While investment firms and regulators continue debating over issues like fee disclosure, advisor conflict of interest, and a standard of care for investors, a new breed of investing services has put the industry on notice by bringing low cost investing to the masses. Last year I reviewed the new robo-advisor entrants, but since then Questrade has got in on the act with its long-awaited Portfolio IQ, a solution billed as “Canada’s only online wealth-management service”.

Questrade Portfolio IQ caters to individual clients by assessing their risk tolerance and suitability before creating a personalized portfolio.

Here’s how it works:

Investors can start with as little as $1 and pay no fees until their account reaches $2,000. Your portfolio is charged a percentage of its total annual value in management fees – applied quarterly. The percentage drops as your portfolio grows.

Questrade Portfolio IQ combines the total value of all your managed accounts – including accounts within your household – to give you the potential to jump to a lower fee faster.

Pricing:

| Asset range | Management fee (annual fee, billed quarterly) |

| Less than $2,000 | Your money will be held as cash, with no fees or penalties |

| $2,000 – $100,000 | 0.7%, $99.95 minimum |

| $100,000 – $250,000 | 0.6% |

| $250,000 – $500,000 | 0.5% |

| $500,000 – $1,000,000 | 0.4% |

| $1,000,000+ | 0.35% |

Model portfolios:

Portfolio IQ offers five types of model portfolios, ranging from aggressive growth to conservative income.

- Aggressive growth – The aggressive growth portfolio is comprised of 100% equity ETFs (35% International, 32% Canadian, and 31% U.S.), aiming to deliver maximum long-term growth potential. The average-weighted MER is between 0.29% and 0.47%.

- Growth – The growth portfolio has a greater concentration of equity ETFs at 80% (28% International, 26% U.S., and 28% Canadian) of the portfolio with 20% invested in fixed income ETFs providing a moderately higher risk level with emphasis on long-term growth. The average-weighted MER is between 0.29% and 0.45%

- Balanced – The balanced portfolio has a target mix of 40% fixed-income and 60% equity ETFs (21% International, 20% Canadian, and 19% U.S.) and an emphasis on growth. The average-weighted MER is between 0.29% and 0.42%.

- Income – The income portfolio invests 60% in fixed income ETFs while including 40% equity ETFs (14% International, 13% U.S., 13% Canadian), blending the potential for growth with an emphasis on steady income. The average-weighted MER is between 0.29% and 0.39%.

- Conservative Income – By investing 80% in fixed income ETFs and 20% in equity ETFs (14% International, 6% Canadian) the income portfolio works to preserve your money, while minimizing exposure to market volatility. The average-weighted MER is between 0.29% and 0.36%.

Holdings:

Portfolio IQ only uses ETFs, with expense ratios as low as 0.04%, and a management fee with zero trailing commissions.

Related: The ins and outs of ETFs

Because you hold the shares of the ETF, you have your own cost base. This can be more tax efficient and allow tax loss harvesting to offset taxes on capital gains.

Rebalancing:

Your portfolio is rebalanced on an ongoing basis to keep it working at peak performance. There is no extra charge for rebalancing, and the portfolio managers will take advantage of tax-loss harvesting.

Availability:

Questrade’s Portfolio IQ is open to all Canadians.

Final thoughts on Questrade Portfolio IQ

Questrade is best known for offering rock-bottom commissions for trading stocks ($4.95) as well as commission-free purchases for any ETF in North America. It’s great to see Questrade rollout a low-cost online wealth management service that is accessible (and scalable) for all Canadian investors.

What are your thoughts on the new offering from Questrade?

Scotia’s Momentum Visa Infinite card is the cash back rewards king in Canada and right now for a limited time when you sign up for the card you’ll get a free $100 gift card upon approval.

This is the go-to rewards card for all of my grocery and gas spending (4% cash back), as well as for drug store spending and recurring bill payments (2% cash back). As an added bonus, the $99 annual fee is waived in the first year.

For the $100 gift card you can choose between Amazon, Starbucks, Future Shop, or the Ultimate Dining card – which includes Swiss Chalet, Montana’s, Kelsey’s, Harvey’s or Milestones.

Travel rewards fans can get in on the act as well with the Scotiabank Gold American Express card, which pays 4x points on groceries, gas, dining, and entertainment spending. The $99 annual fee is waived in the first year.

