Regular readers know that I update and post my net worth twice a year, including a year-end summary. They should also know that I didn’t post an update at the end of 2022.

It’s not because I’m embarrassed that my portfolio suffered losses for the first time in recent memory. That’s a feature of financial markets, not a bug.

The truth is, I haven’t done a net worth calculation this year because our finances are in a state of flux.

We’re in the process of building a house that doesn’t quite have a final price tag yet. It’s only about 40% complete. We’ve paid two out of five total deposits.

Meanwhile, our house went up for sale this week – but until we accept an offer we won’t know exactly how much it’s worth. We also have planned but unknown expenses due this year, such as realtor commissions, moving expenses, blinds, some furnishings, and landscaping.

A net worth statement is supposed to be a snapshot in time, but our current picture is distorted. Do we own 1.4 houses? Do we use the estimated price of our new house and our existing house, minus the soon-to-be new mortgage? What if our house doesn’t sell for a while?

My expectation is that the picture will clear up in a few months. We’ll move into our new house, sell our existing house, use some of the sales proceeds to cover those planned but unknown expenses, maybe put some money back into our TFSAs, and then assume our new mortgage.

For that reason, I’m putting off the net worth update for year-end 2022 and will post a regular mid-year update at the end of June 2023. By then, we’ll have settled into our new normal and I can give a clearer picture of our financial position.

So, to all of the financial voyeurs out there I say just hang tight for a few more months 🙂

This Week’s Recap:

The Engens got a puppy over the holidays!

This little rascal of a golden retriever is one of the big reasons I haven’t posted here very often over the past three weeks. It’s like having a newborn / toddler all over again!

I did manage to update my beginner’s guide to RRSPs.

And at the start of the year I gave you three investing headlines to ignore in 2023.

Finally, I updated my investing and trading activity for 2022.

DIY Investing Course Coming Soon:

I’ve been talking about this course for months but it’s almost ready to launch (for real!).

I’ve helped hundreds of clients make a successful switch to DIY investing – leaving their expensive mutual funds behind and moving to a self-directed portfolio using a single, risk appropriate asset allocation ETF.

In this video series I explain why you’d want to do that, how to pick the right asset mix, how to pick the right asset allocation ETF, and how to choose a discount brokerage platform.

From there I have platform specific videos for Questrade, Wealthsimple Trade, RBC Direct Investing, and TD Direct Investing (that’s all for now) that take you through opening an account and the appropriate account types, funding the account with new and recurring contributions, how to transfer over your existing accounts to your new self-directed account (without having to break-up with your advisor), and how to buy an ETF.

It’s like me sitting in your living room sharing my laptop screen and walking you through each of these steps in a short, easy-to-follow series of videos.

This just might be a game-changing course for long-time mutual fund investors who understand they’re paying too much for their investment fees but can’t work up the courage to switch to a low cost ETF portfolio.

It’s also good for new investors who want to get started the right way without getting trapped in high fee mutual funds at a bank, or falling for some day-trading, option writing, crypto-pumping, meme-stock trading scam on TikTok.

You’ll be the first to read about the launch of my investing course – so stay tuned!

Weekend Reading:

As we all wait patiently for interest rates to peak and inflation to fall, it seemed inevitable that the global economy was headed for a recession. But unemployment remains historically low and consumers are still spending on goods and services. What if there’s no recession and we get that soft landing after all?

Above average or below? How good of an investor are you?

Between a TFSA and non-registered accounts, what is the most tax-effective way to withdraw to fund retirement?

A double-shot from Ben Carlson. First up, why invest in stocks when bond yields are higher?

And, is it realistic to have 100% of your portfolio in stocks?

Justin Bender updated his model portfolio returns for 2022, including the asset allocation ETFs from Vanguard, iShares, BMO, and Mackenzie:

Andrew Hallam shares what we can learn from the best and worst-performing bond funds of 2022 (plus a look at his own investments).

Michael James on Money updated his 2022 investment returns.

David Booth, founder and chairman of Dimensional Funds, says people have memories, markets don’t. And that’s a good thing.

Mr. Booth also wrote that the poor results of 2022 has been a test on developing a financial plan you can stick with:

“I don’t make predictions, but I do believe in the power of human ingenuity to fix problems big and small, innovating the whole way. What has stayed constant throughout my life is the power of people to make progress in the face of challenges.”

