday, and rises to 20% a year when you hit 94.

The downside of a RRIF is your investments may perform badly and, now that you’re not working, it may be impossible for you to recoup those losses to your portfolio. Also, the minimum withdrawal limits may force people with large RRIFs to withdraw more than they really need, thus exposing them to a tax hit.

Related:

To reduce the amount you must withdraw, you can use your spouse’s age at conversion. This can work especially well if your spouse is quite a bit younger.

Option #2 – Annuity

Taking out an annuity can be the most stress free way of turning your savings into a steady stream of retirement income, especially for those worried about outliving their savings. It can supplement CPP and OAS payments and mandatory RRIF withdrawals.

In return for a lump sum, the annuity provides you with regular, guaranteed payments. The amount you pay depends on your age and sex, as well as other factors. Most annuities pay more if your get them later in life.

Annuities come in many forms and they can be complex.

They can be indexed to inflation. You can get one with survivorship so your spouse can still receive payments after you die. Many people worry that if they die within a few years of purchasing an annuity, their heirs will wind up with nothing. For that reason, some annuities have guaranteed payouts for 10 or 20 years.

Once you’ve purchased an annuity, you’re locked in, so it’s vital to investigate them carefully first. Talk with someone who knows the field – and has no vested interest in the product – before you buy.

Annuities are not well suited for everyone, particularly those in poor health or reduced life expectancy.

Retirement home or retire at home?

72% in this age group own their homes

There will likely come a time when you probably won’t be able to physically do as much as you can now, from climbing stairs to shovelling the side-walk and doing home maintenance.

Instead of selling your house you may decide instead to hire a maid service for house cleaning and a lawn-and-garden service to do yard work.

Many seniors find that additional support from family members or from paid home care providers in the family home works better for them. Be realistic, though, about how much help family members can provide.

83% find that paying for at-home care as needed is the most appealing arrangement

You may think of renovating to make your home more senior friendly e.g. walk-in shower or bathtub, grab bars, stair lift, and non-slip flooring.

Renovations may create tax deductions or credits under several federal and provincial programs.

If you don’t want to deal with stairs or maintenance on your large house, you may decide to downsize to a one-level condo or apartment.

Many people move into a retirement home in their late 70’s or early 80’s.

Several helpful directories list retirement homes across Canada.

- www.senioropolis.com – National

- www.thecareguide.com – AB, BC, NS, and ON

- www.seniorshousing.bc.ca – BC

- www.ascha.com – AB

A paid-for-home can be a kind of reserve fund that would help cover high care costs that might arise later in life. You can sell the house to cover costs if you move into a retirement home when you are too frail to live completely on your own. In-home care can be paid from a reverse mortgage or Home Equity Line of Credit.

Plan your legacy

If you haven’t done so already, the 70’s are a good time to plan your financial legacy – giving money to charities or family members. You should think about how to pass on financial assets that you might not need now to your heirs and/or charities while you are still alive.

Make sure your will is up-to date. If you own a business, draw up a succession plan to sell or transfer the business.

Consider how you want to break down any inheritance you want to leave:

- Specific assets you want each child or grandchild to have.

- Amounts to cover specific costs such as university education or contributing to a home purchase.

- Charitable giving.

And, you may want to give away some money now instead of leaving everything to your estate. Make sure you calculate how much you’ll need for your own financial independence going forward.

Setting up trusts can help you pass money on to heirs and charities tax-effectively. For example, a family trust can be a good way to give to children or grandchildren at lower tax rates, while continuing to allow you access to the principle at any time if you need it.

Financial takeaway for your seventies – Simplify your lifestyle and plan your legacy.

Also read:

The last thing I want to do on Easter weekend, or any weekend for that matter, is take a call from work or answer an urgent email from a customer, boss or co-worker. Despite feeling this way I know that many employers want to stay connected with their employees outside of traditional office hours and so I have no problem trading a bit of my freedom to make my employer happy.

But the trade-off of being able to reach me during my spare time is that my employer covers the cost of my cell phone bill.

Fair trade? I think so.

One of the first items I negotiated when I started my current job – aside from my salary – was to get my employer to pay for a new phone and pick up the tab for my monthly cell phone plan.

Fun fact: I’ve carried a cell phone for well over a decade and never spent a dime out of my own pocket on a plan.

When I worked in the hospitality industry, my employer purchased Blackberry’s for the entire sales team and picked up the monthly tab. I didn’t have a cell phone before then, and I’m not sure what kind of phone and plan I’d have now if my current employer didn’t foot the bill.

Some quick math suggests that I’ve saved more than $9,500 over the last 12 years (144 months x $66 per month). That’s $9,500 more dollars to put into my RRSP, or into my kids’ education savings plan.

But I can hear the critics cry out: “What price, freedom?”

Let’s be clear – I don’t get a lot of phone calls or urgent emails to answer after hours. In fact, it’s a pretty rare occurrence.

I’m not a doctor or someone who is on-call and needs to respond at a moment’s notice. More often than not, the questions I get are simple and take only a few minutes to sort out. Then I can get back to spending time with my family, relaxing with a book, or working on my side business.

Final thoughts

Remember that you’ll never get anything if you don’t ask for it or negotiate.

A co-worker overheard me say that I don’t pay for my cell phone plan and got upset because he had to pay out of pocket. We each had a similar role in the organization, but he clearly didn’t ask for the perk and our employer wasn’t going to offer it without being prompted.

If your job (or boss) dictates that you must be available at any time to deal with clients or handle urgent matters, then that’s a great bargaining chip to get your employer to pay for your cell phone plan.

It’s up to you to work out the details – like negotiating that you pay for personal calls, long distance charges, or extra data usage – but the core plan should be the employer’s responsibility.

So go ahead and ask the question: “If staying connected is important to you than why don’t you pick up the cost of my monthly cell phone plan?”