The $100 gift card promotion doesn’t come around often, so if you’re in the market for a new rewards card you should take advantage of this offer today.

This week’s recap:

On Monday I posted my 2014 portfolio rate of return and announced the switch from dividend stocks to my two-fund indexing solution.

On Wednesday Marie asked what was lurking inside your fridge and cabinets with this guide to expiry dates.

On Friday Marie posted a primer on how to get started with a portfolio of index funds.

Over on Rewards Cards Canada I explained how to get top value from your rewards program.

I was happy to contribute to this article by Melissa Leong on nine must-have (and free) financial apps for 2015.

Marie was equally thrilled to share her thoughts on this Gail Johnson column on how to deal with rising interest rates.

Weekend Reading:

Dan Bortolotti has updated the model portfolios on his Canadian Couch Potato blog. Simplicity was the driver behind these changes – no more REITs, real return bonds, or small cap stocks.

Another solid primer – this time by Bridget Casey – on how to build a balanced portfolio using index funds.

Here’s a sad look at how NHL defenseman Jack Johnson was screwed by his parents and left with millions in debt.

Million Dollar Journey continued its series of Net Worth updates from various readers – this one from Nobleea, an oil and gas engineer from Edmonton.

Ever wonder how much money you’ve made over the course of your career? This blogger looked back at the jobs she’s held over the last decade.

Sandi Martin at Spring Personal Finance reveals what she wants from you in 2015.

Stephen Weyman from How To Save explains how to get the most out of your new car warranty.

Financial Uproar’s Nelson Smith takes a look at who should buy life insurance and why.

One of the most colourful personal finance bloggers is J. Money from Budgets are Sexy. He was recently featured in this Forbes article about how he socked away $400,000 in seven years.

Here’s a look at how J. Money saves money…(in pictures).

I took out an RRSP loan last year to catch up on some unused contribution room. Here, Dan Wesley explains the positive and negatives of RRSP loans.

Mark Seed explores what it takes in order to transition from working to retirement.

Michael James on Money uses a clever example to explain why it’s better for investors to use a limit order instead of a market order.

Michael Kitces wonders if the DALBAR study overstates the behaviour gap (the difference between investment returns and investor returns).

Steadyhand’s Tom Bradley says no one can predict the future – not even financial advisors.

And finally, Preet Banerjee continues his video blogging exploits with this analysis that questions how much you actually make when you sell your house:

Have a great weekend, everyone!

“I’m interested in investing but I don’t really understand how to get started. Could you please explain how to begin investing in index funds?”

The work involved in learning about investing may seem overwhelming when you have no idea how to begin.

The following is a primer on how to get started investing with an index portfolio.

How to get started with an index portfolio

The absolute simplest way to start is to go to your bank and open up a mutual fund account. You will be asked to complete a “Know Your Client” questionnaire to determine your investment knowledge, time frame and risk tolerance.

You will strongly explain to the advisor that you want to purchase index funds. All banks have their version of index funds that are quite similar and will give an investor plenty of diversity. Minimum initial purchases are as low as $100 (TD) or $500 (the other banks).

Related: Why TD e-Series funds aren’t just for beginners

A typical conservative asset allocation is 40% fixed income and 60% equities. As a young investor saving for the long term, you may want to increase the equity portion – 25% in each of Fixed Income, Canadian Equity, US Equity and International Equity is a common allocation.

The best way to grow your portfolio is by setting up an automatic savings plan. The minimum amount is usually only $25 per fund but you will want to increase this amount as soon as you are able.

Mutual funds are user friendly and there are no commissions to buy or sell, which makes it cost effective when you need to rebalance your portfolio.

Balanced Index Funds

If you can only invest a small amount to start with, or don’t want to bother with rebalancing a three-to-four asset portfolio you can purchase a single balanced index fund.

A balanced index fund is a diversified assortment of Canadian bonds and stocks with some US and International stocks mixed in. It is a good option for new investors. The fund is automatically rebalanced quarterly.

TD has a version of a balanced index fund that must be purchased at a branch.

Tangerine Investment Funds (formerly ING Streetwise funds) allow you to open an account online. www.tangerine.ca – just follow the steps.

What about ETFs?

You can build a low cost portfolio with ETFs, but it takes a little more time and effort.