A great post by Andrew Hallam: Like a dose of sugar, the high of buying something ‘better’ soon wears off. Here’s how to actually boost your life satisfaction.

Retired actuary and author Fred Vettese says the best asset mix for retirees has a slightly higher dose of equities at 60% stocks and 40% bonds (subs).

My Own Advisor blogger Mark Seed reflects on income needs and wants in retirement.

Do retirees need to pay for private health insurance? This question is high on the list for many of my retired clients (subs).

Finally, welcome to un-retirement. A year of travelling, volunteering, and – yes – working.

Have a great weekend, everyone!

More than sixty years after the federal government introduced the Registered Retirement Savings Plan as a vehicle to save for the future, RRSPs still remain one of the cornerstones of retirement planning for Canadians.

In fact, as employer pension plans become increasingly rare, the ability to save inside an RRSP over the course of a career can often make or break your retirement.

Here’s a beginner’s guide to RRSPs:

The deadline to make RRSP contributions for the 2022 tax year is March 1, 2023.

Anyone living in Canada who has earned income can and should file a tax return to start building RRSP contribution room. Canadian taxpayers can contribute to their RRSP until December 31st of the year he or she turns 71.

Contribution room is based on 18% of your earned income from the previous year, up to a maximum contribution limit of $29,210 for the 2022 tax year, and $30,780 for the 2023 tax year. Don’t worry if you’re not able to use up your entire RRSP contribution room in a given year – unused contribution room can be carried-forward indefinitely.

Keep an eye on over-contributions, however, as the taxman levies a stiff 1% penalty per month for contributions that exceed your deduction limit. The good news is that the government built in a safeguard against possible errors and so you can over-contribute a cumulative lifetime total of $2,000 to your RRSP without incurring a penalty tax.

Find out your RRSP deduction limit on your latest notice of assessment or online using CRA’s My Account service.

You can claim a tax deduction for the amount you contribute to your RRSP each year, which reduces your taxable income. However, just because you made an RRSP contribution doesn’t mean you have to claim the deduction in that tax year. It might make sense to wait until you are in a higher tax bracket to claim the deduction.

When should you contribute to an RRSP?

When your employer offers a matching program: Some companies offer to match their employees’ RRSP contributions, often adding between 25 cents and $1.50 for every dollar put into the plan. Sadly, many Canadians fail to take advantage of this “free” gift from their employers – giving up a guaranteed 25-to-150% return on their contributions.

When your income is higher now than it’s expected to be in retirement: RRSPs are meant to work as a tax-deferral strategy, meaning you get a tax-deduction on your contributions today and your investments grow tax-free until it’s time to withdraw the funds in retirement, a time when you’ll hopefully be taxed at a lower rate. So contributing to your RRSP makes more sense during your high-income working years rather than when you’re just starting out in an entry-level position.

Related: A sensible RRSP vs. TFSA comparison

A good rule of thumb: Consider what is going to benefit you the most from a tax perspective.

When you want to take advantage of the Home Buyers’ Plan: First-time homebuyers can withdraw up to $35,000 from their RRSP tax free to put towards a down payment on a home. Would-be buyers can also team up with their spouse or partner to each withdraw $35,000 when they purchase a home together. The withdrawals must be paid back over a period of 15 years – if not, the amount is added to your taxable income for the year.

*Note, watch for the new First Home Savings Account coming later this year, an account that allows you to contribute up to $8,000 per year to a lifetime limit of $40,000. Contributions are tax deductible, and withdrawals are tax free if used to purchase a qualified home.

When you want to increase your Canada Child Benefit payments: An RRSP contribution reduces your net income, a measure which is used to determine how much parents will receive from the Canada Child Benefit program. These tax-free benefits are reduced or phased-out at certain income thresholds. Young families should consider making an RRSP contribution to lower their adjusted net family income and get more from the Canada Child Benefit program.

Beware of raiding your RRSP early

Unless it’s a dire emergency then it’s generally a bad idea to withdraw from your RRSP before you retire. For starters, you have to report the amount you take out as income on your tax return. Not to mention you won’t get back the contribution room that you originally used.

To make matters worse, your financial institution will hold back taxes – 10% on withdrawals under $5,000, 20% on withdrawals between $5,000 and $15,000, and 30% on withdrawals greater than $15,000 – and pay it directly to the government on your behalf. That means if you take out $20,000 from your RRSP, you’ll not only end up with just $14,000 but you’ll have to add $20,000 to your income at tax time.

What kind of investments can you hold inside your RRSP?

A common misconception is that you “buy RRSPs” when in fact RRSPs are simply a type of account with some tax-saving attributes. It acts as a container in which to hold all types of instruments, such as a savings account, GICs, stocks, bonds, REITs, and gold, to name a few. You can even hold your mortgage inside your RRSP.

Related: 5 common myths about RRSPs

If you hold investments such as cash, bonds, and GICs then it can make sense to keep them sheltered inside an RRSP because interest income is taxed at a higher rate than capital gains and dividends.

A good approach, depending on your age and stage, is the tried-and-true balanced portfolio consisting of 60% stocks and 40% bonds. You can achieve this mix with one balanced mutual fund, one balanced ETF, or a couple of low cost index funds or exchange-traded funds (ETFs).

Final Thoughts

Contributing to an RRSP is simply one of the best ways for Canadians to save for retirement and reduce their tax burden. The RRSP advantage is further heightened when you consider employer-matching programs, access to the Home Buyers’ Plan, and potentially increasing your Canada Child Benefit payments.

The idea is to contribute to your RRSP in your higher income earning years and withdraw from it in retirement, when income is typically lower. Your contributions, invested sensibly, will grow in a tax-deferred manner until retirement, when withdrawals are fully taxable.

Last year was brutal for both stocks and bonds. In the middle of the year, during what turned out to be the market bottom (and inflation peak) I suggested you stop checking your portfolio. This comes from the analogy that your portfolio is like a bar of soap; the more you touch it the smaller it gets.

The idea that stock and bond prices can fall in the short-term is precisely why investors are rewarded in the long-term. The problem is it’s hard to stick with even the most sensible investment plan because markets are extremely noisy and we almost always feel compelled to act.

I hear this from readers and clients all the time. In the 2010s it was all about the S&P 500. No reason to diversify beyond the top 500 U.S. companies when it’s the best performing index (completely ignoring the previous “lost decade”).

From 2020 to 2021 it was all about the NASDAQ. High-flying tech companies were changing the world and you were missing out if you didn’t add a technology “kicker” to your portfolio.

Investors who didn’t diversify beyond U.S. equities or large-cap technology stocks got a rude awakening last year. The NASDAQ was down 33%. The S&P 500 was down 18%. Meanwhile Canadians stocks were down 8.5% and a global portfolio of stocks was down about 11%.

Now what I’m hearing from readers and clients is that after a year of losses, investors are ready to capitulate and move to GICs. They’re forgetting:

“Investors who focus too much on short-term performance tend to react too negatively to recent losses, at the expense of long-term benefits.”

I don’t have a crystal ball to tell you how to position your portfolio in 2023. Last year I said to lower your expectations for future returns after years of outsized performance. Now the best I can offer is that we can increase our expectations for future returns after both stocks and bonds suffered double-digit losses.