ETFs have been a widely promoted alternative to mutual funds because of their low management fees, but the savings can be quickly eroded if you are not careful.

To purchase ETFs you need to open an account with a discount brokerage. You can use the brokerage arm of your bank or a low fee alternative such as Questrade. Take a look at the fees before you open an account.

- Some require a minimum amount to set up an account of $1,000 – $10,000.

- Self Directed RRSP accounts have annual fees of $50 – $100 if assets are less that $15,000 to $25,000.

- Trading fees can be as little as $4.95 to as much as $29 on accounts less than $50,000.

If your brokerage charges for each purchase it is more suitable for larger lump sum ETF purchases.

Some brokerages such as QTrade, Questrade, Scotia iTrade and Virtual Brokers have ETFs available commission free which is an advantage for regular monthly purchases. However, they may have a limited number of ETF options, or charge a commission to sell.

Now that you have opened a brokerage account it’s time to choose your ETFs.

The largest companies that sell ETFs in Canada are iShares, Vanguard, BMO and Horizons. They each have dozens of ETF options to choose from.

Related: A two-fund investing solution

For low cost, stick with cap-weighted indexes that track indexes such as S&P/TSX, S&P 500, MSCI, EAFE and DEX Universal Bond. As with index mutual funds you can choose a single balanced ETF, or 3 to 4 separate asset classes.

As I mentioned this will take more research, but once it’s set up there will not be much maintenance involved.

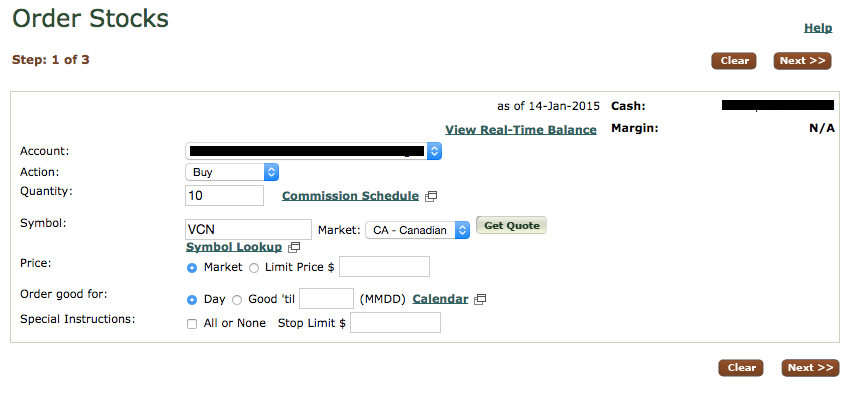

Once you have chosen your funds take note of the three-letter trading symbol because it’s time to buy. Unlike mutual funds where you normally purchase by dollar amount, ETFs are purchased as shares. You can buy as little as one share.

Enter your three-letter trading symbol and the stock exchange. Some are specific – TSX. Others just want the country – Canada.

Get a quote – the ask price. Use the market price for now. (Read this post for more information on using limit orders.)

Determine how many shares you want – and click enter.

Follow the steps until the order is confirmed and make note of the order number.

If you have a problem you can call customer service for help. Once you’ve placed a few trades your confidence will grow.

Resources

To learn everything you ever wanted to know about index investing, read The Little Book of Common Sense Investing by John C. Bogle, the creator of Vanguard.

Also check out John Robertson’s, The Value of Simple: A Practical Guide to Taking the Complexity Out of Investing – a plain language guide to investing for Canadians.

Canadian Couch Potato has a lot of good information, like how to choose your asset allocation as well as sample portfolios.

You can get a comparison of brokerages at MoneySense (or visit your local library and check out the May, 2014 edition.)

Money Smarts Blog has another good brokerage comparison.

And don’t forget Rob Carrick’s annual ranking of online brokers.

In conclusion

Congratulations, you’ve become an investor. As a new investor you will be tempted to check out your funds on a daily basis to see how they’re doing. If they go up, you’ll be elated. If they go down, you’ll be in despair.

What if the price goes down several days – or even weeks – at a time? What will you do? You will do – nothing! Short-term performance is irrelevant to your long-term plan.

Related: What are you doing with this stock market pullback?

Success comes from sticking with a well-chosen portfolio, having realistic goals and, above all, contributing regularly to your savings plan.

And that’s how you become a successful investor.