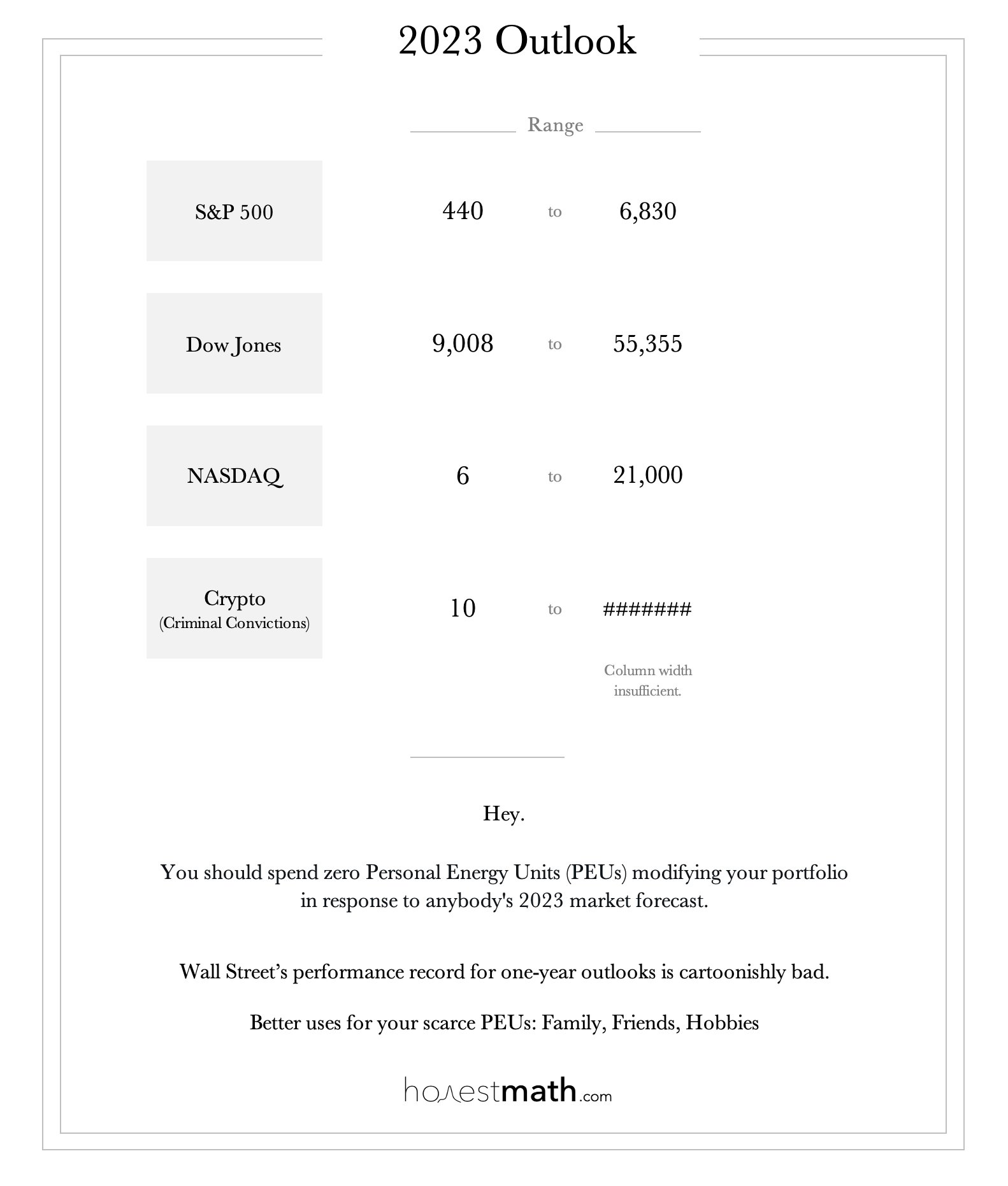

So what should you do? Start by ignoring these three investing headlines this year.

1.) 2023 stock market predictions

Nobody else has a crystal ball either. So why do we eat up these market predictions every year? Besides being nothing more than useless guesses, most predictions invariably go with the current trend.

Last year’s predictions were for the stock market boom to continue (oops!). This year’s predictions are much more pessimistic.

This graphic from the Honest Math website has it right:

2.) Last year’s top performing stock(s) and ETF(s)

Back in the day (I’m talking in the original Wealthy Barber days), investors and their advisors picked investments after combing through performance reports to find last year’s top mutual fund managers and best performing stocks.

But decades of research and data now show this to be a laughably ineffective way to pick investments. Yes, there are a handful of active managers who outperform their benchmark index. The challenge is that it’s impossible to identify them in advance.

The same holds true for individual stocks and actively managed ETFs, or any asset class for that matter. What performed well in the past can quickly revert to the mean with a year of underperformance.

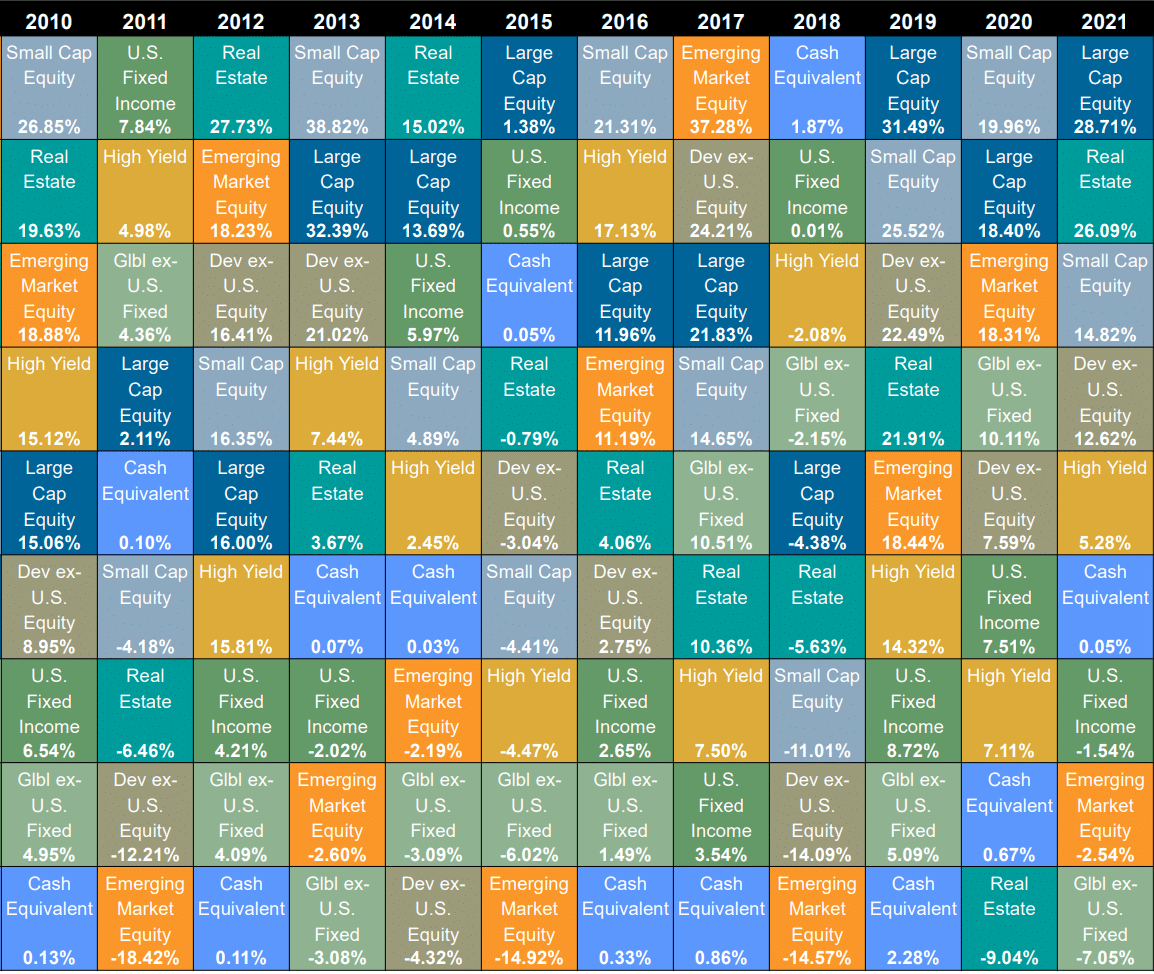

Look no further than the periodic table of investment returns – a brilliant visual on the power of diversification and why performance chasing leads to poor outcomes.

Last year’s winners become this year’s losers, and vice-versa. Making things worse, by the time regular investors shift their portfolios into these winning funds, sectors, or individual stocks, the money has likely already been made.

A better idea is to hold a diversified portfolio of assets so you never have to guess which one will outperform from year-to-year.

3.) What investors need to know today

The Globe and Mail has a long running column called, “what investors need to know today.” I hate it.

It’s great for news junkies who are interested in quarterly earnings reports, IPOs, mergers and acquisitions, inflation expectations, etc. But regular investors don’t *need* to know anything on a daily basis to maintain a sensible portfolio.

One of the main reasons I invest in Vanguard’s All Equity ETF is so that if I pulled a Rip Van Winkle and slept for two decades I could be reasonably confident that I’d end up with a good outcome from my investments.

What can a regular investor glean from a daily newspaper column that might give him an edge trading stocks with professional money managers and computer algorithms? Information is quickly baked into a company’s share price, so unless you have some type of insider knowledge you’re trading on the same information as everyone else. Not helpful.

What investors need to know today circles back to my original point at the top of this article. Stop checking your portfolio so often. Diversify broadly so you get a tighter dispersion of returns rather than the up-and-down roller coaster ride from year-to-year.

And stop chasing performance. Recognize that reversion to the mean will happen. Years of outperformance should lower your expectations for future returns. Similarly, a year of truly bad performance should increase your expectations for future returns.

Again, I don’t know what will happen in 2023, but I’m optimistic that stocks and bonds will have good future returns after a brutal year in 2022.